Hot Features

Hot Features

Mergers and acquisitions are one growth strategy leading brands adopt to stay ahead in their industry – but how do they come about, and what impact do they have? Let’s look at some high-profile mergers across different industries.

In supermarkets: Sainsbury’s and Asda

The proposed merger between UK supermarkets Asda and Sainsbury’s has recently been making the headlines. That’s largely because in the UK, supermarkets are very close to the hearts of many of the population who tend to show great loyalty to the place where they usually shop. With such a high level of brand sentiment, and as a result, each brand has a fairly clear demographic that they appeal to in particular.

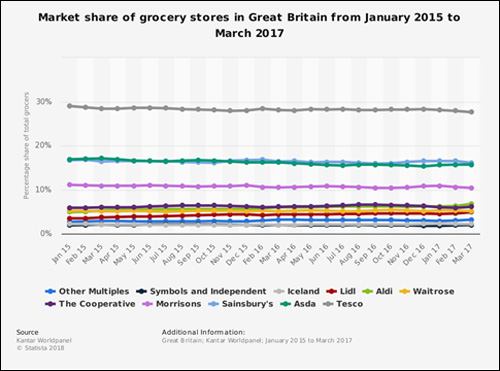

Until a few years ago it was pretty much a four-way split in the supermarket sector with the main players being Asda, Sainsbury’s, Tesco and Morrisons. But then the so-called discount brands Aldi and Lidl started appearing on the scene and three of the big four started to see their market share decline.

While Morrisons continue to go it alone and maintain a market share between 2016 and 2017 of a little over 10%, the other three chains have reacted by announcing high profile mergers, including the proposed coming together of Sainsbury’s and Asda in a £51 billion deal. Tesco, meanwhile, had already taken over the wholesaler Booker in a deal worth £4 billion, a move which put even more pressure on the other two to keep up.

Under their proposed merger Sainsbury’s will be effectively taking over Asda and will be firmly in the driving seat with a 58% stake compared the 42% to be held by Asda’s owners, Walmart.

There are a number of reasons why, on paper, this particular merger is destined to revive the fortunes of both businesses. The first is geographical. Asda, whose headquarters is in Leeds, are traditionally strong in Scotland and the north of England while Sainsbury’s are predominantly a southern business. They also appeal to two very different demographics so are not considered to be in any direct competition with each other.

The real motivation to merge, perhaps, comes from the combined buying power that they hope it will give them. Sainsbury’s have estimated that this could amount to savings of up to £500 million a year. It will also give them a combined market share of 32%, comfortably beating Tesco’s 28%.

But, as with all mergers of this size, it will not be plain sailing to complete it. That’s because it will need to be approved by the Competition and Markets Authority (CMA) before it can go ahead and they will need to be convinced that consumer choice will not be compromised. So it’s very possible that they may insist on the disposal of some stores, just as they did when the Co-Op acquired My Local stores in 2016 and insisted that the former dispose of two stores in Widnes, Cheshire.

In Engineering: GKN and Melrose Industries

Of course, mergers and acquisitions don’t just happen in the supermarket industry – and it’s not only the CMA that can affect their progress. Take, for example, the recently completed acquisition of the UK engineering business GKN by Melrose Industries.

GKN makes components for cars and aircraft and issued a profits warning to its shareholders in 2017. Melrose is a business that specialises in turning around ailing companies and saw the opportunity to snap them up for £8.1 billion.

Initially GKN resisted the bid and conducted a campaign to encourage shareholders to reject the offer by promising a share in $2.5 billion as well as to join up with the US company Dana to create a more profitable car parts division. There were even appeals to the UK Government to intervene, however the deal duly went ahead. But even before the dust has settled Melrose have been dealt a blow by the resignation of Phil Swash, the head of GKN’s automotive arm. Swash had previously predicted that, under his leadership, he could get annual sales to leap from £33 million to £500 million by 2022.

In gambling: Rank, 888 Holdings and William Hill

GKN had hoped, unsuccessfully, that it would be shareholder power that would put a stop to the acquisition. But one merger that was derailed in this way was the 2016 negotiation when the UK betting firm William Hill was being pursued by two rivals, Rank and 888 Holdings.

Although they were offering £3.2 billion, one of the reasons cited for the failure of the bid was that a leading William Hill shareholder believed it was undervaluing the company. At the time this was to be the latest of a long line of mergers in the gambling sector as operators were seeking to create mega-companies capable of seeing off the competition. The fact that Rank and 888 Holdings are still doing well in a very competitive market, despite the merger not going ahead, is undoubtedly being noted by other operators in the sector who – as a result – may well be considering the continuing advantages of going it alone. One of these upcoming independent operators is Roseslots, which specialise in slot games for older female gamblers. There aren’t many gambling companies who set out with the aim of catering specifically for older females with an interest in online slots, this is beneficial to them when it comes to going it alone and avoiding a merger. Mergers are generally seen as irreversible, so new entrants such as Roseslots might be wise to avoid merging with others in the industry too early.

In retail: The Carlyle Group and Accolade

Naturally, not all mergers or acquisitions are carried out with one or other partner determined to resist the overtures of the other. In some cases they make logical and business sense – as well as being able to bring together complementary features. One such example is the recent takeover in Australia of Accolade by The Carlyle Group. The former is the biggest wine company by volume in Australia and Great Britain whose labels include Echo Falls and Banrock Station. American private equity firm, The Carlyle Group, acquired them for Aus$1 billion and the aim is that the winemaker will now be able to fully exploit the free trade agreement that was agreed 2015. This agreement reduces tariffs from 20% to 3% on Australian wine entering China from 20% to just 3%. Even now, Accolade estimate their exports could increase up to 80% by the end of this year because of this acquisition.

In an increasingly global marketplace it seems very likely that we’ll be seeing many more of these kinds of mergers and acquisitions, as combine forces to survive and flourish in their industries. Some will include the features that ensure success, while others may not – but all are certain to make headlines in the financial pages.

So long as their markets remain competitive, perhaps the biggest beneficiaries of these mergers and acquisitions will be consumers themselves, who – with improved efficiency of the companies they’re buying from – could stand to gain better products and improved value for money.