We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Share Name | Share Symbol | Market | Type |

|---|---|---|---|

| First Trust High Yield Opportunities 2027 Term Fund | NYSE:FTHY | NYSE | Common Stock |

| Price Change | % Change | Share Price | High Price | Low Price | Open Price | Shares Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|

| 0.03 | 0.21% | 14.32 | 14.39 | 14.25 | 14.29 | 69,111 | 01:00:00 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-23199

(Exact name of registrant as specified in charter)

120 East Liberty Drive

Wheaton, IL 60187

(Address of principal executive offices) (Zip code)

W. Scott Jardine, Esq.

First Trust Portfolios L.P.

120 East Liberty Drive

Wheaton, IL 60187

(Name and address of agent for

service)

Registrant's telephone number, including area code: 630-765-8000

Date of fiscal year end: May 31

Date of reporting period:

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

(a) The Report to Shareholders is attached herewith.

|

|

1 |

|

|

2 |

|

|

4 |

|

|

7 |

|

|

17 |

|

|

18 |

|

|

19 |

|

|

20 |

|

|

21 |

|

|

22 |

|

|

29 |

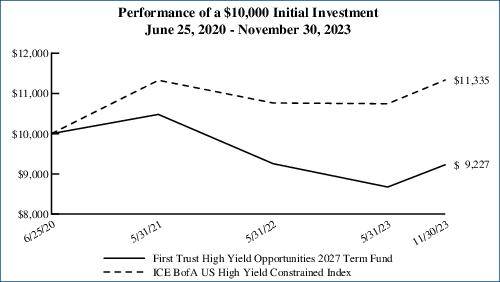

| Performance | |||

| Average

Annual Total Returns | |||

| 6

Months Ended 11/30/23 |

1

Year Ended 11/30/23 |

Inception

(6/25/20) to 11/30/23 | |

| Fund Performance(3) | |||

| NAV(4) | 7.22% | 9.13% | 1.69% |

| Market Value | 6.39% | 3.48% | -2.32% |

| Index Performance | |||

| ICE BofA US High Yield Constrained Index | 5.50% | 8.62% | 3.72% |

| (1) | Most recent distribution paid through November 30, 2023. Subject to change in the future. |

| (2) | Distribution rates are calculated by annualizing the most recent distribution paid through the report date and then dividing by Common Share Price or NAV, as applicable, as of November 30, 2023. Subject to change in the future. |

| (3) | Total return is based on the combination of reinvested dividend, capital gain, and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan and changes in NAV per share for NAV returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of future results. |

| (4) | On January 3, 2023, the fair value methodology used to value the senior loan investments held by the Fund was changed. Prior to that date, the senior loans were valued using the bid side price provided by a pricing service. After such date, the senior loans were valued using the midpoint between the bid and ask price provided by a pricing service. The change in the Fund’s fair value methodology on January 3, 2023, resulted in a one-time increase in the Fund’s NAV of approximately $0.018 per share on that date, which represented a positive impact on the Fund’s performance of 0.11%. Without the change to the pricing methodology, the performance of the Fund on a NAV basis would have been 7.15%, 8.99%, and 1.65%, in the six-month, one-year, and since inception periods ended November 30, 2023, respectively. |

| (5) | The ratings are by S&P Global Ratings except where otherwise indicated. A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of the creditworthiness of an issuer with respect to debt obligations except for those debt obligations that are only privately rated. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest). Investment grade is defined as those issuers that have a long-term credit rating of BBB- or higher. The credit ratings shown relate to the creditworthiness of the issuers of the underlying securities in the Fund, and not to the Fund or its shares. Credit ratings are subject to change. |

| (6) | Percentages are based on long-term positions. Money market funds are excluded. |

| Average

Annual Total Returns | |||

| 6

Months Ended 11/30/23 |

1

Year Ended 11/30/23 |

Inception

(6/25/20) to 11/30/23 | |

| Fund Performance(1) | |||

| NAV(2) | 7.22% | 9.13% | 1.69% |

| Market Value | 6.39% | 3.48% | -2.32% |

| Index Performance | |||

| ICE BofA US High Yield Constrained Index | 5.50% | 8.62% | 3.72% |

| (1) | Total return is based on the combination of reinvested dividend, capital gain and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan and changes in NAV per share for NAV returns and changes in Common Share price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. |

| (2) | On January 3, 2023, the fair value methodology used to value the senior loan investments held by the Fund was changed. Prior to that date, the senior loans were valued using the bid side price provided by a pricing service. After such date, the senior loans were valued using the midpoint between the bid and ask price provided by a pricing service. The change in the Fund’s fair value methodology on January 3, 2023, resulted in a one-time increase in the Fund’s NAV of approximately $0.018 per share on that date, which represented a positive impact on the Fund’s performance of 0.11%. Without the change to the pricing methodology, the performance of the Fund on a NAV basis would have been 7.15%, 8.99%, and 1.65%, in the six-month, one-year, and since inception periods ended November 30, 2023, respectively. |

| (3) | Industry sector classifications for performance attribution are based on the ICE BofA US High Yield Constrained Index’s Level 3 Subgroup. |

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| CORPORATE BONDS AND NOTES – 87.0% | ||||||||

| Aerospace & Defense – 1.2% | ||||||||

| $158,000 |

Booz Allen Hamilton, Inc. (a) (b) |

3.88% | 09/01/28 | $145,400 | ||||

| 2,598,000 |

TransDigm, Inc. (a) (b) |

6.25% | 03/15/26 | 2,582,232 | ||||

| 4,311,000 |

TransDigm, Inc. (a) (b) |

6.75% | 08/15/28 | 4,324,101 | ||||

| 7,051,733 | ||||||||

| Agricultural Products & Services – 0.1% | ||||||||

| 623,000 |

Lamb Weston Holdings, Inc. (a) (b) |

4.88% | 05/15/28 | 596,321 | ||||

| Apparel Retail – 0.8% | ||||||||

| 4,040,000 |

Nordstrom, Inc. (b) |

4.00% | 03/15/27 | 3,801,801 | ||||

| 1,146,000 |

Nordstrom, Inc. (b) |

4.38% | 04/01/30 | 953,687 | ||||

| 4,755,488 | ||||||||

| Application Software – 2.1% | ||||||||

| 2,892,000 |

Alteryx, Inc. (a) (b) |

8.75% | 03/15/28 | 2,910,888 | ||||

| 5,755,000 |

GoTo Group, Inc. (a) (b) |

5.50% | 08/31/27 | 3,402,271 | ||||

| 3,000,000 |

McAfee Corp. (a) (b) |

7.38% | 02/15/30 | 2,593,962 | ||||

| 1,513,000 |

Open Text Holdings, Inc. (a) (b) |

4.13% | 12/01/31 | 1,293,793 | ||||

| 1,576,000 |

RingCentral, Inc. (a) (b) |

8.50% | 08/15/30 | 1,571,524 | ||||

| 11,772,438 | ||||||||

| Automobile Manufacturers – 0.7% | ||||||||

| 3,369,000 |

Ford Motor Co. (b) |

9.63% | 04/22/30 | 3,861,730 | ||||

| Broadcasting – 13.9% | ||||||||

| 5,708,000 |

Gray Television, Inc. (a) (b) |

5.88% | 07/15/26 | 5,341,518 | ||||

| 8,201,000 |

Gray Television, Inc. (a) (b) |

7.00% | 05/15/27 | 7,460,901 | ||||

| 3,409,000 |

Gray Television, Inc. (a) (b) |

4.75% | 10/15/30 | 2,436,902 | ||||

| 13,053,000 |

iHeartCommunications, Inc. (b) |

8.38% | 05/01/27 | 9,148,657 | ||||

| 22,177,000 |

Nexstar Media, Inc. (a) (b) |

5.63% | 07/15/27 | 21,022,142 | ||||

| 1,031,000 |

Nexstar Media, Inc. (a) (b) |

4.75% | 11/01/28 | 913,546 | ||||

| 611,000 |

Scripps Escrow II, Inc. (a) (b) |

3.88% | 01/15/29 | 513,967 | ||||

| 17,974,000 |

Sinclair Television Group, Inc. (a) (b) |

5.13% | 02/15/27 | 15,704,782 | ||||

| 7,069,000 |

Sirius XM Radio, Inc. (a) (b) |

3.13% | 09/01/26 | 6,510,266 | ||||

| 343,000 |

Sirius XM Radio, Inc. (a) (b) |

5.50% | 07/01/29 | 318,990 | ||||

| 8,987,000 |

Tegna Inc. (b) |

4.63% | 03/15/28 | 8,206,749 | ||||

| 2,027,000 |

Univision Communications, Inc. (a) (b) |

6.63% | 06/01/27 | 1,999,838 | ||||

| 79,578,258 | ||||||||

| Building Products – 0.3% | ||||||||

| 588,000 |

Beacon Roofing Supply, Inc (a) (b) |

6.50% | 08/01/30 | 587,761 | ||||

| 574,000 |

Standard Industries, Inc. (a) (b) |

4.75% | 01/15/28 | 540,050 | ||||

| 858,000 |

Standard Industries, Inc. (a) (b) |

4.38% | 07/15/30 | 752,876 | ||||

| 1,880,687 | ||||||||

| Cable & Satellite – 7.1% | ||||||||

| 7,413,000 |

CCO Holdings, LLC/CCO Holdings Capital Corp. (a) (b) |

5.38% | 06/01/29 | 6,878,868 | ||||

| 4,567,000 |

CCO Holdings, LLC/CCO Holdings Capital Corp. (a) (b) |

6.38% | 09/01/29 | 4,409,670 | ||||

| 3,427,000 |

CCO Holdings, LLC/CCO Holdings Capital Corp. (a) (b) |

4.75% | 03/01/30 | 3,001,355 | ||||

| 3,993,000 |

CCO Holdings, LLC/CCO Holdings Capital Corp. (a) (b) |

4.50% | 08/15/30 | 3,428,540 | ||||

| 1,155,000 |

CCO Holdings, LLC/CCO Holdings Capital Corp. (a) (b) |

4.25% | 02/01/31 | 964,221 | ||||

| 3,219,000 |

CCO Holdings, LLC/CCO Holdings Capital Corp. (a) (b) |

7.38% | 03/03/31 | 3,222,541 | ||||

| 1,621,000 |

CCO Holdings, LLC/CCO Holdings Capital Corp. (a) (b) |

4.50% | 06/01/33 | 1,297,977 | ||||

| 2,370,000 |

CSC Holdings, LLC (a) (b) |

7.50% | 04/01/28 | 1,623,152 | ||||

| 667,000 |

CSC Holdings, LLC (a) (b) |

11.25% | 05/15/28 | 666,472 | ||||

| 10,569,000 |

CSC Holdings, LLC (a) (b) |

5.75% | 01/15/30 | 5,979,887 | ||||

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| CORPORATE BONDS AND NOTES (Continued) | ||||||||

| Cable & Satellite (Continued) | ||||||||

| $3,000,000 |

CSC Holdings, LLC (a) (b) |

4.63% | 12/01/30 | $1,654,730 | ||||

| 250,000 |

CSC Holdings, LLC (a) (b) |

3.38% | 02/15/31 | 170,693 | ||||

| 10,306,000 |

CSC Holdings, LLC (a) (b) |

4.50% | 11/15/31 | 7,302,425 | ||||

| 40,600,531 | ||||||||

| Casinos & Gaming – 4.2% | ||||||||

| 1,438,000 |

Boyd Gaming Corp. (a) (b) |

4.75% | 06/15/31 | 1,273,695 | ||||

| 1,999,000 |

Caesars Entertainment, Inc. (a) (b) |

4.63% | 10/15/29 | 1,757,841 | ||||

| 77,000 |

Caesars Entertainment, Inc. (a) (b) |

7.00% | 02/15/30 | 77,142 | ||||

| 71,000 |

CDI Escrow Issuer, Inc. (a) (b) |

5.75% | 04/01/30 | 66,709 | ||||

| 9,182,000 |

Fertitta Entertainment, LLC/Fertitta Entertainment Finance Co., Inc. (a) (b) |

6.75% | 01/15/30 | 7,756,903 | ||||

| 930,000 |

Light & Wonder (FKA Scientific Games International Inc) (a) (b) |

7.50% | 09/01/31 | 944,253 | ||||

| 170,000 |

MGM Resorts International (b) |

6.75% | 05/01/25 | 170,468 | ||||

| 582,000 |

MGM Resorts International (b) |

5.75% | 06/15/25 | 579,108 | ||||

| 284,000 |

Scientific Games Holdings L.P./Scientific Games US FinCo, Inc. (a) (b) |

6.63% | 03/01/30 | 254,397 | ||||

| 2,694,000 |

Station Casinos, LLC (a) (b) |

4.50% | 02/15/28 | 2,438,676 | ||||

| 1,624,000 |

VICI Properties L.P./VICI Note Co., Inc. (a) (b) |

3.50% | 02/15/25 | 1,571,805 | ||||

| 7,698,000 |

VICI Properties L.P./VICI Note Co., Inc. (a) (b) |

4.25% | 12/01/26 | 7,258,031 | ||||

| 60,000 |

VICI Properties L.P./VICI Note Co., Inc. (a) (b) |

3.75% | 02/15/27 | 55,599 | ||||

| 24,204,627 | ||||||||

| Commercial Printing – 0.8% | ||||||||

| 2,000,000 |

Multi-Color Corp. (LABL, Inc.) (a) (b) |

6.75% | 07/15/26 | 1,902,659 | ||||

| 471,000 |

Multi-Color Corp. (LABL, Inc.) (a) (b) |

10.50% | 07/15/27 | 428,430 | ||||

| 2,612,000 |

Multi-Color Corp. (LABL, Inc.) (a) (b) |

9.50% | 11/01/28 | 2,523,849 | ||||

| 4,854,938 | ||||||||

| Construction & Engineering – 0.6% | ||||||||

| 3,855,000 |

Pike Corp. (a) (b) |

5.50% | 09/01/28 | 3,514,970 | ||||

| Construction Materials – 0.9% | ||||||||

| 74,000 |

GYP Holdings III Corp. (a) (b) |

4.63% | 05/01/29 | 64,240 | ||||

| 5,167,000 |

Summit Materials, LLC (a) (b) |

5.25% | 01/15/29 | 4,836,286 | ||||

| 160,000 |

Summit Materials, LLC (a) (b) |

7.25% | 01/15/31 | 161,179 | ||||

| 5,061,705 | ||||||||

| Consumer Finance – 0.5% | ||||||||

| 3,056,000 |

FirstCash, Inc. (a) (b) |

4.63% | 09/01/28 | 2,801,461 | ||||

| Diversified Financial Services – 0.1% | ||||||||

| 638,000 |

GTCR W-2 Merger Sub, LLC (a) (b) |

7.50% | 01/15/31 | 650,489 | ||||

| Diversified Support Services – 0.3% | ||||||||

| 901,000 |

Ritchie Bros. Auctioneers, Inc. (a) (b) |

6.75% | 03/15/28 | 918,759 | ||||

| 625,000 |

Ritchie Bros. Auctioneers, Inc. (a) (b) |

7.75% | 03/15/31 | 649,281 | ||||

| 1,568,040 | ||||||||

| Electric Utilities – 0.4% | ||||||||

| 1,588,000 |

Vistra Operations Co., LLC (a) (b) |

5.00% | 07/31/27 | 1,512,419 | ||||

| 641,000 |

Vistra Operations Co., LLC (a) (b) |

7.75% | 10/15/31 | 656,627 | ||||

| 2,169,046 | ||||||||

| Electrical Components & Equipment – 0.0% | ||||||||

| 333,000 |

Sensata Technologies, Inc. (a) (b) |

3.75% | 02/15/31 | 281,876 | ||||

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| CORPORATE BONDS AND NOTES (Continued) | ||||||||

| Environmental & Facilities Services – 0.5% | ||||||||

| $2,822,000 |

Waste Pro USA, Inc. (a) (b) |

5.50% | 02/15/26 | $2,665,605 | ||||

| Financial Exchanges & Data – 0.4% | ||||||||

| 2,550,000 |

MSCI, Inc. (a) (b) |

3.25% | 08/15/33 | 2,039,430 | ||||

| Food Distributors – 0.1% | ||||||||

| 603,000 |

US Foods, Inc. (a) (b) |

4.75% | 02/15/29 | 559,411 | ||||

| Health Care Facilities – 2.1% | ||||||||

| 1,510,000 |

Acadia Healthcare Co., Inc. (a) (b) |

5.00% | 04/15/29 | 1,410,732 | ||||

| 2,218,000 |

HCA, Inc. (b) |

5.88% | 02/15/26 | 2,222,846 | ||||

| 569,000 |

HCA, Inc. (b) |

5.38% | 09/01/26 | 566,330 | ||||

| 7,842,000 |

Select Medical Corp. (a) (b) |

6.25% | 08/15/26 | 7,791,086 | ||||

| 250,000 |

Tenet Healthcare Corp. (b) |

5.13% | 11/01/27 | 240,121 | ||||

| 12,231,115 | ||||||||

| Health Care Services – 1.7% | ||||||||

| 2,013,000 |

DaVita, Inc. (a) (b) |

4.63% | 06/01/30 | 1,702,967 | ||||

| 551,000 |

DaVita, Inc. (a) (b) |

3.75% | 02/15/31 | 431,811 | ||||

| 10,403,000 |

Global Medical Response, Inc. (a) (b) |

6.50% | 10/01/25 | 7,708,207 | ||||

| 9,842,985 | ||||||||

| Health Care Supplies – 2.3% | ||||||||

| 9,847,000 |

Medline Borrower L.P. (a) (b) |

3.88% | 04/01/29 | 8,747,204 | ||||

| 4,833,000 |

Medline Borrower L.P. (a) (b) |

5.25% | 10/01/29 | 4,377,128 | ||||

| 13,124,332 | ||||||||

| Health Care Technology – 2.7% | ||||||||

| 6,527,000 |

AthenaHealth Group, Inc. (a) (b) |

6.50% | 02/15/30 | 5,661,966 | ||||

| 1,365,000 |

HealthEquity, Inc. (a) (b) |

4.50% | 10/01/29 | 1,230,872 | ||||

| 8,552,000 |

Verscend Escrow Corp. (a) (b) |

9.75% | 08/15/26 | 8,591,493 | ||||

| 15,484,331 | ||||||||

| Hotels, Resorts & Cruise Lines – 0.0% | ||||||||

| 289,000 |

Wyndham Hotels & Resorts, Inc. (a) (b) |

4.38% | 08/15/28 | 266,228 | ||||

| Household Products – 0.6% | ||||||||

| 1,121,000 |

Energizer Holdings, Inc. (a) (b) |

6.50% | 12/31/27 | 1,089,338 | ||||

| 1,746,000 |

Energizer Holdings, Inc. (a) (b) |

4.75% | 06/15/28 | 1,562,146 | ||||

| 650,000 |

Energizer Holdings, Inc. (a) (b) |

4.38% | 03/31/29 | 561,145 | ||||

| 3,212,629 | ||||||||

| Human Resource & Employment Services – 0.1% | ||||||||

| 314,000 |

TriNet Group, Inc. (a) (b) |

7.13% | 08/15/31 | 317,376 | ||||

| Independent Power Producers & Energy Traders – 0.6% | ||||||||

| 3,627,000 |

Calpine Corp. (a) (b) |

5.13% | 03/15/28 | 3,416,264 | ||||

| Industrial Machinery & Supplies & Components – 1.5% | ||||||||

| 2,049,000 |

Emerald Debt Merger Sub, LLC (a) (b) |

6.63% | 12/15/30 | 2,046,439 | ||||

| 6,597,000 |

Gates Global, LLC/Gates Corp. (a) (b) |

6.25% | 01/15/26 | 6,530,205 | ||||

| 8,576,644 | ||||||||

| Insurance Brokers – 13.5% | ||||||||

| 12,321,000 |

Alliant Holdings Intermediate, LLC/Alliant Holdings Co-Issuer (a) (b) |

6.75% | 10/15/27 | 11,828,160 | ||||

| 7,588,000 |

Alliant Holdings Intermediate, LLC/Alliant Holdings Co-Issuer (a) (b) |

6.75% | 04/15/28 | 7,588,635 | ||||

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| CORPORATE BONDS AND NOTES (Continued) | ||||||||

| Insurance Brokers (Continued) | ||||||||

| $210,000 |

Alliant Holdings Intermediate, LLC/Alliant Holdings Co-Issuer (a) (b) |

5.88% | 11/01/29 | $190,071 | ||||

| 12,603,000 |

AmWINS Group, Inc. (a) (b) |

4.88% | 06/30/29 | 11,352,132 | ||||

| 8,980,000 |

AssuredPartners, Inc. (a) (b) |

7.00% | 08/15/25 | 8,965,036 | ||||

| 13,689,000 |

AssuredPartners, Inc. (a) (b) |

5.63% | 01/15/29 | 12,245,021 | ||||

| 2,092,000 |

BroadStreet Partners, Inc. (a) (b) |

5.88% | 04/15/29 | 1,903,010 | ||||

| 675,000 |

Brown & Brown, Inc. (b) |

2.38% | 03/15/31 | 537,972 | ||||

| 1,211,000 |

GTCR AP Finance, Inc. (a) (b) |

8.00% | 05/15/27 | 1,208,234 | ||||

| 12,908,000 |

HUB International Ltd. (a) (b) |

7.00% | 05/01/26 | 12,851,802 | ||||

| 4,934,000 |

HUB International Ltd. (a) (b) |

5.63% | 12/01/29 | 4,477,138 | ||||

| 800,000 |

National Financial Partners Corp. (NFP) (a) (b) |

6.88% | 08/15/28 | 713,152 | ||||

| 3,801,000 |

Ryan Specialty Group, LLC (a) (b) |

4.38% | 02/01/30 | 3,435,154 | ||||

| 77,295,517 | ||||||||

| Integrated Telecommunication Services – 1.0% | ||||||||

| 61,000 |

Zayo Group Holdings, Inc. (a) (b) |

4.00% | 03/01/27 | 46,608 | ||||

| 8,267,000 |

Zayo Group Holdings, Inc. (a) (b) |

6.13% | 03/01/28 | 5,559,091 | ||||

| 5,605,699 | ||||||||

| Interactive Media & Services – 1.4% | ||||||||

| 8,270,000 |

Cars.com, Inc. (a) (b) |

6.38% | 11/01/28 | 7,834,169 | ||||

| Internet Services & Infrastructure – 2.0% | ||||||||

| 6,210,000 |

Go Daddy Operating Co., LLC/GD Finance Co., Inc. (a) (b) |

5.25% | 12/01/27 | 6,013,066 | ||||

| 5,979,000 |

Go Daddy Operating Co., LLC/GD Finance Co., Inc. (a) (b) |

3.50% | 03/01/29 | 5,269,596 | ||||

| 11,282,662 | ||||||||

| Investment Banking & Brokerage – 0.2% | ||||||||

| 1,045,000 |

LPL Holdings, Inc. (a) (b) |

4.63% | 11/15/27 | 984,339 | ||||

| IT Consulting & Other Services – 0.4% | ||||||||

| 613,000 |

CDK Global Inc. (Central Parent, Inc.) (a) (b) |

7.25% | 06/15/29 | 612,887 | ||||

| 2,000,000 |

Gartner, Inc. (a) (b) |

4.50% | 07/01/28 | 1,875,108 | ||||

| 2,487,995 | ||||||||

| Leisure Facilities – 0.0% | ||||||||

| 283,000 |

SeaWorld Parks & Entertainment, Inc. (a) (b) |

5.25% | 08/15/29 | 259,702 | ||||

| Leisure Products – 0.3% | ||||||||

| 1,413,000 |

Acushnet Co. (a) (b) |

7.38% | 10/15/28 | 1,452,218 | ||||

| Managed Health Care – 1.8% | ||||||||

| 6,806,000 |

Centene Corp. (b) |

4.25% | 12/15/27 | 6,430,479 | ||||

| 968,000 |

Molina Healthcare, Inc. (a) (b) |

4.38% | 06/15/28 | 898,453 | ||||

| 2,577,000 |

MPH Acquisition Holdings, LLC (a) (b) |

5.50% | 09/01/28 | 2,241,294 | ||||

| 1,296,000 |

MPH Acquisition Holdings, LLC (a) (b) |

5.75% | 11/01/28 | 1,005,029 | ||||

| 10,575,255 | ||||||||

| Metal, Glass & Plastic Containers – 2.5% | ||||||||

| 903,000 |

Ball Corp. (b) |

6.88% | 03/15/28 | 923,147 | ||||

| 4,227,000 |

Ball Corp. (b) |

2.88% | 08/15/30 | 3,504,908 | ||||

| 5,419,000 |

Berry Global, Inc. (a) (b) |

5.63% | 07/15/27 | 5,302,362 | ||||

| 75,000 |

Crown Americas, LLC (b) |

5.25% | 04/01/30 | 71,003 | ||||

| 4,321,000 |

Owens-Brockway Glass Container, Inc. (a) (b) |

7.25% | 05/15/31 | 4,294,037 | ||||

| 14,095,457 | ||||||||

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| CORPORATE BONDS AND NOTES (Continued) | ||||||||

| Movies & Entertainment – 1.2% | ||||||||

| $4,380,000 |

Live Nation Entertainment, Inc. (a) (b) |

5.63% | 03/15/26 | $4,264,626 | ||||

| 2,620,000 |

Live Nation Entertainment, Inc. (a) (b) |

4.75% | 10/15/27 | 2,465,394 | ||||

| 394,000 |

WMG Acquisition Corp. (a) (b) |

3.00% | 02/15/31 | 325,891 | ||||

| 7,055,911 | ||||||||

| Office Services & Supplies – 0.1% | ||||||||

| 520,000 |

Dun & Bradstreet Corp. (a) (b) |

5.00% | 12/15/29 | 470,197 | ||||

| Paper & Plastic Packaging Products & Materials – 3.4% | ||||||||

| 12,810,000 |

Graham Packaging Co., Inc. (a) (b) |

7.13% | 08/15/28 | 11,283,881 | ||||

| 6,990,000 |

Pactiv Evergreen Group Issuer, Inc./Pactiv Evergreen Group Issuer, LLC (a) (b) |

4.00% | 10/15/27 | 6,402,455 | ||||

| 180,000 |

Pactiv, LLC (b) |

7.95% | 12/15/25 | 181,288 | ||||

| 1,070,000 |

Sealed Air Corp. (a) (b) |

6.13% | 02/01/28 | 1,059,306 | ||||

| 566,000 |

Sealed Air Corp. (a) (b) |

5.00% | 04/15/29 | 528,097 | ||||

| 19,455,027 | ||||||||

| Personal Care Products – 0.2% | ||||||||

| 1,389,000 |

Prestige Brands, Inc. (a) (b) |

5.13% | 01/15/28 | 1,321,165 | ||||

| Pharmaceuticals – 0.2% | ||||||||

| 1,259,000 |

IQVIA, Inc. (a) (b) |

6.50% | 05/15/30 | 1,271,212 | ||||

| Research & Consulting Services – 0.9% | ||||||||

| 973,000 |

Clarivate Science Holdings Corp. (a) (b) |

3.88% | 07/01/28 | 878,886 | ||||

| 3,114,000 |

Clarivate Science Holdings Corp. (a) (b) |

4.88% | 07/01/29 | 2,789,165 | ||||

| 1,493,000 |

CoreLogic, Inc. (a) (b) |

4.50% | 05/01/28 | 1,251,903 | ||||

| 4,919,954 | ||||||||

| Restaurants – 1.0% | ||||||||

| 5,088,000 |

IRB Holding Corp. (a) (b) |

7.00% | 06/15/25 | 5,083,189 | ||||

| 812,000 |

Raising Cane’s Restaurants, LLC (a) (b) |

9.38% | 05/01/29 | 853,651 | ||||

| 5,936,840 | ||||||||

| Security & Alarm Services – 0.3% | ||||||||

| 2,000,000 |

Brink’s (The) Co. (a) (b) |

4.63% | 10/15/27 | 1,876,521 | ||||

| Specialized Consumer Services – 0.8% | ||||||||

| 4,932,000 |

Aramark Services, Inc. (a) (b) |

5.00% | 02/01/28 | 4,671,695 | ||||

| Specialized Finance – 0.1% | ||||||||

| 1,149,000 |

Radiate HoldCo, LLC/Radiate Finance, Inc. (a) (b) |

4.50% | 09/15/26 | 857,206 | ||||

| Specialty Chemicals – 1.3% | ||||||||

| 8,153,000 |

Avantor Funding, Inc. (a) (b) |

4.63% | 07/15/28 | 7,633,660 | ||||

| Systems Software – 5.7% | ||||||||

| 2,724,000 |

Boxer Parent Co., Inc. (a) (b) |

9.13% | 03/01/26 | 2,727,575 | ||||

| 3,484,000 |

Gen Digital, Inc. (a) (b) |

7.13% | 09/30/30 | 3,562,115 | ||||

| 1,000,000 |

Oracle Corp. (b) |

6.15% | 11/09/29 | 1,049,655 | ||||

| 1,000,000 |

Oracle Corp. (b) |

6.25% | 11/09/32 | 1,053,502 | ||||

| 1,796,000 |

Oracle Corp. (b) |

6.50% | 04/15/38 | 1,923,420 | ||||

| 22,995,000 |

SS&C Technologies, Inc. (a) (b) |

5.50% | 09/30/27 | 22,275,031 | ||||

| 32,591,298 | ||||||||

| Trading Companies & Distributors – 2.1% | ||||||||

| 1,794,000 |

Herc Holdings, Inc. (a) (b) |

5.50% | 07/15/27 | 1,743,314 | ||||

| 1,035,000 |

SRS Distribution, Inc. (a) (b) |

6.13% | 07/01/29 | 914,871 | ||||

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| CORPORATE BONDS AND NOTES (Continued) | ||||||||

| Trading Companies & Distributors (Continued) | ||||||||

| $588,000 |

SRS Distribution, Inc. (a) (b) |

6.00% | 12/01/29 | $512,039 | ||||

| 8,786,000 |

United Rentals, Inc. (a) (b) |

6.00% | 12/15/29 | 8,779,122 | ||||

| 11,949,346 | ||||||||

|

Total Corporate Bonds and Notes |

498,823,733 | |||||||

| (Cost $531,794,937) | ||||||||

| Principal Value |

Description | Rate (c) | Stated Maturity (d) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS – 21.9% | ||||||||

| Application Software – 7.9% | ||||||||

| 705,785 |

Applied Systems, Inc., 2026 Term Loan, 3 Mo. CME Term SOFR + 4.50%, 0.50% Floor (b) |

9.89% | 09/18/26 | 709,152 | ||||

| 8,609,622 |

Gainwell Acquisition Corp. (fka Milano), Term Loan B, 3 Mo. CME Term SOFR + CSA + 4.00%, 0.75% Floor (b) |

9.49% | 10/01/27 | 8,322,620 | ||||

| 4,397,599 |

Greeneden U.S. Holdings II, LLC (Genesys Telecommunications Laboratories, Inc.), Initial Dollar Term Loan, 1

Mo. CME Term SOFR + CSA + 4.00%, 0.75% Floor (b) |

9.46% | 12/01/27 | 4,408,087 | ||||

| 6,398,085 |

Informatica Corporation, Initial Term Loan B, 1 Mo. CME Term SOFR + CSA + 2.75%, 0.00% Floor (b) |

8.21% | 10/29/28 | 6,395,685 | ||||

| 3,124,082 |

Internet Brands, Inc. (Web MD/MH Sub I. LLC), 2020 June New Term Loan, 1 Mo. CME Term SOFR + CSA + 3.75%, 1.00%

Floor (b) |

9.21% | 09/15/24 | 3,131,252 | ||||

| 8,877,441 |

Internet Brands, Inc. (Web MD/MH Sub I. LLC), 2nd Lien Term Loan, 1 Mo. CME Term SOFR + 6.25%, 0.00% Floor (b) |

11.60% | 02/23/29 | 8,078,471 | ||||

| 1,871,873 |

Internet Brands, Inc. (Web MD/MH Sub I. LLC), Initial Term Loan, 1 Mo. CME Term SOFR + CSA + 3.75%, 0.00% Floor

(b) |

9.21% | 09/13/24 | 1,875,383 | ||||

| 110,976 |

ION Trading Technologies Limited, Term Loan B, 3 Mo. CME Term SOFR + CSA + 4.75%, 0.00% Floor (b) |

10.24% | 04/01/28 | 110,460 | ||||

| 5,798,394 |

LogMeIn, Inc. (GoTo Group, Inc.), Term Loan B, 3 Mo. CME Term SOFR + CSA + 4.75%, 0.00% Floor (b) |

10.28% | 08/31/27 | 3,855,932 | ||||

| 3,538,182 |

RealPage, Inc., Second Lien Term Loan, 1 Mo. CME Term SOFR + CSA + 6.50%, 0.75% Floor (b) |

11.96% | 04/22/29 | 3,529,337 | ||||

| 1,193,924 |

Ultimate Kronos Group (UKG, Inc.), 2021 Term Loan, 3 Mo. CME Term SOFR + CSA + 3.25%, 0.50% Floor (b) |

8.76% | 05/03/26 | 1,196,163 | ||||

| 3,669,025 |

Ultimate Kronos Group (UKG, Inc.), Initial Term Loan B, 3 Mo. CME Term SOFR + CSA + 3.75%, 0.00% Floor (b) |

9.23% | 05/03/26 | 3,682,931 | ||||

| 45,295,473 | ||||||||

| Cable & Satellite – 0.3% | ||||||||

| 1,542,555 |

Cablevision (aka CSC Holdings, LLC), March 2017 Term Loan B-1, 1 Mo. LIBOR + 2.25%, 0.00% Floor (b) |

7.69% | 07/17/25 | 1,512,089 | ||||

| Education Services – 0.0% | ||||||||

| 142,291 |

Ascensus Holdings, Inc. (Mercury), Second Lien Term Loan, 3 Mo. CME Term SOFR + CSA + 6.50%, 0.50% Floor |

12.18% | 08/02/29 | 136,184 | ||||

| Electric Utilities – 0.4% | ||||||||

| 2,499,223 |

PG&E Corp., Term Loan B, 1 Mo. CME Term SOFR + CSA + 3.00%, 0.50% Floor (b) |

8.46% | 06/23/25 | 2,504,496 | ||||

| Electronic Equipment & Instruments – 0.5% | ||||||||

| 2,921,338 |

Verifone Systems, Inc., Term Loan B, 3 Mo. CME Term SOFR + 4.00%, 0.00% Floor (b) |

9.64% | 08/20/25 | 2,780,573 | ||||

| Principal Value |

Description | Rate (c) | Stated Maturity (d) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS (Continued) | ||||||||

| Health Care Facilities – 0.5% | ||||||||

| $445,372 |

Charlotte Buyer, Inc., Initial Term B Loan, 1 Mo. CME Term SOFR + 5.25%, 0.50% Floor (b) |

10.57% | 02/11/28 | $445,619 | ||||

| 2,430,772 |

Select Medical Corp., Tranche B-1, 1 Mo. CME Term SOFR + 3.00%, 0.00% Floor (b) |

8.35% | 03/08/27 | 2,434,564 | ||||

| 2,880,183 | ||||||||

| Health Care Technology – 6.5% | ||||||||

| 1,950,701 |

Ciox Health (Healthport/CT Technologies Intermediate Holdings, Inc.), New Term Loan B, 1 Mo. CME Term SOFR +

CSA + 4.25%, 0.75% Floor (b) |

9.71% | 12/16/25 | 1,859,262 | ||||

| 9,319,915 |

Navicure, Inc. (Waystar Technologies, Inc.), Term Loan B, 1 Mo. CME Term SOFR + CSA + 4.00%, 0.00% Floor (b) |

9.46% | 10/23/26 | 9,356,029 | ||||

| 17,695,157 |

Verscend Technologies, Inc. (Cotiviti), New Term Loan B-1, 1 Mo. CME Term SOFR + CSA + 4.00%, 0.00% Floor (b) |

9.46% | 08/27/25 | 17,737,537 | ||||

| 7,951,465 |

Zelis Payments Buyer, Inc., New Term Loan B-1, 1 Mo. CME Term SOFR + CSA + 3.50%, 0.00% Floor (b) |

8.96% | 09/30/26 | 7,966,732 | ||||

| 36,919,560 | ||||||||

| Industrial Machinery & Supplies & Components – 0.8% | ||||||||

| 4,323,751 |

Filtration Group Corporation, 2023 Extended Term Loan, 1 Mo. CME Term SOFR + CSA + 4.25%, 0.50% Floor (b) |

9.71% | 10/21/28 | 4,336,355 | ||||

| Insurance Brokers – 3.8% | ||||||||

| 539,273 |

Alliant Holdings I, LLC, Term Loan B-5, 1 Mo. CME Term SOFR + 3.50%, 0.50% Floor (b) |

8.83% | 11/05/27 | 540,482 | ||||

| 6,486,925 |

HUB International Ltd., 2023 Refinancing Term Loan B-5, 3 Mo. CME Term SOFR + 4.25%, 0.75% Floor (b) |

9.66% | 06/20/30 | 6,520,397 | ||||

| 939,058 |

HUB International Ltd., Term Loan B4, 3 Mo. CME Term SOFR + 4.00%, 0.75% Floor (b) |

9.37% | 11/10/29 | 942,772 | ||||

| 5,234,286 |

OneDigital Borrower LLC, Term Loan B, 1 Mo. CME Term SOFR + CSA + 4.25%, 0.50% Floor (b) |

9.70% | 11/16/27 | 5,224,471 | ||||

| 5,335,930 |

Ryan Specialty Group, LLC, Term Loan B, 1 Mo. CME Term SOFR + CSA + 3.00%, 0.75% Floor (b) |

8.45% | 09/01/27 | 5,352,605 | ||||

| 3,275,024 |

USI, Inc. (fka Compass Investors Inc.), 2023 Refi Tranche, 1 Mo. CME Term SOFR + 3.25%, 0.00% Floor (b) |

8.64% | 09/27/30 | 3,275,270 | ||||

| 21,855,997 | ||||||||

| Integrated Telecommunication Services – 0.1% | ||||||||

| 450,834 |

Altice France S.A., Term Loan B-13, 3 Mo. LIBOR + 4.00%, 0.00% Floor (b) |

9.64% | 08/14/26 | 421,448 | ||||

| 61,000 |

Zayo Group Holdings, Inc., Initial Dollar Term Loan, 1 Mo. CME Term SOFR + CSA + 3.00%, 0.00% Floor (b) |

8.46% | 03/09/27 | 52,311 | ||||

| 473,759 | ||||||||

| Life Sciences Tools & Services – 0.2% | ||||||||

| 1,344,253 |

WCG Purchaser Corp. (WIRB-Copernicus Group), Term Loan B, 1 Mo. CME Term SOFR + CSA + 4.00%, 1.00% Floor (b) |

9.46% | 01/08/27 | 1,325,433 | ||||

| Metal, Glass & Plastic Containers – 0.5% | ||||||||

| 2,661,286 |

ProAmpac PG Borrower, LLC, First Lien Term Loan, 3 Mo. CME Term SOFR + 4.50%, 0.75% Floor (b) |

9.87%-9.89% | 09/15/28 | 2,647,980 | ||||

| Security & Alarm Services – 0.1% | ||||||||

| 726,880 |

Garda World Security Corp., Term Loan B-2, 3 Mo. CME Term SOFR + CSA + 4.25%, 0.00% Floor (b) |

9.75% | 10/30/26 | 726,782 | ||||

| Principal Value |

Description | Rate (c) | Stated Maturity (d) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS (Continued) | ||||||||

| Systems Software – 0.3% | ||||||||

| $1,807,320 |

BMC Software Finance, Inc. (Boxer Parent), 2021 Replacement Dollar Term Loan, 1 Mo. CME Term SOFR + CSA + 3.75%,

0.00% Floor (b) |

9.21% | 10/02/25 | $1,809,661 | ||||

|

Total Senior Floating-Rate Loan Interests |

125,204,525 | |||||||

| (Cost $127,844,256) | ||||||||

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| FOREIGN CORPORATE BONDS AND NOTES – 13.6% | ||||||||

| Application Software – 3.8% | ||||||||

| 1,721,000 |

ION Trading Technologies S.A.R.L. (a) (b) |

5.75% | 05/15/28 | 1,464,916 | ||||

| 11,666,000 |

Open Text Corp. (a) (b) |

6.90% | 12/01/27 | 12,005,625 | ||||

| 6,881,000 |

Open Text Corp. (a) (b) |

3.88% | 02/15/28 | 6,269,656 | ||||

| 2,108,000 |

Open Text Corp. (a) (b) |

3.88% | 12/01/29 | 1,845,328 | ||||

| 21,585,525 | ||||||||

| Automotive Parts & Equipment – 1.5% | ||||||||

| 8,691,000 |

Clarios Global LP (Power Solutions) (a) (b) |

8.50% | 05/15/27 | 8,759,372 | ||||

| Building Products – 0.2% | ||||||||

| 973,000 |

Cemex S.A.B. de C.V. (a) |

5.45% | 11/19/29 | 925,528 | ||||

| Data Processing & Outsourced Services – 0.8% | ||||||||

| 5,748,000 |

Paysafe Finance PLC/Paysafe Holdings US Corp. (a) (b) |

4.00% | 06/15/29 | 4,754,918 | ||||

| Environmental & Facilities Services – 1.1% | ||||||||

| 473,000 |

GFL Environmental, Inc. (a) (b) |

3.75% | 08/01/25 | 457,219 | ||||

| 3,000,000 |

GFL Environmental, Inc. (a) (b) |

5.13% | 12/15/26 | 2,912,734 | ||||

| 1,300,000 |

GFL Environmental, Inc. (a) (b) |

4.00% | 08/01/28 | 1,161,291 | ||||

| 1,686,000 |

GFL Environmental, Inc. (a) (b) |

4.75% | 06/15/29 | 1,541,657 | ||||

| 6,072,901 | ||||||||

| Integrated Telecommunication Services – 1.3% | ||||||||

| 3,069,000 |

Altice France S.A. (a) (b) |

10.50% | 05/15/27 | 1,633,021 | ||||

| 2,511,000 |

Altice France S.A. (a) (b) |

5.50% | 01/15/28 | 1,924,177 | ||||

| 1,000,000 |

Altice France S.A. (a) (b) |

5.13% | 01/15/29 | 727,102 | ||||

| 4,590,000 |

Altice France S.A. (a) (b) |

5.13% | 07/15/29 | 3,287,610 | ||||

| 7,571,910 | ||||||||

| Metal, Glass & Plastic Containers – 1.2% | ||||||||

| 7,245,000 |

Trivium Packaging Finance B.V. (a) (b) |

5.50% | 08/15/26 | 6,970,775 | ||||

| Restaurants – 2.1% | ||||||||

| 14,344,000 |

1011778 BC ULC/New Red Finance, Inc. (a) (b) |

4.00% | 10/15/30 | 12,376,613 | ||||

| Security & Alarm Services – 0.7% | ||||||||

| 4,034,000 |

Garda World Security Corp. (a) (b) |

7.75% | 02/15/28 | 4,075,913 | ||||

| Trading Companies & Distributors – 0.9% | ||||||||

| 2,721,000 |

VistaJet Malta Finance PLC/XO Management Holding, Inc. (a) (b) |

7.88% | 05/01/27 | 2,301,136 | ||||

| 3,858,000 |

VistaJet Malta Finance PLC/XO Management Holding, Inc. (a) (b) |

6.38% | 02/01/30 | 2,701,800 | ||||

| 5,002,936 | ||||||||

|

Total Foreign Corporate Bonds and Notes |

78,096,391 | |||||||

| (Cost $81,918,767) | ||||||||

| Shares | Description | Value | ||

| COMMON STOCKS – 0.0% | ||||

| Pharmaceuticals – 0.0% | ||||

| 220,989 |

Akorn, Inc. (e) (f) (g) |

$248,613 | ||

| (Cost $2,534,056) | ||||

| MONEY MARKET FUNDS – 0.4% | ||||

| 2,069,779 |

Morgan Stanley Institutional Liquidity Funds - Treasury Portfolio - Institutional Class - 5.23% (b) (h) |

2,069,779 | ||

| (Cost $2,069,779) | ||||

|

Total Investments – 122.9% |

704,443,041 | |||

| (Cost $746,161,795) | ||||

|

Outstanding Loan – (23.9)% |

(137,000,000) | |||

|

Net Other Assets and Liabilities – 1.0% |

5,914,361 | |||

|

Net Assets – 100.0% |

$573,357,402 | |||

| (a) | This security, sold within the terms of a private placement memorandum, is exempt from registration upon resale under Rule 144A of the Securities Act of 1933, as amended (the “1933 Act”), and may be resold in transactions exempt from registration, normally to qualified institutional buyers. Pursuant to procedures adopted by the Fund’s Board of Trustees, this security has been determined to be liquid by First Trust Advisors L.P. (the “Advisor”). Although market instability can result in periods of increased overall market illiquidity, liquidity for each security is determined based on security specific factors and assumptions, which require subjective judgment. At November 30, 2023, securities noted as such amounted to $531,493,253 or 92.7% of net assets. |

| (b) | All or a portion of this security serves as collateral for the outstanding loan. At November 30, 2023, the segregated value of these securities amounts to $703,132,716. |

| (c) | Senior Floating-Rate Loan Interests (“Senior Loans”) in which the Fund invests pay interest at rates which are periodically predetermined by reference to a base lending rate plus a premium. These base lending rates are generally (i) the lending rate offered by one or more major European banks, such as the LIBOR, (ii) the SOFR obtained from the U.S. Department of the Treasury’s Office of Financial Research or another major financial institution, (iii) the prime rate offered by one or more United States banks or (iv) the certificate of deposit rate. Certain Senior Loans are subject to a LIBOR or SOFR floor that establishes a minimum LIBOR or SOFR rate. When a range of rates is disclosed, the Fund holds more than one contract within the same tranche with identical LIBOR or SOFR period, spread and floor, but different LIBOR or SOFR reset dates. |

| (d) | Senior Loans generally are subject to mandatory and/or optional prepayment. As a result, the actual remaining maturity of Senior Loans may be substantially less than the stated maturities shown. |

| (e) | This issuer has filed for protection in bankruptcy court. |

| (f) | Security received in a transaction exempt from registration under the 1933 Act. The security may be resold pursuant to an exemption from registration under the 1933 Act, typically to qualified institutional buyers (see Note 2E - Restricted Securities in the Notes to Financial Statements). |

| (g) | Non-income producing security. |

| (h) | Rate shown reflects yield as of November 30, 2023. |

| Abbreviations throughout the Portfolio of Investments: | |

| CME | – Chicago Mercantile Exchange |

| CSA | – Credit Spread Adjustment |

| LIBOR | – London Interbank Offered Rate |

| SOFR | – Secured Overnight Financing Rate |

| Total Value at 11/30/2023 |

Level

1 Quoted Prices |

Level

2 Significant Observable Inputs |

Level

3 Significant Unobservable Inputs | |

|

Corporate Bonds and Notes* |

$ 498,823,733 | $ — | $ 498,823,733 | $ — |

|

Senior Floating-Rate Loan Interests* |

125,204,525 | — | 125,204,525 | — |

|

Foreign Corporate Bonds and Notes* |

78,096,391 | — | 78,096,391 | — |

|

Common Stocks* |

248,613 | — | 248,613 | — |

|

Money Market Funds |

2,069,779 | 2,069,779 | — | — |

|

Total Investments |

$ 704,443,041 | $ 2,069,779 | $ 702,373,262 | $— |

| * | See Portfolio of Investments for industry breakout. |

| ASSETS: | |

|

Investments, at value |

$ 704,443,041 |

|

Cash |

33,480 |

| Receivables: | |

|

Interest |

10,126,956 |

|

Investment securities sold |

829,024 |

|

Prepaid expenses |

15,152 |

|

Total Assets |

715,447,653 |

| LIABILITIES: | |

|

Outstanding loan |

137,000,000 |

| Payables: | |

|

Investment securities purchased |

3,167,500 |

|

Interest and fees on loan |

934,513 |

|

Investment advisory fees |

799,418 |

|

Legal fees |

71,708 |

|

Administrative fees |

45,423 |

|

Audit and tax fees |

30,785 |

|

Custodian fees |

23,159 |

|

Shareholder reporting fees |

4,890 |

|

Transfer agent fees |

2,932 |

|

Trustees’ fees and expenses |

2,293 |

|

Financial reporting fees |

771 |

|

Other liabilities |

6,859 |

|

Total Liabilities |

142,090,251 |

|

NET ASSETS |

$573,357,402 |

| NET ASSETS consist of: | |

|

Paid-in capital |

$ 713,913,444 |

|

Par value |

367,730 |

|

Accumulated distributable earnings (loss) |

(140,923,772) |

|

NET ASSETS |

$573,357,402 |

|

NET ASSET VALUE, per Common Share (par value $0.01 per Common Share) |

$15.59 |

|

Number of |

|

|

Investments, at cost |

$746,161,795 |

| INVESTMENT INCOME: | ||

|

Interest |

$ 25,774,140 | |

|

Other |

23,383 | |

|

Total investment income |

25,797,523 | |

| EXPENSES: | ||

|

Investment advisory fees |

4,700,731 | |

|

Interest and fees on loan |

4,524,688 | |

|

Administrative fees |

182,577 | |

|

Legal fees |

63,447 | |

|

Shareholder reporting fees |

57,740 | |

|

Audit and tax fees |

32,824 | |

|

Custodian fees |

20,808 | |

|

Listing expense |

17,956 | |

|

Trustees’ fees and expenses |

9,591 | |

|

Transfer agent fees |

9,117 | |

|

Financial reporting fees |

4,625 | |

|

Other |

18,485 | |

|

Total expenses |

9,642,589 | |

|

NET INVESTMENT INCOME (LOSS) |

16,154,934 | |

| NET REALIZED AND UNREALIZED GAIN (LOSS): | ||

| Net realized gain (loss) on: | ||

|

Investments |

(13,604,840) | |

|

Swap contracts |

(147,114) | |

|

Net realized gain (loss) |

(13,751,954) | |

|

Net change in unrealized appreciation (depreciation) on investments |

33,238,385 | |

|

NET REALIZED AND UNREALIZED GAIN (LOSS) |

19,486,431 | |

|

NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS |

$ 35,641,365 | |

| Six

Months Ended 11/30/2023 (Unaudited) |

Year Ended 5/31/2023 | ||

| OPERATIONS: | |||

|

Net investment income (loss) |

$ 16,154,934 | $ 33,809,782 | |

|

Net realized gain (loss) |

(13,751,954) | (66,424,648) | |

|

Net change in unrealized appreciation (depreciation) |

33,238,385 | 13,008,655 | |

|

Net increase (decrease) in net assets resulting from operations |

35,641,365 | (19,606,211) | |

| DISTRIBUTIONS TO SHAREHOLDERS FROM: | |||

|

Investment operations |

(28,682,932) | (35,642,807) | |

|

Return of capital |

— | (21,134,688) | |

|

Total distributions to shareholders |

(28,682,932) | (56,777,495) | |

|

Total increase (decrease) in net assets |

6,958,433 | (76,383,706) | |

| NET ASSETS: | |||

|

Beginning of period |

566,398,969 | 642,782,675 | |

|

End of period |

$ 573,357,402 | $ 566,398,969 | |

| COMMON SHARES: | |||

|

Common Shares at end of period |

36,772,989 | 36,772,989 |

| Cash flows from operating activities: | ||

|

Net increase (decrease) in net assets resulting from operations |

$35,641,365 | |

| Adjustments to reconcile net increase (decrease) in net assets resulting from operations to net cash provided by operating activities: | ||

|

Purchases of investments |

(253,145,558) | |

|

Sales, maturities and paydown of investments |

252,651,574 | |

|

Net amortization/accretion of premiums/discounts on investments |

(1,317,839) | |

|

Net realized gain/loss on investments |

13,604,840 | |

|

Net change in unrealized appreciation/depreciation on investments |

(33,238,385) | |

| Changes in assets and liabilities: | ||

|

Decrease in interest receivable |

217,234 | |

|

Decrease in prepaid expenses |

16,378 | |

|

Increase in interest and fees payable on loan |

193,662 | |

|

Increase in investment advisory fees payable |

6,142 | |

|

Decrease in audit and tax fees payable |

(23,176) | |

|

Increase in legal fees payable |

48,291 | |

|

Decrease in shareholder reporting fees payable |

(24,081) | |

|

Increase in administrative fees payable |

5,723 | |

|

Increase in custodian fees payable |

15,946 | |

|

Increase in transfer agent fees payable |

1,415 | |

|

Decrease in trustees’ fees and expenses payable |

(5,454) | |

|

Increase in other liabilities payable |

1,936 | |

|

Cash provided by operating activities |

$14,650,013 | |

| Cash flows from financing activities: | ||

|

Distributions to Common Shareholders from investment operations |

(28,682,932) | |

|

Repayment of borrowing |

(68,000,000) | |

|

Proceeds from borrowing |

82,000,000 | |

|

Cash used in financing activities |

(14,682,932) | |

|

Decrease in cash |

(32,919) | |

|

Cash at beginning of period |

66,399 | |

|

Cash at end of period |

$33,480 | |

| Supplemental disclosure of cash flow information: | ||

|

Cash paid during the period for interest and fees |

$4,331,026 |

| Six

Months Ended 11/30/2023 (Unaudited) |

Year Ended | Period Ended 5/31/2021 (a) | ||||||

| 5/31/2023 | 5/31/2022 | |||||||

|

Net asset value, beginning of period |

$ 15.40 | $ 17.48 | $ 21.13 | $ 20.00 | ||||

| Income from investment operations: | ||||||||

|

Net investment income (loss) |

0.44 (b) | 0.92 | 1.16 | 1.08 | ||||

|

Net realized and unrealized gain (loss) |

0.53 | (1.46) | (3.14) | 1.12 | ||||

|

Total from investment operations |

0.97 | (0.54) | (1.98) | 2.20 | ||||

| Distributions paid to shareholders from: | ||||||||

|

Net investment income |

(0.78) | (0.97) | (1.29) | (1.07) | ||||

|

Net realized gain |

— | — | (0.38) | — | ||||

|

Return of capital |

— | (0.57) | — | — | ||||

|

Total distributions paid to Common Shareholders |

(0.78) | (1.54) | (1.67) | (1.07) | ||||

|

Net asset value, end of period |

$ | $15.40 | $17.48 | $21.13 | ||||

|

Market value, end of period |

$ | $13.52 | $16.07 | $19.86 | ||||

|

Total return based on net asset value (c) |

7.22% | (1.86)% | (9.73)% | 11.49% | ||||

|

Total return based on market value (c) |

6.39% | (6.27)% | (11.70)% | 4.79% | ||||

| Ratios to average net assets/supplemental data: | ||||||||

|

Net assets, end of period (in 000’s) |

$ 573,357 | $ 566,399 | $ 642,783 | $ 776,142 | ||||

|

Ratio of total expenses to average net assets |

3.42% (d) | 3.05% | 2.41% | 2.28% (d) | ||||

|

Ratio of total expenses to average net assets excluding interest expense |

1.82% (d) | 1.86% | 2.02% | 1.93% (d) | ||||

|

Ratio of net investment income (loss) to average net assets |

5.74% (d) | 5.75% | 5.81% | 5.62% (d) | ||||

|

Portfolio turnover rate |

21% | 35% | 39% | 54% | ||||

| Indebtedness: | ||||||||

|

Total loan outstanding (in 000’s) |

$ 137,000 | $ 123,000 | $ 278,000 | $ 309,000 | ||||

|

Asset coverage per $1,000 of indebtedness (e) |

$ 5,185 | $ 5,605 | $ 3,312 | $ 3,512 | ||||

| (a) | The Fund was seeded on May 21, 2020 and commenced operations on June 25, 2020. |

| (b) | Based on average shares outstanding. |

| (c) | Total return is based on the combination of reinvested dividend, capital gain and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan, and changes in net asset value per share for net asset value returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of future results. |

| (d) | Annualized. |

| (e) | Calculated by subtracting the Fund’s total liabilities (not including the loan outstanding) from the Fund’s total assets, and dividing by the outstanding loan balance in 000’s. |

| 1) | the most recent price provided by a pricing service; |

| (1) | The terms “security” and “securities” used throughout the Notes to Financial Statements include Senior Loans. |

| 2) | available market prices for the fixed-income security; |

| 3) | the fundamental business data relating to the borrower/issuer; |

| 4) | an evaluation of the forces which influence the market in which these securities are purchased and sold; |

| 5) | the type, size and cost of the security; |

| 6) | the financial statements of the borrower/issuer, or the financial condition of the country of issue; |

| 7) | the credit quality and cash flow of the borrower/issuer, or country of issue, based on the Pricing Committee’s, sub-advisor’s or portfolio manager’s analysis, as applicable, or external analysis; |

| 8) | the information as to any transactions in or offers for the security; |

| 9) | the price and extent of public trading in similar securities (or equity securities) of the borrower/issuer, or comparable companies; |

| 10) | the coupon payments; |

| 11) | the quality, value and salability of collateral, if any, securing the security; |

| 12) | the business prospects of the borrower/issuer, including any ability to obtain money or resources from a parent or affiliate and an assessment of the borrower’s/issuer’s management; |

| 13) | the prospects for the borrower’s/issuer’s industry, and multiples (of earnings and/or cash flows) being paid for similar businesses in that industry; |

| 14) | the borrower’s competitive position within the industry; |

| 15) | the borrower’s ability to access additional liquidity through public and/or private markets; and |

| 16) | other relevant factors. |

| 1) | benchmark yields; |

| 2) | reported trades; |

| 3) | broker/dealer quotes; |

| 4) | issuer spreads; |

| 5) | benchmark securities; |

| 6) | bids and offers; and |

| 7) | reference data including market research publications. |

| 1) | the last sale price on the exchange on which they are principally traded or, for Nasdaq and AIM securities, the official closing price; |

| 2) | the type of security; |

| 3) | the size of the holding; |

| 4) | the initial cost of the security; |

| 5) | transactions in comparable securities; |

| 6) | price quotes from dealers and/or third-party pricing services; |

| 7) | relationships among various securities; |

| 8) | information obtained by contacting the issuer, analysts, or the appropriate stock exchange; |

| 9) | an analysis of the issuer’s financial statements; |

| 10) | the existence of merger proposals or tender offers that might affect the value of the security; and |

| 11) | other relevant factors. |

| • | Level 1 – Level 1 inputs are quoted prices in active markets for identical investments. An active market is a market in which transactions for the investment occur with sufficient frequency and volume to provide pricing information on an ongoing basis. |

| • | Level 2 – Level 2 inputs are observable inputs, either directly or indirectly, and include the following: |

| o | Quoted prices for similar investments in active markets. |

| o | Quoted prices for identical or similar investments in markets that are non-active. A non-active market is a market where there are few transactions for the investment, the prices are not current, or price quotations vary substantially either over time or among market makers, or in which little information is released publicly. |

| o | Inputs other than quoted prices that are observable for the investment (for example, interest rates and yield curves observable at commonly quoted intervals, volatilities, prepayment speeds, loss severities, credit risks, and default rates). |

| o | Inputs that are derived principally from or corroborated by observable market data by correlation or other means. |

| • | Level 3 – Level 3 inputs are unobservable inputs. Unobservable inputs may reflect the reporting entity’s own assumptions about the assumptions that market participants would use in pricing the investment. |

| Security | Acquisition Date |

Shares | Current Price | Carrying Cost |

Value | %

of Net Assets |

| Akorn, Inc. | 10/15/2020 | 220,989 | $1.13 | $2,534,056 | $248,613 | 0.04% |

| Distributions paid from: | |

|

Ordinary income |

$35,642,807 |

|

Capital gains |

— |

|

Return of capital |

21,134,688 |

|

Undistributed ordinary income |

$— |

|

Undistributed capital gains |

— |

|

Total undistributed earnings |

— |

|

Accumulated capital and other losses |

(69,905,200) |

|

Net unrealized appreciation (depreciation) |

(77,977,005) |

|

Total accumulated earnings (losses) |

(147,882,205) |

|

Other |

— |

|

Paid-in capital |

714,281,174 |

|

Total net assets |

$566,398,969 |

| Tax Cost | Gross Unrealized Appreciation |

Gross Unrealized (Depreciation) |

Net

Unrealized Appreciation (Depreciation) | |||

| $746,161,795 | $4,566,380 | $(46,285,134) | $(41,718,754) |

| Statement of Operations Location | |

| Credit Risk Exposure | |

| Net realized gain (loss) on swap contracts | $(147,114) |

| (1) | If Common Shares are trading at or above net asset value (“NAV”) at the time of valuation, the Fund will issue new shares at a price equal to the greater of (i) NAV per Common Share on that date or (ii) 95% of the market price on that date. |

| (2) | If Common Shares are trading below NAV at the time of valuation, the Plan Agent will receive the dividend or distribution in cash and will purchase Common Shares in the open market, on the NYSE or elsewhere, for the participants’ accounts. It is possible that the market price for the Common Shares may increase before the Plan Agent has completed its purchases. Therefore, the average purchase price per share paid by the Plan Agent may exceed the market price at the time of valuation, resulting in the purchase of fewer shares than if the dividend or distribution had been paid in Common Shares issued by the Fund. The Plan Agent will use all dividends and distributions received in cash to purchase Common Shares in the open market within 30 days of the valuation date except where temporary curtailment or suspension of purchases is necessary to comply with federal securities laws. Interest will not be paid on any uninvested cash payments. |

| NOT FDIC INSURED | NOT BANK GUARANTEED | MAY LOSE VALUE |

(b) Not applicable.

Item 2. Code of Ethics.

Not applicable.

Item 3. Audit Committee Financial Expert.

Not applicable.

Item 4. Principal Accountant Fees and Services.

Not applicable.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

| (a) | Schedule of Investments in securities of unaffiliated issuers as of the close of the reporting period is included as part of the report to shareholders filed under Item 1 of this form. |

| (b) | Not applicable. |

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

(a) Not applicable.

| (b) | There have been no changes, as of the date of filing, in any of the Portfolio Managers identified in response to paragraph (a)(1) of this item in the registrant’s most recent annual report on Form N-CSR. |

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

There have been no material changes to the procedures by which the shareholders may recommend nominees to the registrant’s board of directors, where those changes were implemented after the registrant last provided disclosure in response to the requirements of Item 407(c)(2)(iv) of Regulation S-K (17 CFR 229.407) (as required by Item 22(b)(15) of Schedule 14A (17 CFR 240.14a-101)), or this Item.

Item 11. Controls and Procedures.

| (a) | The registrant’s principal executive and principal financial officers, or persons performing similar functions, have concluded that the registrant’s disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30a-3(c))) are effective, as of a date within 90 days of the filing date of the report that includes the disclosure required by this paragraph, based on their evaluation of these controls and procedures required by Rule 30a-3(b) under the 1940 Act (17 CFR 270.30a-3(b)) and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934, as amended (17 CFR 240.13a-15(b) or 240.15d-15(b)). |

| (b) | There were no changes in the registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act (17 CFR 270.30a-3(d)) that occurred during the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting. |

Item 12. Disclosure of Securities Lending Activities for Closed-End Management Investment Companies.

| (a) | Not applicable. |

| (b) | Not applicable. |

Item 13. Exhibits.

| (a)(1) | Not applicable. |

| (a)(2) | Certifications pursuant to Rule 30a-2(a) under the 1940 Act and Section 302 of the Sarbanes-Oxley Act of 2002 are attached hereto. |

| (a)(3) | Not applicable. |

| (a)(4) | Not applicable. |

| (b) | Certifications pursuant to Rule 30a-2(b) under the 1940 Act and Section 906 of the Sarbanes-Oxley Act of 2002 are attached hereto. |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| (Registrant) | First Trust High Yield Opportunities 2027 Target Term Fund |

| By (Signature and Title)* | /s/ James M. Dykas | |

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

| Date: | February 5, 2024 |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By (Signature and Title)* | /s/ James M. Dykas | |

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

| Date: | February 5, 2024 |

| By (Signature and Title)* | /s/ Derek D. Maltbie | |

| Derek D. Maltbie, Treasurer, Chief Financial Officer and Chief Accounting Officer (principal financial officer) |

| Date: | February 5, 2024 |

* Print the name and title of each signing officer under his or her signature.

Certification Pursuant to Rule 30a-2(a) under

the 1940 Act and Section 302

of the Sarbanes-Oxley Act

I, James M. Dykas, certify that:

| 1. | I have reviewed this report on Form N-CSR of First Trust High Yield Opportunities 2027 Target Term Fund; |

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations, changes in net assets, and cash flows (if the financial statements are required to include a statement of cash flows) of the registrant as of, and for, the periods presented in this report; |

| 4. | The registrant's other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940) and internal control over financial reporting (as defined in Rule 30a-3(d) under the Investment Company Act of 1940) for the registrant and have: |

| (a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

| (b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

| (c) | Evaluated the effectiveness of the registrant's disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of a date within 90 days prior to the filing date of this report based on such evaluation; and |

| (d) | Disclosed in this report any change in the registrant's internal control over financial reporting that occurred during the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant's internal control over financial reporting; and |

| 5. | The registrant's other certifying officer(s) and I have disclosed to the registrant's auditors and the audit committee of the registrant's board of directors (or persons performing the equivalent functions): |

| (a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant's ability to record, process, summarize, and report financial information; and |

| (b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant's internal control over financial reporting. |

| Date: | February 5, 2024 | /s/ James M. Dykas | |||

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

Certification Pursuant to Rule 30a-2(a) under

the 1940 Act and Section 302

of the Sarbanes-Oxley Act

I, Derek D. Maltbie, certify that:

| 1. | I have reviewed this report on Form N-CSR of First Trust High Yield Opportunities 2027 Target Term Fund; |

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations, changes in net assets, and cash flows (if the financial statements are required to include a statement of cash flows) of the registrant as of, and for, the periods presented in this report; |

| 4. | The registrant's other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940) and internal control over financial reporting (as defined in Rule 30a-3(d) under the Investment Company Act of 1940) for the registrant and have: |

| (a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

| (b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

| (c) | Evaluated the effectiveness of the registrant's disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of a date within 90 days prior to the filing date of this report based on such evaluation; and |

| (d) | Disclosed in this report any change in the registrant's internal control over financial reporting that occurred during the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant's internal control over financial reporting; and |

| 5. | The registrant's other certifying officer(s) and I have disclosed to the registrant's auditors and the audit committee of the registrant's board of directors (or persons performing the equivalent functions): |

| (a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant's ability to record, process, summarize, and report financial information; and |

| (b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant's internal control over financial reporting. |

| Date: | February 5, 2024 | /s/ Derek D. Maltbie | |||

| Derek D. Maltbie, Treasurer, Chief Financial Officer and Chief Accounting Officer (principal financial officer) |

Certification Pursuant to Rule 30a-2(b) under the

1940 Act and Section 906

of the Sarbanes-Oxley Act

I, James M. Dykas, President and Chief Executive Officer of First Trust High Yield Opportunities 2027 Target Term Fund (the “Registrant”), certify that:

| 1. | The Form N-CSR of the Registrant (the “Report”) fully complies with the requirements of Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended; and |

| 2. | The information contained in the Report fairly presents, in all material respects, the financial condition and results of operations of the Registrant. |

| Date: | February 5, 2024 | /s/ James M. Dykas | |||

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

I, Derek D. Maltbie, Treasurer, Chief Financial Officer and Chief Accounting Officer of First Trust High Yield Opportunities 2027 Target Term Fund (the “Registrant”), certify that:

| 1. | The Form N-CSR of the Registrant (the “Report”) fully complies with the requirements of Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended; and |

| 2. | The information contained in the Report fairly presents, in all material respects, the financial condition and results of operations of the Registrant. |

| Date: | February 5, 2024 | /s/ Derek D. Maltbie | |||

| Derek D. Maltbie, Treasurer, Chief Financial Officer and Chief Accounting Officer (principal financial officer) |

N-2 |

6 Months Ended |

|---|---|

|

Nov. 30, 2023

$ / shares

shares

| |

| Cover [Abstract] | |

| Entity Central Index Key | 0001810523 |

| Amendment Flag | false |

| Entity Inv Company Type | N-2 |

| Document Type | N-CSRS |

| Entity Registrant Name | First Trust High Yield Opportunities 2027 Term Fund |

| General Description of Registrant [Abstract] | |

| Investment Objectives and Practices [Text Block] | The investment objective of the Fund is to provide current income. Under normal market conditions, the Fund will seek to achieve its investment objective by investing at least 80% of its Managed Assets in high yield debt securities of any maturity that are rated below investment grade at the time of purchase or unrated securities determined by the Advisor (as defined below) to be of comparable quality. “Managed Assets” means the total asset value of the Fund minus the sum of its liabilities, other than the principal amount of borrowings. High yield debt securities include U.S. and non-U.S. corporate debt obligations and senior secured floating rate loans (“Senior Loans”) |

| Risk Factors [Table Text Block] | Principal

Risks

The

Fund is a closed-end management investment company designed primarily as a long-term investment and not as a trading vehicle. The Fund

is not intended to be a complete investment program and, due to the uncertainty inherent in all investments, there can be no assurance

that the Fund will achieve its investment objective. The following discussion summarizes the principal risks associated with investing

in the Fund, which includes the risk that you could lose some or all of your investment in the Fund. The Fund is subject to the informational

requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940 and, in accordance therewith, files reports,

proxy statements and other information that is available for review.

CDX

Risk. CDX is an equally-weighted index of credit default swaps that is designed to track a representative

segment of the credit default swap market (e.g., high yield). A credit default swap is a financial derivative that allows an investor

to swap or offset their credit risk with that of another investor. CDX provides exposure to a basket of underlying credit default swaps

in lieu of buying or selling credit default swaps on individual debt securities. The CDX investments in which the Fund will invest are

cleared on an exchange. Regardless of whether the Fund buys or sells CDX credit protection, such investments can result in gains or losses

that may exceed gains or losses the Fund would have incurred investing directly in high yield debt securities, which may impact the Fund’s

net asset value. It is also possible that returns from CDX investments may not correlate with returns of the broader high yield credit

market. There are additional costs associated with investing in CDX, including the payment of premiums when the Fund is a buyer of CDX

credit protection. When the Fund sells CDX credit protection, it assumes additional credit risk. Investment exposure to CDX credit protection

is subject to the risks of the underlying credit default swap obligations, which include general market risk, liquidity risk, credit risk

and counterparty risk. Counterparty risk may be mitigated somewhat compared to buying or selling credit protection using individual credit

default swaps because CDX investments are cleared on an exchange.

Consumer

Discretionary Companies Risk. Consumer discretionary companies, such as retailers, media companies and

consumer services companies, provide non-essential goods and services. These companies manufacture products and provide discretionary

services directly to the consumer, and the success of these companies is tied closely to the performance of the overall domestic and international

economy, interest rates, competition and consumer confidence. Success depends heavily on disposable household income and consumer spending.

Changes in demographics and consumer tastes can also affect the demand for, and success of, consumer discretionary products in the marketplace.

Corporate

Debt Obligations Risk. The market value of corporate debt obligations generally may be expected to rise

and fall inversely with interest rates. The market value of corporate debt obligations also may be affected by factors directly related

to the issuer, such as investors’ perceptions of the creditworthiness of the issuer, the issuer’s financial performance, perceptions

of the issuer in the marketplace, performance of management of the issuer, the issuer’s capital structure and use of financial leverage

and demand for the issuer’s

goods and services. There is a risk that the issuers of corporate debt may not be able to meet their obligations on interest and/or principal

payments at the time called for by an instrument.

Credit

Agency Risk. Credit ratings are determined by credit rating agencies and are only the opinions of such

entities. Ratings assigned by a rating agency are not absolute standards of credit quality and do not evaluate market risk or the liquidity

of securities. Any shortcomings or inefficiencies in credit rating agencies’ processes for determining credit ratings may adversely

affect the credit ratings of securities held by the Fund or such credit rating agency’s ability to evaluate creditworthiness and,

as a result, may adversely affect those securities’ perceived or actual credit risk.

Credit

and Below-Investment Grade Securities Risk. Credit risk is the risk that the issuer or other obligated

party of a debt security in the Fund’s portfolio will fail to pay, or it is perceived that it will fail to pay, dividends and/or

interest or repay principal, when due. Below-investment grade instruments, including instruments that are not rated but judged to be of

comparable quality, are commonly referred to as high yield securities or “junk” bonds and are considered speculative with

respect to the issuer’s capacity to pay dividends or interest and repay principal and are more susceptible to default or decline

in market value than investment grade securities due to adverse economic and business developments. High yield securities are often unsecured

and subordinated to other creditors of the issuer. The market values for high yield securities tend to be very volatile, and these securities

are generally less liquid than investment grade securities. For these reasons, an investment in the Fund is subject to the following specific