We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Share Name | Share Symbol | Market | Type |

|---|---|---|---|

| First Trust abrdn Global Opportunity Income Fund | NYSE:FAM | NYSE | Common Stock |

| Price Change | % Change | Share Price | High Price | Low Price | Open Price | Shares Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|

| 0.00 | 0.00% | 6.51 | 0 | 00:00:00 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21636

(Exact name of registrant as specified in charter)

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(Address of principal executive offices) (Zip code)

W. Scott Jardine, Esq.

First Trust Portfolios L.P.

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(Name and address

of agent for service)

Registrant’s telephone number, including area code: (630) 765-8000

Date of fiscal year end: December 31

Date of reporting period:

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| (a) | The Report to Shareholders is attached herewith. |

|

|

1 |

|

|

2 |

|

|

4 |

|

|

9 |

|

|

16 |

|

|

17 |

|

|

18 |

|

|

19 |

|

|

20 |

|

|

21 |

|

|

29 |

|

|

30 |

|

|

32 |

|

|

42 |

|

|

44 |

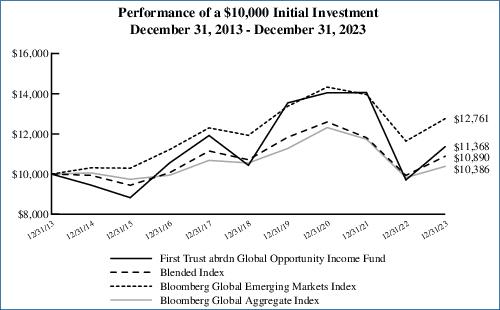

| Performance | ||||

| Average Annual Total Returns | ||||

| 1

Year Ended 12/31/23 |

5

Years Ended 12/31/23 |

10

Years Ended 12/31/23 |

Inception

(11/23/04) to 12/31/23 | |

| Fund Performance(3) | ||||

| NAV | 15.69% | 0.29% | 1.38% | 4.31% |

| Market Value | 17.08% | 1.72% | 1.29% | 3.54% |

| Index Performance | ||||

| Blended Index(4) | 9.58% | 0.32% | 0.86% | 3.45% |

| Bloomberg Global Emerging Markets Index | 9.63% | 1.36% | 2.47% | 5.19% |

| Bloomberg Global Aggregate Index | 5.71% | -0.32% | 0.38% | 2.15% |

| Fund Allocation | % of Net Assets |

| Foreign Sovereign Bonds and Notes | 73.9% |

| Foreign Corporate Bonds and Notes | 28.1 |

| U.S. Government Bonds and Notes | 18.3 |

| Outstanding Loan | (23.6) |

| Net Other Assets and Liabilities(5) | 3.3 |

| Total | 100.0% |

| (1) | Most recent distribution paid through December 31, 2023. Subject to change in the future. |

| (2) | Distribution rates are calculated by annualizing the most recent distribution paid through the report date and then dividing by Common Share Price or NAV, as applicable, as of December 31, 2023. Subject to change in the future. |

| (3) | Total return is based on the combination of reinvested dividend, capital gain, and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan and changes in NAV per share for NAV returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of future results. |

| (4) | Blended Index consists of the following: FTSE World Government Bond Index (40.0%); JPMorgan Emerging Markets Bond Index - Global Diversified (30.0%); JPMorgan Global Bond Index - Emerging Markets Diversified (30.0%). The Blended Index returns are calculated by using the monthly return of the three indices during each period shown above. At the beginning of each month the three indices are rebalanced to a 40.0%, 30.0%, and 30.0% ratio, respectively, to account for divergence from that ratio that occurred during the course of each month. The monthly returns are then compounded for each period shown above, giving the performance for the Blended Index for each period shown above. |

| (5) | Includes forward foreign currency contracts. |

| (6) | The credit quality and ratings information presented above reflects the ratings assigned by one or more nationally recognized statistical rating organizations (NRSROs), including S&P Global Ratings, Moody’s Investors Service, Inc., Fitch Ratings or a comparably rated NRSRO. For situations in which a security is rated by more than one NRSRO and the ratings are not equivalent, the highest ratings are used. Sub-investment grade ratings are those rated BB+/Ba1 or lower. Investment grade ratings are those rated BBB-/Baa3 or higher. The credit ratings shown relate to the creditworthiness of the issuers of the underlying securities in the Fund, and not to the Fund or its shares. Credit ratings are subject to change. |

| (7) | Portfolio securities are included in a country based upon their underlying credit exposure as determined by abrdn Inc., the sub-advisor. |

| Average Annual Total Returns | ||||

| 1

Year Ended 12/31/23 |

5

Years Ended 12/31/23 |

10

Years Ended 12/31/23 |

Inception

(11/23/04) to 12/31/23 | |

| Fund Performance(1) | ||||

| NAV | 15.69% | 0.29% | 1.38% | 4.31% |

| Market Value | 17.08% | 1.72% | 1.29% | 3.54% |

| Index Performance | ||||

| Blended Index(2) | 9.58% | 0.32% | 0.86% | 3.45% |

| Bloomberg Global Emerging Markets Index | 9.63% | 1.36% | 2.47% | 5.19% |

| Bloomberg Global Aggregate Index | 5.71% | -0.32% | 0.38% | 2.15% |

| (1) | Total return is based on the combination of reinvested dividend, capital gain and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan and changes in NAV per share for NAV returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. |

| (2) | Blended Index consists of the following: FTSE World Government Bond Index (40.0%); JPMorgan Emerging Markets Bond Index – Global Diversified (30.0%); JPMorgan Global Bond Index – Emerging Markets Diversified (30.0%). The Blended Index returns are calculated by using the monthly return of the three indices during each period shown above. At the beginning of each month the three indices are rebalanced to a 40.0%, 30.0%, and 30.0% ratio, respectively, to account for divergence from that ratio that occurred during the course of each month. The monthly returns are then compounded for each period shown above, giving the performance for the Blended Index for each period shown above. |

| Principal Value (Local Currency) |

Description | Stated Coupon |

Stated Maturity |

Value (US Dollars) | ||||

| FOREIGN SOVEREIGN BONDS AND NOTES (a) – 73.9% | ||||||||

| Angola – 1.7% | ||||||||

| 1,444,000 |

Angolan Government International Bond (USD) (b) |

9.13% | 11/26/49 | $1,182,275 | ||||

| Argentina – 2.2% | ||||||||

| 383,926 |

Argentine Republic Government International Bond (USD) |

1.00% | 07/09/29 | 154,338 | ||||

| 385,881 |

Argentine Republic Government International Bond (USD) (c) |

0.75% | 07/09/30 | 155,706 | ||||

| 2,949,672 |

Argentine Republic Government International Bond (USD) (c) |

3.63% | 07/09/35 | 1,019,304 | ||||

| 543,200 |

Argentine Republic Government International Bond (USD) (c) |

4.25% | 01/09/38 | 216,288 | ||||

| 1,545,636 | ||||||||

| Australia – 5.7% | ||||||||

| 7,000,000 |

Treasury Corp. of Victoria (AUD) |

1.50% | 11/20/30 | 3,978,351 | ||||

| Bahrain – 1.3% | ||||||||

| 500,000 |

Bahrain Government International Bond (USD) (d) |

4.25% | 01/25/28 | 472,785 | ||||

| 510,000 |

Bahrain Government International Bond (USD) (b) |

6.25% | 01/25/51 | 423,809 | ||||

| 896,594 | ||||||||

| Brazil – 8.8% | ||||||||

| 5,079,000 |

Brazil Notas do Tesouro Nacional, Series F (BRL) |

10.00% | 01/01/27 | 1,052,615 | ||||

| 24,870,000 |

Brazil Notas do Tesouro Nacional, Series F (BRL) |

10.00% | 01/01/29 | 5,121,567 | ||||

| 6,174,182 | ||||||||

| Canada – 1.2% | ||||||||

| 1,251,000 |

CPPIB Capital, Inc. (CAD) (b) |

1.95% | 09/30/29 | 866,669 | ||||

| Colombia – 2.0% | ||||||||

| 6,025,900,000 |

Colombian TES (COP) |

9.25% | 05/28/42 | 1,411,921 | ||||

| Dominican Republic – 1.6% | ||||||||

| 359,000 |

Dominican Republic International Bond (USD) (d) |

5.50% | 02/22/29 | 351,820 | ||||

| 25,050,000 |

Dominican Republic International Bond (DOP) (d) |

11.25% | 09/15/35 | 466,583 | ||||

| 340,000 |

Dominican Republic International Bond (USD) (b) |

5.88% | 01/30/60 | 294,933 | ||||

| 1,113,336 | ||||||||

| Ecuador – 1.6% | ||||||||

| 3,169,400 |

Ecuador Government International Bond (USD) (b) (c) |

3.50% | 07/31/35 | 1,142,184 | ||||

| Egypt – 1.9% | ||||||||

| 1,223,000 |

Egypt Government International Bond (USD) (d) |

8.50% | 01/31/47 | 764,302 | ||||

| 928,000 |

Egypt Government International Bond (USD) (b) |

7.90% | 02/21/48 | 562,211 | ||||

| 1,326,513 | ||||||||

| Georgia – 0.3% | ||||||||

| 200,000 |

Georgia Government International Bond (USD) (d) |

2.75% | 04/22/26 | 187,928 | ||||

| Ghana – 0.4% | ||||||||

| 662,000 |

Ghana Government International Bond (USD) (d) (e) |

7.63% | 05/16/29 | 290,322 | ||||

| Hungary – 2.0% | ||||||||

| 243,430,000 |

Hungary Government Bond (HUF) |

2.50% | 10/24/24 | 676,575 | ||||

| 269,970,000 |

Hungary Government Bond (HUF) |

3.00% | 10/27/27 | 709,462 | ||||

| 1,386,037 | ||||||||

| Indonesia – 0.3% | ||||||||

| 3,259,000,000 |

Indonesia Treasury Bond (IDR) |

8.38% | 03/15/34 | 236,736 | ||||

| Principal Value (Local Currency) |

Description | Stated Coupon |

Stated Maturity |

Value (US Dollars) | ||||

| FOREIGN SOVEREIGN BONDS AND NOTES (a) (Continued) | ||||||||

| Iraq – 1.2% | ||||||||

| 909,563 |

Iraq International Bond (USD) (b) |

5.80% | 01/15/28 | $852,775 | ||||

| Ivory Coast – 1.2% | ||||||||

| 919,000 |

Ivory Coast Government International Bond (EUR) (b) |

6.63% | 03/22/48 | 811,624 | ||||

| Kenya – 1.0% | ||||||||

| 873,000 |

Republic of Kenya Government International Bond (USD) (b) |

8.25% | 02/28/48 | 726,633 | ||||

| Malaysia – 2.0% | ||||||||

| 6,499,000 |

Malaysia Government Bond (MYR) |

3.89% | 03/15/27 | 1,427,194 | ||||

| Mexico – 8.6% | ||||||||

| 20,000,000 |

Mexican Bonos (MXN) |

10.00% | 12/05/24 | 1,172,151 | ||||

| 61,423,900 |

Mexican Bonos (MXN) |

5.75% | 03/05/26 | 3,344,234 | ||||

| 28,833,400 |

Mexican Bonos (MXN) |

7.75% | 11/13/42 | 1,494,902 | ||||

| 6,011,287 | ||||||||

| Morocco – 0.5% | ||||||||

| 400,000 |

Morocco Government International Bond (USD) (b) |

2.38% | 12/15/27 | 359,122 | ||||

| New Zealand – 4.8% | ||||||||

| 3,708,000 |

New Zealand Government Bond (NZD) |

0.50% | 05/15/24 | 2,302,397 | ||||

| 2,337,000 |

New Zealand Government Bond (NZD) |

2.75% | 05/15/51 | 1,055,683 | ||||

| 3,358,080 | ||||||||

| Nigeria – 0.7% | ||||||||

| 634,000 |

Nigeria Government International Bond (USD) (d) |

7.63% | 11/28/47 | 504,654 | ||||

| Oman – 2.4% | ||||||||

| 1,590,000 |

Oman Government International Bond (USD) (d) |

7.00% | 01/25/51 | 1,720,444 | ||||

| Peru – 3.3% | ||||||||

| 8,575,000 |

Peruvian Government International Bond (PEN) (b) |

6.90% | 08/12/37 | 2,339,170 | ||||

| Poland – 3.6% | ||||||||

| 12,836,000 |

Republic of Poland Government Bond (PLN) |

1.75% | 04/25/32 | 2,538,812 | ||||

| Qatar – 2.3% | ||||||||

| 1,733,000 |

Qatar Government International Bond (USD) (b) |

4.40% | 04/16/50 | 1,600,859 | ||||

| Rwanda – 0.6% | ||||||||

| 532,000 |

Rwanda International Government Bond (USD) (d) |

5.50% | 08/09/31 | 427,667 | ||||

| Saudi Arabia – 1.1% | ||||||||

| 745,000 |

Saudi Government International Bond (USD) (d) |

4.38% | 04/16/29 | 743,283 | ||||

| South Africa – 2.3% | ||||||||

| 37,211,600 |

Republic of South Africa Government Bond (ZAR) |

9.00% | 01/31/40 | 1,595,059 | ||||

| Turkey – 2.6% | ||||||||

| 1,617,000 |

Turkey Government International Bond (USD) |

9.38% | 01/19/33 | 1,830,525 | ||||

| Ukraine – 0.2% | ||||||||

| 572,000 |

Ukraine Government International Bond (USD) (b) |

7.75% | 09/01/29 | 158,620 | ||||

| United Kingdom – 2.8% | ||||||||

| 1,458,500 |

United Kingdom Gilt (GBP) (b) |

4.25% | 06/07/32 | 1,968,651 | ||||

| Uruguay – 1.0% | ||||||||

| 25,388,985 |

Uruguay Government International Bond (UYU) |

4.38% | 12/15/28 | 680,517 | ||||

| Principal Value (Local Currency) |

Description | Stated Coupon |

Stated Maturity |

Value (US Dollars) | ||||

| FOREIGN SOVEREIGN BONDS AND NOTES (a) (Continued) | ||||||||

| Uzbekistan – 0.7% | ||||||||

| 300,000 |

National Bank of Uzbekistan (USD) (b) |

4.85% | 10/21/25 | $278,480 | ||||

| 260,000 |

Republic of Uzbekistan International Bond (USD) (d) |

3.70% | 11/25/30 | 219,193 | ||||

| 497,673 | ||||||||

|

Total Foreign Sovereign Bonds and Notes |

51,891,333 | |||||||

| (Cost $53,681,044) | ||||||||

| FOREIGN CORPORATE BONDS AND NOTES (a) (f) – 28.1% | ||||||||

| Barbados – 0.5% | ||||||||

| 337,000 |

Sagicor Financial Co., Ltd. (USD) (d) |

5.30% | 05/13/28 | 323,877 | ||||

| Brazil – 3.4% | ||||||||

| 440,000 |

Banco do Brasil S.A. (USD) (b) (g) |

6.25% | (h) | 430,421 | ||||

| 228,000 |

BRF S.A. (USD) (d) |

5.75% | 09/21/50 | 170,577 | ||||

| 375,274 |

Guara Norte Sarl (USD) (d) |

5.20% | 06/15/34 | 342,289 | ||||

| 500,000 |

Itau Unibanco Holding S.A. (USD) (b) (g) |

4.63% | (h) | 440,369 | ||||

| 291,000 |

Minerva Luxembourg S.A. (USD) (d) |

8.88% | 09/13/33 | 308,182 | ||||

| 1,550,000 |

OAS Finance Ltd. (USD) (e) (g) (i) (j) |

8.88% | (h) | 11,625 | ||||

| 460,000 |

OAS Investments GmbH (USD) (e) (i) (j) |

8.25% | 10/19/19 | 3,450 | ||||

| 765,000 |

Petrobras Global Finance BV (USD) |

5.50% | 06/10/51 | 645,634 | ||||

| 2,352,547 | ||||||||

| Chile – 0.6% | ||||||||

| 468,000 |

Empresa Nacional del Petroleo (USD) (d) |

3.45% | 09/16/31 | 394,948 | ||||

| China – 1.3% | ||||||||

| 888,000 |

Huarong Finance II Co., Ltd. (USD) (b) |

5.50% | 01/16/25 | 880,230 | ||||

| Colombia – 1.0% | ||||||||

| 218,000 |

Ecopetrol S.A. (USD) |

8.88% | 01/13/33 | 237,109 | ||||

| 600,000 |

Empresas Publicas de Medellin ESP (USD) (b) |

4.38% | 02/15/31 | 491,100 | ||||

| 728,209 | ||||||||

| Dominican Republic – 0.6% | ||||||||

| 491,000 |

AES Espana BV (USD) (d) |

5.70% | 05/04/28 | 447,625 | ||||

| Ecuador – 0.7% | ||||||||

| 465,770 |

International Airport Finance S.A. (USD) (d) |

12.00% | 03/15/33 | 478,411 | ||||

| Georgia – 0.5% | ||||||||

| 345,000 |

Georgian Railway JSC (USD) (b) |

4.00% | 06/17/28 | 318,444 | ||||

| India – 2.7% | ||||||||

| 160,000,000 |

HDFC Bank Ltd. (INR) (b) |

8.10% | 03/22/25 | 1,914,960 | ||||

| Israel – 1.3% | ||||||||

| 312,000 |

Bank Leumi Le-Israel BM (USD) (b) (d) (g) |

7.13% | 07/18/33 | 307,202 | ||||

| 311,000 |

Energean Israel Finance Ltd. (USD) (b) (d) |

8.50% | 09/30/33 | 298,171 | ||||

| 300,000 |

Teva Pharmaceutical Finance Netherlands III B.V. (USD) |

7.13% | 01/31/25 | 302,849 | ||||

| 908,222 | ||||||||

| Kazakhstan – 1.0% | ||||||||

| 806,000 |

KazMunayGas National Co. JSC (USD) (b) |

5.75% | 04/19/47 | 708,551 | ||||

| Mexico – 3.3% | ||||||||

| 400,000 |

BBVA Bancomer S.A. (USD) (b) (g) |

5.13% | 01/18/33 | 362,716 | ||||

| 237,000 |

Braskem Idesa S.A.P.I. (USD) (d) |

6.99% | 02/20/32 | 138,962 | ||||

| Principal Value (Local Currency) |

Description | Stated Coupon |

Stated Maturity |

Value (US Dollars) | ||||

| FOREIGN CORPORATE BONDS AND NOTES (a) (f) (Continued) | ||||||||

| Mexico (Continued) | ||||||||

| 225,000 |

Cemex SAB de CV (USD) (d) (g) |

9.13% | (h) | $239,906 | ||||

| 22,160,000 |

Petroleos Mexicanos (MXN) (b) |

7.19% | 09/12/24 | 1,247,992 | ||||

| 350,000 |

Sixsigma Networks Mexico SA de CV (USD) (d) |

7.50% | 05/02/25 | 320,331 | ||||

| 2,309,907 | ||||||||

| Nigeria – 2.2% | ||||||||

| 526,000 |

Access Bank PLC (USD) (d) |

6.13% | 09/21/26 | 474,794 | ||||

| 464,000 |

BOI Finance BV (EUR) (d) |

7.50% | 02/16/27 | 472,179 | ||||

| 270,000 |

IHS Netherlands Holdco BV (USD) (d) |

8.00% | 09/18/27 | 241,369 | ||||

| 400,000 |

SEPLAT Energy PLC (USD) (d) |

7.75% | 04/01/26 | 368,800 | ||||

| 1,557,142 | ||||||||

| Oman – 0.9% | ||||||||

| 250,000 |

EDO Sukuk Ltd. (USD) (d) |

5.88% | 09/21/33 | 258,106 | ||||

| 400,000 |

Oryx Funding Ltd. (USD) (d) |

5.80% | 02/03/31 | 402,093 | ||||

| 660,199 | ||||||||

| Peru – 0.5% | ||||||||

| 522,000 |

Petroleos del Peru S.A. (USD) (d) |

5.63% | 06/19/47 | 322,061 | ||||

| Russia – 0.0% | ||||||||

| 500,000 |

Sovcombank Via SovCom Capital DAC (USD) (e) (g) (i) |

7.75% | (h) | 9,540 | ||||

| Singapore – 0.7% | ||||||||

| 520,000 |

Puma International Financing S.A. (USD) (b) |

5.00% | 01/24/26 | 494,858 | ||||

| South Africa – 2.5% | ||||||||

| 530,000 |

Eskom Holdings SOC Ltd. (USD) (b) |

7.13% | 02/11/25 | 530,895 | ||||

| 43,650,000 |

Eskom Holdings SOC Ltd. (ZAR) |

(k) | 12/31/32 | 516,617 | ||||

| 400,000 |

Liquid Telecommunications Financing PLC (USD) (d) |

5.50% | 09/04/26 | 234,490 | ||||

| 300,000 |

Sasol Financing USA LLC (USD) |

6.50% | 09/27/28 | 286,120 | ||||

| 200,000 |

Transnet SOC Ltd. (USD) (d) |

8.25% | 02/06/28 | 201,973 | ||||

| 1,770,095 | ||||||||

| Tanzania – 0.6% | ||||||||

| 452,000 |

HTA Group Ltd. (USD) (d) |

7.00% | 12/18/25 | 445,973 | ||||

| Trinidad And Tobago – 1.0% | ||||||||

| 632,000 |

Heritage Petroleum Co., Ltd. (USD) (d) |

9.00% | 08/12/29 | 665,496 | ||||

| Turkey – 0.5% | ||||||||

| 352,000 |

WE Soda Investments Holdings PLC (USD) (d) |

9.50% | 10/06/28 | 364,250 | ||||

| Ukraine – 1.6% | ||||||||

| 467,000 |

Kernel Holding S.A. (USD) (d) |

6.75% | 10/27/27 | 306,527 | ||||

| 567,000 |

MHP Lux S.A. (USD) (b) |

6.95% | 04/03/26 | 440,559 | ||||

| 453,000 |

NPC Ukrenergo (USD) (d) (e) |

6.88% | 11/09/28 | 127,384 | ||||

| 460,000 |

Ukraine Railways Via Rail Capital Markets PLC (USD) (b) (e) |

8.25% | 07/09/26 | 252,111 | ||||

| 1,126,581 | ||||||||

| Zambia – 0.7% | ||||||||

| 291,000 |

First Quantum Minerals Ltd. (USD) (b) |

7.50% | 04/01/25 | 278,291 | ||||

| Principal Value (Local Currency) |

Description | Stated Coupon |

Stated Maturity |

Value (US Dollars) | ||||

| FOREIGN CORPORATE BONDS AND NOTES (a) (f) (Continued) | ||||||||

| Zambia (Continued) | ||||||||

| 285,000 |

First Quantum Minerals Ltd. (USD) (d) |

8.63% | 06/01/31 | $241,894 | ||||

| 520,185 | ||||||||

|

Total Foreign Corporate Bonds and Notes |

19,702,311 | |||||||

| (Cost $23,754,554) | ||||||||

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| U.S. GOVERNMENT BONDS AND NOTES (a) – 18.3% | ||||||||

| $2,038,500 |

United States Treasury Bond |

2.38% | 05/15/51 | 1,455,298 | ||||

| 2,783,500 |

United States Treasury Note |

2.75% | 07/31/27 | 2,672,323 | ||||

| 9,432,200 |

United States Treasury Note |

2.38% | 05/15/29 | 8,744,313 | ||||

|

Total U.S. Government Bonds and Notes |

12,871,934 | |||||||

| (Cost $14,086,499) | ||||||||

|

Total Investments – 120.3% |

84,465,578 | ||

| (Cost $91,522,097) | |||

|

Outstanding Loan – (23.6)% |

(16,600,000) | ||

|

Net Other Assets and Liabilities – 3.3% |

2,342,941 | ||

|

Net Assets – 100.0% |

$70,208,519 |

| Forward Foreign Currency Contracts | ||||||||||||||

| Settlement Date |

Counterparty | Amount Purchased |

Amount Sold |

Purchase Value as of 12/31/2023 |

Sale Value as of 12/31/2023 |

Unrealized Appreciation/ (Depreciation) | ||||||||

| 01/19/24 | BAR | CAD | 587,000 | USD | 432,357 | $ 443,133 | $ 432,357 | $ 10,776 | ||||||

| 01/19/24 | CIT | JPY | 454,387,794 | USD | 3,105,874 | 3,233,236 | 3,105,874 | 127,362 | ||||||

| 01/19/24 | GS | USD | 4,427,624 | AUD | 6,875,000 | 4,427,624 | 4,688,335 | (260,711) | ||||||

| 02/08/24 | CIT | USD | 1,702,443 | BRL | 8,460,000 | 1,702,443 | 1,736,160 | (33,717) | ||||||

| 01/19/24 | CIT | USD | 369,509 | GBP | 301,347 | 369,509 | 384,158 | (14,649) | ||||||

| 01/19/24 | BAR | USD | 488,514 | GBP | 397,000 | 488,514 | 506,097 | (17,583) | ||||||

| 01/19/24 | DB | USD | 1,122,711 | NZD | 1,865,000 | 1,122,711 | 1,179,065 | (56,354) | ||||||

| 01/19/24 | DB | USD | 1,779,679 | ZAR | 33,888,132 | 1,779,679 | 1,849,110 | (69,431) | ||||||

|

Net Unrealized Appreciation / (Depreciation) |

$(314,307) | |||||||||||||

| (a) | All of these securities are available to serve as collateral for the outstanding loan. |

| (b) | This security may be resold to qualified foreign investors and foreign institutional buyers under Regulation S of the Securities Act of 1933, as amended (the “1933 Act”). |

| (c) | Step-up security. A security where the coupon increases or steps up at a predetermined date. Interest rate shown reflects the rate in effect at December 31, 2023. |

| (d) | This security, sold within the terms of a private placement memorandum, is exempt from registration upon resale under Rule 144A of the 1933 Act, and may be resold in transactions exempt from registration, normally to qualified institutional buyers. Pursuant to procedures adopted by the Fund’s Board of Trustees, this security has been determined to be liquid by abrdn Inc., the Fund’s sub-advisor (“abrdn” or the “Sub-Advisor”). Although market instability can result in periods of increased overall market illiquidity, liquidity for each security is determined based on security specific factors and assumptions, which require subjective judgment. At December 31, 2023, securities noted as such amounted to $15,046,851 or 21.4% of net assets. |

| (e) | This issuer is in default and interest is not being accrued by the Fund. |

| (f) | Portfolio securities are included in a country based upon their underlying credit exposure as determined by abrdn. |

| (g) | Fixed-to-floating or fixed-to-variable rate security. The interest rate shown reflects the fixed rate in effect at December 31, 2023. At a predetermined date, the fixed rate will change to a floating rate or a variable rate. |

| (h) | Perpetual maturity. |

| (i) | This security, sold within the terms of a private placement memorandum, is exempt from registration upon resale under Rule 144A of the 1933 Act, and may be resold in transactions exempt from registration, normally to qualified institutional buyers (see Note 2C - Restricted Securities in the Notes to Financial Statements). |

| (j) | This issuer has filed for bankruptcy protection in a São Paulo state court. |

| (k) | Zero coupon bond. |

| Abbreviations throughout the Portfolio of Investments: | |

| AUD | – Australian Dollar |

| BAR | – Barclays Bank |

| BRL | – Brazilian Real |

| CAD | – Canadian Dollar |

| CIT | – Citibank, NA |

| COP | – Colombian Peso |

| DB | – Deutsche Bank |

| DOP | – Dominican Republic Peso |

| EUR | – Euro |

| GBP | – British Pound Sterling |

| GS | – Goldman Sachs |

| HUF | – Hungarian Forint |

| IDR | – Indonesian Rupiah |

| INR | – Indian Rupee |

| JPY | – Japanese Yen |

| MXN | – Mexican Peso |

| MYR | – Malaysian Ringgit |

| NZD | – New Zealand Dollar |

| PEN | – Peruvian Nuevo Sol |

| PLN | – Polish Zloty |

| USD | – United States Dollar |

| UYU | – Uruguayan Peso |

| ZAR | – South African Rand |

| Currency

Exposure Diversification |

%

of Total Investments† |

| USD | 61.1% |

| MXN | 8.6 |

| BRL | 5.3 |

| JPY | 3.8 |

| PLN | 3.0 |

| PEN | 2.8 |

| NZD | 2.6 |

| INR | 2.3 |

| MYR | 1.7 |

| COP | 1.7 |

| HUF | 1.6 |

| CAD | 1.6 |

| EUR | 1.5 |

| GBP | 1.3 |

| UYU | 0.8 |

| DOP | 0.5 |

| ZAR | 0.3 |

| IDR | 0.3 |

| AUD | -0.8 |

| Total | 100.0% |

| † | The weightings include the impact of currency forwards. |

| ASSETS TABLE | ||||

| Total Value at 12/31/2023 |

Level

1 Quoted Prices |

Level

2 Significant Observable Inputs |

Level

3 Significant Unobservable Inputs | |

|

Foreign Sovereign Bonds and Notes* |

$ 51,891,333 | $ — | $ 51,891,333 | $ — |

|

Foreign Corporate Bonds and Notes* |

19,702,311 | — | 19,702,311 | — |

|

U.S. Government Bonds and Notes |

12,871,934 | — | 12,871,934 | — |

|

Total Investments |

84,465,578 | — | 84,465,578 | — |

|

Forward Foreign Currency Contracts |

138,138 | — | 138,138 | — |

|

Total |

$ 84,603,716 | $— | $ 84,603,716 | $— |

| LIABILITIES TABLE | ||||

| Total Value at 12/31/2023 |

Level

1 Quoted Prices |

Level

2 Significant Observable Inputs |

Level

3 Significant Unobservable Inputs | |

|

Forward Foreign Currency Contracts |

$ (452,445) | $ — | $ (452,445) | $ — |

| * | See Portfolio of Investments for country breakout. |

| ASSETS: | |

|

Investments, at value |

$ 84,465,578 |

|

Cash |

763,273 |

|

Foreign currency |

2,386 |

|

Restricted Cash |

210,000 |

|

Unrealized appreciation on forward foreign currency contracts |

138,138 |

| Receivables: | |

|

Interest |

1,850,424 |

|

Reclaims |

202,913 |

|

Prepaid expenses |

540 |

|

Total Assets |

87,633,252 |

| LIABILITIES: | |

|

Outstanding loan |

16,600,000 |

|

Unrealized depreciation on forward foreign currency contracts |

452,445 |

|

Due to broker |

80,000 |

| Payables: | |

|

Interest and fees on loan |

83,583 |

|

Investment advisory fees |

72,503 |

|

Audit and tax fees |

63,190 |

|

Legal fees |

19,606 |

|

Shareholder reporting fees |

18,163 |

|

Custodian fees |

16,761 |

|

Administrative fees |

12,266 |

|

Deferred foreign capital gains tax |

2,572 |

|

Transfer agent fees |

1,519 |

|

Financial reporting fees |

771 |

|

Trustees’ fees and expenses |

68 |

|

Other liabilities |

1,286 |

|

Total Liabilities |

17,424,733 |

|

NET ASSETS |

$70,208,519 |

| NET ASSETS consist of: | |

|

Paid-in capital |

$ 107,483,185 |

|

Par value |

101,432 |

|

Accumulated distributable earnings (loss) |

(37,376,098) |

|

NET ASSETS |

$70,208,519 |

|

NET ASSET VALUE, per Common Share (par value $0.01 per Common Share) |

$6.92 |

|

Number of |

|

|

Investments, at cost |

$91,522,097 |

|

Foreign currency, at cost (proceeds) |

$2,344 |

| INVESTMENT INCOME: | ||

|

Interest |

$ 5,927,503 | |

|

Foreign withholding tax |

(10,287) | |

|

Total investment income |

5,917,216 | |

| EXPENSES: | ||

|

Interest and fees on loan |

1,128,908 | |

|

Investment advisory fees |

868,449 | |

|

Legal fees |

81,006 | |

|

Audit and tax fees |

71,302 | |

|

Shareholder reporting fees |

55,377 | |

|

Administrative fees |

50,324 | |

|

Listing expense |

23,756 | |

|

Custodian fees |

22,902 | |

|

Transfer agent fees |

20,576 | |

|

Trustees’ fees and expenses |

20,160 | |

|

Financial reporting fees |

9,250 | |

|

Other |

17,631 | |

|

Total expenses |

2,369,641 | |

|

NET INVESTMENT INCOME (LOSS) |

3,547,575 | |

| NET REALIZED AND UNREALIZED GAIN (LOSS): | ||

| Net realized gain (loss) on: | ||

|

Investments |

(5,305,072) | |

|

Forward foreign currency contracts |

(849,870) | |

|

Foreign currency transactions |

3,107,834 | |

|

Foreign capital gains tax |

(23,023) | |

|

Net realized gain (loss) |

(3,070,131) | |

| Net change in unrealized appreciation (depreciation) on: | ||

|

Investments |

10,983,614 | |

|

Forward foreign currency contracts |

331,031 | |

|

Foreign currency translation |

(2,680,673) | |

|

Deferred foreign capital gains tax |

9,815 | |

|

Net change in unrealized appreciation (depreciation) |

8,643,787 | |

|

NET REALIZED AND UNREALIZED GAIN (LOSS) |

5,573,656 | |

|

NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS |

$ 9,121,231 | |

| Year Ended 12/31/2023 |

Year Ended 12/31/2022 | ||

| OPERATIONS: | |||

|

Net investment income (loss) |

$ 3,547,575 | $ 3,378,717 | |

|

Net realized gain (loss) |

(3,070,131) | (16,810,908) | |

|

Net change in unrealized appreciation (depreciation) |

8,643,787 | (9,625,220) | |

|

Net increase (decrease) in net assets resulting from operations |

9,121,231 | (23,057,411) | |

| DISTRIBUTIONS TO SHAREHOLDERS FROM: | |||

|

Investment operations |

(3,293,675) | — | |

|

Return of capital |

(3,400,868) | (6,947,995) | |

|

Total distributions to shareholders |

(6,694,543) | (6,947,995) | |

| CAPITAL TRANSACTIONS: | |||

|

Proceeds from Common Shares reinvested |

— | 15,965 | |

|

Net increase (decrease) in net assets resulting from capital transactions |

— | 15,965 | |

|

Total increase (decrease) in net assets |

2,426,688 | (29,989,441) | |

| NET ASSETS: | |||

|

Beginning of period |

67,781,831 | 97,771,272 | |

|

End of period |

$ 70,208,519 | $ 67,781,831 | |

| CAPITAL TRANSACTIONS were as follows: | |||

|

Common Shares at beginning of period |

10,143,247 | 10,141,521 | |

|

Common Shares issued as reinvestment under the Dividend Reinvestment Plan |

— | 1,726 | |

|

Common Shares at end of period |

10,143,247 | 10,143,247 |

| Cash flows from operating activities: | ||

|

Net increase (decrease) in net assets resulting from operations |

$9,121,231 | |

| Adjustments to reconcile net increase (decrease) in net assets resulting from operations to net cash provided by operating activities: | ||

|

Purchases of investments |

(26,457,228) | |

|

Sales, maturities and paydown of investments |

37,940,337 | |

|

Net amortization/accretion of premiums/discounts on investments |

(657,683) | |

|

Net realized gain/loss on investments |

5,305,072 | |

|

Net change in unrealized appreciation/depreciation on investments |

(10,983,614) | |

|

Net change in unrealized appreciation/depreciation on forward foreign currency contracts |

(331,031) | |

| Changes in assets and liabilities: | ||

|

Increase in interest receivable |

(388,288) | |

|

Decrease in reclaims receivable |

22,112 | |

|

Decrease in due from broker |

370,000 | |

|

Decrease in prepaid expenses |

12,590 | |

|

Decrease in interest and fees payable on loan |

(31,675) | |

|

Decrease in due to broker |

(89,295) | |

|

Decrease in investment advisory fees payable |

(10,869) | |

|

Decrease in audit and tax fees payable |

(5,888) | |

|

Increase in legal fees payable |

19,606 | |

|

Decrease in shareholder reporting fees payable |

(609) | |

|

Increase in administrative fees payable |

3,082 | |

|

Increase in custodian fees payable |

10,307 | |

|

Decrease in transfer agent fees payable |

(1,589) | |

|

Increase in trustees’ fees and expenses payable |

55 | |

|

Decrease in deferred foreign capital gains tax |

(9,815) | |

|

Decrease in other liabilities payable |

(916) | |

|

Cash provided by operating activities |

$13,835,892 | |

| Cash flows from financing activities: | ||

|

Distributions to Common Shareholders from investment operations |

(3,293,675) | |

|

Distributions to Common Shareholders from return of capital |

(3,400,868) | |

|

Repayment of borrowing |

(13,350,835) | |

|

Effect of exchange rate changes on Euro Loans (a) |

(20,358) | |

|

Cash used in financing activities |

(20,065,736) | |

|

Decrease in cash and foreign currency (b) |

(6,229,844) | |

|

Cash and foreign currency at beginning of period |

7,205,503 | |

|

Cash, foreign currency, and restricted cash at end of period |

$975,659 | |

| Supplemental disclosure of cash flow information: | ||

|

Cash paid during the period for interest and fees |

$1,160,583 |

| (a) | This amount is a component of net change in unrealized appreciation (depreciation) on foreign currency translation as shown on the Statement of Operations. |

| (b) | Includes net change in unrealized appreciation (depreciation) on foreign currency of $(2,701,031), which does not include the effect of exchange rate changes on Euro borrowings. |

| Year Ended December 31, | |||||||||

| 2023 | 2022 | 2021 | 2020 | 2019 | |||||

|

Net asset value, beginning of period |

$ 6.68 | $ 9.64 | $ 11.37 | $ 11.93 | $ 11.07 | ||||

| Income from investment operations: | |||||||||

|

Net investment income (loss) |

0.35 (a) | 0.33 | 0.44 | 0.45 | 0.65 | ||||

|

Net realized and unrealized gain (loss) |

0.55 | (2.60) | (1.27) (b) | (0.06) | 1.09 | ||||

|

Total from investment operations |

0.90 | (2.27) | (0.83) | 0.39 | 1.74 | ||||

| Distributions paid to shareholders from: | |||||||||

|

Net investment income |

(0.32) | — | (0.30) | (0.42) | (0.39) | ||||

|

Return of capital |

(0.34) | (0.69) | (0.65) | (0.54) | (0.49) | ||||

|

Total distributions paid to Common Shareholders |

(0.66) | (0.69) | (0.95) | (0.96) | (0.88) | ||||

|

Common Share repurchases |

— | — | — | 0.01 | 0.00 (c) | ||||

|

Tender offer purchases |

— | — | 0.05 | — | — | ||||

|

Net asset value, end of period |

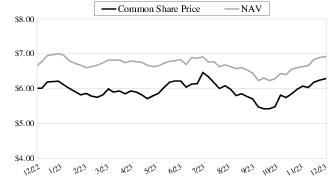

$ | $6.68 | $9.64 | $11.37 | $11.93 | ||||

|

Market value, end of period |

$ | $6.00 | $9.62 | $10.55 | $11.19 | ||||

|

Total return based on net asset value (d) |

15.69% | (23.23)% | (6.96)% (b) | 4.84% | 17.09% | ||||

|

Total return based on market value (d) |

17.08% | (30.91)% | 0.07% | 3.71% | 29.74% | ||||

| Ratios to average net assets/supplemental data: | |||||||||

|

Net assets, end of period (in 000’s) |

$ 70,209 | $ 67,782 | $ 97,771 | $ 144,094 | $ 152,154 | ||||

|

Ratio of total expenses to average net assets |

3.49% | 2.93% | 2.29% | 2.53% | 2.88% | ||||

|

Ratio of total expenses to average net assets excluding interest expense |

1.83% | 1.93% | 1.89% | 2.00% | 1.77% | ||||

|

Ratio of net investment income (loss) to average net assets |

5.23% | 4.57% | 4.53% | 4.13% | 5.60% | ||||

|

Portfolio turnover rate |

28% | 47% | 44% | 39% | 42% | ||||

| Indebtedness: | |||||||||

|

Total loan outstanding (in 000’s) |

$ 16,600 | $ 29,971 | $ 42,184 | $ 53,514 | $ 60,572 | ||||

|

Asset coverage per $1,000 of indebtedness (e) |

$ 5,229 | $ 3,262 | $ 3,318 | $ 3,693 | $ 3,512 | ||||

| (a) | Based on average shares outstanding. |

| (b) | The Fund received a reimbursement from the sub-advisor in the amount of $4,120 in connection with a trade error, which represents less than $0.01 per share. Since the sub-advisor reimbursed the Fund, there was no effect on the total return. |

| (c) | Amount represents less than $0.01. |

| (d) | Total return is based on the combination of reinvested dividend, capital gain and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan, and changes in net asset value per share for net asset value returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of future results. |

| (e) | Calculated by subtracting the Fund’s total liabilities (not including the loan outstanding) from the Fund’s total assets, and dividing by the outstanding loan balance in 000’s. |

| 1) | benchmark yields; |

| 2) | reported trades; |

| 3) | broker/dealer quotes; |

| 4) | issuer spreads; |

| 5) | benchmark securities; |

| 6) | bids and offers; and |

| 7) | reference data including market research publications. |

| 1) | the credit conditions in the relevant market and changes thereto; |

| 2) | the liquidity conditions in the relevant market and changes thereto; |

| 3) | the interest rate conditions in the relevant market and changes thereto (such as significant changes in interest rates); |

| 4) | issuer-specific conditions (such as significant credit deterioration); and |

| 5) | any other market-based data the Advisor’s Pricing Committee considers relevant. In this regard, the Advisor’s Pricing Committee may use last-obtained market-based data to assist it when valuing portfolio securities using amortized cost. |

| 1) | the most recent price provided by a pricing service; |

| 2) | available market prices for the fixed-income security; |

| 3) | the fundamental business data relating to the issuer, or economic data relating to the country of issue; |

| 4) | an evaluation of the forces which influence the market in which these securities are purchased and sold; |

| 5) | the type, size and cost of the security; |

| 6) | the financial statements of the issuer, or the financial condition of the country of issue; |

| 7) | the credit quality and cash flow of the issuer, or country of issue, based on abrdn Inc.’s (“abrdn” or the “Sub-Advisor”) or external analysis; |

| 8) | the information as to any transactions in or offers for the security; |

| 9) | the price and extent of public trading in similar securities (or equity securities) of the issuer, or comparable companies; |

| 10) | the coupon payments; |

| 11) | the quality, value and salability of collateral, if any, securing the security; |

| 12) | the business prospects of the issuer, including any ability to obtain money or resources from a parent or affiliate and an assessment of the issuer’s management (for corporate debt only); |

| 13) | the economic, political and social prospects/developments of the country of issue and the assessment of the country’s governmental leaders/officials (for sovereign debt only); |

| 14) | the prospects for the issuer’s industry, and multiples (of earnings and/or cash flows) being paid for similar businesses in that industry (for corporate debt only); and |

| 15) | other relevant factors. |

| • | Level 1 – Level 1 inputs are quoted prices in active markets for identical investments. An active market is a market in which transactions for the investment occur with sufficient frequency and volume to provide pricing information on an ongoing basis. |

| • | Level 2 – Level 2 inputs are observable inputs, either directly or indirectly, and include the following: |

| o | Quoted prices for similar investments in active markets. |

| o | Quoted prices for identical or similar investments in markets that are non-active. A non-active market is a market where there are few transactions for the investment, the prices are not current, or price quotations vary substantially either over time or among market makers, or in which little information is released publicly. |

| o | Inputs other than quoted prices that are observable for the investment (for example, interest rates and yield curves observable at commonly quoted intervals, volatilities, prepayment speeds, loss severities, credit risks, and default rates). |

| o | Inputs that are derived principally from or corroborated by observable market data by correlation or other means. |

| • | Level 3 – Level 3 inputs are unobservable inputs. Unobservable inputs may reflect the reporting entity’s own assumptions about the assumptions that market participants would use in pricing the investment. |

| Security | Acquisition Date |

Principal Value |

Current Price | Carrying Cost |

Value | %

of Net Assets | ||

| OAS Finance Ltd., 8.88% | 4/18/2013 | $1,550,000 | $0.75 | $1,550,000 | $11,625 | 0.02% | ||

| OAS Investments GmbH, 8.25%, 10/19/19 | 10/12/2012 | 460,000 | 0.75 | 460,000 | 3,450 | 0.01 | ||

| Sovcombank Via SovCom Capital DAC, 7.75% | 2/19/2020 | 500,000 | 1.91 | 511,643 | 9,540 | 0.01 | ||

| $2,521,643 | $24,615 | 0.04% |

| Gross

Amounts not Offset in the Statement of Assets and Liabilities |

|||||||||||

| Gross Amounts of Recognized Assets |

Gross

Amounts Offset in the Statement of Assets and Liabilities |

Net

Amounts of Assets Presented in the Statement of Assets and Liabilities |

Financial Instruments |

Collateral Amounts Received |

Net Amount | ||||||

| Forward

Foreign Currency Contracts* |

$ 138,138 | $ — | $ 138,138 | $ (59,142) | $ — | $ 78,966 | |||||

| Gross

Amounts not Offset in the Statement of Assets and Liabilities |

|||||||||||

| Gross Amounts of Recognized Liabilities |

Gross

Amounts Offset in the Statement of Assets and Liabilities |

Net

Amounts of Liabilities Presented in the Statement of Assets and Liabilities |

Financial Instruments |

Collateral Amounts Pledged |

Net Amount | ||||||

| Forward Foreign Currency Contracts* | $ (452,445) | $ — | $ (452,445) | $ 59,142 | $ — | $ (393,303) | |||||

| Distributions paid from: | 2023 | 2022 |

|

Ordinary income |

$3,293,675 | $— |

|

Capital gains |

— | — |

|

Return of capital |

3,400,868 | 6,947,995 |

|

Undistributed ordinary income |

$— |

|

Undistributed capital gains |

— |

|

Total undistributed earnings |

— |

|

Accumulated capital and other losses |

(27,834,759) |

|

Net unrealized appreciation (depreciation) |

(9,415,168) |

|

Total accumulated earnings (losses) |

(37,249,927) |

|

Other |

(126,171) |

|

Paid-in capital |

107,584,617 |

|

Total net assets |

$70,208,519 |

| Tax Cost | Gross Unrealized Appreciation |

Gross Unrealized (Depreciation) |

Net

Unrealized Appreciation (Depreciation) | |||

| $93,576,632 | $2,310,148 | $(11,735,509) | $(9,425,361) |

| Asset Derivatives | Liability Derivatives | |||||||||

| Derivative Instrument |

Risk Exposure |

Statement

of Assets and Liabilities Location |

Value | Statement

of Assets and Liabilities Location |

Value | |||||

| Forward

foreign currency contracts |

Currency Risk | Unrealized

appreciation on forward foreign currency contracts |

$ 138,138 | Unrealized

depreciation on forward foreign currency contracts |

$ 452,445 | |||||

| Statement of Operations Location | |

| Currency Risk Exposure | |

| Net realized gain (loss) on forward foreign currency contracts | $(849,870) |

| Net change in unrealized appreciation (depreciation) on forward foreign currency contracts | 331,031 |

| (1) | If Common Shares are trading at or above net asset value (“NAV”) at the time of valuation, the Fund will issue new shares at a price equal to the greater of (i) NAV per Common Share on that date or (ii) 95% of the market price on that date. |

| (2) | If Common Shares are trading below NAV at the time of valuation, the Plan Agent will receive the dividend or distribution in cash and will purchase Common Shares in the open market, on the NYSE or elsewhere, for the participants’ accounts. It is possible that the market price for the Common Shares may increase before the Plan Agent has completed its purchases. Therefore, the average purchase price per share paid by the Plan Agent may exceed the market price at the time of valuation, resulting in the purchase of fewer shares than if the dividend or distribution had been paid in Common Shares issued by the Fund. The Plan Agent will use all dividends and distributions received in cash to purchase Common Shares in the open market within 30 days of the valuation date except where temporary curtailment or suspension of purchases is necessary to comply with federal securities laws. Interest will not be paid on any uninvested cash payments. |

| • | May invest up to 40% of its Managed Assets in corporate debt obligations. |

| o | Corporate debt bonds generally are used by corporations to borrow money from investors. The issuer pays the investor a fixed or variable rate of interest and normally must repay the amount borrowed on or before maturity. Certain corporate bonds are “perpetual” in that they have no maturity date. The Fund may invest in non-U.S. corporate bonds which involve unique risks compared to investing in the securities of U.S. issuers. |

| • | May invest up to 60% of its Managed Assets in securities rated below “Baa3” by Moody’s Investment Service, inc. (“Moody’s”) below “BBB-” by Standard & Poor’s Corporation, a division of The McGraw-Hill Companies (“S&P”), or comparably rated by another nationally recognized statistical rating organization or, if unrated, determined by the Sub-Advisor to be of comparable credit quality. |

| o | The Fund may invest in high yield securities of any rating. However, the Fund will not invest more than 15% of its Managed Assets in securities rated below “B-” by Moody’s and/or S& P. |

| • | May invest up to 15% of its Managed Assets in asset-backed securities. |

| o | Asset-backed securities are securities that represent a participation in, or are secured by and payable from, a stream of payments generated by particular assets, most often a pool or pools of similar assets (e.g., trade receivables). The credit quality of these securities depends primarily upon the quality of the underlying assets and the level of credit support and/or enhancement provided. The underlying assets (e.g., loans) are subject to prepayments which shorten the securities’ weighted average maturity and may lower their return. Losses or delays in payment may result if the credit support or enhancement is exhausted because the required payments of principal and interest on the underlying assets |

| are not made. The value of these securities may also change because of changes in the market’s perception of the creditworthiness of the servicing agent for the pool, the originator of the pool or the financial institution or fund providing the credit support or enhancement. |

| • | May invest up to 35% of its Managed Assets in credit linked notes (“Credit Linked Notes”), provided such securities are issued by an institution with at least an “A” credit rating by Moody’s and/or S&P. |

| o | Credit Linked Notes are structured securities typically issued by banks whose principal and interest payments are contingent on the performance of a specified borrower company or companies (the “Reference Issuer”). Credit Linked Notes are created by embedding a credit default swap in a funded asset to form an investment whose credit risk and cash flow characteristics resemble those of a bond or loan. These notes pay an enhanced coupon to the investor for taking on the added credit risk of the Reference Issuer. |

| • | May invest up to 10% of its Managed Assets in securities that, at the time of investment, are illiquid (i.e., securities that cannot be disposed of within seven days in the ordinary course of business at approximately the value at which the Fund has valued the securities). The Fund may also invest, without limit, in securities that are unregistered (but are eligible for purchase and sale by certain qualified institutional buyers) or are held by control persons of the issuer and securities that are subject to contractual restrictions on their resale (“restricted securities”). However, restricted securities determined by the Sub-Advisor, under the supervision of the Board of Trustees, to be illiquid are subject to the limitations set forth above. |

| • | May invest up to 5% of its Managed Assets in non-deliverable forward foreign exchange contracts for purposes of hedging. |

| • | May invest up to 10% of its Managed Assets in forward foreign exchange contracts (both deliverable and non-deliverable). |

| • | Interest Rate Risk. Interest rate risk is the risk that securities will decline in value because of changes in market interest rates. For fixed rate securities, when market interest rates rise, the market value of such securities generally will fall. Investments in fixed rate securities with long-term maturities may experience significant price declines if long-term interest rates increase. During periods of rising interest rates, the average life of certain types of securities may be extended because of slower than expected prepayments. This may lock in a below-market yield, increase the security’s duration and further reduce the value of the security. Fixed rate securities with longer durations tend to be more sensitive to changes in interest rates, usually making them more volatile than securities with shorter durations. |

| • | Issuer Risk. The value of fixed income securities may decline for a number of reasons which directly relate to the issuer, such as management performance, leverage and reduced demand for the issuer’s goods and services. |

| • | Prepayment Risk. Prepayment risk is the risk that the issuer of a debt security will repay principal prior to the scheduled maturity date. During periods of declining interest rates, the issuer of a security may exercise its option to prepay principal earlier than scheduled, forcing the Fund to reinvest the proceeds from such prepayment in lower yielding securities, which may result in a decline in the Fund’s income and distributions to common shareholders. |

| • | Reinvestment Risk. Reinvestment risk is the risk that income from the Fund’s portfolio will decline if the Fund invests the proceeds from matured, traded or called securities at market interest rates that are below the Fund portfolio’s current earnings rate. Similarly, the yield-to-maturity of a security assumes that all coupons are reinvested at the prevailing rate. If rates fall, the actual yield realized on the security may be lower as the security’s coupons are reinvested at lower yields. |

| NOT FDIC INSURED | NOT BANK GUARANTEED | MAY LOSE VALUE |

|

Assumed Portfolio Total Return (Net of Expenses) |

-10% | -5% | 0% | 5% | 10% |

|

Common Share Total Return |

- |

- |

- |

| Name, Year of Birth and Position with the Fund | Term of Office and Year First Elected or Appointed(1) | Principal

Occupations During Past 5 Years |

Number of Portfolios in the First Trust Fund Complex Overseen by Trustee | Other Trusteeships or Directorships Held by Trustee During Past 5 Years |

| INDEPENDENT TRUSTEES | ||||

| Richard

E. Erickson, Trustee (1951) |

• Three Year Term• Since Fund Inception | Retired; Physician, Edward-Elmhurst Medical Group (2021 to September 2023); Physician and Officer, Wheaton Orthopedics (1990 to 2021) | 257 | None |

| Thomas

R. Kadlec, Trustee (1957) |

• Three Year Term• Since Fund Inception | Retired; President, ADM Investor Services, Inc. (Futures Commission Merchant) (2010 to July 2022) | 257 | Director, National Futures Association and ADMIS Singapore Ltd.; Formerly, Director of ADM Investor Services, Inc., ADM Investor Services International, ADMIS Hong Kong Ltd., and Futures Industry Association |

| Denise

M. Keefe, Trustee (1964) |

• Three Year Term• Since 2021 | Executive Vice President, Advocate Aurora Health and President, Advocate Aurora Continuing Health Division (Integrated Healthcare System) | 257 | Director and Board Chair of Advocate Home Health Services, Advocate Home Care Products and Advocate Hospice; Director and Board Chair of Aurora At Home (since 2018); Director of Advocate Physician Partners Accountable Care Organization; Director of RML Long Term Acute Care Hospitals; Director of Senior Helpers (since 2021); and Director of MobileHelp (since 2022) |

| Robert

F. Keith, Trustee (1956) |

• Three Year Term• Since Fund Inception | President, Hibs Enterprises (Financial and Management Consulting) | 257 | Formerly, Director of Trust Company of Illinois |

| Niel

B. Nielson, Trustee (1954) |

• Three Year Term• Since Fund Inception | Senior Advisor (2018 to Present), Managing Director and Chief Operating Officer (2015 to 2018), Pelita Harapan Educational Foundation (Educational Products and Services) | 257 | None |

| (1) | Currently, Richard E. Erickson and Thomas R. Kadlec, as Class II Trustees, are serving as trustees until the Fund’s 2024 annual meeting of shareholders. James A. Bowen, Niel B. Nielson, and Bronwyn Wright as Class III Trustees, are serving as trustees until the Fund’s 2025 annual meeting of shareholders. Denise M. Keefe and Robert F. Keith, as Class I Trustees, are serving as trustees until the Fund’s 2026 annual meeting of shareholders. |

| Name, Year of Birth and Position with the Fund | Term of Office and Year First Elected or Appointed(1) | Principal

Occupations During Past 5 Years |

Number of Portfolios in the First Trust Fund Complex Overseen by Trustee | Other Trusteeships or Directorships Held by Trustee During Past 5 Years |

| INDEPENDENT TRUSTEES | ||||

| Bronwyn

Wright, Trustee (1971) |

• Three Year Term• Since 2023 | Independent Director to a number of Irish collective investment funds (2009 to Present); Various roles at international affiliates of Citibank (1994 to 2009), including Managing Director, Citibank Europe plc and Head of Securities and Fund Services, Citi Ireland (2007 to 2009) | 233 | None |

| INTERESTED TRUSTEE | ||||

| James

A. Bowen(2), Trustee and Chairman of the Board (1955) |

• Three Year Term• Since Fund Inception | Chief Executive Officer, First Trust Advisors L.P. and First Trust Portfolios L.P.; Chairman of the Board of Directors, BondWave LLC (Software Development Company) and Stonebridge Advisors LLC (Investment Advisor) | 257 | None |

| Name and Year of Birth | Position and Offices with Fund | Term of Office and Length of Service | Principal

Occupations During Past 5 Years |

| OFFICERS(3) | |||

| James

M. Dykas (1966) |

President and Chief Executive Officer | • Indefinite

Term • Since 2016 |

Managing Director and Chief Financial Officer, First Trust Advisors L.P. and First Trust Portfolios L.P.; Chief Financial Officer, BondWave LLC (Software Development Company) and Stonebridge Advisors LLC (Investment Advisor) |

| Derek

D. Maltbie (1972) |

Treasurer, Chief Financial Officer and Chief Accounting Officer | • Indefinite

Term • Since 2023 |

Senior Vice President, First Trust Advisors L.P. and First Trust Portfolios L.P., July 2021 to Present. Previously, Vice President, First Trust Advisors L.P. and First Trust Portfolios L.P., 2014 to 2021. |

| W.

Scott Jardine (1960) |

Secretary and Chief Legal Officer | • Indefinite

Term • Since Fund Inception |

General Counsel, First Trust Advisors L.P. and First Trust Portfolios L.P.; Secretary and General Counsel, BondWave LLC; Secretary, Stonebridge Advisors LLC |

| Daniel

J. Lindquist (1970) |

Vice President | • Indefinite

Term • Since December 2005 |

Managing Director, First Trust Advisors L.P. and First Trust Portfolios L.P. |

| Kristi

A. Maher (1966) |

Chief Compliance Officer and Assistant Secretary | •

Indefinite Term • Chief Compliance Officer Since January 2011• Assistant Secretary Since Fund Inception |

Deputy General Counsel, First Trust Advisors L.P. and First Trust Portfolios L.P. |

| (2) | Mr. Bowen is deemed an “interested person” of the Fund due to his position as CEO of First Trust Advisors L.P., investment advisor of the Fund. |

| (3) | The term “officer” means the president, vice president, secretary, treasurer, controller or any other officer who performs a policy making function. |

| • | Information we receive from you and your broker-dealer, investment professional or financial representative through interviews, applications, agreements or other forms; |

| • | Information about your transactions with us, our affiliates or others; |

| • | Information we receive from your inquiries by mail, e-mail or telephone; and |

| • | Information we collect on our website through the use of “cookies.” For example, we may identify the pages on our website that your browser requests or visits. |

| • | In order to provide you with products and services and to effect transactions that you request or authorize, we may disclose your personal information as described above to unaffiliated financial service providers and other companies that perform administrative or other services on our behalf, such as transfer agents, custodians and trustees, or that assist us in the distribution of investor materials such as trustees, banks, financial representatives, proxy services, solicitors and printers. |

| • | We may release information we have about you if you direct us to do so, if we are compelled by law to do so, or in other legally limited circumstances (for example to protect your account from fraud). |

(b) Not applicable.

Item 2. Code of Ethics.

| (a) | The registrant, as of the end of the period covered by this report, has adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party. |

| (c) | There have been no amendments, during the period covered by this report, to a provision of the code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party, and that relates to any element of the code of ethics description. |

| (d) | The registrant has not granted any waivers, including an implicit waiver, from a provision of the code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party, that relates to one or more of the items set forth in paragraph (b) of this item’s instructions. |

| (e) | Not applicable. |

| (f) | A copy of the code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller is filed as an exhibit pursuant to Item 13(a)(1). |

Item 3. Audit Committee Financial Expert.

As of the end of the period covered by the report, the registrant’s board of trustees has determined that Thomas R. Kadlec, Robert F. Keith and Bronwyn Wright are qualified to serve as audit committee financial experts serving on its audit committee and that each of them is “independent,” as defined by Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

(a) Audit Fees (Registrant) — The aggregate fees billed for each of the last two fiscal years for professional services rendered by the principal accountant for the audit of the registrant’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements were $55,000 for 2022 and $55,000 for 2023.

(b) Audit-Related Fees (Registrant) — The aggregate fees billed in each of the last two fiscal years, for assurance and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant’s financial statements and are not reported under paragraph (a) of this Item were $0 for 2022 and $0 for 2023.

Audit-Related Fees (Investment Advisor) — The aggregate fees billed in each of the last two fiscal years of the registrant for assurance and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant’s financial statements and are not reported under paragraph (a) of this Item were $0 for 2022 and $0 for 2023.

(c) Tax Fees (Registrant) — The aggregate fees billed in each of the last two fiscal years for professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning to the registrant were 16,250 for 2022 and $21,000 for 2023. These fees were for tax consultation and/or tax return preparation.

Tax Fees (Investment Advisor) — The aggregate fees billed in each of the last two fiscal years of the registrant for professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning to the registrant’s advisor were $0 for 2022 and $0 for 2023.

(d) All Other Fees (Registrant) — The aggregate fees billed in each of the last two fiscal years for products and services provided by the principal accountant to the registrant, other than the services reported in paragraphs (a) through (c) of this Item were $0 for 2022 and $0 for 2023.

All Other Fees (Investment Advisor) — The aggregate fees billed in each of the last two fiscal years for products and services provided by the principal accountant to the registrant’s investment advisor, other than services reported in paragraphs (a) through (c) of this Item were $0 for 2022 and $0 for 2023.

| (e)(1) | Disclose the audit committee’s pre-approval policies and procedures described in paragraph (c)(7) of Rule 2-01 of Regulation S-X. |

Pursuant to its charter and its Audit and Non-Audit Services Pre-Approval Policy, the Audit Committee (the “Committee”) is responsible for the pre-approval of all audit services and permitted non-audit services (including the fees and terms thereof) to be performed for the registrant by its independent auditors. The Chairman of the Committee is authorized to give such pre-approvals on behalf of the Committee up to $25,000 and report any such pre-approval to the full Committee.

The Committee is also responsible for the pre-approval of the independent auditor’s engagements for non-audit services with the registrant’s advisor (not including a sub-advisor whose role is primarily portfolio management and is sub-contracted or overseen by another investment advisor) and any entity controlling, controlled by or under common control with the investment advisor that provides ongoing services to the registrant, if the engagement relates directly to the operations and financial reporting of the registrant, subject to the de minimis exceptions for non-audit services described in Rule 2-01 of Regulation S-X. If the independent auditor has provided non-audit services to the registrant’s advisor (other than any sub-advisor whose role is primarily portfolio management and is sub-contracted with or overseen by another investment advisor) and any entity controlling, controlled by or under common control with the investment advisor that provides ongoing services to the registrant that were not pre-approved pursuant to its policies, the Committee will consider whether the provision of such non-audit services is compatible with the auditor’s independence.

| (e)(2) | The percentage of services described in each of paragraphs (b) through (d) for the registrant and the registrant’s investment advisor of this Item that were approved by the audit committee pursuant to the pre-approval exceptions included in paragraph (c)(7)(i)(c) or paragraph (c)(7)(ii) of Rule 2-01 of Regulation S-X are as follows: |

(b) 0%

(c) 0%

(d) 0%

| (f) | The percentage of hours expended on the principal accountant’s engagement to audit the registrant’s financial statements for the most recent fiscal year that were attributed to work performed by persons other than the principal accountant’s full-time, permanent employees was less than fifty percent. |

| (g) | The aggregate non-audit fees billed by the registrant’s accountant for services rendered to the registrant, and rendered to the registrant’s investment advisor (not including any sub-advisor whose role is primarily portfolio management and is subcontracted with or overseen by another investment advisor), and any entity controlling, controlled by, or under common control with the advisor that provides ongoing services to the registrant for 2022 were $16,250 and $0 for the registrant and the registrant’s investment advisor, respectively and for 2023 were $21,000 and $44,000 for the registrant and the registrant’s investment advisor, respectively. |

| (h) | The registrant’s audit committee of its Board of Trustees determined that the provision of non-audit services that were rendered to the Registrant’s investment advisor (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment advisor), and any entity controlling, controlled by, or under common control with the investment advisor that provides ongoing services to the registrant that were not pre-approved pursuant to paragraph (c)(7)(ii) of Rule 2-01 of Regulation S-X is compatible with maintaining the principal accountant’s independence. |

Item 5. Audit Committee of Listed Registrants.

| (a) | The registrant has a separately designated audit committee consisting of all the independent trustees of the registrant. The members of the audit committee are: Thomas R. Kadlec, Niel B. Nielson, Denise M. Keefe, Richard E. Erickson and Robert F. Keith. |

Item 6. Investments.

| (a) | Schedule of Investments in securities of unaffiliated issuers as of the close of the reporting period is included as part of the report to shareholders filed under Item 1 of this form. |

| (b) | Not applicable. |

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

A description of the policies and procedures used to vote proxies on behalf of the Fund is attached as an exhibit.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

(a)(1) Identification of Portfolio Manager(s) or Management Team Members and Description of Role of Portfolio Manager(s) or Management Team Members

Information provided as of March 8, 2024

abrdn Inc. (“abrdn” or the “Sub-Advisor”), a Securities and Exchange Commission registered investment advisor, is an indirect wholly-owned subsidiary of abrdn plc. abrdn plc is a publicly-traded global provider of long-term savings and investments listed on the London Stock Exchange, managing assets for institutional and retail clients from offices around the world. Investment decisions for the Fund are made by abrdn using a team approach and not by any one individual. By making team decisions, abrdn seeks to ensure that the investment process results in consistent returns across all portfolios with similar objectives. abrdn does not employ separate research analysts. Instead, abrdn’s investment managers combine analysis with portfolio management. Each member of the team has sector and portfolio responsibilities such as day-to-day monitoring of liquidity. The overall result of this matrix approach is a high degree of cross-coverage, leading to a deeper understanding of the securities in which abrdn invests. Below are the members of the team with significant responsibility for the day-to-day management of the Fund’s portfolio.

Brett Diment

Head of Global Emerging Market Debt

Mr. Diment is the Head of Global Emerging Market Debt and joined abrdn following the acquisition of Deutsche Asset Management (“Deutsche”) in 2005. He is responsible for the day-to-day management of the Emerging Market Debt Team and portfolios. Mr. Diment had been at Deutsche since 1991 as a member of the Fixed Income group and served as Head of the Emerging Debt Team there from 1999 until its acquisition by abrdn.

Max Wolman

Investment Director, Emerging Market Debt

Mr. Wolman is an Investment Director on the Emerging Market Debt Team and has been with abrdn since January 2001. Mr. Wolman originally specialized in currency and domestic debt analysis but is now responsible for a wide range of emerging debt analysis including external and corporate issuers. Mr. Wolman is a member of the Emerging Market Debt Investment Committee at abrdn and is also responsible for the daily implementation of the investment process.

Edwin Gutierrez

Head of Emerging Market Sovereign Debt

Mr. Gutierrez is the Head of Emerging Market Sovereign Debt. Mr. Gutierrez joined abrdn via the acquisition of Deutsche Asset Management's London and Philadelphia fixed income businesses in 2005, where he held the same role since joining Deutsche in 2000.

Aaron Rock

Head of Nominal Rates, Rates Management

Mr. Rock was appointed Head of Nominal Rates in October 2023 and took on the lead management role for the Global Government Bond funds. Prior to that he was an Investment Director within the Rates & Inflation team. Mr. Rock joined abrdn via the acquisition of Ignis Asset Management in 2014.

Kevin Daly

Investment Director, Emerging Markets Debt

Mr. Daly is an Investment Director on the Emerging Market Debt team and joined abrdn in 2007. Prior to joining abrdn, Mr. Daly worked at Standard & Poor’s in London and Singapore where he was as a Credit Market Analyst covering global emerging debt.

| (a)(2) | Other Accounts Managed by Portfolio Manager(s) or Management Team Member and Potential Conflicts of Interest |

Other Accounts Managed by Portfolio Manager(s) or Management Team Member

Information provided as of December 31, 2023

Name of Portfolio Manager or Team Member |

Type of Accounts*** |

|

Assets |

#

of Accounts Managed for which Advisory Fee is Based on Performance |

Total Assets

for |

| 1. Brett Diment | Registered Investment Companies: | 1 | $184,941,858.95 | 0 | $0 |

| Other Pooled Investment Vehicles: | 21 | $4,185,445,579 | 0 | $0 | |

| Other Accounts: | 14 | $8,603,416,051 | 0 | $0 | |

| 2. Max Wolman | Registered Investment Companies: | 1 | $184,941,858.95 | 0 | $0 |

| Other Pooled Investment Vehicles: | 21 | $4,185,445,579 | 0 | $0 | |

| Other Accounts: | 14 | $8,603,416,051 | 0 | $0 | |

| 3. Edwin Gutierrez | Registered Investment Companies: | 1 | $184,941,858.95 | 0 | $0 |

| Other Pooled Investment Vehicles: | 21 | $4,185,445,579 | 0 | $0 | |

| Other Accounts: | 14 | $4,961,920,964 | 0 | $0 | |

| 4. Kevin Daly | Registered Investment Companies: | 1 | $184,941,858.95 | 0 | $0 |

| Other Pooled Investment Vehicles: | 21 | $4,185,445,579 | 0 | $0 | |

| Other Accounts: | 14 | $8,603,416,051 | 0 | $0 | |

| 5. Aaron | Registered Investment Companies: | 0 | $0 | 0 | $0 |

| Other Pooled Investment Vehicles: | 0 | $ | 0 | $0 | |

| Other Accounts: | 21 | $11,999,013,163 | 0 | $0 |

Potential Conflicts of Interests

As of December 31, 2022

CONFLICTS OF INTEREST

Conflicts of Interest may arise, in the course of providing a service, where there may be a risk of damage to the interests of a client. In accordance with legal requirements in the various jurisdictions in which we operate, abrdn have in place arrangements to identify and manage Conflicts of Interest that may arise between them and their clients or between their different clients. Where abrdn does not consider that these arrangements are sufficient to manage a particular conflict, it will inform the relevant client(s) of the nature of the conflict so that the client(s) may decide how to proceed.

abrdn or any other party to whom it may have delegated its functions, may in its absolute discretion, effect transactions in which it or any of its affiliated companies has, directly or indirectly, a material interest, or a relationship of any description with another party which may involve a potential conflict with abrdn’s duty to its client. abrdn ensures that such transactions are effected on terms which are not materially less favorable to the client than if the potential conflict had not existed.

Such potential conflicting interests or duties may, inter alia, arise because:

| • | abrdn or an affiliated company undertakes an activity that is regulated by a relevant regulator for other clients including its affiliated companies (and the clients of affiliated companies) |

| • | a Director or Employee of abrdn, or of an affiliated company, is a director of, holds or deals in securities of, or is otherwise interested in, any company whose securities are held or dealt in on behalf of a client |

| • | a transaction is effected in securities issued by an affiliated company or the client of an affiliated company |

| • | a transaction is effected in securities in respect of which abrdn or an affiliated company may benefit from a commission, fee, mark-up or mark-down payable otherwise than by the client, and abrdn may be remunerated by the counterparty to any such transaction |

| • | abrdn deals on behalf of the client with, or in the securities of, an affiliated company |

| • | abrdn acts as agent for the client in relation to transactions in which it is also acting as agent for the account of other clients and/or affiliated companies |

| • | abrdn, acting as principal, sells to or purchases currency from the client and, in exceptional circumstances, deals in securities as principal with the client |