We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Name | Symbol | Market | Type |

|---|---|---|---|

| JP Morgan Chase and Co | NYSE:JPM-M | NYSE | Preference Share |

| Price Change | % Change | Price | High Price | Low Price | Open Price | Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|

| -0.05 | -0.26% | 19.20 | 19.21 | 19.11 | 19.18 | 64,916 | 21:00:04 |

|

March , 2024

|

Registration Statement Nos. 333-270004 and 333-270004-01; Rule 424(b)(2)

|

|

JPMorgan Chase Financial Company LLC

Structured Investments

Auto Callable Contingent Interest Notes Linked to the Least

Performing of the Nasdaq-100® Technology Sector IndexSM, the

Russell 2000® Index and the SPDR® S&P® Regional Banking ETF

due December 17, 2025

Fully and Unconditionally Guaranteed by JPMorgan Chase & Co.

●The notes are designed for investors who seek a Contingent Interest Payment with respect to each Review Date for which the

closing value of each of the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and the SPDR® S&P®

Regional Banking ETF, which we refer to as the Underlyings, is greater than or equal to 70.00% of its Initial Value, which we

refer to as an Interest Barrier.

●The notes will be automatically called if the closing value of each Underlying on any Review Date (other than the first, second,

third, fourth, fifth and final Review Dates) is greater than or equal to its Initial Value.

●The earliest date on which an automatic call may be initiated is September 12, 2024.

●Investors should be willing to accept the risk of losing some or all of their principal and the risk that no Contingent Interest

Payment may be made with respect to some or all Review Dates.

●Investors should also be willing to forgo fixed interest and dividend payments, in exchange for the opportunity to receive

Contingent Interest Payments.

●The notes are unsecured and unsubordinated obligations of JPMorgan Chase Financial Company LLC, which we refer to as

JPMorgan Financial, the payment on which is fully and unconditionally guaranteed by JPMorgan Chase & Co. Any payment

on the notes is subject to the credit risk of JPMorgan Financial, as issuer of the notes, and the credit risk of

JPMorgan Chase & Co., as guarantor of the notes.

●Payments on the notes are not linked to a basket composed of the Underlyings. Payments on the notes are linked to the

performance of each of the Underlyings individually, as described below.

●Minimum denominations of $1,000 and integral multiples thereof

●The notes are expected to price on or about March 12, 2024 and are expected to settle on or about March 15, 2024.

●CUSIP: 48134W7C5

|

|

|

Price to Public (1)

|

Fees and Commissions (2)

|

Proceeds to Issuer

|

|

Per note

|

$1,000

|

$

|

$

|

|

Total

|

$

|

$

|

$

|

|

(1) See “Supplemental Use of Proceeds” in this pricing supplement for information about the components of the price to public of the notes.

(2) J.P. Morgan Securities LLC, which we refer to as JPMS, acting as agent for JPMorgan Financial, will pay all of the selling commissions it

receives from us to other affiliated or unaffiliated dealers. In no event will these selling commissions exceed $7.25 per $1,000 principal amount

note. See “Plan of Distribution (Conflicts of Interest)” in the accompanying product supplement.

|

|||

|

Issuer: JPMorgan Chase Financial Company LLC, an indirect,

wholly owned finance subsidiary of JPMorgan Chase & Co.

Guarantor: JPMorgan Chase & Co.

Underlyings: The Nasdaq-100® Technology Sector IndexSM

(Bloomberg ticker: NDXT) and the Russell 2000® Index

(Bloomberg ticker: RTY) (each an “Index” and collectively, the

“Indices”) and the SPDR® S&P® Regional Banking ETF

(Bloomberg ticker: KRE) (the “Fund”) (each of the Indices and

the Fund, an “Underlying” and collectively, the “Underlyings”)

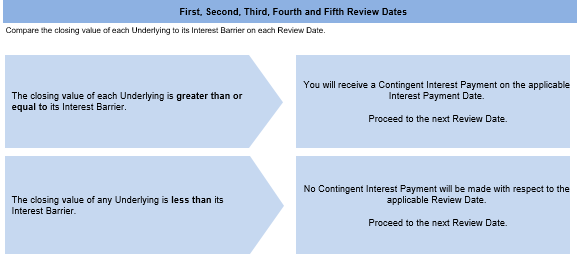

Contingent Interest Payments:

If the notes have not been automatically called and the closing

value of each Underlying on any Review Date is greater than or

equal to its Interest Barrier, you will receive on the applicable

Interest Payment Date for each $1,000 principal amount note a

Contingent Interest Payment equal to at least $11.5417

(equivalent to a Contingent Interest Rate of at least 13.85% per

annum, payable at a rate of at least 1.15417% per month) (to be

provided in the pricing supplement).

If the closing value of any Underlying on any Review Date is

less than its Interest Barrier, no Contingent Interest Payment will

be made with respect to that Review Date.

Contingent Interest Rate: At least 13.85% per annum, payable

at a rate of at least 1.15417% per month (to be provided in the

pricing supplement)

Interest Barrier: With respect to each Underlying, 70.00% of its

Initial Value

Trigger Value: With respect to each Underlying, 60.00% of its

Initial Value

Pricing Date: On or about March 12, 2024

Original Issue Date (Settlement Date): On or about March 15,

2024

Review Dates*: April 12, 2024, May 13, 2024, June 12, 2024,

July 12, 2024, August 12, 2024, September 12, 2024, October

14, 2024, November 12, 2024, December 12, 2024, January 13,

2025, February 12, 2025, March 12, 2025, April 14, 2025, May

12, 2025, June 12, 2025, July 14, 2025, August 12, 2025,

September 12, 2025, October 13, 2025, November 12, 2025

and December 12, 2025 (final Review Date)

Interest Payment Dates*: April 17, 2024, May 16, 2024, June

17, 2024, July 17, 2024, August 15, 2024, September 17, 2024,

October 17, 2024, November 15, 2024, December 17, 2024,

January 16, 2025, February 18, 2025, March 17, 2025, April 17,

2025, May 15, 2025, June 17, 2025, July 17, 2025, August 15,

2025, September 17, 2025, October 16, 2025, November 17,

2025 and the Maturity Date

Maturity Date*: December 17, 2025

Call Settlement Date*: If the notes are automatically called on

any Review Date (other than the first, second, third, fourth, fifth

and final Review Dates), the first Interest Payment Date

immediately following that Review Date

* Subject to postponement in the event of a market disruption event and

as described under “General Terms of Notes — Postponement of a

Determination Date — Notes Linked to Multiple Underlyings” and

“General Terms of Notes — Postponement of a Payment Date” in the

accompanying product supplement

|

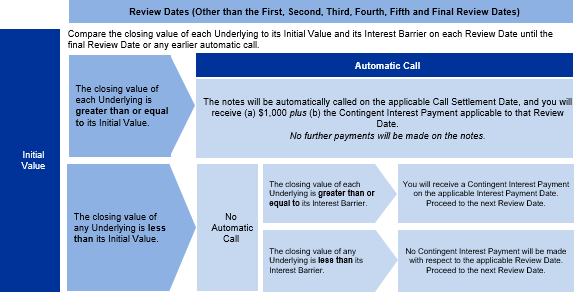

Automatic Call:

If the closing value of each Underlying on any Review Date

(other than the first, second, third, fourth, fifth and final Review

Dates) is greater than or equal to its Initial Value, the notes will

be automatically called for a cash payment, for each $1,000

principal amount note, equal to (a) $1,000 plus (b) the

Contingent Interest Payment applicable to that Review Date,

payable on the applicable Call Settlement Date. No further

payments will be made on the notes.

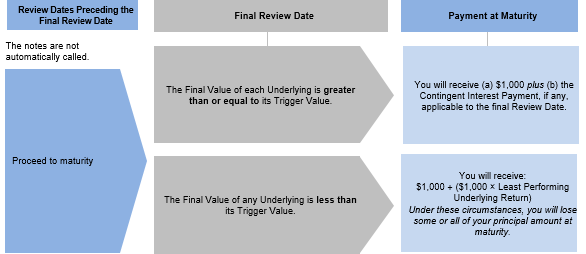

Payment at Maturity:

If the notes have not been automatically called and the Final

Value of each Underlying is greater than or equal to its Trigger

Value, you will receive a cash payment at maturity, for each

$1,000 principal amount note, equal to (a) $1,000 plus (b) the

Contingent Interest Payment, if any, applicable to the final

Review Date.

If the notes have not been automatically called and the Final

Value of any Underlying is less than its Trigger Value, your

payment at maturity per $1,000 principal amount note will be

calculated as follows:

$1,000 + ($1,000 × Least Performing Underlying Return)

If the notes have not been automatically called and the Final

Value of any Underlying is less than its Trigger Value, you will

lose more than 40.00% of your principal amount at maturity and

could lose all of your principal amount at maturity.

Least Performing Underlying: The Underlying with the Least

Performing Underlying Return

Least Performing Underlying Return: The lowest of the

Underlying Returns of the Underlyings

Underlying Return: With respect to each Underlying,

(Final Value – Initial Value)

Initial Value

Initial Value: With respect to each Underlying, the closing value

of that Underlying on the Pricing Date

Final Value: With respect to each Underlying, the closing value

of that Underlying on the final Review Date

Share Adjustment Factor: The Share Adjustment Factor is

referenced in determining the closing value of the Fund and is

set equal to 1.0 on the Pricing Date. The Share Adjustment

Factor is subject to adjustment upon the occurrence of certain

events affecting the Fund. See “The Underlyings – Funds –

Anti-Dilution Adjustments” in the accompanying product

supplement for further information.

|

|

PS-1 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

PS-2 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

Number of Contingent

Interest Payments

|

Total Contingent Interest

Payments

|

|

21

|

$242.3750

|

|

20

|

$230.8333

|

|

19

|

$219.2917

|

|

18

|

$207.7500

|

|

17

|

$196.2083

|

|

16

|

$184.6667

|

|

15

|

$173.1250

|

|

14

|

$161.5833

|

|

13

|

$150.0417

|

|

12

|

$138.5000

|

|

11

|

$126.9583

|

|

10

|

$115.4167

|

|

9

|

$103.8750

|

|

8

|

$92.3333

|

|

7

|

$80.7917

|

|

6

|

$69.2500

|

|

5

|

$57.7083

|

|

4

|

$46.1667

|

|

3

|

$34.6250

|

|

2

|

$23.0833

|

|

1

|

$11.5417

|

|

0

|

$0.0000

|

|

PS-3 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

Date

|

Closing Value of Least

Performing Underlying

|

Payment (per $1,000 principal amount note)

|

|

First Review Date

|

105.00

|

$11.5417

|

|

Second Review Date

|

110.00

|

$11.5417

|

|

Third Review Date

|

110.00

|

$11.5417

|

|

Fourth Review Date

|

105.00

|

$11.5417

|

|

Fifth Review Date

|

110.00

|

$11.5417

|

|

Sixth Review Date

|

120.00

|

$1,011.5417

|

|

Total Payment

|

$1,069.25 (6.925% return)

|

|

PS-4 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

Date

|

Closing Value of Least

Performing Underlying

|

Payment (per $1,000 principal amount note)

|

|

First Review Date

|

95.00

|

$11.5417

|

|

Second Review Date

|

85.00

|

$11.5417

|

|

Third through Twentieth

Review Dates

|

Less than Interest Barrier

|

$0

|

|

Final Review Date

|

90.00

|

$1,011.5417

|

|

Total Payment

|

$1,034.625 (3.4625% return)

|

|

Date

|

Closing Value of Least

Performing Underlying

|

Payment (per $1,000 principal amount note)

|

|

First Review Date

|

80.00

|

$11.5417

|

|

Second Review Date

|

75.00

|

$11.5417

|

|

Third through Twentieth

Review Dates

|

Less than Interest Barrier

|

$0

|

|

Final Review Date

|

60.00

|

$1,000.00

|

|

Total Payment

|

$1,023.0833 (2.30833% return)

|

|

Date

|

Closing Value of Least

Performing Underlying

|

Payment (per $1,000 principal amount note)

|

|

First Review Date

|

50.00

|

$0

|

|

Second Review Date

|

55.00

|

$0

|

|

Third through Twentieth

Review Dates

|

Less than Interest Barrier

|

$0

|

|

Final Review Date

|

50.00

|

$500.00

|

|

Total Payment

|

$500.00 (-50.00% return)

|

|

PS-5 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

PS-6 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

PS-7 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

PS-8 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

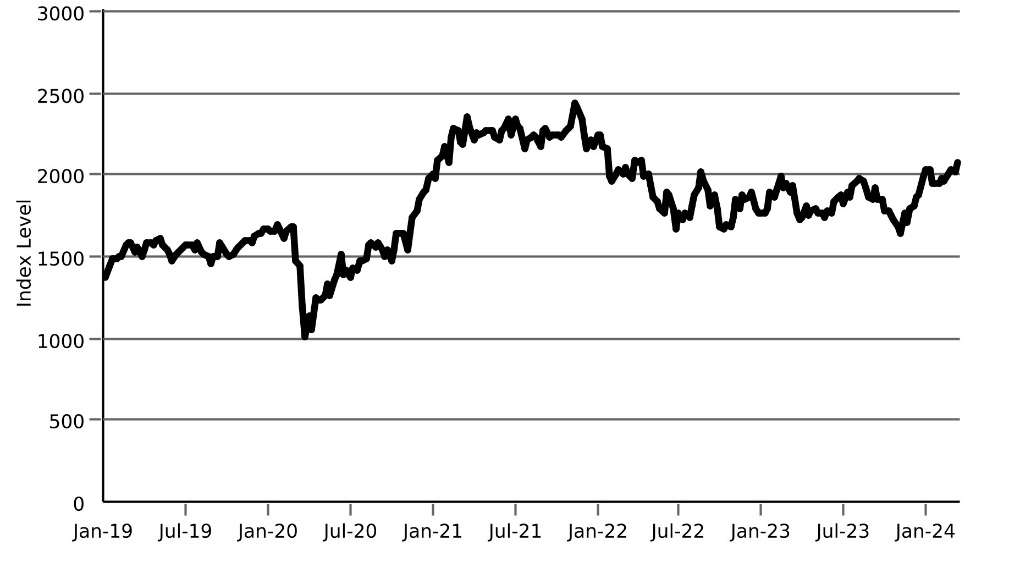

Historical Performance of the Nasdaq-100® Technology Sector IndexSM

Source: Bloomberg

|

|

Historical Performance of the Russell 2000® Index

Source: Bloomberg

|

|

PS-9 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

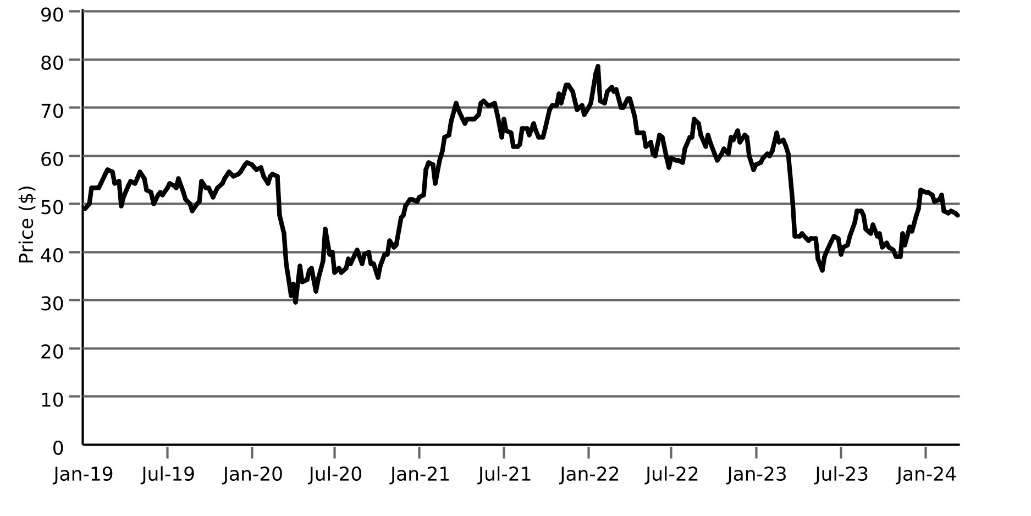

Historical Performance of the SPDR® S&P® Regional Banking ETF

Source: Bloomberg

|

|

PS-10 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

PS-11 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

PS-12 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

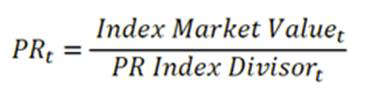

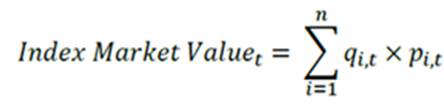

(1)

|

“Index Market Value” shall be calculated as follows:

|

|

“Index Security” shall mean a security that has been selected for membership in the Nasdaq-100® Technology Sector IndexSM,

having met all applicable eligibility requirements.

n = Number of Index Securities included in the Nasdaq-100® Technology Sector IndexSM

qi = Number of shares of Index Security i applied in the Nasdaq-100® Technology Sector IndexSM.

pi = Price in quote currency of Index Security i. Depending on the time of the calculation, the price can be either of the following:

|

||

|

PS-13 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

a.

|

The Start of Day (SOD) price which is the previous index calculation day’s (t-1) closing price for Index Security i adjusted

for corporate action(s) occurring prior to market open on date t, if any, for the SOD calculation only;

|

|

|

b.

|

The intraday price which reflects the current trading price received from the Nasdaq during the index calculation day;

|

|

|

c.

|

The End of Day (EOD) price refers to the Last Sale Price, which refers to the last regular-way trade reported on Nasdaq; or

|

|

|

d.

|

The Volume Weighted Average Price (VWAP)

|

|

|

t = current index calculation day

t-1 = current index calculation day

|

||

|

(2)

|

“PR Index Divisor” should be calculated as follows:

|

|

|

PS-14 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

|

PS-15 | Structured Investments

|

|

|

Auto Callable Contingent Interest Notes Linked to the Least Performing of

the Nasdaq-100® Technology Sector IndexSM, the Russell 2000® Index and

the SPDR® S&P® Regional Banking ETF

|

1 Year JP Morgan Chase Chart |

1 Month JP Morgan Chase Chart |

It looks like you are not logged in. Click the button below to log in and keep track of your recent history.

Support: +44 (0) 203 8794 460 | support@advfn.com

By accessing the services available at ADVFN you are agreeing to be bound by ADVFN's Terms & Conditions

Hot Features

Hot Features