We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Share Name | Share Symbol | Market | Type |

|---|---|---|---|

| Tricon Residential Inc | NYSE:TCN | NYSE | Common Stock |

| Price Change | % Change | Share Price | High Price | Low Price | Open Price | Shares Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|

| 0.00 | 0.00% | 11.25 | 0 | 00:00:00 |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 13E-3

RULE 13E-3 TRANSACTION STATEMENT UNDER SECTION 13(e)

OF THE SECURITIES EXCHANGE ACT OF 1934

Tricon Residential Inc.

(Name of the Issuer)

Tricon Residential Inc.

Creedence Acquisition ULC

BCORE Preferred Holdco LLC

Blackstone Real Estate Partners X L.P.

Blackstone Real Estate Income Trust, Inc.

BREIT Operating Partnership L.P.

Creedence Intermediate Holdings Inc.

Blackstone Real Estate Associates X L.P.

(Names of Persons Filing Statement)

Common Shares, no par value

(Title of Class of Securities)

89612W102

(CUSIP Number of Class of Securities)

| David Veneziano Tricon Residential Inc. 7 St. Thomas Street, Suite 801 Toronto, Ontario Canada, M5S 2B7 +1 416-925-7228 |

Jacob Werner Creedence Acquisition ULC c/o Blackstone Inc. 345 Park Avenue New York, New York 10154 +1 212-583-5000 |

(Name, Address and Telephone Number of Person Authorized to Receive Notices and Communications on Behalf of the Persons Filing Statement)

With copies to

| Matthew W. Abbott Christopher J. Cummings Brian C. Lavin Paul, Weiss, Rifkind, Wharton & Garrison LLP 1285 Avenue of the Americas New York, New York 10019 +1 212-373-3000 |

Johnny Connon Tara Hunt Goodmans LLP 333 Bay St., Suite 3400 Toronto, Ontario M5H 2S7 +1 416-979-2211 |

Brian M. Stadler Matthew B. Rogers Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017 +1 212-455-2000 |

Vincent Mercier Kevin Greenspoon Joseph DiPonio Davies Ward Phillips & Vineberg LLP 155 Wellington Street West Toronto, Ontario M5V 3J7 +1 416-863-0900 |

This statement is filed in connection with (check the appropriate box):

| a. ☐ | The filing of solicitation materials or an information statement subject to Regulation 14A (§§240.14a-1 through 240.14b-2), Regulation 14C (§§240.14c-1 through 240.14c-101) or Rule 13e-3(c) (§240.13e-3(c)) under the Securities Exchange Act of 1934 (“the Act”). |

| b. ☐ | The filing of a registration statement under the Securities Act of 1933. |

| c. ☐ | A tender offer. |

| d. ☒ | None of the above. |

Check the following box if the soliciting materials or information statement referred to in checking box (a) are preliminary copies: ☐

Check the following box if the filing is a final amendment reporting the results of the transaction: ☐

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THIS TRANSACTION, PASSED UPON THE MERITS OR FAIRNESS OF THIS TRANSACTION, OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THIS TRANSACTION STATEMENT ON SCHEDULE 13E-3. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

INTRODUCTION

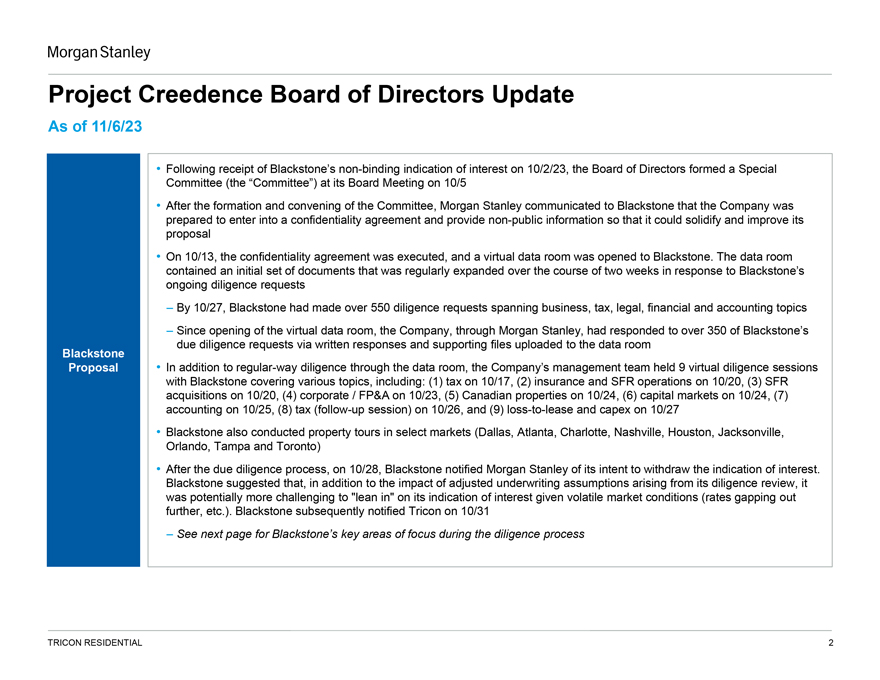

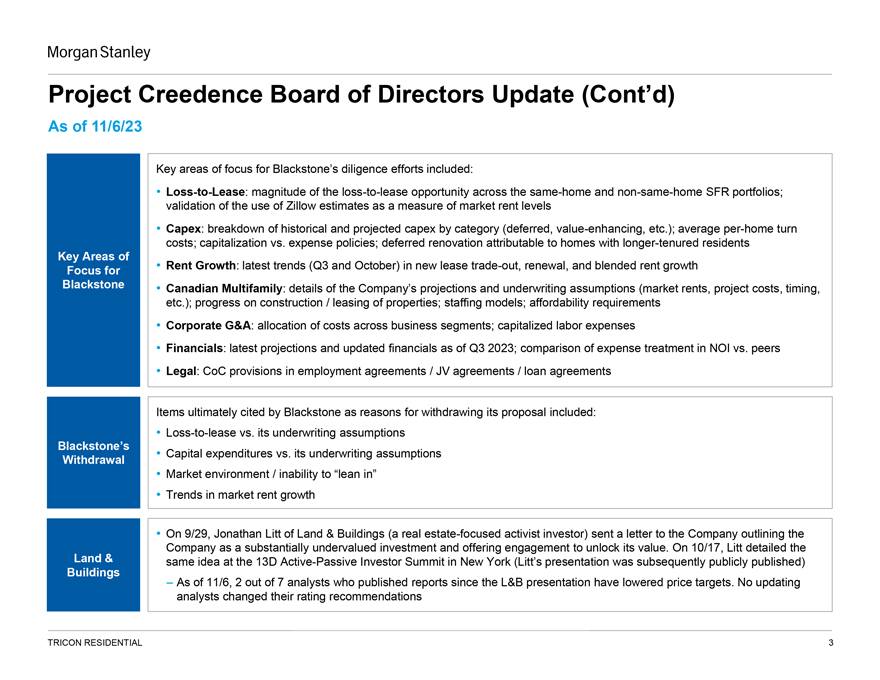

This Rule 13E-3 Transaction Statement on Schedule 13E-3, together with the exhibits hereto (this “Schedule 13E-3” or “Transaction Statement”), is being filed with the Securities and Exchange Commission (the “SEC”) pursuant to Section 13(e) of the Securities Exchange Act of 1934, as amended (together with the rules and regulations promulgated thereunder, the “Exchange Act”), jointly by the following persons (each, a “Filing Person,” and collectively, the “Filing Persons”): (i) Tricon Residential Inc., a corporation existing under the laws of the Province of Ontario and the issuer of the common shares, no par value (the “Shares”) that is subject to the Rule 13e-3 transaction (“Tricon” or the “Corporation”); (ii) Creedence Acquisition ULC, an unlimited liability company organized under the laws of the Province of British Columbia (“Creedence” or the “Purchaser”), an entity formed to effect the acquisition of the Corporation by Blackstone Real Estate Partners X L.P. (“BREP X”) and Blackstone Real Estate Income Trust, Inc. (“BREIT”, and collectively with BREP X and their respective affiliates, including the Purchaser, “Blackstone”); (iii) BCORE Preferred Holdco LLC, a Delaware limited liability company (“BREIT Shareholder”); (iv) BREP X, a Delaware limited partnership; (v) BREIT, a Maryland corporation; (vi) BREIT Operating Partnership L.P., a Delaware limited partnership; (vii) Creedence Intermediate Holdings Inc., a corporation organized under the laws of the Province of British Columbia; and (viii) Blackstone Real Estate Associates X L.P., a Delaware limited partnership.

On January 18, 2024, the Corporation and the Purchaser entered into an Arrangement Agreement (as amended, restated, supplemented or otherwise modified from time to time in accordance with its terms, the “Arrangement Agreement”), which provides for, among other things, the acquisition by the Purchaser of all of the issued and outstanding Shares of the Corporation through a Plan of Arrangement (the “Plan of Arrangement”) pursuant to Section 182 of the Business Corporations Act (Ontario) (“OBCA”), pursuant to which the Corporation would become a direct wholly owned subsidiary of the Purchaser (the “Arrangement”). A copy of the Plan of Arrangement is included as Appendix “B” to the Management Information Circular, which is attached as Exhibit (a)(2)(i) hereto (the “Circular”). A special meeting of the Corporation’s shareholders (the “Shareholders”) has been called for March 28, 2024 (the “Meeting”) to consider and, if thought advisable, pass a special resolution approving the Arrangement in the form attached as Appendix “A” to the Circular (the “Arrangement Resolution”). Capitalized terms used but not expressly defined in this Schedule 13E-3 are given the respective meanings given to them in the Circular.

The Circular is being provided to the Shareholders pursuant to applicable Canadian law. In order to become effective, the Arrangement must be approved by (i) at least two thirds (662⁄3%) of the votes cast on the Arrangement Resolution by the Shareholders present or represented by proxy at the Meeting, voting as a single class and (ii) a simple majority (more than 50%) of the votes cast by the Shareholders present or represented by proxy at the Meeting, excluding for the purposes of (ii), the votes attached to the Excluded Shares required to be excluded under MI 61-101.

Under the terms of the Plan of Arrangement, each outstanding Share, other than (i) Shares owned by BREIT Shareholder and (ii) Shares with respect to which a Shareholder has duly and validly exercised Dissent Rights, shall, without any further action by or on behalf of a holder of such Shares, be deemed to be assigned and transferred by the holder thereof to the Purchaser, and be entitled to receive US$11.25 in cash for each Share held, subject to applicable withholdings.

The Arrangement remains subject to the satisfaction or waiver of the conditions set forth in the Arrangement Agreement, including the approval and adoption of the Arrangement Resolution by the Shareholders, the grant of the Final Order by the Ontario Superior Court of Justice (Commercial List) approving the Arrangement and the Required Regulatory Approvals.

The cross-references below are being supplied pursuant to General Instruction F to Schedule 13E-3 and show the location in the Circular of the information required to be included in response to the items of Schedule 13E-3. Pursuant to General Instruction F to Schedule 13E-3, the information contained in the Circular, including all appendices thereto, is incorporated herein by reference, in its entirety and the responses to each item in this Schedule 13E-3 are qualified in their entirety by the information contained in the Circular and the appendices thereto.

A special committee of the Board of Directors of the Corporation (the “Board of Directors” or the “Board”) consisting entirely of independent directors (the “Special Committee”), conducted, with the assistance of its independent financial and legal advisors, a review of the Corporation’s operations and

financing needs and alternatives available to the Corporation and obtained an independent formal valuation of the Shares. Following this process, and after careful consideration, the Board (other than Frank Cohen, being the director on the Board appointed by Blackstone, who recused himself from the deliberations regarding the transactions contemplated hereby), acting on the unanimous recommendation of the Special Committee and after receiving legal and financial advice, (i) determined it would be in the best interests of the Corporation to enter into the Arrangement Agreement and that the Arrangement and the transactions contemplated thereby are fair to the Shareholders (other than Blackstone), (ii) resolved to unanimously recommend that the Shareholders vote in favour of the Arrangement Resolution, and (iii) authorized the entering into the Arrangement Agreement and the performance by Corporation of its obligations under the Arrangement Agreement.

All information concerning the Corporation contained in, or incorporated by reference into this Schedule 13E-3 and the Circular was supplied by the Corporation. Similarly, all information concerning each other Filing Person contained in, or incorporated by reference into this Schedule 13E-3 and the Circular was supplied by such Filing Person. No Filing Person, including the Corporation, is responsible for the accuracy or completeness of any information supplied by any other Filing Person.

Item 1. Summary Term Sheet

The information set forth in the Circular under the following captions is incorporated herein by reference:

“Summary of Arrangement”

“Questions and Answers About the Shareholder Meeting and the Arrangement”

Item 2. Subject Company Information

(a) Name and Address.

The name of the subject company is Tricon Residential Inc. The address and telephone number of the subject company’s principal executive office are as follows:

7 St. Thomas Street, Suite 801

Toronto, ON

Canada, M5S 2B7

+1 416-925-7228

The information set forth in the Circular under the caption “Information Concerning Tricon – General” is incorporated herein by reference.

(b) Securities.

The subject class of equity securities is common shares, no par value, of the Corporation. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Information Concerning the Shareholder Meeting and Voting – Voting Common Shares”

“The Arrangement”

“The Arrangement – Company Shareholder Approvals of the Arrangement”

“Information Concerning Tricon – Description of Share Capital”

(c) Trading Market and Price. The information set forth in the Circular under the following captions in incorporated herein by reference:

“Special Factors – Certain Effects of the Arrangement”

“Information Concerning Tricon – Trading in Shares”

“Arrangement Agreement – Agreement to Take Certain Actions”

“Certain Legal Matters – Securities Law Matters – Stock Exchange Delisting and Reporting Issuer Status”

“Certain Canadian Federal Income Tax Considerations – Holders Not Resident in Canada – Taxable Canadian Property”

(d) Dividends. The information set forth in the Circular under the caption “Information Concerning Tricon – Dividend Policy” is incorporated herein by reference.

(e) Prior Public Offerings. The information set forth in the Circular under the caption “Information Concerning Tricon – Previous Distributions” is incorporated herein by reference.

(f) Prior Stock Purchases. The information set forth in the Circular under the caption “Information Concerning Tricon – Previous Purchases and Sales” is incorporated herein by reference.

Item 3. Identity and Background of Filing Person

(a) – (c) Name and Address; Business and Background of Entities; Business and Background of Natural Persons.

The information set forth in the Circular under the following captions is incorporated herein by reference:

“Summary of Arrangement – Parties to the Arrangement”

“Information Concerning the Purchaser and Blackstone”

“Information Concerning Tricon – General”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement – Ownership of Securities”

“Exhibit “B” – Directors, Executive Officers and Control Persons of the Blackstone Filing Parties”

“Exhibit “C” – Directors and Executive Officers of the Company”

Item 4. Terms of the Transaction

(a)(1) Material Terms. Tender Offers.

Not applicable.

(a)(2) Material Terms. Mergers or Similar Transactions. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Purpose of the Shareholder Meeting”

“Summary of Arrangement – Summary of the Arrangement”

“Summary of Arrangement – Recommendation of the Special Committee”

“Summary of Arrangement – Recommendation of the Unconflicted Company Board”

“Summary of Arrangement – Reasons for the Recommendation”

“Summary of Arrangement – Blackstone Filing Parties’ Purposes and Reasons for the Arrangement”

“Summary of Arrangement – Required Company Shareholder Approvals”

“Summary of Arrangement – MI 61-101 Requirements”

“Summary of Arrangement – Procedural Safeguards for Company Shareholders”

“Summary of Arrangement – Certain Canadian Federal Income Tax Considerations”

“Summary of Arrangement – Certain U.S. Federal Income Tax Considerations”

“Special Factors – Background to the Arrangement”

“Special Factors – Tricon’s Purposes and Reasons for the Arrangement”

“Special Factors – Recommendation of the Special Committee and the Unconflicted Company Board; Position of Tricon as to Fairness of the Arrangement”

“Special Factors – Scotia Capital Formal Valuation and Fairness Opinion”

“Special Factors – Morgan Stanley Fairness Opinion”

“Special Factors – Blackstone Filing Parties’ Purposes and Reasons for the Arrangement”

“Special Factors – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

“Special Factors – Certain Effects of the Arrangement”

“Information Concerning the Shareholder Meeting and Voting – Voting Common Shares”

“The Arrangement – Overview”

“The Arrangement – Company Shareholder Approvals of the Arrangement”

“The Arrangement – Implementation of the Arrangement”

“The Arrangement – Payment of Consideration”

“The Arrangement – Accounting Treatment of the Arrangement”

“Arrangement Agreement – Agreement to Take Certain Actions”

“Risk Factors – Risks Related to the Arrangement – Rights of Former Company Shareholders after the Arrangement”

“Risk Factors – Risks Related to the Arrangement – The Resulting Tax Payable by Most Company Shareholders”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement – Ownership of Securities”

“Certain Canadian Federal Income Tax Considerations”

“Certain U.S. Federal Income Tax Considerations”

(c) Different Terms. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Summary of Arrangement – Blackstone Filing Parties’ Purposes and Reasons for the Arrangement”

“Summary of Arrangement – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

“Summary of Arrangement – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

“Special Factors – Certain Effects of the Arrangement – Benefits and Detriments of the Arrangement for Directors and Executive Officers of the Company”

“Information Concerning the Purchaser and Blackstone”

“Risk Factors – Risks Related to the Arrangement – Interests of Certain Persons in the Arrangement”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

(d) Appraisal Rights. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Implementation of the Arrangement”

“Summary of Arrangement – Dissent Rights”

“The Arrangement – Implementation of the Arrangement”

“Certain Canadian Federal Income Tax Considerations – Holders Resident in Canada – Dissenting Resident Holders of Common Shares”

“Certain Canadian Federal Income Tax Considerations – Holders Not Resident in Canada – Dissenting Non-Resident Holders”

“Certain U.S. Federal Income Tax Considerations – Consequences to Dissenting U.S. Company Shareholders”

“Dissenting Shareholders’ Rights”

“Appendix “E”: Interim Order”

“Appendix “G”: Section 185 of the Business Corporations Act (Ontario)”

(e) Provisions for Unaffiliated Security Holders. The information set forth in the Circular under the following captions is incorporated herein by reference:

“The Arrangement – Arrangements between Tricon and Security Holders”

“Provisions for Unaffiliated Security Holders”

(f) Eligibility for Listing or Trading.

Not applicable.

Item 5. Past Contacts, Transactions, Negotiations and Agreements

(a)(1)-(2) Transactions. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Special Factors – Background to the Arrangement”

“Information Concerning Tricon – Previous Purchases and Sales”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

(b) – (c) Significant Corporate Events; Negotiations or Contacts. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Special Factors – Background to the Arrangement”

“Summary of Arrangement – Support Agreement”

“The Arrangement – Support Agreement”

“The Arrangement – Intentions of Directors and Executive Officers”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement – Employment Arrangements”

“Appendix “B”: Plan of Arrangement Under Section 182 of the Business Corporations Act (Ontario)”

(e) Agreements Involving the Subject Company’s Securities. The information set forth in the Circular Statement under the following captions is incorporated herein by reference:

“Special Factors – Background to the Arrangement”

“Summary of Arrangement – Support Agreement”

“Summary of Arrangement – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

“The Arrangement – Support Agreement”

“The Arrangement – Intentions of Directors and Executive Officers”

“Information Concerning the Purchaser and Blackstone – Agreements Involving the Company Securities”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

“Appendix “B”: Plan of Arrangement Under Section 182 of the Business Corporations Act (Ontario)”

Item 6. Purposes of the Transaction and Plans or Proposals

(b) Use of Securities Acquired. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Blackstone Filing Parties’ Purposes and Reasons for the Arrangement”

“Special Factors – Certain Effects of the Arrangement – Benefits and Detriments of the Arrangement for the Blackstone Filing Parties”

“The Arrangement – Implementation of the Arrangement”

“Certain Legal Matters – Implementation of the Arrangement and Timing”

(c)(1) – (8) Plans. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Summary of Arrangement – Stock Exchange Delisting and Reporting Issuer Status”

“Special Factors – Certain Effects of the Arrangement”

“The Arrangement – Arrangements between Tricon and Security Holders”

“Arrangement Agreement – Agreement to Take Certain Actions”

“Arrangement Agreement – Employee Matters”

“Information Concerning Tricon – Material Changes in the Affairs of the Company”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

“Certain Legal Matters – Securities Law Matters – Stock Exchange Delisting and Reporting Issuer Status”

“Risk Factors – Risks Related to the Arrangement – Interests of Certain Persons in the Arrangement”

“Appendix “B”: Plan of Arrangement Under Section 182 of the Business Corporations Act (Ontario)”

Item 7. Purposes, Alternatives, Reasons and Effects

(a) Purposes. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Reasons for the Recommendation”

“Summary of Arrangement – Blackstone Filing Parties’ Purposes and Reasons for the Arrangement”

“Special Factors – Background to the Arrangement”

“Special Factors – Tricon’s Purposes and Reasons for the Arrangement”

“Special Factors – Recommendation of the Special Committee and the Unconflicted Company Board; Position of Tricon as to Fairness of the Arrangement”

“Special Factors – Blackstone Filing Parties’ Purposes and Reasons for the Arrangement”

“Special Factors – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

(b) Alternatives. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Reasons for the Recommendation”

“Special Factors – Recommendation of the Special Committee and the Unconflicted Company Board; Position of Tricon as to Fairness of the Arrangement”

“Special Factors – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

(c) Reasons. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Recommendation of the Special Committee”

“Summary of Arrangement – Recommendation of the Unconflicted Company Board”

“Summary of Arrangement – Reasons for the Recommendation”

“Summary of Arrangement – Blackstone Filing Parties’ Purposes and Reasons for the Arrangement”

“Summary of Arrangement – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

“Special Factors – Background to the Arrangement”

“Special Factors – Tricon’s Purposes and Reasons for the Arrangement”

“Special Factors – Recommendation of the Special Committee and the Unconflicted Company Board; Position of Tricon as to Fairness of the Arrangement”

“Special Factors – Blackstone Filing Parties’ Purposes and Reasons for the Arrangement”

“Special Factors – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

(d) Effects. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Summary of the Arrangement”

“Summary of Arrangement – Reasons for the Recommendation”

“Summary of Arrangement – Blackstone Filing Parties’ Purposes and Reasons for the Arrangement”

“Summary of Arrangement – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

“Summary of Arrangement – Implementation of the Arrangement”

“Summary of Arrangement – Certain Canadian Federal Income Tax Considerations”

“Summary of Arrangement – Certain U.S. Federal Income Tax Considerations”

“Summary of Arrangement – Stock Exchange Delisting and Reporting Issuer Status”

“Summary of Arrangement – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

“Special Factors – Certain Effects of the Arrangement”

“The Arrangement – Implementation of the Arrangement”

“The Arrangement – Payment of Consideration”

“Arrangement Agreement – Agreement to Take Certain Actions”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

“Certain Legal Matters – Securities Law Matters – Stock Exchange Delisting and Reporting Issuer Status”

“Risk Factors – Risks Related to the Arrangement – Rights of Former Company Shareholders after the Arrangement”

“Risk Factors – Risks Related to the Arrangement – The Resulting Tax Payable by Most Company Shareholders”

“Certain Canadian Federal Income Tax Considerations”

“Certain U.S. Federal Income Tax Considerations”

“Appendix “B”: Plan of Arrangement under Section 182 of the Business Corporations Act (Ontario)”

Item 8. Fairness of the Transaction

(a), (b) Fairness; Factors Considered in Determining Fairness. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Recommendation of the Special Committee”

“Summary of Arrangement – Recommendation of the Unconflicted Company Board”

“Summary of Arrangement – Reasons for the Recommendation”

“Summary of Arrangement – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

“Special Factors – Background to the Arrangement”

“Special Factors – Tricon’s Purposes and Reasons for the Arrangement”

“Special Factors – Recommendation of the Special Committee and the Unconflicted Company Board; Position of Tricon as to Fairness of the Arrangement”

“Special Factors – Scotia Capital Formal Valuation and Fairness Opinion”

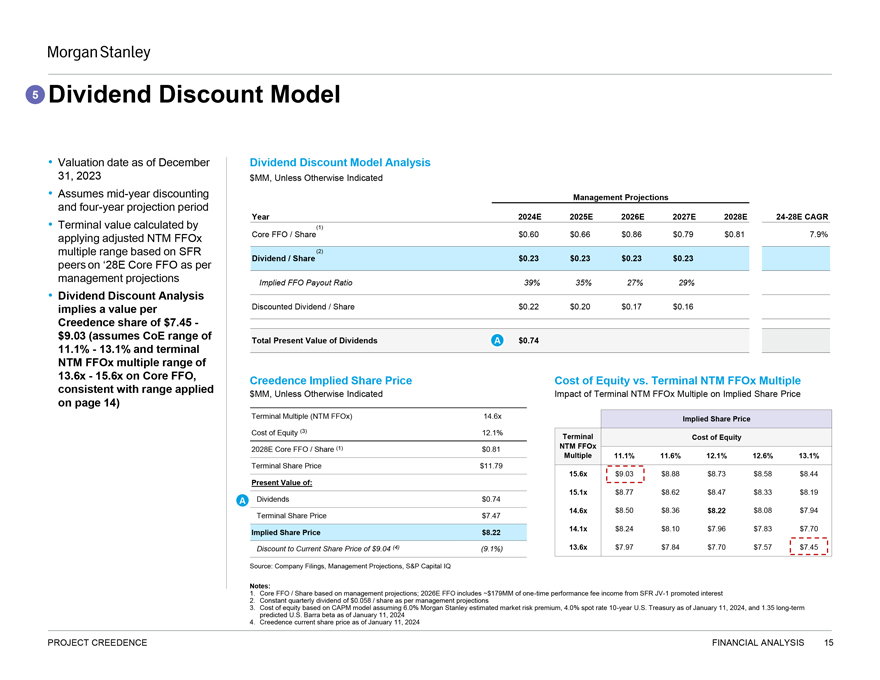

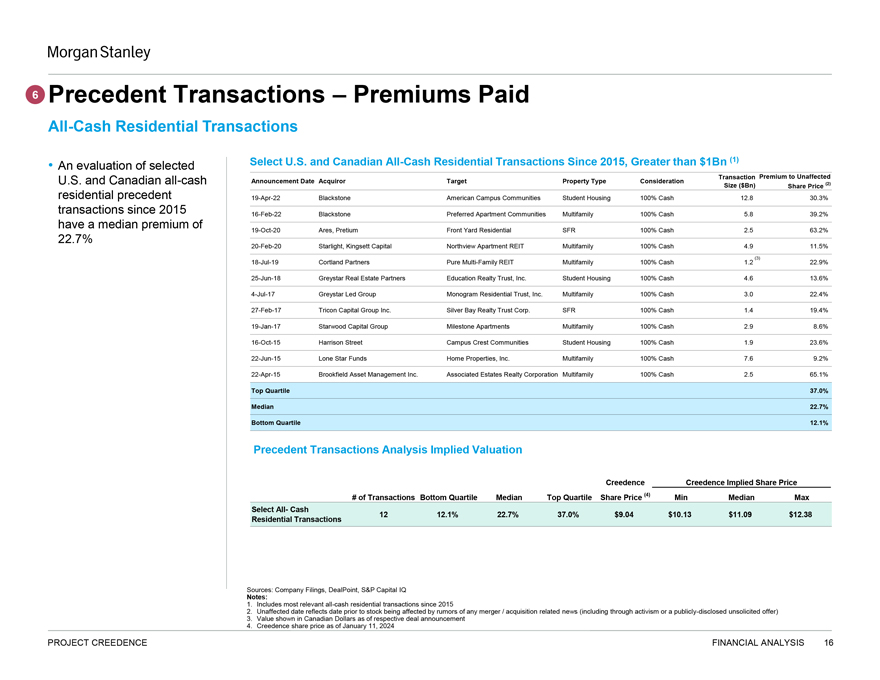

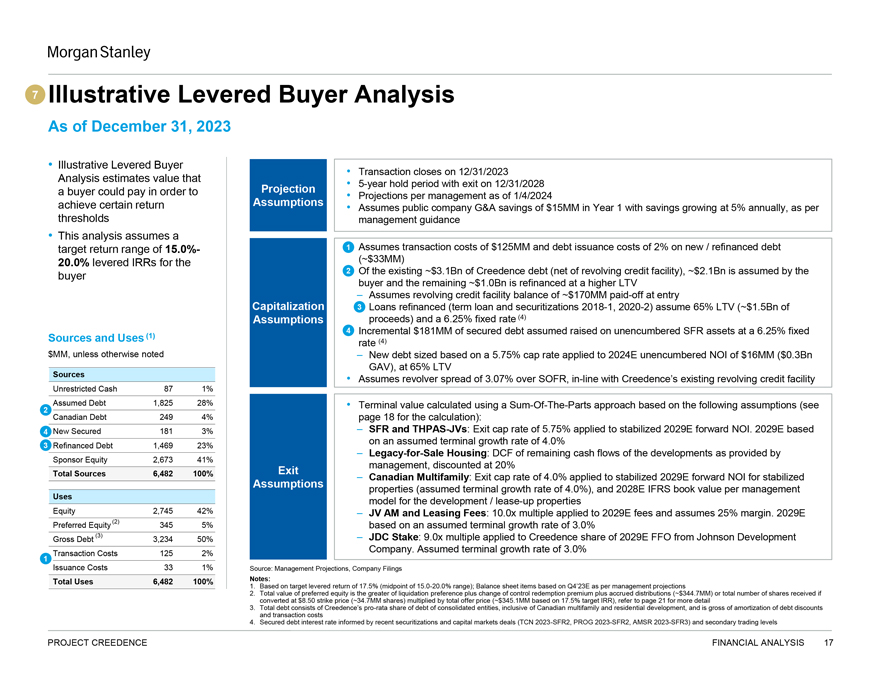

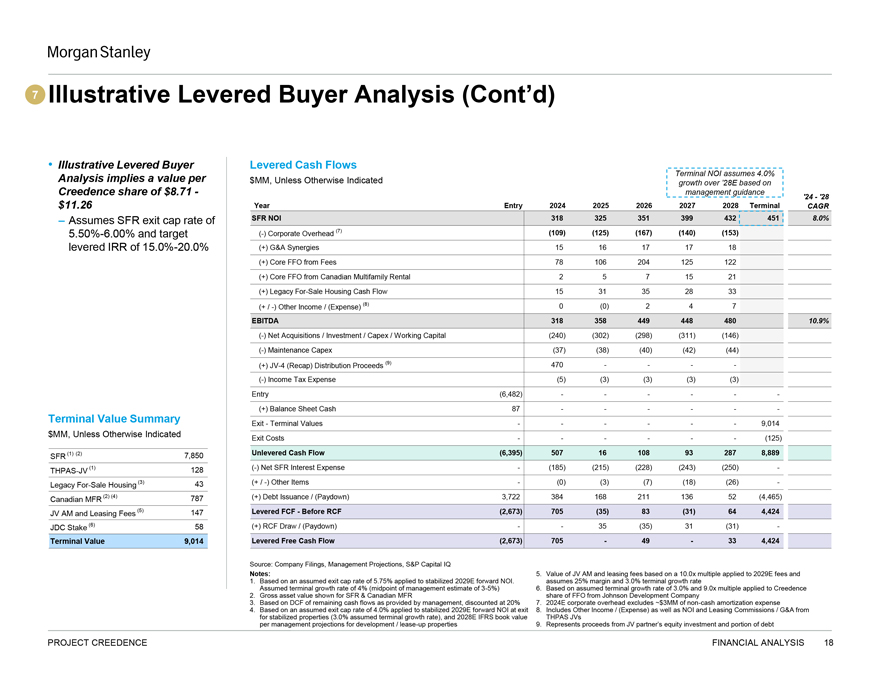

“Special Factors – Morgan Stanley Fairness Opinion”

“Special Factors – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

“Appendix “C”: Formal Valuation and Fairness Opinion of Scotia Capital Inc.”

“Appendix “D”: Fairness Opinion of Morgan Stanley & Co. LLC”

(c) Approval of Security Holders. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Purpose of the Shareholder Meeting”

“Summary of Arrangement – Reasons for the Recommendation”

“Summary of Arrangement – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

“Summary of Arrangement – Required Company Shareholder Approvals”

“Summary of Arrangement – MI 61-101 Requirements”

“Summary of Arrangement – Procedural Safeguards for Company Shareholders”

“Summary of Arrangement – Dissent Rights”

“Special Factors – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

“The Arrangement – Company Shareholder Approvals of the Arrangement”

“Certain Legal Matters – Securities Law Matters – Application of MI 61-101”

“Certain Legal Matters – Securities Law Matters – Minority Approval”

(d) Unaffiliated Representative. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Special Factors – Background to the Arrangement”

“Special Factors – Recommendation of the Special Committee and the Unconflicted Company Board; Position of Tricon as to Fairness of the Arrangement –Recommendation and Reasons of the Special Committee”

“The Arrangement – Arrangements between Tricon and Security Holders”

“Provisions for Unaffiliated Security Holders”

(e) Approval of Directors. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Summary of Arrangement – Recommendation of the Special Committee”

“Summary of Arrangement – Recommendation of the Unconflicted Company Board”

“Summary of Arrangement – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

“Special Factors – Recommendation of the Special Committee and the Unconflicted Company Board; Position of Tricon as to Fairness of the Arrangement”

“Special Factors – Tricon’s Purposes and Reasons for the Arrangement”

“Risk Factors – Risks Related to the Arrangement – Interests of Certain Persons in the Arrangement”

(f) Other Offers. Not applicable.

Item 9. Reports, Opinions, Appraisals and Negotiations

(a) – (c) Report, Opinion or Appraisal; Preparer and Summary of the Report, Opinion or Appraisal; Availability of Documents. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Questions and Answers About the Shareholder Meeting and the Arrangement”

“Summary of Arrangement – Recommendation of the Special Committee”

“Summary of Arrangement – Recommendation of the Unconflicted Company Board”

“Summary of Arrangement – Reasons for the Recommendation”

“Summary of Arrangement – Formal Valuation and Fairness Opinions”

“Special Factors – Background to the Arrangement”

“Special Factors – Scotia Capital Formal Valuation and Fairness Opinion”

“Special Factors – Morgan Stanley Fairness Opinion”

“Information Concerning Tricon – Additional Information”

“Certain Legal Matters – Securities Law Matters – Formal Valuation”

“Consent of Scotia Capital Inc.”

“Consent of Morgan Stanley & Co. LLC”

“Appendix “C”: Formal Valuation and Fairness Opinion of Scotia Capital Inc.”

“Appendix “D”: Fairness Opinion of Morgan Stanley & Co. LLC”

Item 10. Source and Amount of Funds or Other Consideration

(a), (b) Source of Funds; Conditions. The information set forth in the Circular under the caption “The Arrangement – Expenses of the Arrangement” is incorporated herein by reference.

(c) Expenses. The information set forth in the Circular under the following captions is incorporated herein by reference:

“The Arrangement – Expenses of the Arrangement”

“Arrangement Agreement – Financing Cooperation”

(d) Borrowed Funds. The information set forth in the Circular under the caption “The Arrangement – Financing of the Arrangement” is incorporated herein by reference.

Item 11. Interest in Securities of the Subject Company

(a) Securities Ownership. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Information Concerning the Shareholder Meeting and Voting – Principal Company Shareholders”

“The Arrangement – Company Shareholder Approvals of the Arrangement”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement – Ownership of Securities”

(b) Securities Transactions. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Information Concerning Tricon – Previous Purchases and Sales”

“Information Concerning Tricon – Previous Distributions”

Item 12. The Solicitation or Recommendation

(d) Intent to Tender or Vote in a Going-Private Transaction. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Summary of Arrangement – Support Agreement”

“The Arrangement – Support Agreement”

“The Arrangement – Intentions of Directors and Executive Officers”

(e) Recommendation of Others. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Summary of Arrangement – Recommendation of the Special Committee”

“Summary of Arrangement – Recommendation of the Unconflicted Company Board”

“Summary of Arrangement – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

“Special Factors – Recommendation of the Special Committee and the Unconflicted Company Board; Position of Tricon as to Fairness of the Arrangement”

“Special Factors – Position of Blackstone Filing Parties as to the Fairness of the Arrangement”

Item 13. Financial Statements

(a) Financial Information. The audited financial statements of the Corporation for the fiscal years ended December 31, 2022 and 2021 are incorporated herein by reference to the Corporation’s Amendment No. 1 to Form 40-F for the fiscal year ended December 31, 2022, filed on March 2, 2023 (see Exhibit 99.3 thereto). The interim financial statements of the Corporation are incorporated herein by reference to Exhibit 99.1 to the Corporation’s report on Form 6-K furnished on November 7, 2023.

The information set forth in the Circular under the following captions is incorporated herein by reference:

“Information Concerning Tricon – Selected Historical Financial Information”

“Information Concerning Tricon – Net Book Value”

“Information Concerning Tricon – Additional Information”

(b) Pro Forma Information. Not applicable.

(c) Summary Information. The information set forth in the Circular under the caption “Information Concerning Tricon– Selected Historical Financial Information” is incorporated herein by reference.

Item 14. Persons/Assets, Retained, Employed, Compensated or Used

(a) Solicitations or Recommendations. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Information Concerning the Shareholder Meeting and Voting – Solicitation of Proxies”

“The Arrangement – Expenses of the Arrangement”

(b) Employees and Corporate Assets. The information set forth in the Circular under the following captions is incorporated herein by reference:

“Information Concerning the Meeting and Voting – Solicitation of Proxies”

“The Arrangement – Expenses of the Arrangement”

“Certain Legal Matters – Interest of Certain Persons in the Arrangement; Benefits from the Arrangement”

Item 15. Additional Information

(b) Golden Parachute Compensation. Not applicable.

(c) Other Material Information. The entirety of the Circular, including all appendices thereto, is incorporated herein by reference.

Item 16. Exhibits

The following exhibits are filed herewith:

SIGNATURES

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

| TRICON RESIDENTIAL INC. | ||

| By: |

/s/ David Veneziano | |

| Name: David Veneziano | ||

| Title: Executive Vice President and Chief Legal Officer | ||

Date: February 16, 2024

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

| CREEDENCE ACQUISITION ULC | ||

| By: |

/s/ Jacob Werner | |

| Name: Jacob Werner | ||

| Title: Director | ||

Date: February 16, 2024

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

| BCORE PREFERRED HOLDCO LLC | ||

| By: |

/s/ Jacob Werner | |

| Name: Jacob Werner | ||

| Title: Senior Managing Director | ||

Date: February 16, 2024

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

| BLACKSTONE REAL ESTATE PARTNERS X L.P. | ||

| By: Blackstone Real Estate Associates X L.P., its general partner | ||

| By: BREA X L.L.C., its general partner | ||

| By: |

/s/ Jacob Werner | |

| Name: Jacob Werner | ||

| Title: Senior Managing Director | ||

Date: February 16, 2024

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

| BLACKSTONE REAL ESTATE INCOME TRUST, INC. | ||

| By: |

/s/ Jacob Werner | |

| Name: Jacob Werner | ||

| Title: Senior Managing Director | ||

Date: February 16, 2024

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

| BREIT OPERATING PARTNERSHIP L.P. | ||

| By: Blackstone Real Estate Income Trust, Inc., its general partner | ||

| By: |

/s/ Jacob Werner | |

| Name: Jacob Werner | ||

| Title: Senior Managing Director | ||

Date: February 16, 2024

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

| CREEDENCE INTERMEDIATE HOLDINGS INC. | ||

| By: |

/s/ Jacob Werner | |

| Name: Jacob Werner | ||

| Title: Director | ||

Date: February 16, 2024

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

| BLACKSTONE REAL ESTATE ASSOCIATES X L.P. | ||

| By: BREA X L.L.C., its general partner | ||

| By: |

/s/ Jacob Werner | |

| Name: Jacob Werner | ||

| Title: Senior Managing Director | ||

Date: February 16, 2024

Exhibit (a)(2)(i)

These materials are important and require your immediate attention. They require shareholders of Tricon Residential Inc. to make important decisions. If you are in doubt about how to make such decisions, please contact your financial, legal, tax or other professional advisors. If you are a shareholder of Tricon Residential Inc. and have any questions regarding the information contained in this management information circular or require assistance in completing your form of proxy, please contact our proxy solicitation agent and shareholder communications advisor, Laurel Hill Advisory Group, at 1-877-452-7184 (toll-free within North America) or by calling 1-416-304-0211 (outside of North America) or by email at assistance@laurelhill.com. Questions on how to complete the letter of transmittal should be directed to Tricon Residential Inc.’s transfer agent, TSX Trust Company, at 1-866-600-5869 (toll-free within North America) or at 416-342-1091 (outside of North America) or by email at txstis@tmx.com.

Company Shareholders in the United States should read the section “Notice to Company Shareholders in the United States” on page (iv) of the accompanying management information circular.

ARRANGEMENT INVOLVING

TRICON RESIDENTIAL INC.

AND

CREEDENCE ACQUISITION ULC

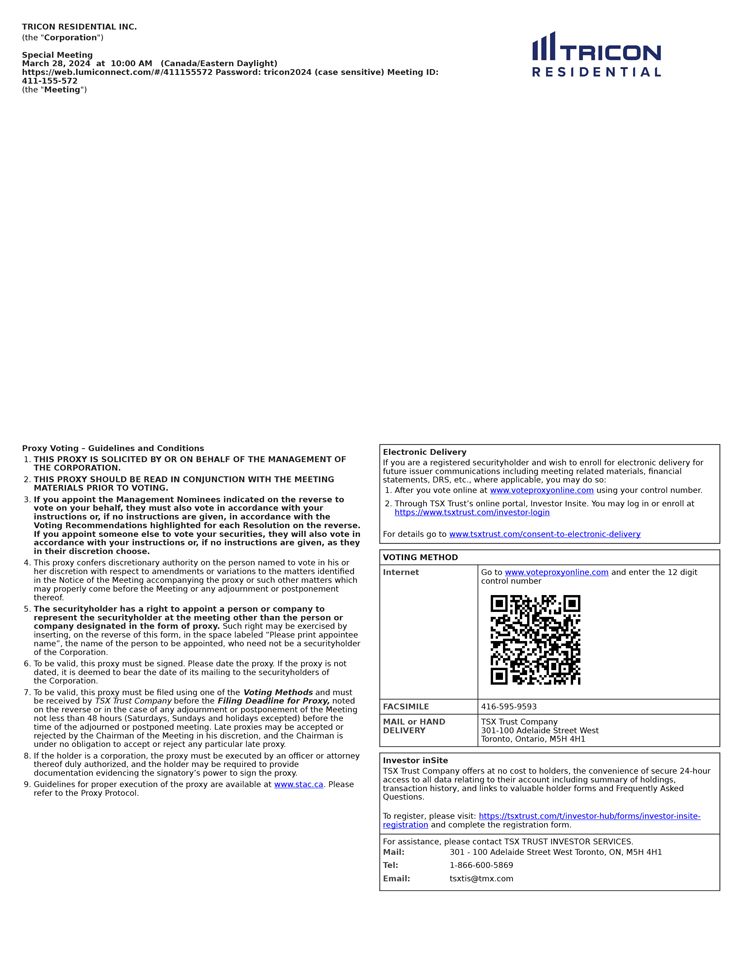

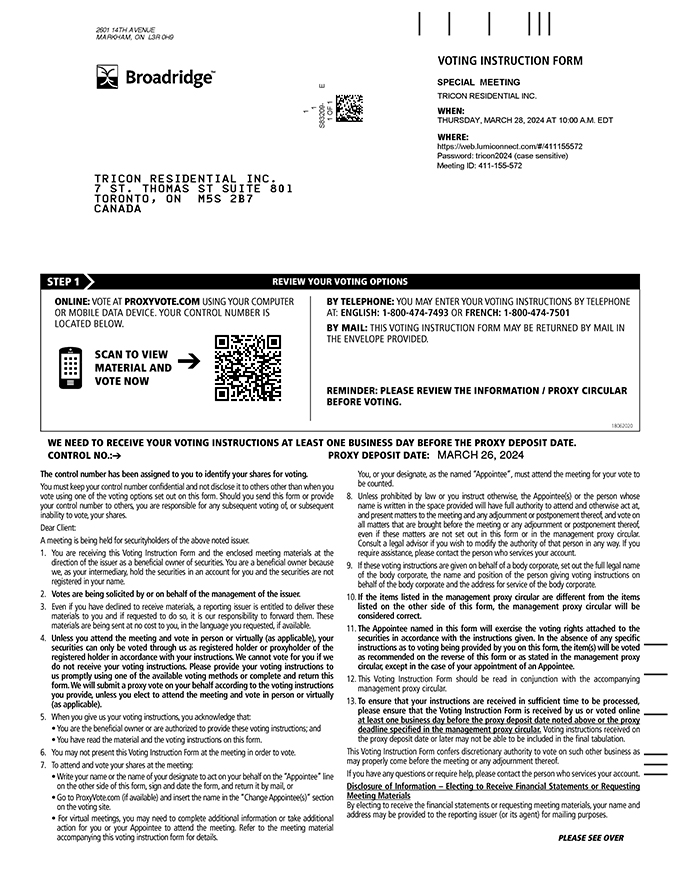

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

to be held on Thursday, March 28, 2024 at 10:00 a.m. (Toronto time)

virtually via live audio webcast at https://web.lumiconnect.com/#/411155572

Password: tricon2024 (case sensitive) and Meeting ID: 411-155-572

AND

MANAGEMENT INFORMATION CIRCULAR

YOUR VOTE IS IMPORTANT. TAKE ACTION AND VOTE TODAY.

The Unconflicted Company Board, acting on the unanimous recommendation of the Special Committee, unanimously

recommends that Company Shareholders vote

FOR

the Arrangement Resolution

NEITHER THE U.S. SECURITIES AND EXCHANGE COMMISSION NOR THE SECURITIES REGULATORY AUTHORITY IN ANY STATE IN THE UNITED STATES HAS APPROVED OR DISAPPROVED OF THE ARRANGEMENT OR PASSED UPON THE FAIRNESS OR MERITS OF THE ARRANGEMENT, NOR HAS THE U.S. SECURITIES AND EXCHANGE COMMISSION OR THE SECURITIES REGULATORY AUTHORITIES OF ANY STATE IN THE UNITED STATES PASSED ON THE ADEQUACY OR ACCURACY OF THIS CIRCULAR. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENCE. IN ADDITION, NEITHER THE TORONTO STOCK EXCHANGE NOR ANY CANADIAN SECURITIES REGULATORY AUTHORITY HAS IN ANY WAY PASSED UPON THE MERITS OF THE TRANSACTION DESCRIBED IN THIS CIRCULAR, AND ANY REPRESENTATION OTHERWISE IS AN OFFENCE.

February 15, 2024

LETTER TO COMPANY SHAREHOLDERS

February 15, 2024

Dear Company Shareholders:

You are invited to attend a special meeting of holders of common shares (the “Company Shareholders”) of Tricon Residential Inc. (“Tricon” or the “Company”) to be held virtually on Thursday, March 28, 2024 at 10:00 a.m. (Toronto time) (the “Shareholder Meeting”). The purpose of the Shareholder Meeting is to allow Company Shareholders to consider the proposed acquisition by Creedence Acquisition ULC (the “Purchaser”), an entity formed to effect the acquisition of the Company by Blackstone Real Estate Partners X L.P. (“BREP X”) and Blackstone Real Estate Income Trust, Inc. (“BREIT”, and collectively with BREP X and their respective affiliates, including the Purchaser, “Blackstone”), of all of the common shares of Tricon (each, a “Common Share”) not currently owned by Blackstone pursuant to which each Company Shareholder (other than Blackstone and any dissenting Company Shareholders) will be entitled to receive US$11.25 in cash per Common Share (the “Consideration”) by way of a Court-approved statutory plan of arrangement (the “Arrangement”) pursuant to the provisions of the Business Corporations Act (Ontario).

A special committee of the Board of Directors of the Company (the “Company Board”) consisting entirely of independent directors (the “Special Committee”) conducted, with the assistance of its independent financial and legal advisors, a review of the Company’s operations and financing needs and alternatives available to the Company and obtained an independent valuation of the Common Shares. Following this process, and after careful consideration, the Special Committee unanimously recommended that the Unconflicted Company Board (as defined below) determine that the Arrangement is in the best interests of the Company and fair to the Company Shareholders (excluding Blackstone) and that the Company Board approve the Arrangement and recommend that the Company Shareholders vote FOR the Arrangement Resolution (as defined below).

The Company Board, with Frank Cohen (being the director on the Company Board appointed by Blackstone) having recused himself (the “Unconflicted Company Board”), after receiving the unanimous recommendation of the Special Committee and in consultation with its independent financial and legal advisors, determined that the Arrangement is in the best interests of the Company and fair to the Company Shareholders (excluding Blackstone) and unanimously recommends that the Company Shareholders vote FOR the Arrangement Resolution.

In reaching its recommendation, the Special Committee took into consideration, among other things, the following:

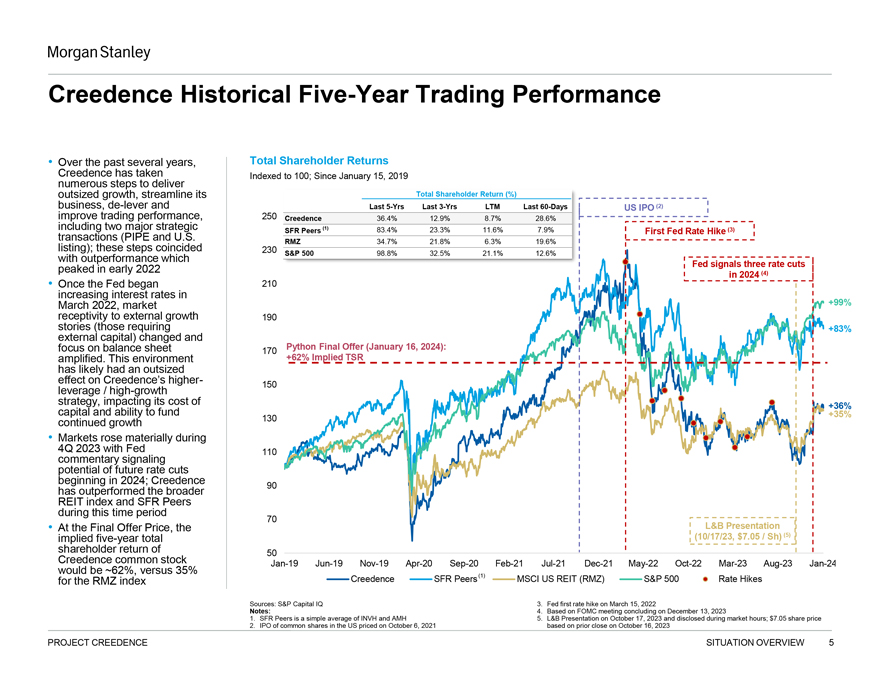

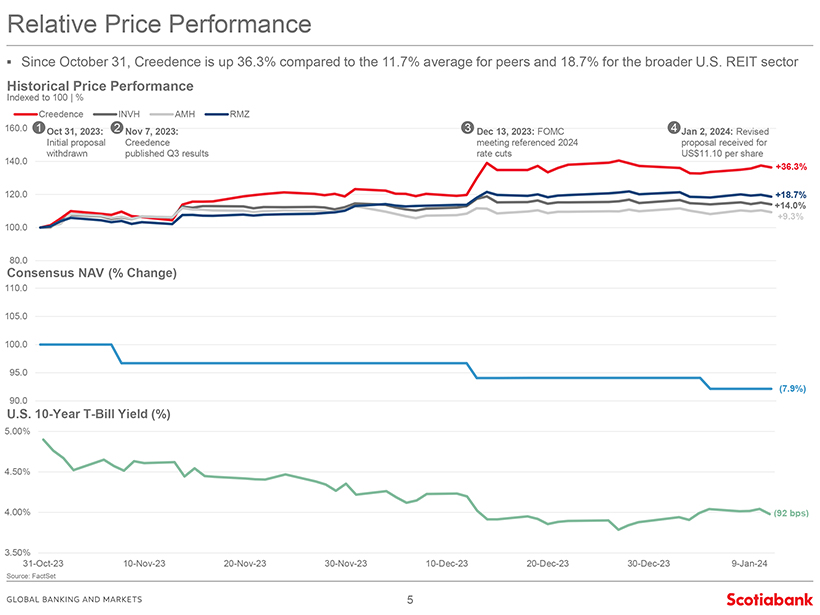

| • | Significant premium to market price. The Consideration of $11.25 per Common Share in cash represents a premium of approximately 30% to the closing price of the Common Shares on the New York Stock Exchange (“NYSE”) as of January 18, 2024, the last trading day prior to the public announcement of the Arrangement, and a premium of approximately 42% to the volume weighted average share price on the NYSE over the 90-day period ended January 18, 2024. |

| • | Certainty of value of cash consideration. The Consideration to be received by Company Shareholders is payable entirely in cash, providing Company Shareholders with certainty of value and liquidity immediately upon the closing of the Arrangement, in comparison to the risks, uncertainties and longer potential timeline for realizing equivalent value from the Company Board-approved strategic plan or possible strategic alternatives involving transactions in which all or a portion of the consideration would be payable in equity or would require a series of transactions involving sales of properties to separate acquirors. |

| • | Transaction represents compelling value relative to alternatives. Prior to entering into the Arrangement Agreement, the Special Committee and the Unconflicted Company Board, with the assistance of their financial and legal advisors, and based upon their collective knowledge of the business, operations, financial condition, earnings and prospects of the Company, as well as their collective knowledge of the current and prospective environment in which the Company operates (including economic and market conditions), assessed the relative benefits and risks to the Company’s security holders, employees and residents of various alternatives reasonably available to the Company, including continued execution of the Company’s existing Company Board-approved strategic plan and the possibility of soliciting other potential buyers of the Company. As part of that evaluation process, the Special Committee unanimously was of the view that: |

| ○ | the Consideration represents greater value for the Company Shareholders than would reasonably be expected from the continued execution of the Company Board-approved strategic plan; |

| ○ | contacting other bidders before announcing a transaction would result in significant risks to the Company and its business, including the risk that it could jeopardize the availability of the Blackstone proposal and that market leaks and rumours regarding a potential transaction would disrupt relationships with joint venture partners, jeopardize transactions currently in the pipeline, risk employee turnover, increase turnover in the Company Shareholder base and lead to potential Common Share price volatility; and |

| ○ | there exists a limited universe of potential third parties with an interest in acquiring the Company, and it is unlikely that any other party would be willing to acquire the Company on terms that are more favourable to Company Shareholders, from a financial point of view, than the Arrangement, due to the size and varied nature of the Company’s portfolio and business lines, the Company’s cross border structure and the fact that leverage constraints could impact the price that public company bidders may be able to pay. |

| • | Rigorous arm’s length negotiation process. The Arrangement Agreement is the result of a rigorous arm’s length negotiation process that was undertaken with the oversight and participation of the Special Committee and the Unconflicted Company Board and their financial and legal advisors which included price increases by Blackstone from its initial proposed price of $11.00 per Common Share. The Special Committee concluded that $11.25 per Common Share is the highest price that Blackstone was willing to pay to acquire the Company. |

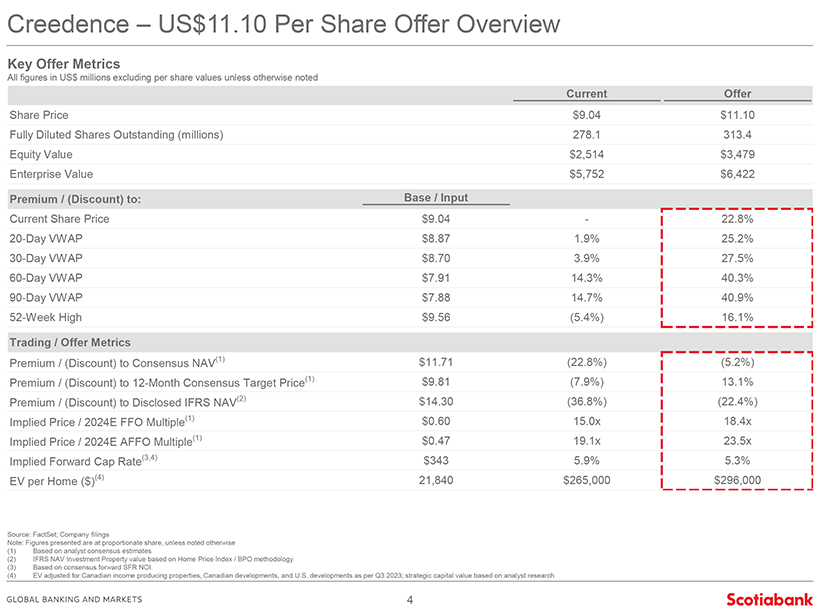

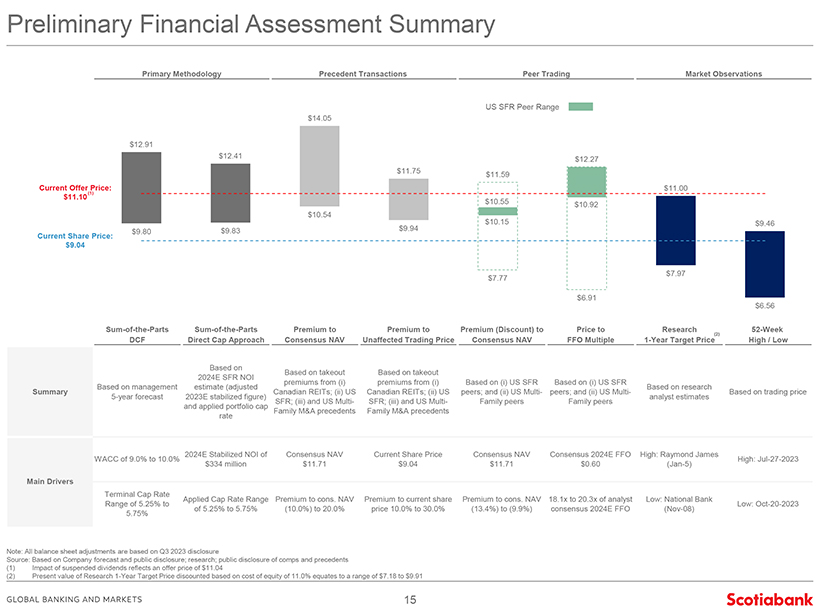

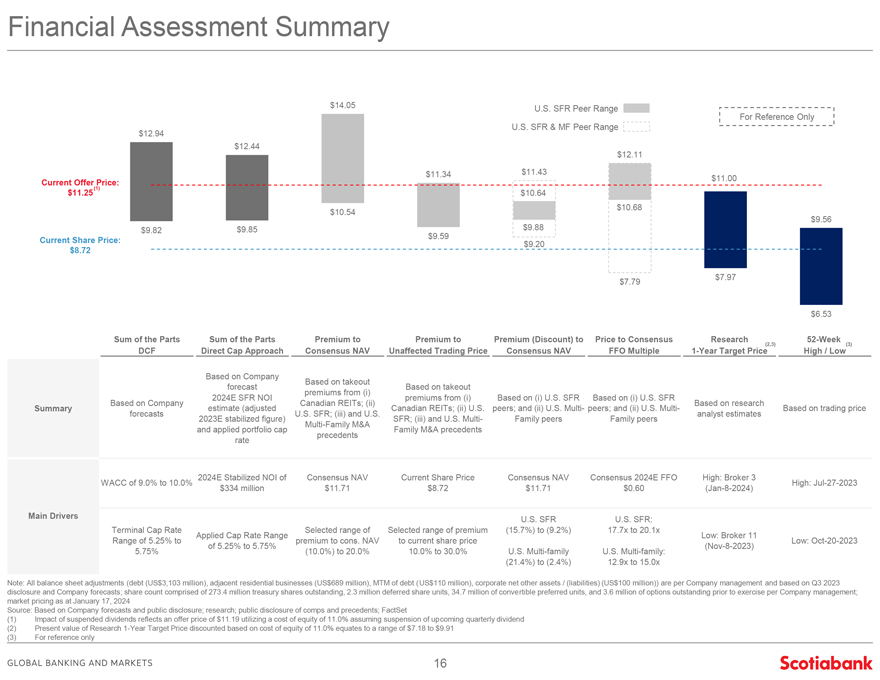

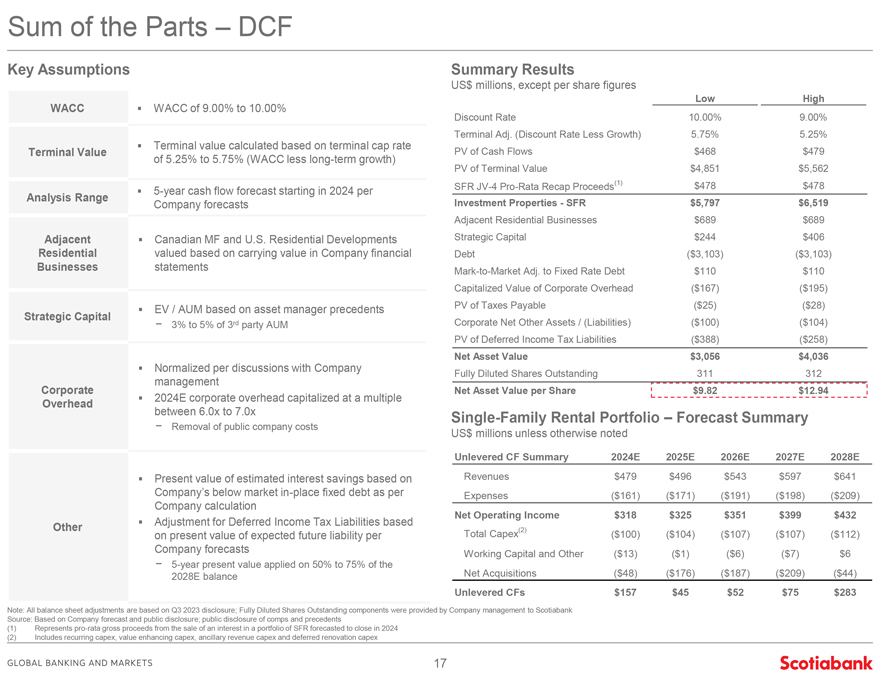

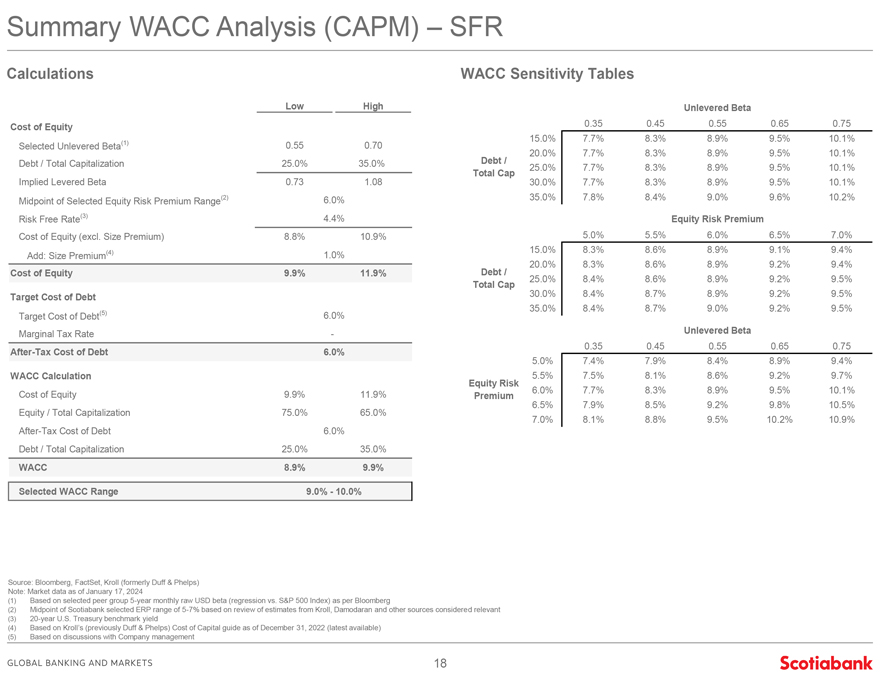

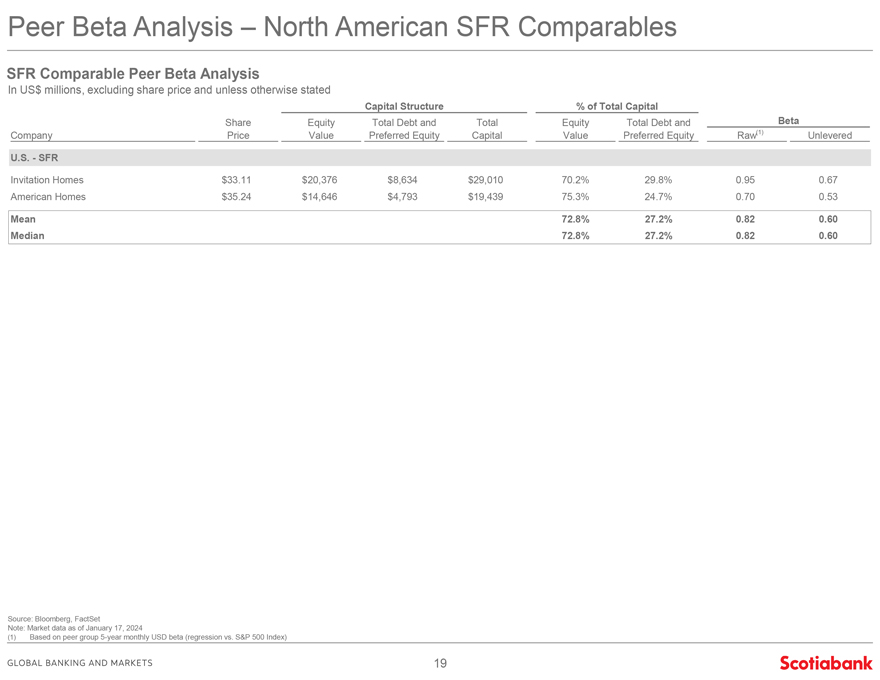

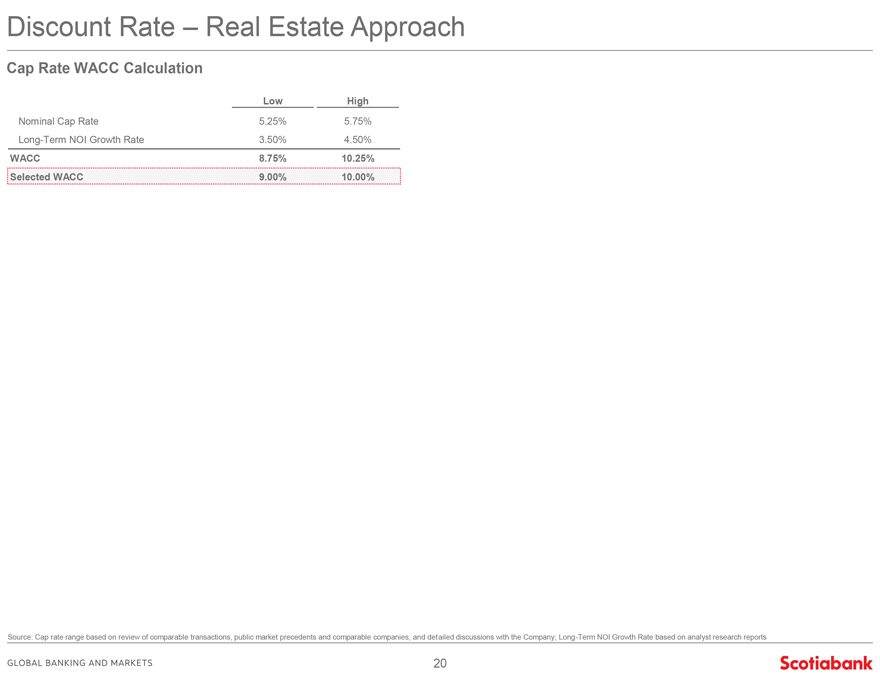

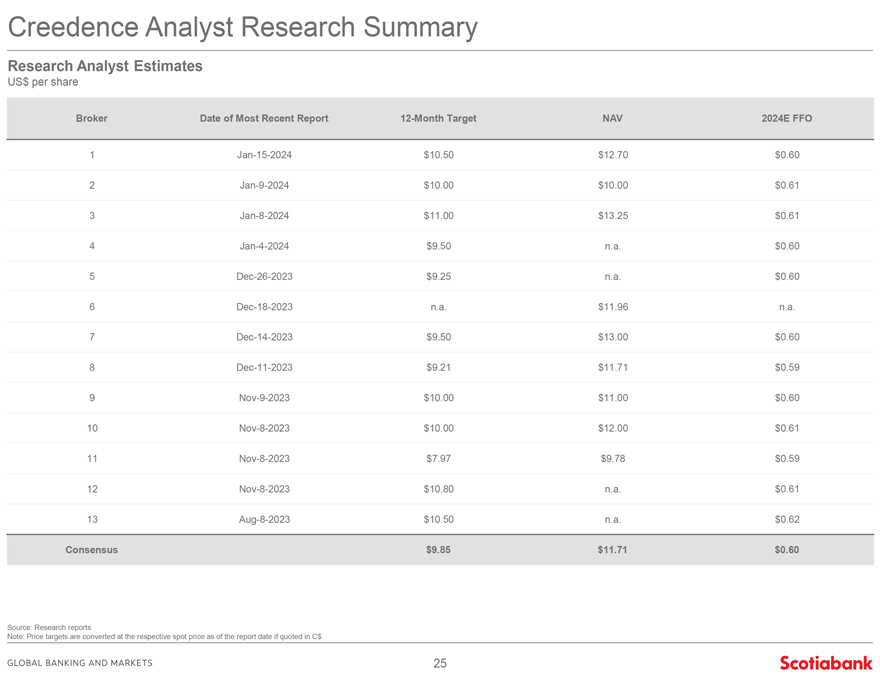

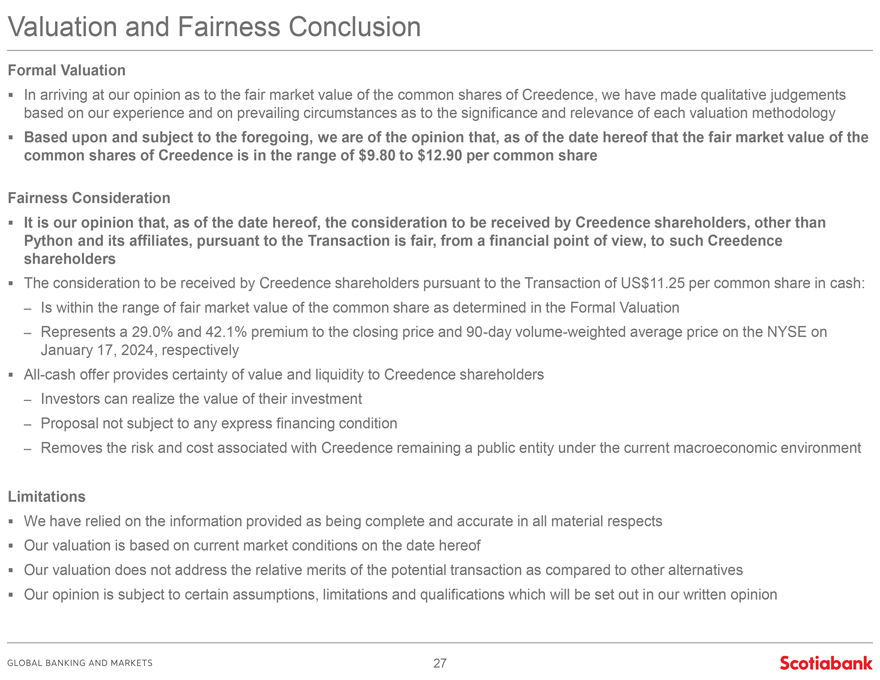

| • | Scotia Capital Formal Valuation and Fairness Opinion. The Special Committee received a formal valuation and fairness opinion from Scotia Capital Inc., which states that, as of the date thereof, and based upon and subject to the analyses, assumptions, limitations and qualifications set out therein: (i) the fair market value of a Common Share is in the range of $9.80 to $12.90 per Common Share, and (ii) the Consideration to be received by the Company Shareholders (excluding Blackstone) pursuant to the Arrangement is fair, from a financial point of view, to the Company Shareholders (excluding Blackstone). |

| • | Blackstone’s reputation and track record of closing transactions. The Special Committee concluded that it is likely that Blackstone will complete the Arrangement if all conditions are satisfied given (i) Blackstone’s proven ability to complete large acquisition transactions, including substantial experience with take-private transactions, (ii) Blackstone’s extensive experience in the real estate industry, (iii) Blackstone’s substantial available capital and (iv) the Purchaser Termination Fee of $526 million payable to the Company if the Arrangement Agreement is terminated in certain circumstances (representing approximately 15% of the Company’s equity value (assuming the exchange of all Preferred Units)), $466.843 million of which payment is guaranteed by BREP X and $59.157 million of which payment is guaranteed by BREIT Operating Partnership L.P. |

| • | Reasonable timeline to closing. The Arrangement is structured as a statutory plan of arrangement under the Business Corporations Act (Ontario). The completion of the Arrangement is expected to occur in the second quarter of this year, and is subject to customary closing conditions, including court approval, the approval of the Company Shareholders and required regulatory approvals under the Competition Act (Canada) and Investment Canada Act. |

- ii -

The negotiations leading to the execution and announcement of the Arrangement Agreement were supervised by the Special Committee, which was comprised solely of independent directors and advised by experienced and qualified independent financial and legal advisors. The Arrangement is subject to the following approvals from Company Shareholders and the Ontario Superior Court of Justice (Commercial List) (the “Court”), which provides additional protection to the Company Shareholders (excluding Blackstone):

| (a) | a special resolution (the “Arrangement Resolution”), the full text of which is outlined in Appendix “A” of the accompanying management information circular (the “Circular”), must be approved by at least two-thirds (66 2/3%) of the votes cast by Company Shareholders present or represented by proxy at the Shareholder Meeting, voting as a single class; |

| (b) | as the Arrangement constitutes a “business combination” for the purposes of Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (“MI 61-101”), the Arrangement Resolution must also be approved by a simple majority (more than 50%) of the votes cast by Company Shareholders present or represented by proxy at the Shareholder Meeting, excluding, for this purpose, the votes attached to the Common Shares held by Blackstone, David Berman, Gary Berman and any other Company Shareholders required to be excluded under MI 61-101; and |

| (c) | the Arrangement must be approved by the Court, which will consider, among other things, the procedural and substantive fairness of the Arrangement to Company Shareholders (excluding Blackstone). |

The 28,123,624 Common Shares beneficially owned or controlled, directly or indirectly, by BREIT, along with the 4,266,422 Common Shares and the 2,113,977 Common Shares beneficially owned or controlled, directly or indirectly, by David Berman and Gary Berman, respectively, collectively representing approximately 11.70% of the Common Shares as of the Record Date, will be excluded for the purposes of the “minority approval” required under MI 61-101. Frank Cohen (the director on the Company Board appointed by Blackstone) does not own any Common Shares and accordingly need not be excluded for the purposes of the “minority approval” required under MI 61-101.

In connection with the proposed Arrangement, all directors and executive officers of the Company have advised the Company that they intend to vote or cause to be voted all Common Shares beneficially held by them, if any, in favour of the Arrangement Resolution.

The Arrangement is currently expected to be completed in the second quarter of this year based on the assumption that all required Company Shareholder, Court and regulatory approvals are obtained and all other conditions to the Arrangement are satisfied or waived prior to such date.

The Shareholder Meeting will be held on Thursday, March 28, 2024 at 10:00 a.m. (Toronto time) in virtual format via live audio webcast at https://web.lumiconnect.com/#/411155572, Password: tricon2024 (case sensitive) and Meeting ID: 411-155-572. As the Company aims to maximize Company Shareholder participation, the Shareholder Meeting will be in a virtual-only format, which will be conducted via live audio webcast. All Company Shareholders, regardless of geographic location, will have an equal opportunity to participate at the Shareholder Meeting. Company Shareholders will not be able to attend the Shareholder Meeting in person. Registered Company Shareholders and duly appointed proxyholders will be able to attend, participate or vote at the Shareholder Meeting online. Guests and non-registered Company Shareholders (being shareholders who hold their Common Shares through a broker, investment dealer, bank, trust company, custodian, nominee or other intermediary) must duly appoint themselves as proxyholder in order to be able to vote or ask questions at the Shareholder Meeting. The online Shareholder Meeting will ensure that Company Shareholders who attend the Shareholder Meeting will be afforded the same rights and opportunities to participate as they would at an in-person meeting.

- iii -

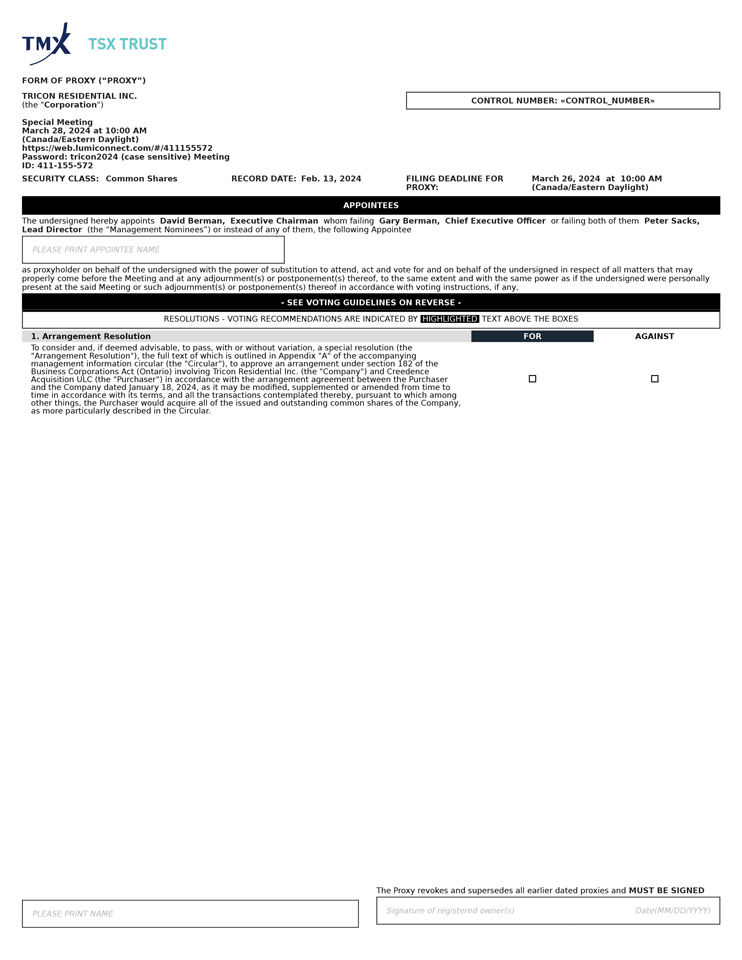

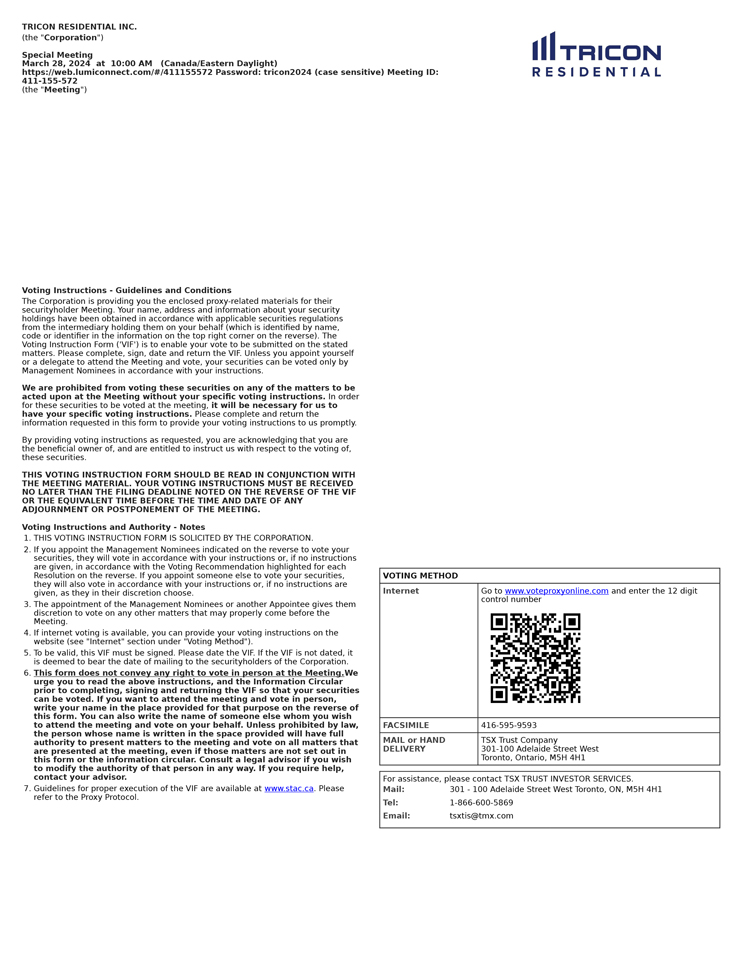

Please arrange for your proxy to be received by the Company’s transfer agent, TSX Trust Company (“TSX Trust”), at 301-100 Adelaide Street West, Toronto, Ontario, M5H 4H1, Attention: Proxy Department, by no later than 10:00 a.m. (Toronto time) on Tuesday, March 26, 2024 (or, if the Shareholder Meeting is adjourned or postponed, 48 hours, excluding Saturdays, Sundays and statutory holidays, prior to the commencement of the reconvened Shareholder Meeting). Late proxies may be accepted or rejected by the Chair of the Shareholder Meeting at his or her discretion, subject to the terms of the Arrangement Agreement, and the Chair of the Shareholder Meeting is under no obligation to accept or reject any particular late proxy.

Company Shareholders should review the accompanying notice of special meeting of Company Shareholders and the Circular, which describes, among other things, the background to the Arrangement as well as the reasons for the determinations and recommendations of the Special Committee and the Company Board. The Circular contains a detailed description of the Arrangement and includes additional information to assist you in considering how to vote at the Shareholder Meeting. You are urged to read this information carefully and, if you require assistance, you are urged to consult your financial, legal, tax or other professional advisors.

Your vote is important regardless of the number of Common Shares you own. If you are unable to attend the Shareholder Meeting, we encourage you to take the time now to complete, sign, date and return the enclosed form of proxy or voting instruction form, as applicable, so that your Common Shares can be voted at the Shareholder Meeting in accordance with your instructions. If you are a registered Company Shareholder, we also encourage you to complete, sign, date and return the enclosed letter of transmittal, which will help the Company arrange for the prompt payment for your Common Shares if the Arrangement is completed.

If you have any questions about the information contained in this Circular or require assistance in completing your form of proxy please contact our proxy solicitation agent and shareholder communications advisor, Laurel Hill Advisory Group, at 1-877-452-7184 (toll-free in North America), or by calling 1-416-304-0211 (outside of North America) or by email at assistance@laurelhill.com. Questions on how to complete the letter of transmittal should be directed to the Company’s transfer agent, TSX Trust, at 1-866-600-5869 (toll-free within North America) or at 416-342-1091 (outside of North America) or by email at txstis@tmx.com.

On behalf of the Company Board, we would like to take this opportunity to thank you for the support you have shown as Company Shareholders.

| Yours very truly, |

||

| (signed) David Berman |

||

| David Berman Executive Chairman of the Board of Directors |

||

- iv -

Voting is Easy. Vote Well in Advance of the Proxy Deadline of March 26, 2024 at

10:00 a.m. (Toronto time)

Questions or Require Voting Assistance?

Contact our proxy solicitation agent:

North America Toll Free: 1-877-452-7184

Outside North America: 1-416-304-0211

Email: assistance@laurelhill.com

- v -

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

Toronto, Ontario, Canada, February 15, 2024

NOTICE IS HEREBY GIVEN that, in accordance with an interim order of the Ontario Superior Court of Justice (Commercial List) dated February 15, 2024 (the “Interim Order”), a special meeting (the “Shareholder Meeting”) of the holders (the “Company Shareholders”) of common shares (the “Common Shares”) of Tricon Residential Inc. (“Tricon” or the “Company”) will be held on Thursday, March 28, 2024 at 10:00 a.m. (Toronto time) in virtual format for the following purposes:

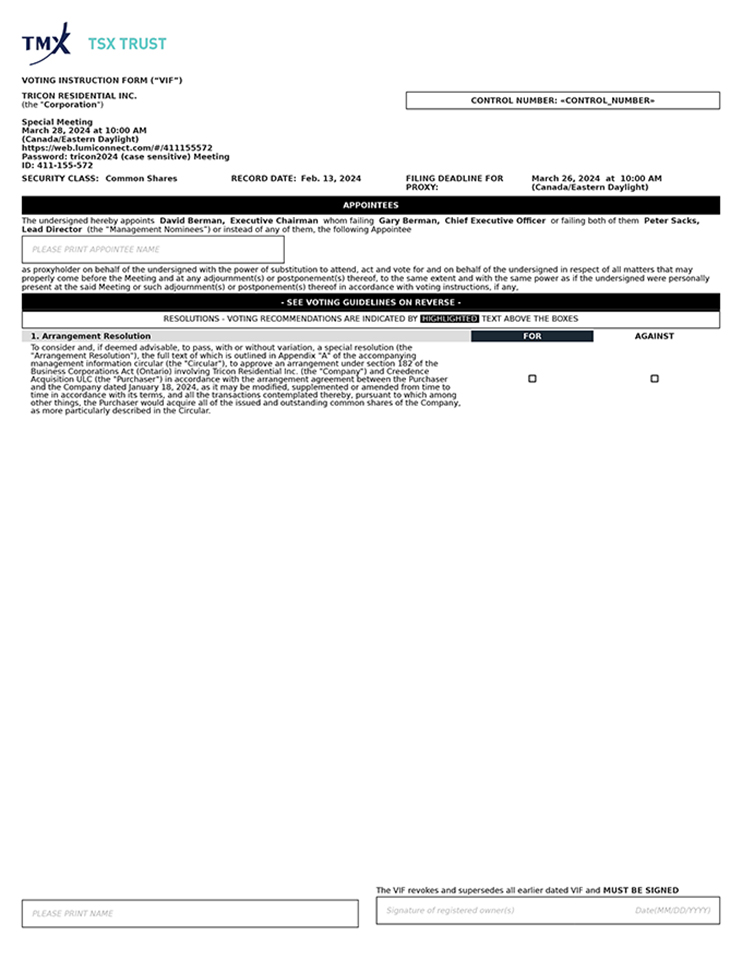

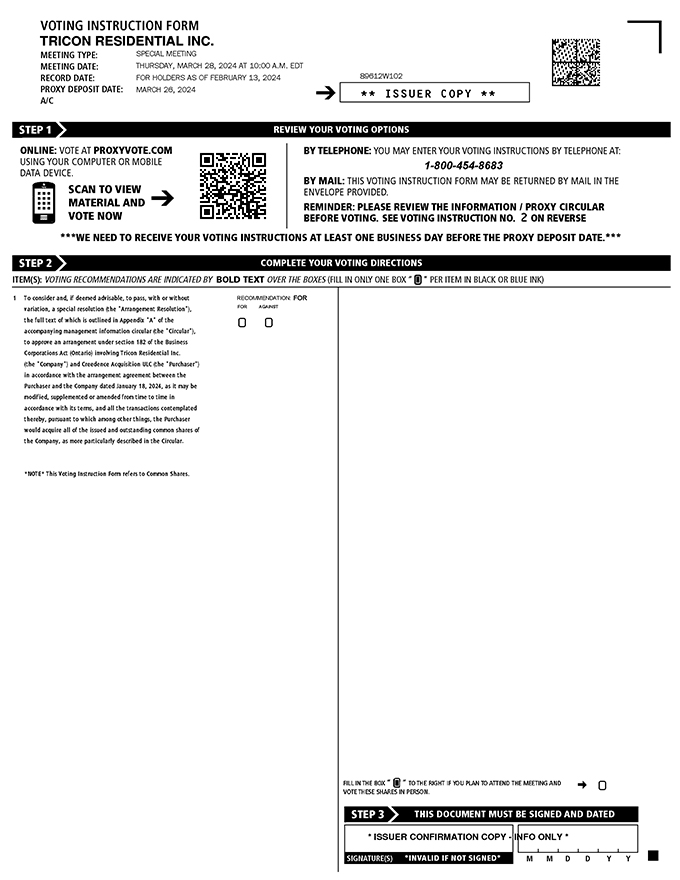

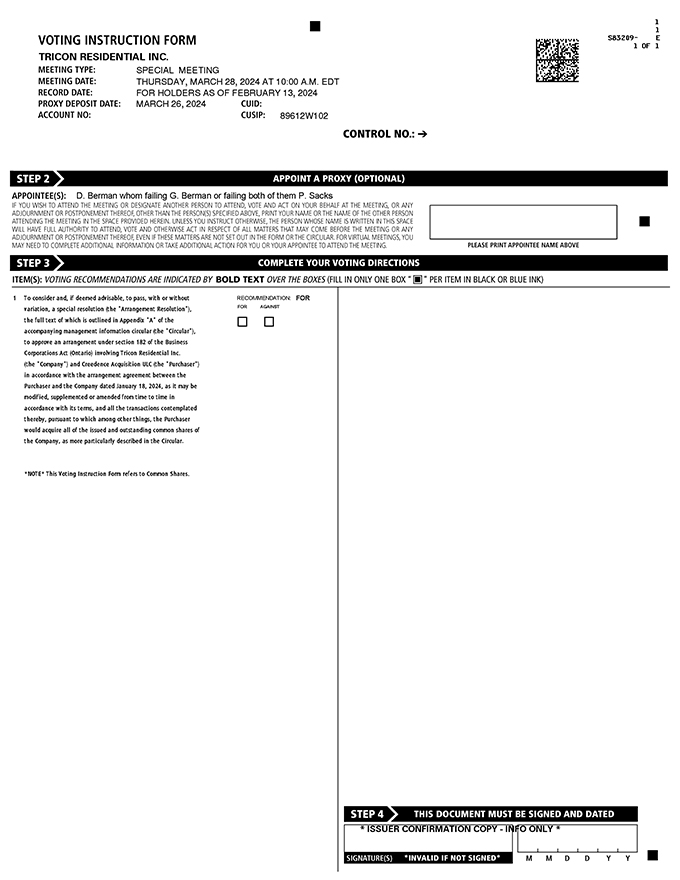

| 1. | to consider, and, if deemed advisable, to pass, with or without variation, a special resolution (the “Arrangement Resolution”), the full text of which is outlined in Appendix “A” of the accompanying management information circular (the “Circular”), to approve an arrangement (the “Arrangement”) under section 182 of the Business Corporations Act (Ontario) (the “OBCA”) involving the Company and Creedence Acquisition ULC (the “Purchaser”) in accordance with the arrangement agreement between the Purchaser and the Company dated January 18, 2024, as it may be modified, supplemented or amended from time to time in accordance with its terms, and all the transactions contemplated thereby, pursuant to which, among other things, the Purchaser would acquire all of the issued and outstanding Common Shares, as more particularly described in the Circular; and |

| 2. | to transact such other business as may properly come before the Shareholder Meeting or any adjournment or postponement(s) thereof. |

The Circular provides additional information relating to the matters to be addressed at the Shareholder Meeting, including the Arrangement. Company Shareholders are encouraged to read the Circular carefully when evaluating the matters to be considered at the Shareholder Meeting.

Shareholder Meeting

The Shareholder Meeting will be held on Thursday, March 28, 2024 at 10:00 a.m. (Toronto time) in virtual format via live audio webcast at https://web.lumiconnect.com/#/411155572, Password: tricon2024 (case sensitive) and Meeting ID: 411-155-572. As the Company aims to maximize Company Shareholder participation, the Shareholder Meeting will be in a virtual-only format, which will be conducted via live audio webcast. All Company Shareholders, regardless of geographic location, will have an equal opportunity to participate at the Shareholder Meeting. Company Shareholders will not be able to attend the Shareholder Meeting in person. Registered Company Shareholders and duly appointed proxyholders will be able to attend, participate and vote at the Shareholder Meeting online. Guests and non-registered Company Shareholders (being shareholders who hold their common shares through an Intermediary (as defined below)) must duly appoint themselves as proxyholder in order to be able to vote or ask questions at the Shareholder Meeting. The online Shareholder Meeting will ensure that Company Shareholders who attend the Shareholder Meeting will be afforded the same rights and opportunities to participate as they would at an in-person meeting.

You can participate online using your smartphone, tablet or computer. Confirm that the browser for whichever device you are using is compatible by visiting https://web.lumiconnect.com/#/411155572 in advance of the Shareholder Meeting. You will need the latest version of Chrome, Safari, Edge or Firefox (please do not use Internet Explorer). Internal networks, firewalls, as well as VPNs (virtual private networks) may block the audio webcast or access to the virtual platform for the Shareholder Meeting. If you experience issues, make sure your VPN is deactivated or that you are not using a computer connected to an enterprise network.

Company Shareholders are encouraged to submit their vote in advance by completing a form of proxy (in the case of registered Company Shareholders) or voting instruction form (in the case of non-registered Company Shareholders), or where advanced voting is not possible, to do so at the virtual Shareholder Meeting. Detailed voting instructions can be found in the section of the Circular entitled “Information Concerning the Shareholder Meeting and Voting – How to Vote”.

Appointment of Proxyholders

Company Shareholders who wish to appoint a person other than the management nominees identified in the form of proxy or voting instruction form, including non-registered (beneficial) Company Shareholders who wish to appoint themselves as proxyholder, must carefully follow the instructions in the accompanying Circular and on their form of proxy or voting instruction form. Detailed instructions for appointing proxyholders can be found in the section of the Circular entitled “Information Concerning the Shareholder Meeting and Voting – How to Vote”.

Record Date

The Board of Directors of the Company (the “Company Board”) has set the close of business on Tuesday, February 13, 2024 as the record date (the “Record Date”) for determining the Company Shareholders who are entitled to receive notice of, and to vote their Common Shares at the Shareholder Meeting. Only persons who are shown on the register of Company Shareholders at the close of business on the Record Date, or their duly appointed proxyholders, will be entitled to attend the Shareholder Meeting and vote on the Arrangement Resolution.

As of the Record Date, there were 294,859,359 Common Shares issued and outstanding. Each Common Share entitles its holder to one (1) vote with respect to the matters to be voted on at the Shareholder Meeting.

Shareholder Approval

In order to become effective, the Arrangement must be approved by (i) at least two-thirds (66 2/3%) of the votes cast by Company Shareholders present or represented by proxy at the Shareholder Meeting, voting as a single class, and (ii) as the proposed transaction constitutes a “business combination” for the purposes of Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (“MI 61-101”), a simple majority (more than 50%) of the votes cast by Company Shareholders present or represented by proxy at the Shareholder Meeting, excluding, for the purposes of (ii), the votes attached to the Common Shares held by Blackstone, David Berman, Gary Berman and any other Company Shareholders required to be excluded under MI 61-101 (collectively, the “Excluded Shares”). The 28,123,624 Common Shares beneficially owned or controlled, directly or indirectly, by BREIT, along with the 4,266,422 Common Shares and the 2,113,977 Common Shares beneficially owned or controlled, directly or indirectly, by David Berman and Gary Berman, respectively, representing an aggregate of approximately 11.70% of the Common Shares as of the Record Date, will be Excluded Shares for purposes of such “minority approval” required under MI 61-101. Frank Cohen (the director on the Company Board appointed by Blackstone) does not own any Common Shares and accordingly need not be excluded for the purposes of the “minority approval” required under MI 61-101.

Letter of Transmittal

Accompanying this notice of meeting is the Circular, a proxy form and a letter of transmittal (for registered Company Shareholders) (the “Letter of Transmittal”). The accompanying Circular provides information relating to the matters to be addressed at the Shareholder Meeting and is incorporated into this notice of meeting. Any adjourned or postponed meeting resulting from an adjournment or postponement of the Shareholder Meeting will be held at a time and place to be specified either by the Company before the Shareholder Meeting or at the Chair’s discretion at the Shareholder Meeting.

For a registered Company Shareholder (other than BREIT Shareholder and any dissenting Company Shareholders) to receive US$11.25 in cash per Common Share (the “Consideration”) to which they may be entitled pursuant to the Arrangement, they must complete, sign and return the Letter of Transmittal together with their Share Certificate(s) and/or Direct Registration System advice(s), as applicable, and any other required documents and instruments to the depositary named in the Letter of Transmittal, in accordance with the procedures set out therein.

- ii -

Voting

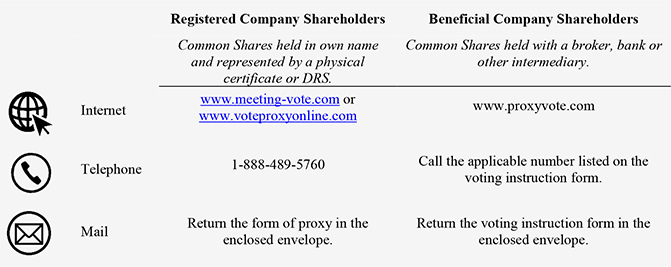

Whether or not you are able to attend the Shareholder Meeting, the Company Board and management of the Company urge you to participate in the Shareholder Meeting and vote your Common Shares. If you are a registered Company Shareholder and cannot attend the Shareholder Meeting to vote your Common Shares, please vote in one of the following ways:

| i. | by following the instructions for internet voting in the accompanying proxy form at least 48 hours, excluding Saturdays, Sundays and holidays, prior to the Shareholder Meeting or related adjournment(s) or postponement(s); or |

| ii. | by completing and signing the accompanying proxy form and returning it in the enclosed envelope, postage prepaid at least 48 hours, excluding Saturdays, Sundays and statutory holidays, prior to the Shareholder Meeting or related adjournment(s) or postponement(s); or |

| iii. | by duly appointing someone as a proxy to participate in the Shareholder Meeting and vote your Common Shares for you. |

The chair of the Shareholder Meeting reserves the right to accept late proxies and to extend or waive the proxy cut off at their discretion, with or without notice, subject to the terms of the Arrangement Agreement.

If you are a beneficial (non-registered) Company Shareholder, please refer to the section in the Circular entitled “Information Concerning the Shareholder Meeting and Voting – Non-Registered Company Shareholders” for information on how to vote your Common Shares. Beneficial (non-registered) Company Shareholders who hold their Common Shares through a broker, investment dealer, bank, trust company, custodian, nominee or another intermediary (an “Intermediary”), should carefully follow the instructions of their Intermediary to ensure that their Common Shares are voted at the Shareholder Meeting in accordance with such Company Shareholders’ instructions and, as applicable, to arrange for their Intermediary to complete the necessary transmittal documents and to ensure that they receive payment of the Consideration for their Common Shares if the Arrangement is completed.

Dissent Rights

Pursuant to the Interim Order, registered Company Shareholders have the right to dissent with respect to the Arrangement Resolution and, if the Arrangement becomes effective, to be paid the fair value of their Common Shares (less the amount of their entitlement to a pro rata portion of the return of capital distribution described in the accompanying Circular, if any) by the Purchaser in accordance with the provisions of Section 185 of the OBCA (the “Dissent Rights”), as modified by the Interim Order and/or the plan of arrangement pertaining to the Arrangement (the “Plan of Arrangement”). A registered Company Shareholder wishing to exercise Dissent Rights with respect to the Arrangement Resolution must provide a written notice of dissent (a “Dissent Notice”) to the Company, which the Company must receive, c/o David Veneziano, Executive Vice President and Chief Legal Officer, at 7 St. Thomas Street, Suite 801, Toronto, Ontario, M5S 2B7, Canada, with copies to each of:

| i. | Goodmans LLP, Bay Adelaide Centre, 333 Bay Street, Suite 3400, Toronto, Ontario, Canada, M5H 2S7, Attention: John Connon, email: jconnon@goodmans.ca and Tara Hunt, email: thunt@goodmans.ca; and |

| ii. | Davies Ward Phillips & Vineberg LLP, 155 Wellington Street West, Toronto, ON M5V 3J7, Attention: Kevin Greenspoon, email: kgreenspoon@dwpv.com and Joseph DiPonio, email: jdiponio@dwpv.com. |

by no later than 5:00 p.m. (Toronto time) on March 26, 2024 (or, if the Shareholder Meeting is adjourned or postponed, by no later than 5:00 p.m. on the second (2nd) business day, excluding Saturdays, Sundays and statutory holidays, prior to the commencement of the reconvened Shareholder Meeting), and must otherwise strictly comply with the dissent procedures described in the accompanying Circular, the Interim Order, the Plan of Arrangement and Section 185 of the OBCA, as modified by the Interim Order and the Plan of Arrangement. A Company Shareholder’s Dissent Notice sent with respect to the Arrangement shall be deemed to be and shall be automatically revoked if such Company Shareholder has voted (some or all of their Common Shares) FOR the Arrangement Resolution, whether online, virtually at the Shareholder Meeting or by proxy.

- iii -

Anyone who is a beneficial owner of Common Shares registered in the name of an Intermediary and who wishes to exercise Dissent Rights should be aware that only registered Company Shareholders are entitled to exercise Dissent Rights. A non-registered Company Shareholder who wishes to exercise Dissent Rights must make arrangements for the registered Company Shareholder of such Common Shares to exercise Dissent Rights on behalf of such Company Shareholder. A registered Company Shareholder who intends to exercise Dissent Rights must do so with respect to all of the Common Shares registered in the Company Shareholder’s name that either: (i) they hold on their own behalf; or (ii) they hold on behalf of any one beneficial Company Shareholder, and must deliver a Dissent Notice to the Company in the manner and within the time described above. There is no right to a partial Dissent Right.

It is recommended that you seek independent legal advice if you wish to exercise Dissent Rights. The Dissent Rights are more particularly described in the accompanying Circular, and copies of the Plan of Arrangement, the Interim Order and the text of Section 185 of the OBCA are set forth in Appendix “B”, Appendix “E” and Appendix “G”, respectively, of the Circular. Failure to strictly comply with the requirements set forth in Section 185 of the OBCA, as modified by the Interim Order and/or the Plan of Arrangement, may result in the loss of the Dissent Rights.

| By order of the Company Board, | ||

| (signed) David Berman | ||

| David Berman Executive Chairman of the Company Board | ||

- iv -

TRICON RESIDENTIAL INC.

MANAGEMENT INFORMATION CIRCULAR

This management information circular (this “Circular”) is provided in relation to the solicitation of proxies by the management of Tricon Residential Inc. (“we”, “us”, “our”, “Tricon” and the “Company”) for use at the special meeting of Company Shareholders (the “Shareholder Meeting”) of the Company to be held on Thursday, March 28, 2024 at 10:00 a.m. (Toronto time) virtually via live audio webcast at https://web.lumiconnect.com/#/411155572 and at any adjournment or postponement thereof. Unless otherwise indicated, the information provided in this Circular is provided as of the Record Date of Tuesday, February 13, 2024.

All capitalized terms used in this Circular but not otherwise defined herein have the meanings set forth in the “Glossary of Terms”. In this Circular, unless there is something in the subject matter or context inconsistent therewith, words importing the singular number only (including defined terms) include the plural. Capitalized words and terms used in the Schedules attached to this Circular are defined separately therein.

CURRENCY AND EXCHANGE RATES

Unless otherwise indicated, references to “$” or “US$” refer to the lawful currency of the United States of America and references to “C$” refer to the lawful currency of Canada. On February 13, 2024, the daily average exchange rate as reported by the Bank of Canada was: C$1.00 = US$0.7377 and US$1.00 = C$1.3556.

CAUTIONARY STATEMENTS

We have not authorized any person to give any information or make any representation regarding the Arrangement or any other matters to be considered at the Shareholder Meeting other than those contained in this Circular. If any such information or representation is given or made to you, you should not rely on it as being authorized or accurate.

This Circular does not constitute an offer to buy, or a solicitation of an offer to sell, any securities, or the solicitation of a proxy, by any person in any jurisdiction in which such an offer or solicitation is not authorized or in which the person making such an offer or solicitation is not qualified to do so or to any person to whom it is unlawful to make such an offer or solicitation. The delivery of this Circular will not, under any circumstances, create any implication or be treated as a representation that there has been no change in the information set out herein since the date of this Circular.

Management is soliciting your proxy. The Company has retained Laurel Hill Advisory Group (“Laurel Hill”) as its proxy solicitation agent and shareholder communications advisor for assistance in connection with the solicitation of proxies for the Shareholder Meeting, and will pay Laurel Hill fees of C$175,000 for such services in addition to certain out-of-pocket expenses. Management requests that you sign and return the proxy form or voting instruction form so that your votes are exercised at the Shareholder Meeting. The solicitation of proxies will be conducted primarily by mail but may also be made by telephone, facsimile transmission or other electronic means of communication or in-person by the directors, officers and employees of Tricon. The Company will bear the cost of such solicitation and will reimburse Intermediaries for their reasonable charges and expenses incurred in forwarding proxy materials to non-registered Company Shareholders. The Purchaser and its affiliates may also participate in the solicitation of proxies.

Company Shareholders should not construe the contents of this Circular as legal, tax or financial advice and are urged to consult with their own legal, tax, financial or other professional advisors.

The information contained in this Circular concerning the Purchaser and its affiliates, including such information under the heading “Special Factors – Background to the Arrangement”, has been provided by the Purchaser and its affiliates for inclusion in this Circular. Although the Company has no knowledge that any statement contained herein taken from, or based on, such information and records or information provided by the Purchaser or its affiliates are untrue or incomplete, the Company assumes no responsibility for the accuracy of the information contained in such documents, records or information or for any failure by the Purchaser or its affiliates to disclose events which may have occurred or may affect the significance or accuracy of any such information but which are unknown to the Company.

All summaries of and references to the Arrangement Agreement, the Plan of Arrangement, and Support Agreement in this Circular are qualified in their entirety by the complete text of such documents and Company Shareholders should refer to the full text for complete details of such documents. The Plan of Arrangement is attached as Appendix “B” to this Circular, and copies of the Arrangement Agreement and Support Agreement are available under Tricon’s profiles on SEDAR+ at www.sedarplus.ca and EDGAR at www.sec.gov. You are urged to read the full text of the Arrangement Agreement and the Plan of Arrangement carefully.

NO CANADIAN SECURITIES REGULATORY AUTHORITY NOR THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION OR ANY STATE SECURITIES COMMISSION HAS PASSED UPON THE ACCURACY OR ADEQUACY OF THIS CIRCULAR. ANY REPRESENTATION TO THE CONTRARY IS AN OFFENCE.

FORWARD-LOOKING INFORMATION

This Circular contains “forward-looking information” within the meaning of applicable Canadian Securities Laws, and Tricon intends that such forward-looking statements be subject to the safe harbours created thereby. Forward-looking statements are statements other than historical information or statements of current condition. Words such as may, expect, believe, plan, anticipate, intend, could, estimate, continue, or similar expressions or the negative of such expressions are intended to identify forward-looking statements. In addition, any statements that refer to expectations, projections or other characterizations of future events and circumstances are considered forward-looking statements. They are not guarantees of future performance and these statements involve known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking statements. More particularly and without restriction, this Circular contains forward-looking statements and information regarding: the Company Forecasts; the anticipated benefits of the Arrangement for the Company and Company Shareholders; the Company Shareholder Approvals, Court approval and Required Regulatory Approvals and other conditions required to complete the Arrangement; the anticipated timing of the completion of the Arrangement; future distributions by the Company and Company Subsidiaries; the de-listing of the Common Shares from the TSX and the NYSE, and the Company ceasing to be a reporting issuer in Canada; the consequences to Company Shareholders if the Arrangement is not completed; the anticipated expenses of the Arrangement; the Canadian and U.S. income tax consequences of the Arrangement and expected tax treatment of the Return of Capital Distribution, if any, and Common Share Acquisition Price; and such other statements regarding the Company’s expectations, intentions, plans and beliefs.