We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Share Name | Share Symbol | Market | Type |

|---|---|---|---|

| First Trust Energy Infrastructure Fund | NYSE:FIF | NYSE | Common Stock |

| Price Change | % Change | Share Price | High Price | Low Price | Open Price | Shares Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|

| 0.00 | 0.00% | 18.10 | 0 | 01:00:00 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22528

(Exact name of registrant as specified in charter)

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(Address of principal executive offices) (Zip code)

W. Scott Jardine, Esq.

First Trust Portfolios L.P.

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(Name and address of agent for service)

Registrant’s telephone number, including area code: 630-765-8000

Date of fiscal year end: November 30

Date of reporting period: May 31, 2023

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| (a) | The Report to Shareholders is attached herewith. |

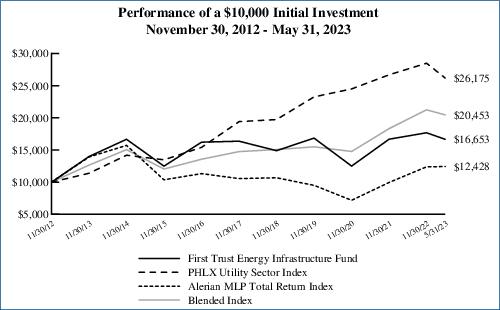

| Performance | |||||

| Average Annual Total Returns | |||||

| 6

Months Ended 5/31/23 |

1

Year Ended 5/31/23 |

5

Years Ended 5/31/23 |

10

Years Ended 5/31/23 |

Inception (9/27/11) to 5/31/23 | |

| Fund Performance(3) | |||||

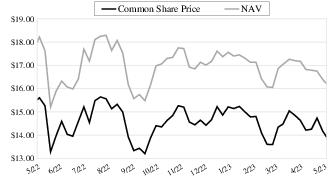

| NAV | -6.68% | -4.60% | 6.60% | 4.86% | 7.41% |

| Market Value | -5.77% | -5.04% | 3.75% | 3.62% | 5.60% |

| Index Performance | |||||

| PHLX Utility Sector Index | -8.10% | -10.44% | 8.63% | 9.23% | 9.21% |

| Alerian MLP Total Return Index | 0.39% | 7.84% | 4.97% | 0.80% | 3.70% |

| Blended Index(4) | -3.69% | -1.03% | 8.79% | 6.24% | 7.60% |

| (1) | Most recent distribution paid through May 31, 2023. Subject to change in the future. |

| (2) | Distribution rates are calculated by annualizing the most recent distribution paid through the report date and then dividing by Common Share Price or NAV, as applicable, as of May 31, 2023. Subject to change in the future. |

| (3) | Total return is based on the combination of reinvested dividend, capital gain, and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan and changes in NAV per share for NAV returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of future results. |

| (4) | The Blended Index consists of the following: PHLX Utility Sector Index (50%) and Alerian MLP Total Return Index (50%). The Blended Index reflects the diverse allocation of companies engaged in the energy infrastructure sector in the Fund’s portfolio. The indices do not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown. Indexes are unmanaged and an investor cannot invest directly in an index. The Blended Index returns are calculated by using the monthly return of the two indices during each period shown above. At the beginning of each month the two indices are rebalanced to a 50-50 ratio to account for divergence from that ratio that occurred during the course of each month. The monthly returns are then compounded for each period shown above, giving the performance for the Blended Index for each period shown above. |

| (5) | Includes swap contracts. |

| Average Annual Total Returns | |||||

| 6

Months Ended 5/31/23 |

1

Year Ended 5/31/23 |

5

Years Ended 5/31/23 |

10

Years Ended 5/31/23 |

Inception (9/27/11) to 5/31/23 | |

| Fund Performance(1) | |||||

| NAV | -6.68% | -4.60% | 6.60% | 4.86% | 7.41% |

| Market Value | -5.77% | -5.04% | 3.75% | 3.62% | 5.60% |

| Index Performance | |||||

| PHLX Utility Sector Index | -8.10% | -10.44% | 8.63% | 9.23% | 9.21% |

| Alerian MLP Total Return Index | 0.39% | 7.84% | 4.97% | 0.80% | 3.70% |

| Blended Index(2) | -3.69% | -1.03% | 8.79% | 6.24% | 7.60% |

| (1) | Total return is based on the combination of reinvested dividend, capital gain and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan and changes in NAV per share for NAV returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of future results. |

| (2) | The Blended Index consists of the following: PHLX Utility Sector Index (50%) and Alerian MLP Total Return Index (50%). The Blended Index reflects the diverse allocation of companies engaged in the energy infrastructure sector in the Fund’s portfolio. The indexes do not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown. Indexes are unmanaged and an investor cannot invest directly in an index. The Blended Index returns are calculated by using the monthly return of the two indices during each period shown above. At the beginning of each month the two indices are rebalanced to a 50-50 ratio to account for divergence from that ratio that occurred during the course of each month. The monthly returns are then compounded for each period shown above, giving the performance for the Blended Index for each period shown above. |

| (3) | Source: FactSet, Bloomberg. |

| (4) | Source: BP Statistical Review of World Energy – June 2022. |

| (5) | Source: World Bank, EIP Estimates. |

| (6) | There is no guarantee that any investment strategy will successfully protect against inflation or will even be profitable. |

| Shares | Description | Value | ||

| COMMON STOCKS (a) – 69.6% | ||||

| Construction & Engineering – 0.1% | ||||

| 1,890 |

Quanta Services, Inc. |

$335,626 | ||

| Electric Utilities – 12.3% | ||||

| 104,690 |

Alliant Energy Corp. (b) |

5,387,347 | ||

| 87,400 |

American Electric Power Co., Inc. |

7,264,688 | ||

| 8,110 |

Duke Energy Corp. |

724,142 | ||

| 18,930 |

Emera, Inc. (CAD) |

780,488 | ||

| 79,420 |

Enel S.p.A., ADR |

494,787 | ||

| 8,000 |

Entergy Corp. |

785,600 | ||

| 26,240 |

Evergy, Inc. |

1,517,984 | ||

| 25,130 |

Eversource Energy |

1,739,750 | ||

| 62,300 |

Exelon Corp. |

2,470,195 | ||

| 18,450 |

Fortis, Inc. (CAD) |

776,055 | ||

| 7,230 |

IDACORP, Inc. |

752,426 | ||

| 40,913 |

NextEra Energy, Inc. |

3,005,469 | ||

| 11,600 |

Orsted A/S, ADR |

339,532 | ||

| 112,890 |

PPL Corp. |

2,957,718 | ||

| 35,650 |

Xcel Energy, Inc. |

2,327,588 | ||

| 31,323,769 | ||||

| Energy Equipment & Services – 0.3% | ||||

| 80,600 |

Archrock, Inc. |

725,400 | ||

| Gas Utilities – 5.2% | ||||

| 18,700 |

AltaGas Ltd. (CAD) |

317,108 | ||

| 27,900 |

Atmos Energy Corp. |

3,216,312 | ||

| 136,200 |

National Fuel Gas Co. |

6,933,942 | ||

| 14,800 |

New Jersey Resources Corp. |

717,060 | ||

| 19,720 |

ONE Gas, Inc. |

1,596,137 | ||

| 13,894 |

UGI Corp. |

388,615 | ||

| 13,169,174 | ||||

| Independent Power & Renewable Electricity Producers – 2.1% | ||||

| 167,170 |

AES (The) Corp. (b) |

3,299,936 | ||

| 51,970 |

Clearway Energy, Inc., Class A |

1,428,136 | ||

| 14,170 |

EDP Renovaveis S.A. (EUR) |

281,418 | ||

| 18,940 |

Northland Power, Inc. (CAD) |

415,494 | ||

| 5,424,984 | ||||

| Multi-Utilities – 12.3% | ||||

| 147,910 |

Atco Ltd., Class I (CAD) |

4,546,802 | ||

| 17,020 |

Canadian Utilities Ltd., Class A (CAD) |

457,001 | ||

| 10,619 |

CenterPoint Energy, Inc. |

299,562 | ||

| 25,600 |

CMS Energy Corp. |

1,484,288 | ||

| 28,810 |

DTE Energy Co. |

3,099,956 | ||

| 89,000 |

Public Service Enterprise Group, Inc. |

5,317,750 | ||

| 95,320 |

Sempra Energy |

13,681,280 | ||

| 26,320 |

WEC Energy Group, Inc. |

2,299,052 | ||

| 31,185,691 | ||||

| Oil, Gas & Consumable Fuels – 37.0% | ||||

| 165,090 |

BP PLC, ADR |

5,565,184 | ||

| 45,178 |

Cheniere Energy, Inc. |

6,314,529 | ||

| 318,590 |

DT Midstream, Inc. |

14,483,101 | ||

| 123,800 |

Enbridge, Inc. |

4,357,760 | ||

| 361,830 |

Keyera Corp. (CAD) |

8,076,206 | ||

| 904,565 |

Kinder Morgan, Inc. (b) |

14,572,542 | ||

| Shares | Description | Value | ||

| COMMON STOCKS (a) (Continued) | ||||

| Oil, Gas & Consumable Fuels (Continued) | ||||

| 176,123 |

ONEOK, Inc. (b) |

$9,979,129 | ||

| 109,230 |

Shell PLC, ADR (b) |

6,116,880 | ||

| 103,070 |

Targa Resources Corp. (b) |

7,013,914 | ||

| 20,455 |

TC Energy Corp. |

796,518 | ||

| 106,730 |

TotalEnergies SE, ADR |

6,008,899 | ||

| 374,750 |

Williams (The) Cos., Inc. (b) |

10,740,335 | ||

| 94,024,997 | ||||

| Semiconductors & Semiconductor Equipment – 0.2% | ||||

| 2,040 |

Enphase Energy, Inc. (c) |

354,715 | ||

| Water Utilities – 0.1% | ||||

| 2,170 |

American Water Works Co., Inc. |

313,457 | ||

|

Total Common Stocks |

176,857,813 | |||

| (Cost $185,816,554) | ||||

| Units | Description | Value | ||

| MASTER LIMITED PARTNERSHIPS (a) – 47.4% | ||||

| Chemicals – 0.6% | ||||

| 69,395 |

Westlake Chemical Partners, L.P. |

1,491,298 | ||

| Energy Equipment & Services – 0.1% | ||||

| 14,800 |

USA Compression Partners, L.P. |

276,464 | ||

| Independent Power & Renewable Electricity Producers – 3.2% | ||||

| 135,418 |

NextEra Energy Partners, L.P. (d) |

8,114,247 | ||

| Oil, Gas & Consumable Fuels – 43.5% | ||||

| 99,089 |

Cheniere Energy Partners, L.P. |

4,404,506 | ||

| 1,572,880 |

Energy Transfer, L.P. |

19,503,712 | ||

| 29,780 |

EnLink Midstream, LLC (d) |

290,653 | ||

| 824,240 |

Enterprise Products Partners, L.P. |

20,877,999 | ||

| 432,710 |

Hess Midstream, L.P., Class A (d) |

12,068,282 | ||

| 176,346 |

Holly Energy Partners, L.P. |

3,027,861 | ||

| 359,772 |

Magellan Midstream Partners, L.P. |

21,661,872 | ||

| 240,770 |

MPLX, L.P. |

8,027,272 | ||

| 1,455,078 |

Plains GP Holdings, L.P., Class A (d) |

19,789,061 | ||

| 29,940 |

Western Midstream Partners, L.P. |

755,685 | ||

| 110,406,903 | ||||

|

Total Master Limited Partnerships |

120,288,912 | |||

| (Cost $98,108,517) | ||||

| Shares | Description | Value | ||

| MONEY MARKET FUNDS (a) – 9.2% | ||||

| 23,397,919 |

Morgan Stanley Institutional Liquidity Funds - Treasury Portfolio - Institutional Class - 4.96% (e) |

23,397,919 | ||

| (Cost $23,397,919) | ||||

|

Total Investments – 126.2% |

320,544,644 | |||

| (Cost $307,322,990) | ||||

| Number of Contracts | Description | Notional Amount | Exercise Price | Expiration Date | Value | |||||

| CALL OPTIONS WRITTEN – (0.1)% | ||||||||||

| (1,671) |

AES (The) Corp. (f) |

$(3,298,554) | $26.00 | 06/16/23 | (16,710) | |||||

| (1,046) |

Alliant Energy Corp. (f) |

(5,382,716) | 57.50 | 06/16/23 | (13,598) | |||||

| (1,500) |

Kinder Morgan, Inc. |

(2,416,500) | 17.00 | 07/21/23 | (28,500) | |||||

| Number of Contracts | Description | Notional Amount | Exercise Price | Expiration Date | Value | |||||

| CALL OPTIONS WRITTEN (Continued) | ||||||||||

| (1,761) |

ONEOK, Inc. |

$(9,977,826) | $62.50 | 07/21/23 | $(61,635) | |||||

| (1,092) |

Shell PLC, ADR |

(6,115,200) | 63.00 | 06/16/23 | (5,460) | |||||

| (1,030) |

Targa Resources Corp. (f) |

(7,009,150) | 80.00 | 06/16/23 | (6,180) | |||||

| (1,247) |

Williams (The) Cos., Inc. |

(3,573,902) | 30.00 | 06/16/23 | (9,976) | |||||

|

Total Call Options Written |

(142,059) | |||||||||

| (Premiums received $608,127) | ||||||||||

|

Outstanding Loans – (27.7)% |

(70,300,000) | ||

|

Net Other Assets and Liabilities – 1.6% |

3,800,712 | ||

|

Net Assets – 100.0% |

$253,903,297 |

| Counterparty | Rate Receivable | Expiration Date | Notional Amount |

Rate Payable | Unrealized Appreciation (Depreciation)/ Value | |||||

| Bank of Nova Scotia(1) | (2) | 09/03/24 | $36,475,000 | 2.367%(3) | $1,202,670 | |||||

| N/A(4) (5) | 5.080%(6) | 10/21/25 | 303,796 | 5.090%(7) | (168) | |||||

| $36,778,796 | $1,202,502 | |||||||||

| (1) Payment frequency is monthly | ||||||||||

| (2) 1 month LIBOR until 08/03/23 and then the rate is SOFR + 0.11448%. At 05/31/23, the rate accrued is 5.193%. | ||||||||||

| (3) Fixed Rate | ||||||||||

| (4) Centrally cleared on the Chicago Mercantile Exchange | ||||||||||

| (5) No cash payments are made by either party prior to the expiration dates shown above | ||||||||||

| (6) Federal Funds Rate | ||||||||||

| (7) SOFR + 0.01036% | ||||||||||

| (a) | All of these securities are available to serve as collateral for the outstanding loans. |

| (b) | All or a portion of this security’s position represents cover for outstanding options written. |

| (c) | Non-income producing security. |

| (d) | This security is taxed as a “C” corporation for federal income tax purposes. |

| (e) | Rate shown reflects yield as of May 31, 2023. |

| (f) | This investment is fair valued by the Advisor’s Pricing Committee in accordance with procedures approved by the Fund’s Board of Trustees, and in accordance with the provisions of the Investment Company Act of 1940 and rules thereunder, as amended. At May 31, 2023, investments noted as such are valued at $(36,488) or (0.0)% of net assets. |

| ADR | American Depositary Receipt |

| CAD | Canadian Dollar |

| EUR | Euro |

| LIBOR | London Interbank Offered Rate |

| SOFR | Secured Overnight Financing Rate |

| ASSETS TABLE | ||||

| Total Value at 5/31/2023 |

Level

1 Quoted Prices |

Level

2 Significant Observable Inputs |

Level

3 Significant Unobservable Inputs | |

|

Common Stocks* |

$ 176,857,813 | $ 176,857,813 | $ — | $ — |

|

Master Limited Partnerships* |

120,288,912 | 120,288,912 | — | — |

|

Money Market Funds |

23,397,919 | 23,397,919 | — | — |

|

Total Investments |

320,544,644 | 320,544,644 | — | — |

|

Interest Rate Swap Agreements |

1,202,670 | — | 1,202,670 | — |

|

Total |

$ 321,747,314 | $ 320,544,644 | $ 1,202,670 | $— |

| LIABILITIES TABLE | ||||

| Total Value at 5/31/2023 |

Level

1 Quoted Prices |

Level

2 Significant Observable Inputs |

Level

3 Significant Unobservable Inputs | |

|

Call Options Written |

$ (142,059) | $ (105,571) | $ (36,488) | $ — |

|

Interest Rate Swap Agreements |

(168) | — | (168) | — |

|

Total |

$ (142,227) | $ (105,571) | $ (36,656) | $— |

| * | See Portfolio of Investments for industry breakout. |

| ASSETS: | |

|

Investments, at value (Cost $307,322,990) |

$ 320,544,644 |

|

Cash segregated as collateral for open swap contracts |

1,458,874 |

|

Swap contracts, at value |

1,202,670 |

| Receivables: | |

|

Investment securities sold |

2,428,329 |

|

Dividends |

484,933 |

|

Interest |

81,015 |

|

Dividend reclaims |

9,449 |

|

Prepaid expenses |

17,217 |

|

Total Assets |

326,227,131 |

| LIABILITIES: | |

|

Outstanding loans |

70,300,000 |

|

Options written, at value (Premiums received $608,127) |

142,059 |

|

Due to custodian |

21,525 |

|

Swap contracts, at value |

168 |

|

Due to custodian foreign currency (Proceeds $2) |

2 |

| Payables: | |

|

Investment securities purchased |

1,244,848 |

|

Investment advisory fees |

281,503 |

|

Interest and fees on loans |

253,538 |

|

Audit and tax fees |

29,925 |

|

Administrative fees |

15,757 |

|

Shareholder reporting fees |

12,817 |

|

Trustees’ fees and expenses |

7,666 |

|

Custodian fees |

7,216 |

|

Legal fees |

2,248 |

|

Transfer agent fees |

1,505 |

|

Financial reporting fees |

758 |

|

Other liabilities |

2,299 |

|

Total Liabilities |

72,323,834 |

|

NET ASSETS |

$253,903,297 |

| NET ASSETS consist of: | |

|

Paid-in capital |

$ 229,909,801 |

|

Par value |

156,660 |

|

Accumulated distributable earnings (loss) |

23,836,836 |

|

NET ASSETS |

$253,903,297 |

|

NET ASSET VALUE, per Common Share (par value $0.01 per Common Share) |

$16.21 |

|

Number of |

| INVESTMENT INCOME: | ||

|

Dividends (net of foreign withholding tax of $156,312) |

$ 3,572,615 | |

|

Interest |

418,623 | |

|

Total investment income |

3,991,238 | |

| EXPENSES: | ||

|

Interest and fees on loans |

1,969,975 | |

|

Investment advisory fees |

1,678,778 | |

|

Administrative fees |

79,745 | |

|

Shareholder reporting fees |

71,049 | |

|

Audit and tax fees |

30,470 | |

|

Legal fees |

30,070 | |

|

Custodian fees |

14,538 | |

|

Listing expense |

10,554 | |

|

Trustees’ fees and expenses |

9,192 | |

|

Transfer agent fees |

9,167 | |

|

Financial reporting fees |

4,612 | |

|

Other |

21,526 | |

|

Total expenses |

3,929,676 | |

|

NET INVESTMENT INCOME (LOSS) |

61,562 | |

| NET REALIZED AND UNREALIZED GAIN (LOSS): | ||

| Net realized gain (loss) on: | ||

|

Investments |

11,905,161 | |

|

Written options contracts |

1,834,472 | |

|

Swap contracts |

390,281 | |

|

Foreign currency transactions |

(24,146) | |

|

Net realized gain (loss) |

14,105,768 | |

| Net change in unrealized appreciation (depreciation) on: | ||

|

Investments |

(34,625,194) | |

|

Written options contracts |

877,800 | |

|

Swap contracts |

(199,583) | |

|

Foreign currency translation |

507 | |

|

Net change in unrealized appreciation (depreciation) |

(33,946,470) | |

|

NET REALIZED AND UNREALIZED GAIN (LOSS) |

(19,840,702) | |

|

NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS |

$(19,779,140) | |

| Six

Months Ended 5/31/2023 (Unaudited) |

Year Ended 11/30/2022 | ||

| OPERATIONS: | |||

|

Net investment income (loss) |

$ 61,562 | $ 965,487 | |

|

Net realized gain (loss) |

14,105,768 | 42,103,089 | |

|

Net change in unrealized appreciation (depreciation) |

(33,946,470) | 20,570,411 | |

|

Net increase (decrease) in net assets resulting from operations |

(19,779,140) | 63,638,987 | |

| DISTRIBUTIONS TO SHAREHOLDERS FROM: | |||

|

Investment operations |

(7,192,130) | (8,831,837) | |

|

Return of capital |

— | (3,385,574) | |

|

Total distributions to shareholders |

(7,192,130) | (12,217,411) | |

| CAPITAL TRANSACTIONS: | |||

|

Repurchase of Common Shares * |

(333,089) | (14,078,800) | |

|

Net increase (decrease) in net assets resulting from capital transactions |

(333,089) | (14,078,800) | |

|

Total increase (decrease) in net assets |

(27,304,359) | 37,342,776 | |

| NET ASSETS: | |||

|

Beginning of period |

281,207,656 | 243,864,880 | |

|

End of period |

$ 253,903,297 | $ 281,207,656 | |

| CAPITAL TRANSACTIONS were as follows: | |||

|

Common Shares at beginning of period |

15,688,201 | 16,664,338 | |

|

Common Shares repurchased * |

(22,162) | (976,137) | |

|

Common Shares at end of period |

15,666,039 | 15,688,201 |

| * | On September 15, 2020, the Fund commenced a share repurchase program. For the six months ended May 31, 2023 and the fiscal year ended November 30, 2022, the Fund repurchased 22,162 and 976,137 Common Shares, respectively, at a weighted-average discount of 13.97% and 13.62%, respectively, from net asset value per share. The Fund’s share repurchase program ended on March 15, 2023. |

| Cash flows from operating activities: | ||

|

Net increase (decrease) in net assets resulting from operations |

$(19,779,140) | |

| Adjustments to reconcile net increase (decrease) in net assets resulting from operations to net cash used in operating activities: | ||

|

Purchases of investments |

(137,588,951) | |

|

Sales, maturities and paydown of investments |

121,949,078 | |

|

Proceeds from written options |

2,476,171 | |

|

Amount paid to close written options |

(124,915) | |

|

Return of capital received from investment in MLPs |

4,820,520 | |

|

Net realized gain/loss on investments and written options |

(13,739,633) | |

|

Net change in unrealized appreciation/depreciation on investments and written options |

33,747,394 | |

|

Net change in unrealized appreciation/depreciation on swap contracts |

199,583 | |

| Changes in assets and liabilities: | ||

|

Increase in interest receivable |

(81,015) | |

|

Increase in dividend reclaims receivable |

(2,836) | |

|

Decrease in dividends receivable |

24,109 | |

|

Increase in prepaid expenses |

(12,224) | |

|

Increase in due to custodian foreign currency |

2 | |

|

Increase in due to custodian |

21,525 | |

|

Increase in interest and fees payable on loans |

96,572 | |

|

Increase in investment advisory fees payable |

923 | |

|

Decrease in audit and tax fees payable |

(30,363) | |

|

Increase in legal fees payable |

82 | |

|

Decrease in shareholder reporting fees payable |

(12,952) | |

|

Increase in administrative fees payable |

497 | |

|

Increase in custodian fees payable |

2,441 | |

|

Decrease in transfer agent fees payable |

(27) | |

|

Increase in trustees’ fees and expenses payable |

4,583 | |

|

Decrease in financial reporting fees payable |

(13) | |

|

Decrease in other liabilities payable |

(286) | |

|

Cash used in operating activities |

$(8,028,875) | |

| Cash flows from financing activities: | ||

|

Repurchase of Common Shares |

(333,089) | |

|

Distributions to Common Shareholders from investment operations |

(7,192,130) | |

|

Cash used in financing activities |

(7,525,219) | |

|

Decrease in cash and cash segregated as collateral for open swap contracts (a) |

(15,554,094) | |

|

Cash and cash segregated as collateral for open swap contracts at beginning of period |

17,012,968 | |

|

Cash and cash segregated as collateral for open swap contracts at end of period |

$1,458,874 | |

| Supplemental disclosure of cash flow information: | ||

|

Cash paid during the period for interest and fees |

$1,873,403 | |

| Cash and cash segregated as collateral for open swap contracts reconciliation: | ||

|

Cash |

$0 | |

|

Cash segregated as collateral for open swap contracts |

1,458,874 | |

|

Cash and cash segregated as collateral for open swap contracts at end of period |

$1,458,874 |

| (a) | Includes net change in unrealized appreciation (depreciation) on foreign currency of $507. |

| Six

Months Ended 5/31/2023 (Unaudited) |

Year Ended November 30, | |||||||||||

| 2022 | 2021 | 2020 | 2019 | 2018 | ||||||||

|

Net asset value, beginning of period |

$ 17.92 | $ 14.63 | $ 12.47 | $ 16.84 | $ 16.79 | $ 18.73 | ||||||

| Income from investment operations: | ||||||||||||

|

Net investment income (loss) |

0.01 | 0.06 | 0.16 | 0.03 | 0.01 | 0.18 | ||||||

|

Net realized and unrealized gain (loss) |

(1.26) | 3.84 | 2.68 | (3.43) | 1.36 | (0.80) | ||||||

|

Total from investment operations |

(1.25) | 3.90 | 2.84 | (3.40) | 1.37 | (0.62) | ||||||

| Distributions paid to shareholders from: | ||||||||||||

|

Net investment income |

(0.46) | (0.17) | (0.18) | (0.46) | (0.25) | (0.63) | ||||||

|

Net realized gain |

— | (0.37) | — | — | (0.05) | — | ||||||

|

Return of capital |

— | (0.21) | (0.57) | (0.53) | (1.02) | (0.69) | ||||||

|

Total distributions paid to Common Shareholders |

(0.46) | (0.75) | (0.75) | (0.99) | (1.32) | (1.32) | ||||||

|

Common Share repurchases |

0.00 (a) | 0.14 | 0.07 | 0.02 | — | — | ||||||

|

Net asset value, end of period |

$ | $17.92 | $14.63 | $12.47 | $16.84 | $16.79 | ||||||

|

Market value, end of period |

$ | $15.24 | $13.23 | $10.52 | $15.45 | $14.86 | ||||||

|

Total return based on net asset value (b) |

(6.68)% | 29.10% | 24.46% | (19.31)% | 9.14% | (2.83)% | ||||||

|

Total return based on market value (b) |

(5.77)% | 21.34% | 33.41% | (25.80)% | 13.13% | (9.00)% | ||||||

| Ratios to average net assets/supplemental data: | ||||||||||||

|

Net assets, end of period (in 000’s) |

$ 253,903 | $ 281,208 | $ 243,865 | $ 216,439 | $ 295,623 | $ 294,617 | ||||||

|

Ratio of total expenses to average net assets |

2.96% (c) | 2.03% | 1.70% | 2.04% | 2.65% | 2.50% | ||||||

|

Ratio of total expenses to average net assets excluding interest expense and fees on loans |

1.48% (c) | 1.45% | 1.45% | 1.52% | 1.55% | 1.54% | ||||||

|

Ratio of net investment income (loss) to average net assets |

0.05% (c) | 0.36% | 0.99% | 0.24% | 0.05% | 1.02% | ||||||

|

Portfolio turnover rate |

29% | 60% | 73% | 80% | 55% | 58% | ||||||

| Indebtedness: | ||||||||||||

|

Total loans outstanding (in 000’s) |

$ 70,300 | $ 70,300 | $ 62,800 | $ 55,300 | $ 107,500 | $ 104,500 | ||||||

|

Asset coverage per $1,000 of indebtedness (d) |

$ 4,612 | $ 5,000 | $ 4,883 | $ 4,914 | $ 3,750 | $ 3,819 | ||||||

| (a) | Amount represents less than $0.01 per share. |

| (b) | Total return is based on the combination of reinvested dividend, capital gain and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan, and changes in net asset value per share for net asset value returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of future results. |

| (c) | Annualized. |

| (d) | Calculated by subtracting the Fund’s total liabilities (not including the loans outstanding) from the Fund’s total assets, and dividing by the outstanding loans balance in 000’s. |

| 1) | the last sale price on the exchange on which they are principally traded or, for Nasdaq and AIM securities, the official closing price; |

| 2) | the type of security; |

| 3) | the size of the holding; |

| 4) | the initial cost of the security; |

| 5) | transactions in comparable securities; |

| 6) | price quotes from dealers and/or third-party pricing services; |

| 7) | relationships among various securities; |

| 8) | information obtained by contacting the issuer, analysts, or the appropriate stock exchange; |

| 9) | an analysis of the issuer’s financial statements; |

| 10) | the existence of merger proposals or tender offers that might affect the value of the security; and |

| 11) | other relevant factors. |

| 1) | the value of similar foreign securities traded on other foreign markets; |

| 2) | ADR trading of similar securities; |

| 3) | closed-end fund or exchange-traded fund trading of similar securities; |

| 4) | foreign currency exchange activity; |

| 5) | the trading prices of financial products that are tied to baskets of foreign securities; |

| 6) | factors relating to the event that precipitated the pricing problem; |

| 7) | whether the event is likely to recur; |

| 8) | whether the effects of the event are isolated or whether they affect entire markets, countries or regions; and |

| 9) | other relevant factors. |

| • | Level 1 – Level 1 inputs are quoted prices in active markets for identical investments. An active market is a market in which transactions for the investment occur with sufficient frequency and volume to provide pricing information on an ongoing basis. |

| • | Level 2 – Level 2 inputs are observable inputs, either directly or indirectly, and include the following: |

| o | Quoted prices for similar investments in active markets. |

| o | Quoted prices for identical or similar investments in markets that are non-active. A non-active market is a market where there are few transactions for the investment, the prices are not current, or price quotations vary substantially either over time or among market makers, or in which little information is released publicly. |

| o | Inputs other than quoted prices that are observable for the investment (for example, interest rates and yield curves observable at commonly quoted intervals, volatilities, prepayment speeds, loss severities, credit risks, and default rates). |

| o | Inputs that are derived principally from or corroborated by observable market data by correlation or other means. |

| • | Level 3 – Level 3 inputs are unobservable inputs. Unobservable inputs may reflect the reporting entity’s own assumptions about the assumptions that market participants would use in pricing the investment. |

| Gross

Amounts not Offset in the Statement of Assets and Liabilities |

|||||||||||

| Gross Amounts of Recognized Assets |

Gross

Amounts Offset in the Statement of Assets and Liabilities |

Net

Amounts of Assets Presented in the Statement of Assets and Liabilities |

Financial Instruments |

Collateral Amounts Received |

Net Amount | ||||||

| Interest

Rate Swap Agreements |

$ 1,202,670 | $ — | $ 1,202,670 | $ — | $ — | $ 1,202,670 | |||||

| Gross

Amounts not Offset in the Statement of Assets and Liabilities |

|||||||||||

| Gross Amounts of Recognized Liabilities |

Gross

Amounts Offset in the Statement of Assets and Liabilities |

Net

Amounts of Liabilities Presented in the Statement of Assets and Liabilities |

Financial Instruments |

Collateral Amounts Pledged |

Net Amount | ||||||

| Interest

Rate Swap Agreements |

$ (168) | $ — | $ (168) | $ — | $ 168 | $ — | |||||

| Distributions paid from: | |

|

Ordinary income |

$8,831,837 |

|

Capital gains |

— |

|

Return of capital |

3,385,574 |

|

Undistributed ordinary income |

$— |

|

Undistributed capital gains |

— |

|

Total undistributed earnings |

— |

|

Accumulated capital and other losses |

— |

|

Net unrealized appreciation (depreciation) |

56,890,204 |

|

Total accumulated earnings (losses) |

56,890,204 |

|

Other |

(6,082,098) |

|

Paid-in capital |

230,399,550 |

|

Total net assets |

$281,207,656 |

| Tax Cost | Gross Unrealized Appreciation |

Gross Unrealized (Depreciation) |

Net

Unrealized Appreciation (Depreciation) | |||

| $306,714,863 | $29,545,099 | $(14,654,875) | $14,890,224 |

| Asset Derivatives | Liability Derivatives | |||||||||

| Derivative Instrument |

Risk Exposure |

Statement

of Assets and Liabilities Location |

Value | Statement

of Assets and Liabilities Location |

Value | |||||

| Written Options | Equity Risk | — | $ — | Options written, at value | $ 142,059 | |||||

| Interest Rate Swap Agreements | Interest Rate Risk | Swap contracts, at value | 1,202,670 | Swap contracts, at value | 168 | |||||

| Statement of Operations Location | |

| Equity Risk Exposure | |

| Net realized gain (loss) on written options contracts | $1,834,472 |

| Net change in unrealized appreciation (depreciation) on written options contracts | 877,800 |

| Interest Rate Risk Exposure | |

| Net realized gain (loss) on swap contracts | $390,281 |

| Net change in unrealized appreciation (depreciation) on swap contracts | (199,583) |

| (1) | If Common Shares are trading at or above net asset value (“NAV”) at the time of valuation, the Fund will issue new shares at a price equal to the greater of (i) NAV per Common Share on that date or (ii) 95% of the market price on that date. |

| (2) | If Common Shares are trading below NAV at the time of valuation, the Plan Agent will receive the dividend or distribution in cash and will purchase Common Shares in the open market, on the NYSE or elsewhere, for the participants’ accounts. It is possible that the market price for the Common Shares may increase before the Plan Agent has completed its purchases. Therefore, the average purchase price per share paid by the Plan Agent may exceed the market price at the time of valuation, resulting in the purchase of fewer shares than if the dividend or distribution had been paid in Common Shares issued by the Fund. The Plan Agent will use all dividends and distributions received in cash to purchase Common Shares in the open market within 30 days of the valuation date except where temporary curtailment or suspension of purchases is necessary to comply with federal securities laws. Interest will not be paid on any uninvested cash payments. |

| (b) | Not applicable. |

Item 2. Code of Ethics.

Not applicable.

Item 3. Audit Committee Financial Expert.

Not applicable.

Item 4. Principal Accountant Fees and Services.

Not applicable.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

| (a) | Schedule of Investments in securities of unaffiliated issuers as of the close of the reporting period is included as part of the report to shareholders filed under Item 1 of this form. |

| (b) | Not applicable. |

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

| (a) | Not applicable. |

| (b) | There have been no changes, as of the date of this filing, in any of the portfolio managers identified in response to paragraph (a)(1) of this Item in the registrant’s most recent annual report on Form N-CSR. |

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

| Period | (a) Total Number of Shares (or Units) Purchased | (b) Average Price Paid per Share (or Unit) | (c) Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | (d) Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs |

| Month #1 (12/01/2022 – 12/31/2022) |

22,162 | 15.03 | 1,884,197 | 4,825 |

| Month #2 (01/01/2023 – 01/31/2023) |

0 | 0 | 0 | 0 |

| Month #3 (02/01/2023 – 02/28/2023) |

0 | 0 | 0 | 0 |

| Month #4 (03/01/2023 – 03/31/2023) |

0 | 0 | 0 | 0 |

| Month #5 (04/01/2023 – 04/30/2023) |

0 | 0 | 0 | 0 |

| Month #6 (05/01/2023 – 05/31/2023) |

0 | 0 | 0 | 0 |

| Total | 22,162 | $15.03 | 1,884,197 |

Item 10. Submission of Matters to a Vote of Security Holders.

There have been no material changes to the procedures by which the shareholders may recommend nominees to the registrant’s board of directors, where those changes were implemented after the registrant last provided disclosure in response to the requirements of Item 407(c)(2)(iv) of Regulation S-K (17 CFR 229.407) (as required by Item 22(b)(15) of Schedule 14A (17 CFR 240.14a-101)), or this Item.

Item 11. Controls and Procedures.

| (a) | The registrant's principal executive and principal financial officers, or persons performing similar functions, have concluded that the registrant's disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940, as amended (the "1940 Act") (17 CFR 270.30a-3(c))) are effective, as of a date within 90 days of the filing date of the report that includes the disclosure required by this paragraph, based on their evaluation of these controls and procedures required by Rule 30a-3(b) under the 1940 Act (17 CFR 270.30a-3(b)) and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934, as amended (17 CFR 240.13a-15(b) or 240.15d-15(b)). |

| (b) | There were no changes in the registrant's internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act (17 CFR 270.30a-3(d)) that occurred during the period covered by this report that have materially affected, or are reasonably likely to materially affect, the registrant's internal control over financial reporting. |

Item 12. Disclosure of Securities Lending Activities for Closed-End Management Investment Companies.

| (a) | Not applicable. |

| (b) | Not applicable. |

Item 13. Exhibits.

| (a)(1) | Not applicable. |

| (a)(2) | Certifications pursuant to Rule 30a-2(a) under the 1940 Act and Section 302 of the Sarbanes-Oxley Act of 2002 are attached hereto. |

| (a)(3) | Not applicable. |

| (a)(4) | Not applicable. |

| (b) | Certifications pursuant to Rule 30a-2(b) under the 1940 Act and Section 906 of the Sarbanes-Oxley Act of 2002 are attached hereto. |

| (c) | Notices to the registrant’s common shareholders in accordance with the order under Section 6(c) of the 1940 Act granting an exemption from Section 19(b) of the 1940 Act and Rule 19a-1 under the 1940 Act. (1) |

| (1) | The Fund received exemptive relief from the Securities and Exchange Commission which permits the Fund to make periodic distributions of long-term capital gains as frequently as monthly each taxable year. The relief is conditioned, in part, on an undertaking by the Fund to make the disclosures to the holders of the Fund’s common shares, in addition to the information required by Section 19(a) of the 1940 Act and Rule 19a-1 thereunder. The Fund is likewise obligated to file with the SEC the information contained in any such notice to shareholders. In that regard, attached as an exhibit to this filing is a copy of such notice made during the period. |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| (registrant) | First Trust Energy Infrastructure Fund |

| By (Signature and Title)* | /s/ James M. Dykas | |

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

| Date: | August 4, 2023 |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By (Signature and Title)* | /s/ James M. Dykas | |

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

| Date: | August 4, 2023 |

| By (Signature and Title)* | /s/ Donald P. Swade | |

| Donald P. Swade, Treasurer, Chief Financial Officer and Chief Accounting Officer (principal financial officer) |

| Date: | August 4, 2023 |

* Print the name and title of each signing officer under his or her signature.

Certification Pursuant to Rule 30a-2(a) under

the 1940 Act and Section 302

of the Sarbanes-Oxley Act

I, James M. Dykas, certify that:

| 1. | I have reviewed this report on Form N-CSR of First Trust Energy Infrastructure Fund; |

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations, changes in net assets, and cash flows (if the financial statements are required to include a statement of cash flows) of the registrant as of, and for, the periods presented in this report; |

| 4. | The registrant’s other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940) and internal control over financial reporting (as defined in Rule 30a-3(d) under the Investment Company Act of 1940) for the registrant and have: |

| (a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

| (b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

| (c) | Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of a date within 90 days prior to the filing date of this report based on such evaluation; and |

| (d) | Disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and |

| 5. | The registrant’s other certifying officer(s) and I have disclosed to the registrant’s auditors and the audit committee of the registrant’s board of directors (or persons performing the equivalent functions): |

| (a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant’s ability to record, process, summarize, and report financial information; and |

| (b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal control over financial reporting. |

| Date: | August 4, 2023 | /s/ James M. Dykas | |||

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

Certification Pursuant to Rule 30a-2(a) under

the 1940 Act and Section 302

of the Sarbanes-Oxley Act

I, Donald P. Swade, certify that:

| 1. | I have reviewed this report on Form N-CSR of First Trust Energy Infrastructure Fund; |

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations, changes in net assets, and cash flows (if the financial statements are required to include a statement of cash flows) of the registrant as of, and for, the periods presented in this report; |

| 4. | The registrant’s other certifying officer(s) and I are responsible for establishing and maintaining disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940) and internal control over financial reporting (as defined in Rule 30a-3(d) under the Investment Company Act of 1940) for the registrant and have: |

| (a) | Designed such disclosure controls and procedures, or caused such disclosure controls and procedures to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; |

| (b) | Designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; |

| (c) | Evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of a date within 90 days prior to the filing date of this report based on such evaluation; and |

| (d) | Disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and |

| 5. | The registrant’s other certifying officer(s) and I have disclosed to the registrant’s auditors and the audit committee of the registrant’s board of directors (or persons performing the equivalent functions): |

| (a) | All significant deficiencies and material weaknesses in the design or operation of internal control over financial reporting which are reasonably likely to adversely affect the registrant’s ability to record, process, summarize, and report financial information; and |

| (b) | Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant’s internal control over financial reporting. |

| Date: | August 4, 2023 | /s/ Donald P. Swade | |||

| Donald P. Swade, Treasurer, Chief Financial Officer and Chief Accounting Officer (principal financial officer) |

Certification Pursuant to Rule 30a-2(b) under the

1940 Act and Section 906

of the Sarbanes-Oxley Act

I, James M. Dykas, President and Chief Executive Officer of First Trust Energy Infrastructure Fund (the “Registrant”), certify that:

| 1. | The Form N-CSR of the Registrant (the “Report”) fully complies with the requirements of Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended; and |

| 2. | The information contained in the Report fairly presents, in all material respects, the financial condition and results of operations of the Registrant. |

| Date: | August 4, 2023 | /s/ James M. Dykas | |||

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

I, Donald P. Swade, Treasurer, Chief Financial Officer and Chief Accounting Officer of First Trust Energy Infrastructure Fund (the “Registrant”), certify that:

| 1. | The Form N-CSR of the Registrant (the “Report”) fully complies with the requirements of Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended; and |

| 2. | The information contained in the Report fairly presents, in all material respects, the financial condition and results of operations of the Registrant. |

| Date: | August 4, 2023 | /s/ Donald P. Swade | |||

| Donald P. Swade, Treasurer, Chief Financial Officer and Chief Accounting Officer (principal financial officer) |

Notice Regarding Your Monthly Distribution

First Trust Energy Infrastructure Fund (FIF)

The closed-end fund listed above (the “Fund”) has declared a distribution payable on December 15, 2022, to shareholders of record as of December 2, 2022, with an ex-dividend date of December 1, 2022. This Notice is meant to provide you information about the sources of your Fund's distributions. You should not draw any conclusions about the Fund’s investment performance from the amount of its distribution or from the terms of its Managed Distribution Plan.

The following tables set forth the estimated amounts of the current distribution and the cumulative distributions paid this fiscal year to date for the Fund from the following sources: net investment income (“NII”); net realized short-term capital gains (“STCG”); net realized long-term capital gains (“LTCG”); and return of capital (“ROC”). These estimates are based upon information as of November 30, 2022, are calculated based on a generally accepted accounting principles (“GAAP”) basis and include the prior fiscal year-end undistributed net investment income. The amounts and sources of distributions are expressed per common share.

| Annualized | 5 Year Avg. | |||||||||||||||||||||||||

| Total | Current Distribution ($) | Current Distribution (%) | Current Dist. Rate | Annual Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Current Distribution | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.06400 | $0.06400 | — | — | — | 100.00% | — | — | — | 4.28% | 6.56% | |||||||||||||

| Cumulative | Cumulative | |||||||||||||||||||||||||

| Total Cumulative | Cumulative Distributions Fiscal YTD ($) | Cumulative Distributions Fiscal YTD (%) | Fiscal YTD Distributions | Fiscal YTD Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Fiscal YTD Distributions (1) | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.06400 | $0.06400 | — | — | — | 100.00% | — | — | — | 0.36% | 29.10% | |||||||||||||

| (1) | Includes the most recent monthly distribution paid on December 15, 2022. |

| (2) | The Fund estimates that it has distributed more than its income and net realized capital gains; therefore, a portion of your distribution may be a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund's investment performance and should not be confused with "yield" or "income." |

| (3) | Based on Net Asset Value (“NAV”) as of November 30, 2022. |

| (4) | Total Returns are through November 30, 2022. |

| (5) | The Fund anticipates that, due to the tax treatment of cash distributions made by Master Limited Partnerships in which the Fund invests, a portion of distributions the Fund makes to Common Shareholders may consist of a tax-deferred return of capital. |

The amounts and sources of distributions reported in this Notice are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Fund's investment experience during the remainder of its fiscal year and may be subject to changes based on tax regulations. The Fund will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for federal income tax purposes. You should not use this Notice as a substitute for your Form 1099-DIV.

_____________________________________

First Trust Advisors L.P. Contact:

Don Swade (630) 765-8661

Notice Regarding Your Monthly Distribution

First Trust Energy Infrastructure Fund (FIF)

The closed-end fund listed above (the “Fund”) has declared a distribution payable on January 17, 2023, to shareholders of record as of January 4, 2023, with an ex-dividend date of January 3, 2023. This Notice is meant to provide you information about the sources of your Fund's distributions. You should not draw any conclusions about the Fund’s investment performance from the amount of its distribution or from the terms of its Managed Distribution Plan.

The following tables set forth the estimated amounts of the current distribution and the cumulative distributions paid this fiscal year to date for the Fund from the following sources: net investment income (“NII”); net realized short-term capital gains (“STCG”); net realized long-term capital gains (“LTCG”); and return of capital (“ROC”). These estimates are based upon information as of December 31, 2022, are calculated based on a generally accepted accounting principles (“GAAP”) basis and include the prior fiscal year-end undistributed net investment income. The amounts and sources of distributions are expressed per common share.

| Annualized | 5 Year Avg. | |||||||||||||||||||||||||

| Total | Current Distribution ($) | Current Distribution (%) | Current Dist. Rate | Annual Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Current Distribution | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.06450 | $0.06450 | — | — | — | 100.00% | — | — | — | 4.55% | 5.33% | |||||||||||||

| Cumulative | Cumulative | |||||||||||||||||||||||||

| Total Cumulative | Cumulative Distributions Fiscal YTD ($) | Cumulative Distributions Fiscal YTD (%) | Fiscal YTD Distributions | Fiscal YTD Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Fiscal YTD Distributions (1) | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.12850 | $0.12850 | — | — | — | 100.00% | — | — | — | 0.76% | -4.71% | |||||||||||||

| (1) | Includes the most recent monthly distribution paid on January 17, 2023. |

| (2) | The Fund estimates that it has distributed more than its income and net realized capital gains; therefore, a portion of your distribution may be a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund's investment performance and should not be confused with "yield" or "income." |

| (3) | Based on Net Asset Value (“NAV”) as of December 31, 2022. |

| (4) | Total Returns are through December 31, 2022. |

| (5) | The Fund anticipates that, due to the tax treatment of cash distributions made by Master Limited Partnerships in which the Fund invests, a portion of distributions the Fund makes to Common Shareholders may consist of a tax-deferred return of capital. |

The amounts and sources of distributions reported in this Notice are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Fund's investment experience during the remainder of its fiscal year and may be subject to changes based on tax regulations. The Fund will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for federal income tax purposes. You should not use this Notice as a substitute for your Form 1099-DIV.

_____________________________________

First Trust Advisors L.P. Contact:

Don Swade (630) 765-8661

Notice Regarding Your Monthly Distribution

First Trust Energy Infrastructure Fund (FIF)

The closed-end fund listed above (the “Fund”) has declared a distribution payable on February 15, 2023, to shareholders of record as of February 2, 2023, with an ex-dividend date of February 1, 2023. This Notice is meant to provide you information about the sources of your Fund's distributions. You should not draw any conclusions about the Fund’s investment performance from the amount of its distribution or from the terms of its Managed Distribution Plan.

The following tables set forth the estimated amounts of the current distribution and the cumulative distributions paid this fiscal year to date for the Fund from the following sources: net investment income (“NII”); net realized short-term capital gains (“STCG”); net realized long-term capital gains (“LTCG”); and return of capital (“ROC”). These estimates are based upon information as of January 31, 2023, are calculated based on a generally accepted accounting principles (“GAAP”) basis and include the prior fiscal year-end undistributed net investment income. The amounts and sources of distributions are expressed per common share.

| Annualized | 5 Year Avg. | |||||||||||||||||||||||||

| Total | Current Distribution ($) | Current Distribution (%) | Current Dist. Rate | Annual Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Current Distribution | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.06500 | $0.06500 | — | — | — | 100.00% | — | — | — | 4.44% | 6.12% | |||||||||||||

| Cumulative | Cumulative | |||||||||||||||||||||||||

| Total Cumulative | Cumulative Distributions Fiscal YTD ($) | Cumulative Distributions Fiscal YTD (%) | Fiscal YTD Distributions | Fiscal YTD Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Fiscal YTD Distributions (1) | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.19350 | $0.19350 | — | — | — | 100.00% | — | — | — | 1.10% | -1.21% | |||||||||||||

| (1) | Includes the most recent monthly distribution paid on February 15, 2023. |

| (2) | The Fund estimates that it has distributed more than its income and net realized capital gains; therefore, a portion of your distribution may be a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund's investment performance and should not be confused with "yield" or "income." |

| (3) | Based on Net Asset Value (“NAV”) as of January 31, 2023. |

| (4) | Total Returns are through January 31, 2023. |

| (5) | The Fund anticipates that, due to the tax treatment of cash distributions made by Master Limited Partnerships in which the Fund invests, a portion of distributions the Fund makes to Common Shareholders may consist of a tax-deferred return of capital. |

The amounts and sources of distributions reported in this Notice are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Fund's investment experience during the remainder of its fiscal year and may be subject to changes based on tax regulations. The Fund will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for federal income tax purposes. You should not use this Notice as a substitute for your Form 1099-DIV.

_____________________________________

First Trust Advisors L.P. Contact:

Don Swade (630) 765-8661

Notice Regarding Your Monthly Distribution

First Trust Energy Infrastructure Fund (FIF)

The closed-end fund listed above (the “Fund”) has declared a distribution payable on March 15, 2023, to shareholders of record as of March 3, 2023, with an ex-dividend date of March 2, 2023. This Notice is meant to provide you information about the sources of your Fund's distributions. You should not draw any conclusions about the Fund’s investment performance from the amount of its distribution or from the terms of its Managed Distribution Plan.

The following tables set forth the estimated amounts of the current distribution and the cumulative distributions paid this fiscal year to date for the Fund from the following sources: net investment income (“NII”); net realized short-term capital gains (“STCG”); net realized long-term capital gains (“LTCG”); and return of capital (“ROC”). These estimates are based upon information as of February 28, 2023, are calculated based on a generally accepted accounting principles (“GAAP”) basis and include the prior fiscal year-end undistributed net investment income. The amounts and sources of distributions are expressed per common share.

| Annualized | 5 Year Avg. | |||||||||||||||||||||||||

| Total | Current Distribution ($) | Current Distribution (%) | Current Dist. Rate | Annual Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Current Distribution | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.06550 | $0.06550 | — | — | — | 100.00% | — | — | — | 4.67% | 7.56% | |||||||||||||

| Cumulative | Cumulative | |||||||||||||||||||||||||

| Total Cumulative | Cumulative Distributions Fiscal YTD ($) | Cumulative Distributions Fiscal YTD (%) | Fiscal YTD Distributions | Fiscal YTD Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Fiscal YTD Distributions (1) | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.25900 | $0.25900 | — | — | — | 100.00% | — | — | — | 1.54% | -4.96% | |||||||||||||

| (1) | Includes the most recent monthly distribution paid on March 15, 2023. |

| (2) | The Fund estimates that it has distributed more than its income and net realized capital gains; therefore, a portion of your distribution may be a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund's investment performance and should not be confused with "yield" or "income." |

| (3) | Based on Net Asset Value (“NAV”) as of February 28, 2023. |

| (4) | Total Returns are through February 28, 2023. |

| (5) | The Fund anticipates that, due to the tax treatment of cash distributions made by Master Limited Partnerships in which the Fund invests, a portion of distributions the Fund makes to Common Shareholders may consist of a tax-deferred return of capital. |

The amounts and sources of distributions reported in this Notice are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Fund's investment experience during the remainder of its fiscal year and may be subject to changes based on tax regulations. The Fund will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for federal income tax purposes. You should not use this Notice as a substitute for your Form 1099-DIV.

_____________________________________

First Trust Advisors L.P. Contact:

Don Swade (630) 765-8661

Notice Regarding Your Monthly Distribution

First Trust Energy Infrastructure Fund (FIF)

The closed-end fund listed above (the “Fund”) has declared a distribution payable on April 17, 2023, to shareholders of record as of April 4, 2023, with an ex-dividend date of April 3, 2023. This Notice is meant to provide you information about the sources of your Fund's distributions. You should not draw any conclusions about the Fund’s investment performance from the amount of its distribution or from the terms of its Managed Distribution Plan.

The following tables set forth the estimated amounts of the current distribution and the cumulative distributions paid this fiscal year to date for the Fund from the following sources: net investment income (“NII”); net realized short-term capital gains (“STCG”); net realized long-term capital gains (“LTCG”); and return of capital (“ROC”). These estimates are based upon information as of March 31, 2023, are calculated based on a generally accepted accounting principles (“GAAP”) basis and include the prior fiscal year-end undistributed net investment income. The amounts and sources of distributions are expressed per common share.

| Annualized | 5 Year Avg. | |||||||||||||||||||||||||

| Total | Current Distribution ($) | Current Distribution (%) | Current Dist. Rate | Annual Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Current Distribution | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.10000 | $0.10000 | — | — | — | 100.00% | — | — | — | 7.12% | 8.50% | |||||||||||||

| Cumulative | Cumulative | |||||||||||||||||||||||||

| Total Cumulative | Cumulative Distributions Fiscal YTD ($) | Cumulative Distributions Fiscal YTD (%) | Fiscal YTD Distributions | Fiscal YTD Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Fiscal YTD Distributions (1) | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.35900 | $0.35900 | — | — | — | 100.00% | — | — | — | 2.13% | -4.28% | |||||||||||||

| (1) | Includes the most recent monthly distribution paid on April 17, 2023. |

| (2) | The Fund estimates that it has distributed more than its income and net realized capital gains; therefore, a portion of your distribution may be a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund's investment performance and should not be confused with "yield" or "income." |

| (3) | Based on Net Asset Value (“NAV”) as of March 31, 2023. |

| (4) | Total Returns are through March 31, 2023. |

| (5) | The Fund anticipates that, due to the tax treatment of cash distributions made by Master Limited Partnerships in which the Fund invests, a portion of distributions the Fund makes to Common Shareholders may consist of a tax-deferred return of capital. |

The amounts and sources of distributions reported in this Notice are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Fund's investment experience during the remainder of its fiscal year and may be subject to changes based on tax regulations. The Fund will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for federal income tax purposes. You should not use this Notice as a substitute for your Form 1099-DIV.

_____________________________________

First Trust Advisors L.P. Contact:

Don Swade (630) 765-8661

Notice Regarding Your Monthly Distribution

First Trust Energy Infrastructure Fund (FIF)

The closed-end fund listed above (the “Fund”) has declared a distribution payable on May 15, 2023, to shareholders of record as of May 2, 2023, with an ex-dividend date of May 1, 2023. This Notice is meant to provide you information about the sources of your Fund's distributions. You should not draw any conclusions about the Fund’s investment performance from the amount of its distribution or from the terms of its Managed Distribution Plan.

The following tables set forth the estimated amounts of the current distribution and the cumulative distributions paid this fiscal year to date for the Fund from the following sources: net investment income (“NII”); net realized short-term capital gains (“STCG”); net realized long-term capital gains (“LTCG”); and return of capital (“ROC”). These estimates are based upon information as of April 30, 2023, are calculated based on a generally accepted accounting principles (“GAAP”) basis and include the prior fiscal year-end undistributed net investment income. The amounts and sources of distributions are expressed per common share.

| Annualized | 5 Year Avg. | |||||||||||||||||||||||||

| Total | Current Distribution ($) | Current Distribution (%) | Current Dist. Rate | Annual Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Current Distribution | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.10000 | $0.10000 | — | — | — | 100.00% | — | — | — | 6.99% | 8.00% | |||||||||||||

| Cumulative | Cumulative | |||||||||||||||||||||||||

| Total Cumulative | Cumulative Distributions Fiscal YTD ($) | Cumulative Distributions Fiscal YTD (%) | Fiscal YTD Distributions | Fiscal YTD Total | ||||||||||||||||||||||

| Fund Ticker | Fund Cusip | Fiscal Year End | Fiscal YTD Distributions (1) | NII | STCG | LTCG | ROC (2) | NII | STCG | LTCG | ROC (2) | as a % of NAV (3) | Return on NAV (4) | |||||||||||||

| FIF (5) | 33738C103 | 11/30/2023 | $0.45900 | $0.45900 | — | — | — | 100.00% | — | — | — | 2.67% | -1.88% | |||||||||||||

| (1) | Includes the most recent monthly distribution paid on May 15, 2023. |

| (2) | The Fund estimates that it has distributed more than its income and net realized capital gains; therefore, a portion of your distribution may be a return of capital. A return of capital may occur, for example, when some or all of the money that you invested in the Fund is paid back to you. A return of capital distribution does not necessarily reflect the Fund's investment performance and should not be confused with "yield" or "income." |

| (3) | Based on Net Asset Value (“NAV”) as of April 30, 2023. |

| (4) | Total Returns are through April 30, 2023. |

| (5) | The Fund anticipates that, due to the tax treatment of cash distributions made by Master Limited Partnerships in which the Fund invests, a portion of distributions the Fund makes to Common Shareholders may consist of a tax-deferred return of capital. |

The amounts and sources of distributions reported in this Notice are only estimates and are not being provided for tax reporting purposes. The actual amounts and sources of the amounts for tax reporting purposes will depend upon the Fund's investment experience during the remainder of its fiscal year and may be subject to changes based on tax regulations. The Fund will send you a Form 1099-DIV for the calendar year that will tell you how to report these distributions for federal income tax purposes. You should not use this Notice as a substitute for your Form 1099-DIV.

_____________________________________

First Trust Advisors L.P. Contact:

Don Swade (630) 765-8661

N-2 |

6 Months Ended |

|---|---|

|

May 31, 2023

$ / shares

shares

| |

| Cover [Abstract] | |

| Entity Central Index Key | 0001513789 |

| Amendment Flag | false |

| Entity Inv Company Type | N-2 |

| Document Type | N-CSRS |

| Entity Registrant Name | First Trust Energy Infrastructure Fund |

| General Description of Registrant [Abstract] | |

| Investment Objectives and Practices [Text Block] | The Fund’s investment objective is to seek a high level of total return with an emphasis on current distributions paid to shareholders. The Fund pursues its investment objective by investing primarily in securities of companies engaged in the energy infrastructure sector. These companies principally include publicly-traded master limited partnerships and limited liability companies taxed as partnerships (“MLPs”), MLP affiliates, YieldCos, pipeline companies, utilities and other infrastructure-related companies that derive at least 50% of their revenues from operating, or providing services in support of, infrastructure assets such as pipelines, power transmission and petroleum and natural gas storage in the petroleum, natural gas and power generation industries (collectively, “Energy Infrastructure Companies”). For purposes of the Fund’s investment objective, total return includes capital appreciation of, and all distributions received from, securities in which the Fund invests, taking into account the varying tax characteristics of such securities. Under normal market conditions, the Fund invests at least 80% of its managed assets (total asset value of the Fund minus the sum of the Fund’s liabilities other than the principal amount of borrowings) in securities of Energy Infrastructure Companies. There can be no assurance that the Fund will achieve its investment objective. The Fund may not be appropriate for all investors. |

| Risk [Text Block] | Principal

Risks

The

Fund is a closed-end management investment company designed primarily as a long-term investment and not as a trading vehicle. The Fund

is not intended to be a complete investment program and, due to the uncertainty inherent in all investments, there can be no assurance

that the Fund will achieve its investment objective. The following discussion summarizes the principal risks associated with investing

in the Fund, which includes the risk that you could lose some or all of your investment in the Fund. The Fund is subject to the informational

requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940 and, in accordance therewith, files reports,

proxy statements and other information that is available for review.

Covered

Call Options Risk. As the writer (seller) of a call option, the Fund forgoes, during the life

of the option, the opportunity to profit from increases in the market value of the portfolio security covering the option above the sum

of the premium and the strike price of the call option but retains the risk of loss should the price of the underlying security decline.

The value of call options written by the Fund, which are priced daily, are determined by trading activity in the broad options market

and will be affected by, among other factors, changes in the value of the underlying security in relation to the strike price, changes

in dividend rates of the underlying security, changes in interest rates, changes in actual or perceived volatility of the stock market

and the underlying security, and the time remaining until the expiration date. The value of call options written by the Fund may be adversely

affected if the market for the option is reduced or becomes illiquid. There can be no assurance that a liquid market will exist when the