We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Share Name | Share Symbol | Market | Type |

|---|---|---|---|

| Grayscale Horizen Trust (QX) | USOTC:HZEN | OTCMarkets | Common Stock |

| Price Change | % Change | Share Price | Bid Price | Offer Price | High Price | Low Price | Open Price | Shares Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|---|---|

| 1.98 | 33.28% | 7.93 | 7.30 | 7.93 | 7.93 | 5.95 | 5.9973 | 83,420 | 21:01:47 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _____ to ______

Commission File Number

SPONSORED BY GRAYSCALE INVESTMENTS, LLC

(Exact Name of Registrant as Specified in Its Charter)

(State or Other Jurisdiction of |

(I.R.S. Employer |

|

|

(Address of Principal Executive Offices) |

(Zip Code) |

(

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(g) of the Act:

|

|

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

N/A |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

☐ |

Accelerated filer |

☐ |

|

|

|

|

☒ |

Smaller reporting company |

||

|

|

|

|

|

|

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

Aggregate market value of registrant’s Shares held by non-affiliates of the registrant, based upon the closing price of a Share on March 31, 2024 as reported by the OTC Markets Group Inc. on that date: $

Number of Shares of the registrant outstanding as of November 18, 2024:

DOCUMENTS INCORPORATED BY REFERENCE:

f

i

Industry and Market Data

Although we are responsible for all disclosure contained in this Annual Report on Form 10-K, in some cases we have relied on certain market and industry data obtained from third-party sources that we believe to be reliable. Market estimates are calculated by using independent industry publications in conjunction with our assumptions regarding the Horizen industry and market. While we are not aware of any misstatements regarding any market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the headings “Forward-Looking Statements” and “Item 1A. Risk Factors” in this Annual Report.

Forward-Looking Statements

This Annual Report on Form 10-K contains “forward-looking statements” with respect to the financial conditions, results of operations, plans, objectives, future performance and business of Grayscale Horizen Trust (ZEN) (the “Trust”). Statements preceded by, followed by or that include words such as “may,” “might,” “will,” “should,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “potential” or “continue,” the negative of these terms and other similar expressions are intended to identify some of the forward-looking statements. All statements (other than statements of historical fact) included in this Annual Report that address activities, events or developments that will or may occur in the future, including such matters as changes in market prices and conditions, the Trust’s operations, the plans of Grayscale Investments, LLC (the “Sponsor”) and references to the Trust’s future success and other similar matters are forward-looking statements. These statements are only predictions. Actual events or results may differ materially from such statements. These statements are based upon certain assumptions and analyses the Sponsor made based on its perception of historical trends, current conditions and expected future developments, as well as other factors appropriate in the circumstances. Whether or not actual results and developments will conform to the Sponsor’s expectations and predictions, however, is subject to a number of risks and uncertainties, including, but not limited to, those described in “Part I. Item 1A. Risk Factors.” Forward-looking statements are made based on the Sponsor’s beliefs, estimates and opinions on the date the statements are made and neither the Trust nor the Sponsor is under a duty or undertakes an obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, other than as required by applicable laws. Investors are therefore cautioned against relying on forward-looking statements. Factors which could have a material adverse effect on the Trust’s business, financial condition or results of operations and future prospects or which could cause actual results to differ materially from the Trust’s expectations include, but are not limited to:

ii

Unless otherwise stated or the context otherwise requires, the terms “we,” “our” and “us” in this Annual Report refer to the Sponsor acting on behalf of the Trust.

A glossary of industry and other defined terms is included in this Annual Report, beginning on page 106.

This Annual Report supplements and where applicable amends the Memorandum, as defined in the Trust’s Amended and Restated Declaration of Trust and Trust Agreement, for general purposes.

iii

Table of Contents

Item No. |

|

Item Caption |

|

Page |

PART I |

|

|

|

|

Item 1. |

|

|

1 |

|

Item 1A. |

|

|

50 |

|

Item 1B. |

|

|

85 |

|

Item 1C. |

|

|

85 |

|

Item 2. |

|

|

85 |

|

Item 3. |

|

|

86 |

|

Item 4. |

|

|

86 |

|

PART II |

|

|

|

|

Item 5. |

|

|

87 |

|

Item 6. |

|

|

87 |

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

88 |

Item 7A. |

|

|

96 |

|

Item 8. |

|

|

96 |

|

Item 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

96 |

Item 9A. |

|

|

96 |

|

Item 9B. |

|

|

97 |

|

Item 9C. |

|

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

|

97 |

PART III |

|

|

|

|

Item 10. |

|

|

98 |

|

Item 11. |

|

|

99 |

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

99 |

Item 13. |

|

Certain Relationships and Related Transactions and Director Independence |

|

100 |

Item 14. |

|

|

102 |

|

PART IV |

|

|

|

|

Item 15. |

|

|

103 |

|

Item 16. |

|

|

105 |

|

|

|

106 |

||

iv

PART I

Item 1. Business

Overview of the Trust and the Shares

Grayscale Horizen Trust (ZEN) (formerly known as Horizen Investment Trust) (the “Trust”) is a Delaware Statutory Trust that was formed on July 3, 2018 by the filing of the Certificate of Trust with the Delaware Secretary of State in accordance with the provisions of the Delaware Statutory Trust Act.

The Trust’s purpose is to hold Horizen (“ZEN”). The Horizen Network, an alternative software implementation of the Bitcoin, network was created in 2017 by a group that forked Zclassic, which is a clone of Zcash. Although the Horizen Network is similar to the Bitcoin Network, there are several key differences between the Horizen Network and the Bitcoin Network. Historically, the fundamental difference between the Bitcoin Network and the Horizen Network was that the Horizen Network offered selective privacy-preserving features. However, the Horizen Network implemented an update in September 2023 that removed many of these privacy preserving features, as described below. In addition, the Bitcoin Network uses the SHA-256 algorithm, which is preferred for parallel processing, but is also easily used to build application-specific integrated circuits (ASICs) to mine the network more efficiently. In contrast, the Horizen Network employs the Equihash algorithm. Horizen has a current block size of 2MB, compared to the variable block size of the Bitcoin Network, which has a limit of approximately 4MB. Horizen blocks are also generated every 2.5 minutes, which is approximately four times faster than Bitcoin’s block production. Horizen halvings occur every 840,000 blocks, unlike Bitcoin’s halvings that occur every 210,000 blocks. The Horizen mining difficulty is also roughly one three-millionth of Bitcoin’s, making it significantly easier to mine blocks and earn rewards. Additionally, Horizen and Bitcoin both have a maximum supply of 21 million coins. As of September 30, 2024, Horizen had a circulating supply of approximately 15.5 million coins, which was less than Bitcoin’s circulating supply of approximately 19.8 million coins. As of September 30, 2024, the 24-hour trading volume of Horizen and Bitcoin were approximately $3.5 million and $15.4 billion, respectively. As of September 30, 2024, the aggregate market value of Horizen was $124.9 million, as compared to the $1,251.5 billion aggregate value of Bitcoin. As of September 30, 2024, ZEN was the 314th largest digital asset by market capitalization as tracked by CoinMarketCap.com.

The Horizen Network is one of a number of projects intended to enhance blockchain technology. One of the Horizen Network’s primary enhancements of the blockchain was to add additional layers of confidentiality to traditional blockchain infrastructure so that users could engage in transactions and selectively disclose details related to those transactions. ZEN accomplished this level of confidentiality by using novel cryptographic protocols called Zero-Knowledge Succinct Non-Interactive Argument of Knowledge (“zk-SNARKs”) to protect both the amount and the sender and recipient of the transaction. The result was a confidential transaction known as a “shielded” transaction, which was distinct from a public transaction on the Horizen Network, known as an “unshielded” transaction. From the inception of the Horizen Network through September 30, 2022, approximately 22% of Horizen transactions had been unshielded, approximately 4% involved one party utilizing a shielded address, and approximately 74% involved both parties utilizing a shielded address. However, in September 2023, the Horizen protocol implemented an update intended to deprecate these privacy shields, with the intent of causing it to no longer be considered a “privacy coin,” and, following the update, the Horizen Network no longer supported transactions from unshielded addresses to shielded addresses. See “—Overview of the ZEN Industry and Market” for additional information on the Horizen Network’s historical selective privacy-preserving features and recent upgrades.

As of September 30, 2024, the Trust holds approximately 3.8% of the ZEN in circulation. The size of the Trust’s position does not itself enable the Sponsor or the Trust to participate in or otherwise influence the development of the Horizen Network. As a decentralized digital asset network, the Horizen Network consists of several stakeholders, including core developers of ZEN, users, services, businesses, miners and other constituencies, of which the Trust is only one constituent. Furthermore, in contrast to other protocols in which token holders participate in the governance of the network, ownership of ZEN confers no such rights.

On January 11, 2019, the Trust changed its name from Horizen Investment Trust to Grayscale Horizen Trust (ZEN) by filing a Certificate of Amendment to the Certificate of Trust with the Delaware Secretary of State. The Trust issues common units of fractional undivided beneficial interest (“Shares”), which represent ownership in the Trust, on a periodic basis to certain “accredited investors” within the meaning of Rule 501(a) of Regulation D under the Securities Act of 1933, as amended (the “Securities Act”) in exchange for deposits of ZEN. The Shares are quoted on OTC Markets Group Inc.’s OTCQX® Best Market (“OTCQX”) under the ticker symbol “HZEN.”

Grayscale Investments, LLC is the sponsor and administrator of the Trust (the “Sponsor”), CSC Delaware Trust Company is the trustee of the Trust (the “Trustee”), Continental Stock Transfer & Trust Company is the transfer agent of the Trust (in such capacity, the “Transfer Agent”) and Coinbase Custody Trust Company, LLC is the custodian of the Trust (the “Custodian”).

The Trust issues Shares only in one or more blocks of 100 Shares (a block of 100 Shares is called a “Basket”) to certain authorized participants (“Authorized Participants”) from time to time. Baskets are offered in exchange for ZEN. At this time, the Sponsor is not operating a redemption program for the Shares and therefore Shares are not redeemable by the Trust. Due to the lack of an ongoing redemption program as well as price volatility, trading volume and closings of Digital Asset Trading Platforms due to fraud, failure, security breaches or otherwise, there can be no assurance that the value of the Shares will reflect the value of the Trust’s ZEN, less the Trust’s expenses and other liabilities, and the Shares may trade at a substantial premium over, or a substantial discount to, the value of the Trust’s ZEN, less the Trust’s expenses and other liabilities.

1

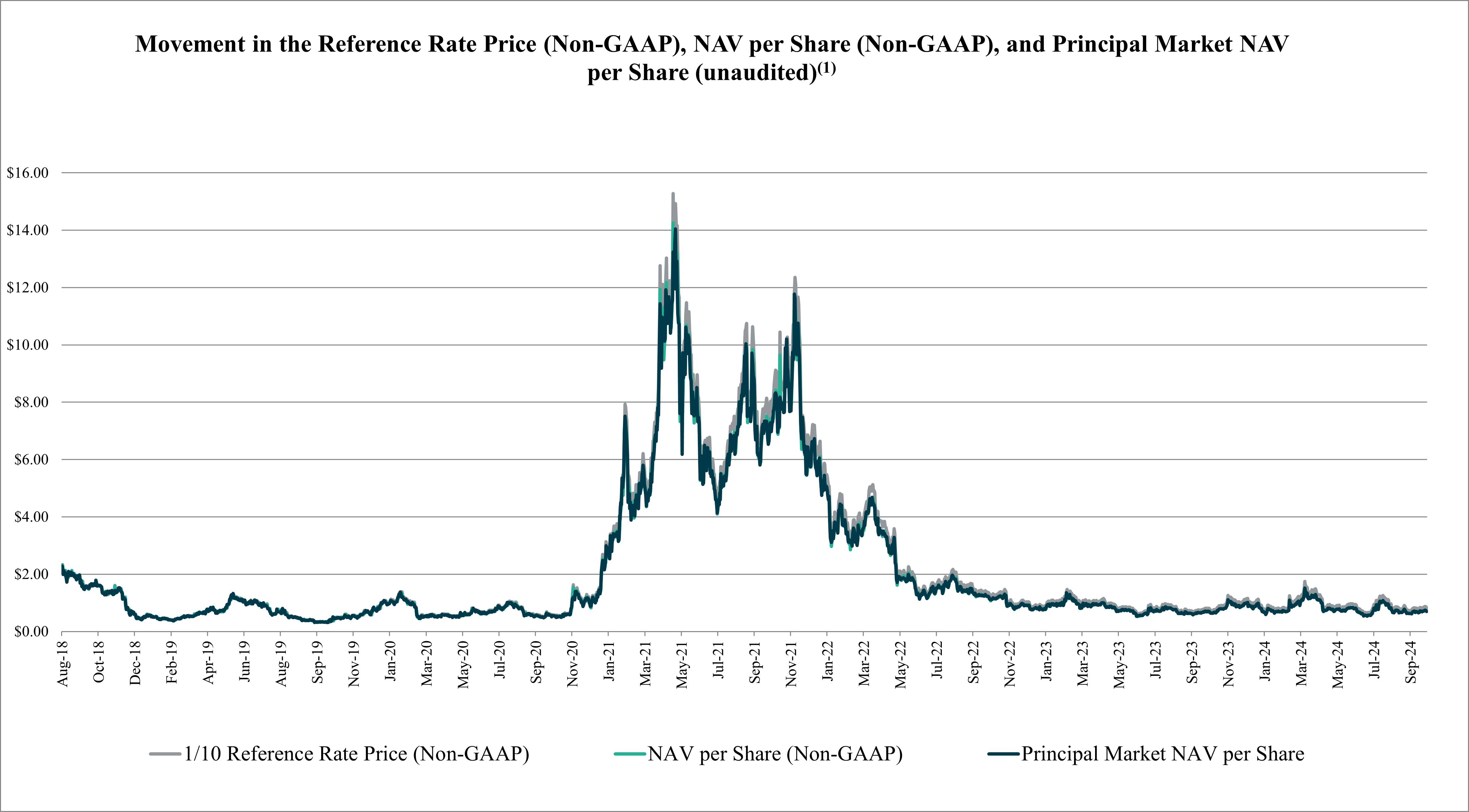

The U.S. dollar value of a Basket of Shares at 4:00 p.m., New York time, on the trade date of a creation order is equal to the Basket Amount, which is the amount of ZEN required to create a Basket of Shares, multiplied by the “Reference Rate Price,” which is a volume-weighted average price in U.S. dollars for the immediately preceding 24-hour period derived from data collected from Digital Asset Trading Platforms trading ZEN selected by the Reference Rate Provider as of 4:00 p.m., New York time, and included in the CoinDesk Horizen Reference Rate (the “Reference Rate”), on each business day. The Reference Rate Price is calculated using non-GAAP methodology and is not used in the Trust’s financial statements. See “—Overview of the ZEN Industry and Market—ZEN Value—The Reference Rate and the Reference Rate Price.” On June 16, 2023, the Reference Rate Provider removed Binance.US from the Reference Rate due to Binance.US’s announcement that the trading platform was suspending U.S. dollar deposits and withdrawals and planned to delist its U.S. dollar trading pairs, and did not add any Constituent Trading Platforms as part of its review. As a result of this removal, there were no longer sufficient Constituent Trading Platforms for the Reference Rate Provider to continue producing the Reference Rate pursuant to the Constituent Trading Platform selection methodology described in “—Overview of the ZEN Industry and Market—ZEN Value—The Reference Rate and the Reference Rate Price—Constituent Trading Platform Selection” below. If the Reference Rate becomes unavailable, the Sponsor employs an alternative method to determine the Reference Rate Price under the cascading set of rules set forth in “—Overview of the ZEN Industry and Market—ZEN Value—The Reference Rate and the Reference Rate Price—Determination of the Reference Rate Price When Reference Rate Price is Unavailable” below. Effective June 20, 2023, CoinDesk Indices, Inc. no longer determines the Reference Rate Price, and the Reference Rate Price is the price set by Coin Metrics Real-Time Rate (the “Secondary Reference Rate”) as of 4:00 p.m., New York time, on the valuation date (the “Secondary Reference Rate Price”). The Secondary Reference Rate Price is a real-time reference rate price, calculated using trade data from constituent markets selected by Coin Metrics, Inc. (the “Secondary Reference Rate Provider”). Effective June 20, 2023, any references to the “Reference Rate Price” in this Annual Report refers to the Secondary Reference Rate Price set by the Secondary Reference Rate selected by the Secondary Reference Rate Provider.

The Basket Amount is determined by dividing (x) the amount of ZEN owned by the Trust at 4:00 p.m., New York time, on such trade date, after deducting the amount of ZEN representing the U.S. dollar value of accrued but unpaid fees and expenses of the Trust (converted using the Reference Rate Price at such time, and carried to the eighth decimal place), by (y) the number of Shares outstanding at such time (with the quotient so obtained calculated to one one-hundred-millionth of one ZEN (i.e., carried to the eighth decimal place)), and multiplying such quotient by 100.

The Shares are neither interests in nor obligations of the Sponsor or the Trustee.

The Sponsor maintains an internet website at www.grayscale.com/crypto-products/grayscale-horizen-trust/, through which the registrant’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are made available free of charge after they have been filed or furnished to the SEC. Additional information regarding the Trust may also be found on the SEC’s EDGAR database at www.sec.gov.

The contents of the websites referred to above and any websites referred to herein are not incorporated into this filing or any other reports or documents we file with or furnish to the SEC. Further, our references to the URLs for these websites are intended to be inactive textual references only.

Investment Objective

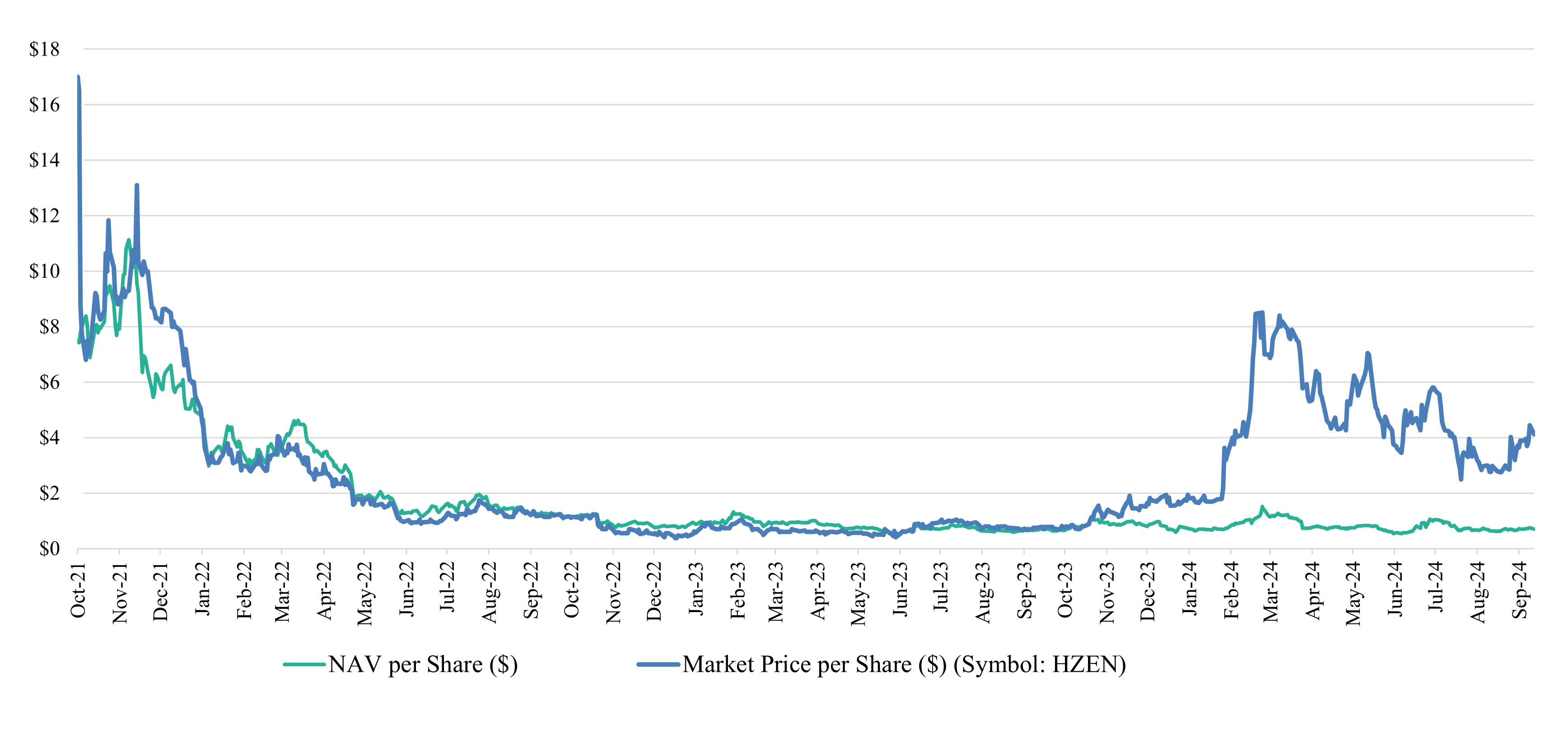

The Trust’s investment objective is for the value of the Shares (based on ZEN per Share) to reflect the value of ZEN held by the Trust, determined by reference to the Reference Rate Price, less the Trust’s expenses and other liabilities. To date, the Trust has not met its investment objective and the Shares quoted on OTCQX have not reflected the value of ZEN held by the Trust, less the Trust’s expenses and other liabilities, but instead have traded at both premiums and discounts to such value, which at times have been substantial.

In the event the Shares trade at a substantial premium, investors who purchase Shares on OTCQX will pay substantially more for their Shares than investors who purchase Shares in the private placement. The value of the Shares may not reflect the value of the Trust’s ZEN, less the Trust’s expenses and other liabilities, for a variety of reasons, including the holding period under Rule 144 for Shares purchased in the private placement, the lack of an ongoing redemption program, any halting of creations by the Trust, ZEN price volatility, trading volumes on, or closures of, trading platforms where digital assets trade due to fraud, failure, security breaches or otherwise, and the non-current trading hours between OTCQX and the global trading platform market for trading ZEN. As a result, the Shares may continue to trade at a substantial premium over, or a substantial discount to, the value of the Trust’s ZEN, less the Trust’s expenses and other liabilities, and the Trust may be unable to meet its investment objective for the foreseeable future.

For example, from October 19, 2021 to September 30, 2024, the maximum premium of the closing price of the Shares quoted on OTCQX over the value of the Trust’s NAV per Share was 766%, the average premium was 223%, the maximum discount of the closing price of the Shares quoted on OTCQX below the value of the Trust’s NAV per Share was 54%, and the average discount was 20%. The closing price of the Shares, as quoted on OTCQX at 4:00 p.m., New York time, on each business day between October 19, 2021 and September 30, 2024, has been quoted at a discount on 348 days. As of September 30, 2024, the last business day of the period, the Trust’s Shares were quoted on OTCQX at a premium of 492% to the Trust’s NAV per Share. Prior to February 7, 2024, NAV was referred to as Digital Asset Holdings and NAV per Share was referred to as Digital Asset Holdings per Share. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Secondary Market Trading.”

2

While an investment in the Shares is not a direct investment in ZEN, the Shares are designed to provide investors with a cost-effective and convenient way to gain investment exposure to ZEN. A substantial direct investment in ZEN may require expensive and sometimes complicated arrangements in connection with the acquisition, security and safekeeping of the ZEN and may involve the payment of substantial fees to acquire such ZEN from third-party facilitators through cash payments of U.S. dollars. Because the value of the Shares is correlated with the value of the ZEN held by the Trust, it is important to understand the investment attributes of, and the market for, ZEN.

Shares purchased in the private placement are restricted securities that may not be resold except in transactions exempt from registration under the Securities Act and state securities laws and any such transaction must be approved in advance by the Sponsor. In determining whether to grant approval, the Sponsor will specifically look at whether the conditions of Rule 144 under the Securities Act, including the requisite holding period thereunder, and any other applicable laws have been met. Any attempt to sell the Shares without the approval of the Sponsor in its sole discretion will be void ab initio. See “—Description of the Shares—Transfer Restrictions” for more information.

Pursuant to Rule 144, the minimum holding period for Shares purchased in the private placement is six months.

The Trust’s ZEN are carried, for financial statement purposes, at fair value, as required by the U.S. generally accepted accounting principles (“U.S. GAAP”). The Trust determines the fair value of ZEN based on the price provided by the Digital Asset Market that the Trust considers its principal market as of 4:00 p.m., New York time, on the valuation date. The net asset value of the Trust determined on a U.S. GAAP basis is referred to in this Annual Report as “Principal Market NAV.” Prior to February 7, 2024, Principal Market NAV was referred to as NAV. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies and Estimates—Principal Market and Fair Value Determination” for more information on the Trust’s principal market selection.

The Trust uses the Reference Rate Price to calculate its “NAV,” a non-GAAP metric, which is the aggregate value, expressed in U.S. dollars, of the Trust’s assets (other than U.S. dollars, other fiat currency, Incidental Rights or IR Virtual Currency), less the U.S. dollar value of the Trust’s expenses and other liabilities calculated in the manner set forth under “—Valuation of ZEN and Determination of NAV.” “NAV per Share” is calculated by dividing NAV by the number of Shares currently outstanding. NAV and NAV per Share are not measures calculated in accordance with U.S. GAAP. NAV is not intended to be a substitute for the Trust’s Principal Market NAV calculated in accordance with U.S. GAAP, and NAV per Share is not intended to be a substitute for the Trust’s Principal Market NAV per Share calculated in accordance with U.S. GAAP. Prior to February 7, 2024, NAV was referred to as Digital Asset Holdings and Principal Market NAV was referred to as NAV.

At this time, the Trust is not operating a redemption program for Shares and therefore Shares are not redeemable by the Trust. In addition, the Trust may halt creations for extended periods of time for a variety of reasons, including in connection with forks, airdrops and other similar occurrences. As a result, Authorized Participants are not able to take advantage of arbitrage opportunities created when the market value of the Shares deviates from the value of the Trust’s NAV per Share, which may cause the Shares to trade at a substantial premium over, or a substantial discount to, the value of the Trust’s NAV per Share.

Subject to receipt of regulatory approval from the SEC and approval by the Sponsor in its sole discretion, the Trust may in the future operate a redemption program. However, because the Sponsor does not believe that the SEC would, at this time, entertain an application for the waiver of rules needed in order to operate an ongoing redemption program, the Sponsor currently has no intention of seeking regulatory approval from the SEC for the Trust to operate an ongoing redemption program. Even if such relief is sought in the future, no assurance can be given as to the timing of such relief or that such relief will be granted. If such relief is granted and the Sponsor approves a redemption program, the Shares will be redeemable in accordance with the provisions of the Trust Agreement and the relevant Participant Agreement. Although the Sponsor cannot predict with certainty what effect, if any, the operation of a redemption program would have on the trading price of the Shares, a redemption program would allow Authorized Participants to take advantage of arbitrage opportunities created when the market value of the Shares deviates from the value of the Trust’s ZEN, less the Trust’s expenses and other liabilities, which may have the effect of reducing any premium or discount at which the Shares trade on OTCQX over or below such value, respectively, which at times has been substantial.

For a discussion of risks relating to the deviation in the trading price of the Shares from the NAV per Share, see “Item 1A. Risk Factors—Risk Factors Related to the Trust and the Shares—Because of the holding period under Rule 144, the lack of an ongoing redemption program and the Trust’s ability to halt creations from time to time, there is no arbitrage mechanism to keep the value of the Shares closely linked to the Reference Rate Price and the Shares have historically traded at a substantial premium over, or a substantial discount to, the NAV per Share,” “Item 1A. Risk Factors—Risk Factors Related to the Trust and the Shares—The Shares may trade at a price that is at, above or below the Trust’s NAV per Share as a result of the non-current trading hours between OTCQX and the Digital Asset Trading Platform Market,” “Item 1A. Risk Factors—Risk Factors Related to the Trust and the Shares—Shareholders may suffer a loss on their investment if the Shares trade above or below the Trust’s NAV per Share” and “Item 1A. Risk Factors—Risk Factors Related to the Trust and the Shares—The restrictions on transfer and redemption may result in losses on the value of the Shares.”

3

Pursuant to the terms of the Trust Agreement, the Trust is required to dissolve under certain circumstances. In addition, the Sponsor may, in its sole discretion, dissolve the Trust for a number of reasons, including if the Sponsor determines, in its sole discretion, that it is desirable or advisable for any reason to discontinue the affairs of the Trust. For example, if the Sponsor determines that ZEN is a security under the federal securities laws, whether that determination is initially made by the Sponsor itself, or because a federal court upholds an allegation that ZEN is a security, the Sponsor does not intend to permit the Trust to continue holding ZEN in a way that would violate the federal securities laws (and therefore would either dissolve the Trust or potentially seek to operate the Trust in a manner that complies with the federal securities laws, including the Investment Company Act of 1940 (the “Investment Company Act”)). See “—Description of the Trust Agreement—Termination of the Trust” for additional discussion of the circumstances under which the Trust could be dissolved. See “Item 1A. Risk Factors—Risk Factors Related to the Trust and the Shares—A determination that ZEN or any other digital asset is a “security” may adversely affect the value of ZEN and the value of the Shares, and result in potentially extraordinary, nonrecurring expenses to, or termination of, the Trust.”

Characteristics of the Shares

The Shares are intended to offer investors an opportunity to gain exposure to digital assets through an investment in securities. As of September 30, 2024, each Share represented approximately 0.0857 ZEN. The logistics of accepting, transferring and safekeeping of ZEN are dealt with by the Sponsor and Custodian, and the related expenses are built into the value of the Shares. Therefore, shareholders do not have additional tasks or costs over and above those generally associated with investing in any other privately placed security.

The Shares have certain other key characteristics, including the following:

The Trust differentiates itself from many competing digital asset financial vehicles in the following ways:

4

Activities of the Trust

The activities of the Trust are limited to (i) issuing Baskets in exchange for ZEN transferred to the Trust as consideration in connection with the creations, (ii) transferring or selling ZEN, Incidental Rights and IR Virtual Currency as necessary to cover the Sponsor’s Fee and/or any Additional Trust Expenses, (iii) transferring ZEN in exchange for Baskets surrendered for redemption (subject to obtaining regulatory approval from the SEC and approval from the Sponsor), (iv) causing the Sponsor to sell ZEN, Incidental Rights and IR Virtual Currency on the termination of the Trust, (v) making distributions of Incidental Rights and/or IR Virtual Currency or cash from the sale thereof and (vi) engaging in all administrative and security procedures necessary to accomplish such activities in accordance with the provisions of the Trust Agreement, the Custodian Agreement, the Reference Rate License Agreement, the Secondary Reference Rate Provider Agreement and the Participant Agreements.

In addition, the Trust may engage in any lawful activity necessary or desirable in order to facilitate shareholders’ access to Incidental Rights or IR Virtual Currency, provided that such activities do not conflict with the terms of the Trust Agreement. The Trust will not be actively managed. It will not engage in any activities designed to obtain a profit from, or to ameliorate losses caused by, changes in the market prices of ZEN.

Incidental Rights and IR Virtual Currency

The Trust may from time to time come into possession of Incidental Rights and/or IR Virtual Currency by virtue of its ownership of ZEN, generally through a fork in the Horizen Blockchain, an airdrop offered to holders of ZEN or other similar event. Pursuant to the terms of the Trust Agreement, the Trust may take any lawful action necessary or desirable in connection with the Trust’s ownership of Incidental Rights, including the acquisition of IR Virtual Currency, unless such action would adversely affect the status of the Trust as a grantor trust for U.S. federal income tax purposes or otherwise be prohibited by the Trust Agreement. These actions include (i) selling Incidental Rights and/or IR Virtual Currency in the Digital Asset Market and distributing the cash proceeds to shareholders, (ii) distributing Incidental Rights and/or IR Virtual Currency in-kind to the shareholders or to an agent acting on behalf of the shareholders for sale by such agent if an in-kind distribution would otherwise be infeasible and (iii) irrevocably abandoning Incidental Rights or IR Virtual Currency. The Trust may also use Incidental Rights and/or IR Virtual Currency to pay the Sponsor’s Fee and Additional Trust Expenses, if any, as discussed below under “—Expenses; Sales of ZEN.” However, the Trust does not expect to take any Incidental Rights or IR Virtual Currency it may hold into account for purposes of determining the Trust’s NAV, the NAV per Share, the Principal Market NAV and the Principal Market NAV per Share.

With respect to any fork, airdrop or similar event, the Sponsor may, in its discretion, decide to cause the Trust to distribute the Incidental Rights or IR Virtual Currency in-kind to an agent of the shareholders for resale by such agent, or to irrevocably abandon the Incidental Rights or IR Virtual Currency. In the case of a distribution in-kind to an agent acting on behalf of the shareholders, the shareholders’ agent will attempt to sell the Incidental Rights or IR Virtual Currency, and if the agent is able to do so, will remit the cash proceeds to shareholders, net of expenses and any applicable withholding taxes. There can be no assurance as to the price or prices for any Incidental Rights or IR Virtual Currency that the agent may realize, and the value of the Incidental Rights or IR Virtual Currency may increase or decrease after any sale by the agent. In the case of abandonment of Incidental Rights or IR Virtual Currency, the Trust would not receive any direct or indirect consideration for the Incidental Rights or IR Virtual Currency and thus the value of the Shares will not reflect the value of the Incidental Rights or IR Virtual Currency.

On July 29, 2019, the Sponsor delivered to the Custodian a notice (the “Pre-Creation Abandonment Notice”) stating that the Trust is abandoning irrevocably for no direct or indirect consideration, effective immediately prior to each time at which the Trust creates Shares (any such time, a “Creation Time”), all Incidental Rights and IR Virtual Currency to which it would otherwise be entitled as of such time (any such abandonment, a “Pre-Creation Abandonment”); provided that a Pre-Creation Abandonment will not apply to any Incidental Rights and/or IR Virtual Currency if (i) the Trust has taken, or is taking at such time, an Affirmative Action to acquire or abandon such Incidental Rights and/or IR Virtual Currency at any time prior to such Creation Time or (ii) such Incidental Rights and/or IR Virtual Currency has been subject to a previous Pre-Creation Abandonment. An Affirmative Action refers to a written notification

5

from the Sponsor to the Custodian of the Trust’s intention (i) to acquire and/or retain any Incidental Rights and/or IR Virtual Currency or (ii) to abandon, with effect prior to the relevant Creation Time, any Incidental Rights and/or IR Virtual Currency.

In determining whether to take an Affirmative Action to acquire and/or retain an Incidental Right and/or IR Virtual Currency, the Trust takes into consideration a number of factors, including:

In determining whether the IR Virtual Currency is, or may be, a security under federal securities laws, the Sponsor takes into account a number of factors, including the various definitions of “security” under the federal securities laws and federal court decisions interpreting elements of these definitions, such as the U.S. Supreme Court’s decisions in the Howey and Reves cases, as well as reports, orders, press releases, public statements and speeches by the SEC and its staff providing guidance on when a digital asset may be a security for purposes of the federal securities laws.

As a result of the Pre-Creation Abandonment Notice, since July 29, 2019, the Trust has irrevocably abandoned, prior to the Creation Time of any Shares, any Incidental Right or IR Virtual Currency that it may have any right to receive at such time. The Trust has no right to receive any Incidental Right or IR Virtual Currency abandoned pursuant to either the Pre-Creation Abandonment Notice or Affirmative Actions. Furthermore, the Custodian has no authority, pursuant to the Custodian Agreement or otherwise, to exercise, obtain or hold, as the case may be, any such abandoned Incidental Right or IR Virtual Currency on behalf of the Trust or to transfer any such abandoned Incidental Right or IR Virtual Currency to the Trust if the Trust terminates its custodial agreement with the Custodian.

The Sponsor intends to evaluate each fork, airdrop or similar occurrence on a case-by-case basis in consultation with the Trust’s legal advisers, tax consultants, and Custodian, and may decide to abandon any Incidental Rights or IR Virtual Currency resulting from a hard fork, airdrop or similar occurrence should the Sponsor conclude, in its discretion, that such abandonment is in the best interests of the Trust. In the event the Sponsor decides to sell any Incidental Right or IR Virtual Currency, it would expect to execute the sale to or through an eligible financial institution that is subject to federal and state licensing requirements and practices regarding anti-money laundering (“AML”) and know-your-customer (“KYC”) regulations, which may include an Authorized Participant, a Liquidity Provider (as defined below in “—Service Providers of the Trust—Authorized Participants”), or one or more of their affiliates. In either case, the Sponsor expects that an Authorized Participant or Liquidity Provider would only be willing to transact with the Sponsor on behalf of the Trust if an Authorized Participant or Liquidity Provider considered it possible to trade the Incidental Right or IR Virtual Currency on a Digital Asset Trading Platform or other venue to which the Authorized Participant or Liquidity Provider has access. Generally, any such Authorized Participant or Liquidity Provider would have access only to Digital Asset Trading Platforms or other venues that it reasonably believes are operating in compliance with applicable law, including federal and state licensing requirements, based upon information and assurances provided to it by each venue.

Secondary Market Trading

While the Trust’s investment objective is for the value of the Shares (based on ZEN per Share) to reflect the value of ZEN held by the Trust, determined by reference to the Reference Rate Price, less the Trust’s expenses and other liabilities, the Shares may trade in the Secondary Market on OTCQX (or on another Secondary Market in the future) at prices that are lower or higher than the NAV per Share. The amount of the discount or premium in the trading price relative to the NAV per Share may be influenced by non-concurrent trading hours and liquidity between OTCQX and larger Digital Asset Trading Platforms. While the Shares are listed and trade on OTCQX from 6:00 a.m. until 5:00 p.m., New York time, liquidity in the Digital Asset Markets may fluctuate depending upon the volume and availability of larger Digital Asset Trading Platforms. As a result, during periods in which Digital Asset Market liquidity is limited or a major Digital Asset Trading Platform is off-line, trading spreads, and the resulting premium or discount, on the Shares may widen.

6

Overview of the ZEN Industry and Market

Horizen, or ZEN, is a digital asset that is created and transmitted through the operations of the peer-to-peer Horizen Network, a decentralized network of computers that operates on cryptographic protocols. No single entity owns or operates the Horizen Network, the infrastructure of which is collectively maintained by a decentralized user base. The Horizen Network allows people to exchange tokens of value, called ZEN, which are recorded on a public transaction ledger known as a blockchain. ZEN can be used to pay for goods and services, including computational power on the Horizen Network, or it can be converted to fiat currencies, such as the U.S. dollar, at rates determined on Digital Asset Trading Platforms or in individual end-user-to-end-user transactions under a barter system.

The Horizen Network is one of a number of projects intended to enhance blockchain technology. One of the Horizen Network’s primary enhancements of the blockchain was to add additional layers of confidentiality to traditional blockchain infrastructure so that users could make transactions and selectively disclose details related to those transactions. ZEN accomplished this level of confidentiality by using novel cryptographic zk-SNARKs to protect both the amount and the sender and recipient of the transaction. The result was a confidential transaction known as a “shielded” transaction. From the inception of the Horizen Network through September 30, 2022, approximately 22% of Horizen transactions had been unshielded, approximately 4% involved one party utilizing a shielded address, and approximately 74% involved both parties utilizing a shielded address. However, in September 2023, the Horizen protocol implemented an update intended to deprecate these privacy shields, with the intent of causing it to no longer be considered a “privacy coin,” and, following the update, the Horizen Network no longer supported transactions from unshielded addresses to shielded addresses.

The Horizen Network was launched on May 23, 2017 as “ZenCash” by a team of scientists, cryptographers, engineers and advisers of the Horizen Blockchain Foundation (the “Foundation”), bringing into existence the first ZEN tokens. In this role, the Foundation supports the development of ZEN by, among other things, reviewing and implementing upgrades that become part of the main implementation of ZEN. The Horizen Network was created through a fork of the Zclassic protocol, which in turn was created through a clone of the Zcash blockchain, which in turn was created through a clone of the Bitcoin blockchain, the first and most widely used blockchain. Zcash was the first digital asset protocol to introduce zk-SNARKs. The Zclassic protocol is substantially similar to the Zcash protocol except that it changed key economic and governance parameters, including removing a 20% block reward that is distributed to a group of Zcash founders, investors, employees and advisers as a “founders reward” for the first four years of the Zcash network’s operation. The ZEN blockchain further forked the Zclassic protocol to develop a platform with additional changes to the economic, governance and technical parameters of the network, as described below.

Unlike Zcash and Zclassic, which were originally designed to apply the privacy-preserving features of zk-SNARKs to financial transactions, the creators of Horizen realized that zk-SNARKs had wider applications beyond the privacy-preserving financial transactions, such as privacy-preserving messaging and publishing. The creators of Horizen principally achieved this by expanding beyond a single layer blockchain to utilize two-layer parallel blockchains. As a result, today the Horizen Network is comprised of two core blockchain layers: (1) the main Horizen Blockchain, which serves as the base layer for a simple Peer-2-Peer (P2P) digital asset protocol and (2) parallel blockchains (each a “Sidechain” and collectively, “Sidechains”), which provide for additional functionality and blockchain application features. In this sense, Horizen is a “blockchain-of-blockchains.” Both the Horizen Blockchain and Sidechains share a common digital asset, ZEN. On the Horizen Blockchain, ZEN can be used as a P2P digital asset, like Bitcoin and Zcash, and on the Sidechains, ZEN can be used to fuel decentralized applications (dApps) and smart contracts, like Ethereum. With all of these functionalities, the Horizen Network seeks to create a high-performing platform for money, media and messaging.

While ZEN’s monetary base is intended to be fixed at 21 million, the same as the monetary base of Bitcoin and Zcash, and while the rate of ZEN creation will similarly halve every four years, there are some important differences in how ZEN is mined and distributed. For example, of the 6.25 ZEN created every 2.5 minutes, the block reward is distributed such that 60% is distributed to miners, 10% to nodes securing the Eon network side chain launched by the Horizen ecosystem in October 2023 (the “EON 1.0 nodes”), 10% to Super Nodes and 20% to the Foundation. However, the allocation of new ZEN as block rewards is expected to change with the EON 2.0 Migration, as described further below. See “—Creation of New ZEN” and “—Market Participants” for more information. This is in contrast to Zcash, where, during the first four years of ZEC’s existence, 80% of newly created ZEC is distributed to miners and 20% is allocated to the founders’ reward, with 10% of the ZEC in existence ultimately being distributed to the founders’ reward, and Zclassic, which eliminated the concept of a founders’ reward such that all newly created ZCL, the native token of the Zclassic protocol, is distributed to miners. Like Zcash, ZEN also implemented a memory-hard proof-of-work algorithm, Equihash, which involves adding a memory-hard problem to be solved in valid blocks, which is intended to result in less centralized hash power.

The Horizen Network is decentralized and does not require governmental, financial institution intermediaries or others, including the Foundation, to create, transmit or determine the value of ZEN. Rather, ZEN is created and allocated by the Horizen Network protocol through a “mining” process. Although the Foundation does not control the Horizen Network, it monitors the development of the Horizen Network and offers updates to the Horizen protocol, which the public may choose to implement or ignore. The Foundation does not sell, exchange, transmit or retain custody of ZEN for consumers or the public at large. The value of ZEN is determined by the supply of and demand for ZEN on the Digital Asset Trading Platforms or in private end-user-to-end-user transactions.

7

Similar to the Bitcoin Network and the Zcash network, the Horizen Network operates on a proof-of-work model. A portion of new ZEN are created and rewarded to the miners of a block in the Horizen Network for verifying transactions. The Horizen Network is effectively a decentralized database that includes all blocks that have been solved by miners and it is updated to include new blocks as they are solved. Each ZEN transaction is broadcast to the Horizen Network and, when included in a block, recorded in the Horizen Blockchain. As each new block records outstanding ZEN transactions, and outstanding transactions are settled and validated through such recording, the Horizen Blockchain represents a complete, unshielded and unbroken history of all transactions of the Horizen Network. For further details, see “—Creation of New ZEN.”

In June 2024, members of the ZEN ecosystem voted to deprecate the Horizen Network in favor of the yet-to-be-launched “EON 2.0” network (the “EON 2.0 Migration”). The EON 2.0 network is intended be a smart contract platform, unlike the Horizen Network, which is primarily intended as a payment platform. Just as in the Horizen Network, ZEN is intended to serve as the native digital asset for EON 2.0. However, unlike the Horizen Network’s proof-of-work consensus mechanism, in which miners expend computational resources to compete to validate transactions and are rewarded coins in proportion to the amount of computational resources expended, EON 2.0 intends to leverage proof-of-stake, whereby validators of the network risk or “stake” ZEN to compete to be selected to validate transactions and are rewarded ZEN in proportion to the amount of tokens staked. ZEN’s supply cap of 21 million is not expected to be affected by the EON 2.0 Migration. However, in September 2024, members of the ZEN ecosystem voted to approve a proposal to adjust the allocation of newly minted ZEN. This proposal is expected to take effect upon the completed EON 2.0 Migration. The proposal calls for 40% of newly issued ZEN to be distributed to validators securing the EON 2.0 network, 32.5% to be distributed to the Horizen Foundation, and 27.5% to be distributed to a decentralized autonomous organization under the collective control of ZEN holders (the “Horizen DAO”).

The proposal also called for replacing the ZEN’s per-block issuance schedule with a time-based release schedule. Under the proposal, the full amount of future ZEN allocated to the Horizen Foundation and Horizen DAO would be issued immediately upon the EON 2.0 Migration, with 25% of those amounts to be unlocked immediately upon the EON 2.0 Migration and the remaining 75% to be unlocked linearly at monthly intervals for 48 months thereafter. Newly issued ZEN allocated to EON 2.0 validators would continue issuance according to the halving schedule previously in place. As with the changes to ZEN allocation, these changes to the ZEN emission schedule are expected to occur upon the EON 2.0 Migration, which is expected to occur in 2025. The Horizen Network is expected to be deprecated in favor of EON 2.0 in 2025 and holders of ZEN on the Horizen Network are expected to be able to claim an equal amount of ZEN on the EON 2.0 network around that time. It is possible that the actual implementation of EON 2.0 and migration from the Horizen Network, including but not limited to the changes to the issuance schedule of new ZEN, may occur differently than is currently expected or possibly not occur at all.

Similar to Bitcoin and Zcash, ZEN can be used to pay for goods and services or can be converted to fiat currencies, such as the U.S. dollar, at rates determined on digital asset trading platforms or in individual end-user-to-end-user transactions under a barter system. Additionally, ZEN is used to pay for transaction fees to miners for verifying transactions on the Horizen Network.

Overview of the Horizen Network’s Operations

In order to own, transfer or use ZEN directly on the Horizen Network (as opposed to through an intermediary, such as a custodian), a person generally must have internet access to connect to the Horizen Network. ZEN transactions may be made directly between end-users without the need for a third-party intermediary. To prevent the possibility of double-spending ZEN, a user must notify the Horizen Network of the transaction by broadcasting certain transaction data to its network peers. The Horizen Network provides confirmation against double-spending by memorializing transactions in the Horizen Blockchain, in the case of public transactions, or through zk-SNARK zero-knowledge proofs in the case of shielded transactions. This memorialization and verification against double-spending is accomplished through the Horizen Network mining process, which adds “blocks” of data, including certain transaction information, to the Horizen Blockchain. Although the Horizen Network is publicly accessible, shielded transactions do not, by design, have the same level of transparency as the Bitcoin blockchain. Nonetheless, in September 2023, the Horizen protocol implemented an update intended to deprecate these privacy shields, with the intent of causing it to no longer be considered a “privacy coin,” and, following the update, the Horizen Network no longer supported transactions from unshielded addresses to shielded addresses.

Brief Description of ZEN Transfers

There are two types of transactions that can occur on the Horizen Network: (1) unshielded transactions, which are similar to the transactions that take place on other blockchains, such as the Bitcoin Network and the Ethereum network and (2) shielded transactions, which maintain a higher degree of privacy compared to unshielded transactions.

Prior to engaging in ZEN transactions directly on the Horizen Network, a user generally must first install on its computer or mobile device a Horizen Network software program that will allow the user to generate a private and public key pair associated with a ZEN address, commonly referred to as a “wallet.” The Horizen Network software program and the ZEN address also enable the user to connect to the Horizen Network and transfer ZEN to, and receive ZEN from, other users.

8

Each Horizen Network address, or wallet, is associated with a unique “public key” and “private key” pair. To receive ZEN, the ZEN recipient must provide its public key to the party initiating the transfer. This activity is analogous to a recipient for a transaction in U.S. dollars providing a routing address in wire instructions to the payor so that cash may be wired to the recipient’s account. The payor approves the transfer to the address provided by the recipient by “signing” a transaction that consists of the recipient’s public key with the private key of the address from where the payor is transferring the ZEN. The recipient, however, does not make public or provide to the sender its related private key.

Neither the recipient nor the sender reveal their private keys in a transaction, because the private key authorizes transfer of the funds in that address to other users. Therefore, if a user loses his or her private key, the user may permanently lose access to the ZEN contained in the associated address. Likewise, ZEN is irretrievably lost if the private key associated with them is deleted and no backup has been made. When sending ZEN, a user’s Horizen Network software program must validate the transaction with the associated private key. In addition, since every computation on the Horizen Network requires processing power, there is a transaction fee involved with the transfer that is paid by the payor. The resulting digitally validated transaction is sent by the user’s Horizen Network software program to the Horizen Network miners to allow transaction confirmation.

As discussed in greater detail below in “—Creation of New ZEN,” Horizen Network miners record and confirm transactions when they mine and add blocks of information to the Horizen Blockchain. When a miner mines a block, it creates that block, which includes data relating to (i) the satisfaction of the consensus mechanism to mine the block, (ii) a reference to the prior block in the Horizen Blockchain to which the new block is being added, and (iii) transactions that have submitted to the Horizen Network but have not yet been added to the Horizen Blockchain. The miner becomes aware of outstanding, unrecorded transactions through the data packet transmission and distribution discussed above.

Upon the addition of a block included in the Horizen Blockchain, the Horizen Network software program of both the spending party and the receiving party will show confirmation of the transaction on the Horizen Blockchain and reflect an adjustment to the ZEN balance in each party’s Horizen Network public key, completing the ZEN transaction. Once a transaction is confirmed on the Horizen Blockchain, it is irreversible. Shielded transactions utilize a scientific breakthrough in the field of cryptography known as “zero-knowledge proofs.” Zero-knowledge proofs allow users to prove knowledge of some facts about hidden information without revealing that information by encrypting certain aspects of the transaction. Ordinarily, if a blockchain’s transaction data is encrypted, nodes in the blockchain cannot determine whether senders really held the tokens they sent, whether they previously sent it to someone else or whether they never had it in the first place. The encrypted data becomes unverifiable by network nodes.

With the Horizen Network, a particular type of zero-knowledge proof called zk-SNARKs solves this problem. In a ZEN shielded transaction, the sender provides a string of data that makes up the “zero-knowledge proof” and encrypted transaction data, which proves properties of the encrypted data cryptographically, including that the sender could not have generated a specific string unless the sender had ownership over the private key and unless the input and output values were equal. The proof also guarantees creation of a unique nullifier which is used to mark tokens as spent, when they are, in fact spent. In other words, zero-knowledge proofs allow verifiability without compromising confidentiality. Shielded transactions must involve a “shielded address,” or an address capable of utilizing zero-knowledge proof technologies in its transactions. By default, ZEN is stored in unshielded addresses unless or until they are sent to a shielded address.

Shielded transactions may: (1) involve only shielded addresses, in which the identity of the transacting parties and the amount sent is hidden, or (2) involve a mix of shielded and unshielded addresses, in which the identity of the shielded addresses is hidden but the identity of the unshielded address and the amount sent are publicly known. Following the deprecation of privacy shields from the Horizen Network in September 2023, transactions sent from unshielded addresses to shielded addresses are no longer possible on the Horizen Network, and the amount of ZEN remaining in shielded addresses, and, therefore, the amounts of ZEN involved in shielded transactions, is expected to decrease over time.

Some ZEN transactions are conducted “off-blockchain” and are therefore not recorded in the Horizen Blockchain. Some “off-blockchain transactions” involve the transfer of control over, or ownership of, a specific digital wallet holding ZEN or the reallocation of ownership of certain ZEN in a pooled-ownership digital wallet, such as a digital wallet owned by a Digital Asset Trading Platform. In contrast to on-blockchain transactions, which are publicly recorded on the Horizen Blockchain, information and data regarding off-blockchain transactions are generally not publicly available. Therefore, off-blockchain transactions are not truly ZEN transactions in that they do not involve the transfer of transaction data on the Horizen Network and do not reflect a movement of ZEN between addresses recorded in the Horizen Blockchain. For these reasons, off-blockchain transactions are subject to risks as any such transfer of ZEN ownership is not protected by the protocol behind the Horizen Network or recorded in, and validated through, the blockchain mechanism.

9

Creation of New ZEN

Initial Creation of ZEN

The initial creation of ZEN as part of the first Horizen Network block, or genesis block, was conducted on May 23, 2017. All additional ZEN have been, and will be, created through the mining process.

Mining Process

The Horizen Network is kept running by computers all over the world. In order to incentivize those who incur the computational costs of securing the network by validating transactions, there is a reward that is given to the computer that was able to create the latest block on the chain. Every 2.5 minutes, on average, a new block is added to the Horizen Blockchain with the latest transactions processed by the network, and the computer that generated this block is currently awarded 6.25 ZEN. Due to the nature of the algorithm for block generation, this process (generating a “proof-of-work”) is guaranteed to be random. Over time, rewards are expected to be proportionate to the computational power of each machine.

The process by which ZEN is “mined” results in new blocks being added to the Horizen Blockchain and new ZEN tokens being issued to the miners, EON 1.0 nodes, Super Nodes and the Foundation. Computers on the Horizen Network engage in a set of prescribed complex mathematical calculations in order to add a block to the Horizen Blockchain and thereby confirm ZEN transactions included in that block’s data.

To begin mining, a user can download and run Horizen Network mining software, which turns the user’s computer into a “node” on the Horizen Network that validates blocks. Each block contains the details of some or all of the most recent transactions that are not memorialized in prior blocks, as well as a record of the award of ZEN to the miner who added the new block. Each unique block can be solved and added to the Horizen Blockchain by only one miner or mining pool. Therefore, all individual miners and mining pools on the Horizen Network are engaged in a competitive process of constantly increasing their computing power to improve their likelihood of solving for new blocks. As more miners join the Horizen Network and its processing power increases, the Horizen Network adjusts the complexity of the block-solving equation to maintain a predetermined pace of adding a new block to the Horizen Blockchain approximately every 2.5 minutes. A miner’s proposed block is added to the Horizen Blockchain once a majority of the nodes on the Horizen Network confirms the miner’s work. Miners that are successful in adding a block to the Horizen Blockchain are automatically awarded ZEN for their effort and may also receive transaction fees paid by transferors whose transactions are recorded in the block. This reward system is the method by which new ZEN enter into circulation to the public.

Staking Process

The Horizen Network also relies on a proof-of-stake algorithm for certain functionalities. Under a proof-of-stake ecosystem, the validating node, known as a validator, locks up an amount of his or her coins to verify a block of transactions in a process that requires less computing power and electricity. Validators can participate in block production by posting a security deposit, or bond. After posting a bond, one may bet on which block will be included next. Validators make money by betting with the eventual consensus and lose money by betting against the consensus. Any cryptographically-provable misbehavior results in the forfeiture of the bond. Moreover, an honest validator is expected to have very low costs, compared to the costs an attacker would incur. On the Horizen Network, Secure Nodes and Super Nodes stake their coins. See “—Market Participants” below for more information.

Limits on ZEN Supply

The Horizen Network is structured to allow a maximum of 21 million ZEN to be created, which are mined over time with the creation of each new block. At inception, 12.5 ZEN were created every 2.5 minutes, on average. Of each block of newly created ZEN, 60% is distributed to miners, 10% is distributed to nodes securing the Eon network side chain launched by the Horizen ecosystem in October 2023 (the “EON 1.0 nodes”), 10% is distributed to Super Nodes and 20% is distributed to the Foundation. Every four years, the rate of ZEN being created will halve, just as it does for Bitcoin. Thus, in December 2020, the reward was halved to 6.25 ZEN for every block, and will again be halved to 3.125 in December 2024. However, in September 2024, members of the ZEN ecosystem voted to approve a proposal to adjust the allocation of newly minted ZEN. This proposal is expected to take effect upon the completed EON 2.0 Migration. The proposal calls for 40% of newly issued ZEN to be distributed to validators securing the EON 2.0 network, 32.5% to be distributed to the Horizen Foundation, and 27.5% to be distributed to the Horizen DAO.

As of September 30, 2024, approximately 15.5 million ZEN were outstanding, and estimates of when the 21 million ZEN limitation will be reached range from at or near the year 2051. However, this expected timeline may be impacted by the EON 2.0 Migration. It is unclear whether or how the EON 2.0 Migration will affect the creation and distribution schedule of ZEN.

10

Modifications to the ZEN Protocol

The Horizen Network is an open-source project with no official developer or group of developers that controls it. However, historically the Horizen Network’s development has been overseen by the Foundation. The Foundation is able to access and alter the Horizen Network source code and, as a result, they are responsible for quasi-official releases of updates and other changes to the Horizen Network’s source code.

For example, in June 2018, an upgrade was implemented to the Horizen Network to make it more computationally and economically expensive to privately mine blocks and later introduce those blocks to the valid Horizen Blockchain. The purpose of this upgrade was to significantly increase the difficulty of 51% attacks through delayed block submissions. In another example, in September 2023, an upgrade was implemented on the Horizen Network to remove the ability to transfer ZEN from unshielded to shielded addresses. As an effect, ZEN could be transferred out of shielded addresses, but could not be transferred into them, with the intention of reducing the amount of ZEN that could be transacted with privacy-preserving features over time. The purpose of this upgrade was to deprecate privacy shields and cause Horizen to no longer be considered a “privacy coin.”

The release of updates to the Horizen Network’s source code does not guarantee that the updates will be automatically adopted. Users and miners must accept any changes made to the Horizen Network source code by downloading the proposed modification of the Horizen Network’s source code. A modification of the Horizen Network’s source code is only effective with respect to the ZEN users and miners that download it. If a modification is accepted only by a percentage of users and miners, a division in the Horizen Network will occur such that one network will run the pre-modification source code and the other network will run the modified source code. Such a division is known as a “fork.” See “Item 1A. Risk Factors—Risk Factors Related to Digital Assets—A temporary or permanent “fork” or a “clone” could adversely affect the value of the Shares.” Consequently, as a practical matter, a modification to the source code becomes part of the Horizen Network only if accepted by participants collectively having a majority of the processing power on the Horizen Network. In June 2024, members of the ZEN ecosystem voted to implement the EON 2.0 Migration. The EON 2.0 network is intended be a smart contract platform, unlike the Horizen Network, which is primarily intended as a payment platform. It is unclear how the EON 2.0 Migration will be implemented, and it is possible miners in the Horizen Network will continue to sustain the network, possibly resulting in a fork if blocks for both the Horizen Network and EON 2.0 network continue to be processed.

Core development of the Horizen Network source code has increasingly focused on modifications of the Horizen Network protocol to increase speed and scalability and also allow for non-financial, next generation uses on Sidechains. Because the Trust only holds ZEN on the Horizen Network, it will not take advantage of such Sidechains. However, because such projects may utilize ZEN as tokens for the facilitation of their non-financial uses, they may increase demand for ZEN and the utility of the Horizen Network as a whole. Conversely, projects that operate and are built within the Horizen Blockchain may increase the data flow on the Horizen Network and could either “bloat” the size of the Horizen Blockchain or slow confirmation times.

ZEN Value

Digital Asset Trading Platform Valuation

The value of ZEN is determined by the value that various market participants place on ZEN through their transactions. The most common means of determining the value of a ZEN is by surveying one or more Digital Asset Trading Platforms where ZEN is traded publicly and transparently.

Digital Asset Trading Platform Public Market Data

On each online Digital Asset Trading Platform, ZEN is traded with publicly disclosed valuations for each executed trade, measured by one or more fiat currencies such as the U.S. dollar or euro, or by the widely used cryptocurrency Bitcoin. Over-the-counter dealers or market makers do not typically disclose their trade data.

Effective June 16, 2023, the Reference Rate Provider removed Binance.US from the Reference Rate due to Binance.US’s announcement that the trading platform was suspending U.S. dollar deposits and withdrawals and planned to delist its U.S. dollar trading pairs, and did not add any Constituent Trading Platforms as part of its review. As a result of this removal, there were no longer sufficient Constituent Trading Platforms for the Reference Rate Provider to continue producing the Reference Rate pursuant to the Constituent Trading Platform selection methodology described in “—The Reference Rate and the Reference Rate Price—Constituent Trading Platform Selection” below. If the Reference Rate becomes unavailable, the Sponsor employs an alternative method to determine the Reference Rate Price under the cascading set of rules set forth in “—The Reference Rate and the Reference Rate Price—Determination of the Reference Rate Price When Reference Rate Price is Unavailable” below. Effective June 20, 2023, CoinDesk Indices, Inc. no longer determines the Reference Rate Price, and the Reference Rate Price is the Secondary Reference Rate Price, which is the price set by Coin Metrics Real-Time Rate as of 4:00 p.m., New York time, on the valuation date. The Secondary Reference Rate Price is a real-time reference rate price, calculated using trade data from constituent markets selected by Coin Metrics, Inc., the Secondary Reference

11

Rate Provider. Effective June 20, 2023, any references to the “Reference Rate Price” in this Annual Report refers to the Secondary Reference Rate Price set by the Secondary Reference Rate selected by the Secondary Reference Rate Provider.

As of September 30, 2024, the Digital Asset Trading Platforms included in the Reference Rate and used to determine the Reference Rate Price are Coinbase, Binance, Bybit, Gate.io, and KuCoin.

Currently, there are several Digital Asset Trading Platforms operating worldwide and online Digital Asset Trading Platforms represent a substantial percentage of ZEN buying and selling activity and provide the most data with respect to prevailing valuations of ZEN. These trading platforms include established trading platforms such as trading platforms included in the Secondary Reference Rate which provide a number of options for buying and selling ZEN. The below tables reflect the trading volume in ZEN and market share of the ZEN-U.S. dollar, ZEN-Bitcoin, and ZEN-USDT trading pairs of each of the Digital Asset Trading Platforms included in the Secondary Reference Rate Price as of September 30, 2024 (collectively, “Constituent Trading Platforms”), using data since the inception of the Trust:

Digital Asset Trading Platforms included in the Secondary Reference Rate as of September 30, 2024 |

|

Volume (ZEN)(1) |

|

|

Market Share(2) |

|

||

Coinbase |

|

|

21,610,699 |

|

|

|

53.15 |

% |

Total ZEN-U.S. Dollar trading pair |

|

|

21,610,699 |

|

|

|

53.15 |

% |

Digital Asset Trading Platforms included in the Secondary Reference Rate as of September 30, 2024 |

|

Volume (ZEN)(1) |

|

|

Market Share(3) |

|

||

Binance |

|

|

67,605,414 |

|

|

|

88.79 |

% |

Total ZEN-Bitcoin trading pair |

|

|

67,605,414 |

|

|

|

88.79 |

% |

Digital Asset Trading Platforms included in the Secondary Reference Rate as of September 30, 2024 |

|

Volume (ZEN)(1) |

|

|

Market Share(4) |

|

||

Binance |

|

|

272,922,294 |

|

|

|

86.72 |

% |

Bybit |

|

|

12,910,532 |

|

|

|

4.10 |

% |

Gate.io |

|

|

12,517,187 |

|

|

|

3.98 |

% |

KuCoin |

|

|

1,279,367 |

|

|

|

0.40 |

% |

Total ZEN-USDT trading pair |

|

|

299,629,379 |

|

|

|

95.20 |

% |

12

The domicile, regulation and legal compliance of the Digital Asset Trading Platforms included in the Reference Rate varies. Information regarding each Digital Asset Trading Platform may be found, where available, on the websites for such Digital Asset Trading Platforms, among other places.

Although the Reference Rate is designed to accurately capture the market price of ZEN, third parties may be able to purchase and sell ZEN on public or private markets not included among the constituent Digital Asset Trading Platforms of the Reference Rate, and such transactions may take place at prices materially higher or lower than the Reference Rate Price. Moreover, there may be variances in the prices of ZEN on the various Digital Asset Trading Platforms, including as a result of differences in fee structures or administrative procedures on different Digital Asset Trading Platforms. For example, based on data provided by the Reference Rate Provider, on any given day during the year ended September 30, 2024, the maximum differential between the 4:00 p.m., New York time, spot price of any single Digital Asset Trading Platform included in the Reference Rate and Reference Rate Price was 11.17% and the average of the maximum differentials of the 4:00 p.m., New York time, spot price of each Digital Asset Trading Platform included in the Reference Rate and the Reference Rate Price was 5.98%. During this same period, the average differential between the 4:00 p.m., New York time, spot prices of all the Digital Asset Trading Platforms included in the Reference Rate and Reference Rate Price was 0.04%. All Digital Asset Trading Platforms that were included in the Reference Rate throughout the period were considered in this analysis. To the extent such prices differ materially from the Reference Rate Price, investors may lose confidence in the Shares’ ability to track the market price of ZEN.

The Reference Rate and the Reference Rate Price

The Reference Rate is a U.S. dollar-denominated composite reference rate for the price of ZEN. The Reference Rate is designed to provide a semi real-time, volume-weighted value of ZEN.

The Reference Rate Price is determined by the Reference Rate Provider through a process in which trade data from the Digital Asset Trading Platforms included in the Reference Rate is compiled to calculate a volume-weighted average price. Pursuant to the set of rules described under “—Determination of the Reference Rate Price When Reference Rate is Unavailable,” effective June 20, 2023, CoinDesk Indices, Inc. no longer determines the Reference Rate Price, and the Reference Rate Price is the price set by Coin Metrics Real-Time Rate (the “Secondary Reference Rate”) as of 4:00 p.m., New York time, on the valuation date (the “Secondary Reference Rate Price”), as further described under “—Determination of the Secondary Reference Rate Price.”

Determination of the Reference Rate Price

The Reference Rate Price for ZEN is calculated daily at 4:00 p.m., New York time, by the Reference Rate Provider using a volume-weighted average price across the Constituent Trading Platforms over the prior 24-hour period. Price and volume inputs are sourced from the Constituent Trading Platforms. Price and volume inputs are weighted as received with no further adjustments made to the weighting of each trading platform based on market anomalies observed on a Constituent Trading Platform or otherwise.

Each Constituent Trading Platform is weighted relative to its share of trading volume to the trading volume of all Constituent Trading Platforms. As such, price inputs from Constituent Trading Platforms with higher trading volumes will be weighted more heavily in calculating the Reference Rate Price than price inputs from Constituent Trading Platforms with lower trading volumes.

If the Reference Rate Price becomes unavailable, or if the Sponsor determines in good faith that such Reference Rate Price does not reflect an accurate price for ZEN, then the Sponsor will, on a best efforts basis, contact the Reference Rate Provider to obtain the Reference Rate Price directly from the Reference Rate Provider. If after such contact such Reference Rate Price remains unavailable or the Sponsor continues to believe in good faith that such Reference Rate Price does not reflect an accurate price for the relevant digital asset, then the Sponsor will employ a cascading set of rules to determine the Reference Rate Price, as described below in “—Determination of the Reference Rate Price When Reference Rate Price is Unavailable.”