false

FY

0001961847

http://fasb.org/us-gaap/2024#UsefulLifeTermOfLeaseMember

0001961847

2023-10-01

2024-09-30

0001961847

2024-03-31

0001961847

2024-12-03

0001961847

2022-10-01

2023-09-30

0001961847

2024-09-30

0001961847

2023-09-30

0001961847

us-gaap:NonrelatedPartyMember

2024-09-30

0001961847

us-gaap:NonrelatedPartyMember

2023-09-30

0001961847

us-gaap:RelatedPartyMember

2024-09-30

0001961847

us-gaap:RelatedPartyMember

2023-09-30

0001961847

us-gaap:ProductMember

2023-10-01

2024-09-30

0001961847

us-gaap:ProductMember

2022-10-01

2023-09-30

0001961847

us-gaap:ServiceMember

2023-10-01

2024-09-30

0001961847

us-gaap:ServiceMember

2022-10-01

2023-09-30

0001961847

INHD:LicensingIncomeMember

2023-10-01

2024-09-30

0001961847

INHD:LicensingIncomeMember

2022-10-01

2023-09-30

0001961847

us-gaap:CommonStockMember

2022-09-30

0001961847

us-gaap:AdditionalPaidInCapitalMember

2022-09-30

0001961847

us-gaap:RetainedEarningsMember

2022-09-30

0001961847

us-gaap:NoncontrollingInterestMember

2022-09-30

0001961847

2022-09-30

0001961847

us-gaap:CommonStockMember

2023-09-30

0001961847

us-gaap:AdditionalPaidInCapitalMember

2023-09-30

0001961847

us-gaap:RetainedEarningsMember

2023-09-30

0001961847

us-gaap:NoncontrollingInterestMember

2023-09-30

0001961847

us-gaap:CommonStockMember

2022-10-01

2023-09-30

0001961847

us-gaap:AdditionalPaidInCapitalMember

2022-10-01

2023-09-30

0001961847

us-gaap:RetainedEarningsMember

2022-10-01

2023-09-30

0001961847

us-gaap:NoncontrollingInterestMember

2022-10-01

2023-09-30

0001961847

us-gaap:CommonStockMember

2023-10-01

2024-09-30

0001961847

us-gaap:AdditionalPaidInCapitalMember

2023-10-01

2024-09-30

0001961847

us-gaap:RetainedEarningsMember

2023-10-01

2024-09-30

0001961847

us-gaap:NoncontrollingInterestMember

2023-10-01

2024-09-30

0001961847

us-gaap:CommonStockMember

2024-09-30

0001961847

us-gaap:AdditionalPaidInCapitalMember

2024-09-30

0001961847

us-gaap:RetainedEarningsMember

2024-09-30

0001961847

us-gaap:NoncontrollingInterestMember

2024-09-30

0001961847

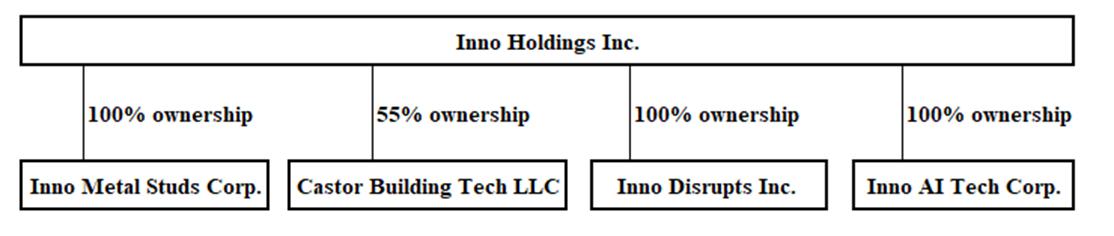

INHD:CastorBuildingTechLLCMember

2022-01-18

0001961847

INHD:CastorBuildingTechLLCMember

INHD:NewOwnershipAgreementMember

2023-10-16

0001961847

INHD:InnoMetalStudsCorpMember

2022-01-21

0001961847

INHD:MrDekuiLiuMember

2022-01-21

2022-01-21

0001961847

INHD:MrDekuiLiuMember

INHD:InnoMetalStudsCorpMember

2022-01-21

0001961847

INHD:InnoResearchInstituteLLCMember

INHD:InnoMetalStudsCorpMember

2021-09-08

0001961847

2024-01-27

2024-01-27

0001961847

2022-11-30

2022-11-30

0001961847

2023-07-23

0001961847

2023-07-24

0001961847

us-gaap:SubsequentEventMember

2024-10-09

2024-10-09

0001961847

us-gaap:MachineryAndEquipmentMember

2024-09-30

0001961847

us-gaap:OfficeEquipmentMember

2024-09-30

0001961847

us-gaap:VehiclesMember

2024-09-30

0001961847

us-gaap:LeaseholdImprovementsMember

2024-09-30

0001961847

us-gaap:MachineryAndEquipmentMember

2023-09-30

0001961847

us-gaap:OfficeEquipmentMember

2023-09-30

0001961847

us-gaap:VehiclesMember

2023-09-30

0001961847

us-gaap:ConstructionInProgressMember

2024-09-30

0001961847

us-gaap:ConstructionInProgressMember

2023-09-30

0001961847

us-gaap:LeaseholdImprovementsMember

2023-09-30

0001961847

2022-09-16

0001961847

us-gaap:LineOfCreditMember

2023-10-01

2024-09-30

0001961847

us-gaap:LineOfCreditMember

2022-10-01

2023-09-30

0001961847

INHD:ThreeIndividualsMember

2023-06-01

2023-08-31

0001961847

INHD:IndividualsMember

2024-09-30

0001961847

INHD:IndividualsMember

2023-09-30

0001961847

2021-10-28

0001961847

2021-11-28

2021-11-28

0001961847

2021-10-28

2021-10-28

0001961847

INHD:MrDekuiLiuMember

2024-09-30

0001961847

INHD:MrDekuiLiuMember

2023-09-30

0001961847

INHD:InnoResearchInstituteMember

2022-10-01

2023-09-30

0001961847

INHD:YunitedAssetsLLCMember

2022-10-01

2023-09-30

0001961847

INHD:YunitedAssetsLLCMember

2024-09-30

0001961847

INHD:YunitedAssetsLLCMember

2023-09-30

0001961847

INHD:BaichengTradingLLCMember

2023-10-01

2024-09-30

0001961847

INHD:BaichengTradingLLCMember

2024-09-30

0001961847

INHD:BaichengTradingLLCMember

2023-09-30

0001961847

INHD:ZfounderOrganizationIncMember

2023-09-30

0001961847

INHD:WiseHillIncMember

2023-09-30

0001961847

INHD:VisionOpportunityFundLPMember

2023-03-01

2023-03-31

0001961847

INHD:VisionOpportunityFundLPMember

2024-09-30

0001961847

INHD:VisionOpportunityFundLPMember

2023-10-01

2024-09-30

0001961847

2021-09-08

0001961847

us-gaap:CommonStockMember

us-gaap:InvestorMember

2022-12-01

2022-12-31

0001961847

us-gaap:CommonStockMember

us-gaap:InvestorMember

2022-12-31

0001961847

us-gaap:CommonStockMember

us-gaap:InvestorMember

2023-02-01

2023-02-28

0001961847

us-gaap:CommonStockMember

us-gaap:InvestorMember

2023-02-28

0001961847

us-gaap:CommonStockMember

us-gaap:InvestorMember

2023-03-01

2023-03-31

0001961847

us-gaap:CommonStockMember

us-gaap:InvestorMember

2023-03-31

0001961847

srt:ChiefFinancialOfficerMember

2023-06-20

2023-06-20

0001961847

INHD:OneNonemployeeContractorMember

2023-06-20

2023-06-20

0001961847

2023-06-20

0001961847

INHD:OneNonemployeeContractorMember

2024-01-01

2024-01-01

0001961847

us-gaap:IPOMember

2023-12-18

0001961847

us-gaap:IPOMember

2023-12-18

2023-12-18

0001961847

srt:MaximumMember

2024-09-30

0001961847

INHD:WarrantAssumptionAgreementMember

2024-03-01

0001961847

INHD:WarrantAssumptionAgreementMember

2024-03-01

2024-03-01

0001961847

INHD:WarrantAssumptionAgreementMember

2024-09-30

0001961847

2024-03-01

2024-03-01

0001961847

2023-12-19

2023-12-19

0001961847

srt:MaximumMember

2023-09-30

0001961847

us-gaap:CustomerConcentrationRiskMember

us-gaap:SalesRevenueNetMember

INHD:FourCustomersMember

2023-10-01

2024-09-30

0001961847

us-gaap:CustomerConcentrationRiskMember

us-gaap:SalesRevenueNetMember

INHD:ThreeCustomersMember

2022-10-01

2023-09-30

0001961847

us-gaap:CustomerConcentrationRiskMember

us-gaap:AccountsReceivableMember

INHD:OneCustomerMember

2022-10-01

2023-09-30

0001961847

us-gaap:SupplierConcentrationRiskMember

us-gaap:CostOfGoodsTotalMember

INHD:TwoSuppliersMember

2023-10-01

2024-09-30

0001961847

us-gaap:SupplierConcentrationRiskMember

us-gaap:CostOfGoodsTotalMember

INHD:ThreeSuppliersMember

2022-10-01

2023-09-30

0001961847

us-gaap:SupplierConcentrationRiskMember

us-gaap:AccountsPayableMember

INHD:TwoSuppliersMember

2023-10-01

2024-09-30

0001961847

us-gaap:SupplierConcentrationRiskMember

us-gaap:AccountsPayableMember

INHD:TwoSuppliersMember

2022-10-01

2023-09-30

0001961847

srt:MinimumMember

INHD:DecemberOneTwoThousandNineteenAndDecemberThirtyOneTwoThousandAndTwentyFourMember

2023-10-01

2024-09-30

0001961847

srt:MaximumMember

INHD:DecemberOneTwoThousandNineteenAndDecemberThirtyOneTwoThousandAndTwentyFourMember

2023-10-01

2024-09-30

0001961847

INHD:JanuaryOneTwoThousandTwentyFourAndTwoThousandTwentySevenMember

2024-01-01

2024-01-01

0001961847

2024-01-01

0001961847

srt:MinimumMember

INHD:MayOneTwoThousandAndTwentyTwoAndAprilThirtyTwoThousandAndTwentySevenMember

2023-10-01

2024-09-30

0001961847

srt:MaximumMember

INHD:MayOneTwoThousandAndTwentyTwoAndAprilThirtyTwoThousandAndTwentySevenMember

2023-10-01

2024-09-30

0001961847

2023-08-01

2023-08-31

0001961847

2023-08-31

0001961847

2024-06-20

2024-06-20

0001961847

srt:MinimumMember

INHD:AugustEighteenTwoThousandAndTwentyThreeAndAugustSeventeenTwoThousandAndTwentyFiveMember

2023-10-01

2024-09-30

0001961847

srt:MaximumMember

INHD:AugustEighteenTwoThousandAndTwentyThreeAndAugustSeventeenTwoThousandAndTwentyFiveMember

2023-10-01

2024-09-30

0001961847

2024-07-23

2024-07-23

0001961847

2024-04-12

2024-04-12

0001961847

2024-04-12

0001961847

us-gaap:SubsequentEventMember

2024-10-25

2024-10-25

0001961847

us-gaap:GeneralAndAdministrativeExpenseMember

2023-10-01

2024-09-30

0001961847

us-gaap:GeneralAndAdministrativeExpenseMember

2022-10-01

2023-09-30

0001961847

srt:MinimumMember

2024-09-30

0001961847

srt:MinimumMember

2023-09-30

0001961847

2017-12-21

2017-12-21

0001961847

2017-12-22

2017-12-22

0001961847

2018-01-01

2018-01-01

0001961847

INHD:CoreModuLLCMember

us-gaap:SubsequentEventMember

2024-10-14

0001961847

INHD:CoreModuLLCMember

us-gaap:SubsequentEventMember

2024-10-14

0001961847

INHD:PurchaseAgreementMember

us-gaap:CommonStockMember

us-gaap:SubsequentEventMember

2024-10-31

2024-10-31

0001961847

INHD:PurchaseAgreementMember

us-gaap:CommonStockMember

us-gaap:SubsequentEventMember

2024-10-31

0001961847

INHD:PurchaseAgreementMember

us-gaap:PrivatePlacementMember

us-gaap:CommonStockMember

INHD:NineInvestorsMember

us-gaap:SubsequentEventMember

2024-11-13

2024-11-13

0001961847

INHD:PurchaseAgreementMember

us-gaap:CommonStockMember

us-gaap:PrivatePlacementMember

INHD:NineInvestorsMember

us-gaap:SubsequentEventMember

2024-11-13

0001961847

INHD:PurchaseAgreementMember

us-gaap:CommonStockMember

INHD:FromSixOfTheNinePurchasersMember

us-gaap:SubsequentEventMember

2024-11-27

2024-11-27

0001961847

2024-07-01

2024-09-30

iso4217:USD

xbrli:shares

iso4217:USD

xbrli:shares

utr:sqft

utr:acre

xbrli:pure

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

☒

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934:

For

the fiscal year ending September 30, 2024

☐

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934:

For

the transition period from __________ to __________.

Commission

file number: 001-41882

INNO

HOLDINGS INC.

(Exact

name of registrant as specified in its charter)

| Texas |

|

87-4294543 |

(State

or Other Jurisdiction of Incorporation or Organization) |

|

(I.R.S.

Employer Identification No.) |

2465

Farm Market 359 South, Brookshire, TX 77423

(Address

of principal executive offices, including ZIP Code)

(800)

909-8800

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to Section 12(b) of the Act:

| Title

of Each Class |

|

Trading

Symbol(s) |

|

Name

of each exchange on which registered |

| Common

stock, no par value |

|

INHD |

|

The

Nasdaq Stock Market |

Securities

registered pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has

been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files). Yes ☒ No ☐

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,”

“smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large

accelerated filer ☐ |

|

Accelerated

filer ☐ |

| Non-accelerated

filer ☒ |

|

Smaller

reporting company ☒ |

| |

|

Emerging

growth company ☒ |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. ☐

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As

of March 31, 2024, the last business day of the Registrant’s most recently completed second fiscal quarter, the aggregate market

value of the voting common stock held by non-affiliates of the Registrant (without admitting that any person whose shares are not included

in such calculation is an affiliate) was $2,798,633.

As

of December 3, 2024, there were 3,057,043 shares of common stock, no par value, issued and outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE

None.

Table

of Contents

SPECIAL

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This

annual report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of

1995, Section 27A of the Securities Act of 1933, and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements may

appear throughout this annual report, including in the following sections: “Business” and “Management’s Discussion

and Analysis of Financial Condition and Results of Operations.” Forward-looking statements are based on current expectations and

assumptions that are subject to risks and uncertainties that may cause actual results to differ materially. When used in this annual

report, the words “anticipate,” “believe,” “estimate,” “expect,” “future,”

“intend,” “plan,” or the negative of these terms and similar expressions, as they relate to us or our management,

identify forward-looking statements. Such statements include, but are not limited to, statements contained in this annual report relating

to our business strategy, our future operating results, and our liquidity and capital-resources outlook. Forward-looking statements are

based on our current expectations and assumptions regarding our business, the economy, and other future conditions. Because forward-looking

statements relate to the future, they are subject to inherent uncertainties, risks, and changes in circumstances that are difficult to

predict. Our actual results may differ materially from those contemplated by the forward-looking statements. They are neither statements

of historical fact nor guarantees of assurance of future performance. We caution you, therefore, against relying on any of these forward-looking

statements. Important factors that could cause actual results to differ materially from those in the forward-looking statements include,

without limitation:

| |

● |

our

ability to effectively operate our business segments; |

| |

● |

our

ability to manage our research, development, expansion, growth, and operating expenses; |

| |

● |

our

ability to evaluate and measure our business, prospects, and performance metrics; |

| |

● |

our

ability to compete, directly and indirectly, and succeed in a highly competitive and evolving industry; |

| |

● |

our

ability to respond and adapt to changes in technology and customer behavior; |

| |

● |

our

ability to protect our intellectual property and to develop, maintain, and enhance a strong brand; and |

| |

● |

other

factors relating to our industry, our operations, and results of operations. |

Should

one or more of these risks or uncertainties materialize, or should the underlying assumptions prove incorrect, actual results may differ

significantly from those anticipated, believed, estimated, expected, intended or planned.

Factors

or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of

them. We cannot guarantee future results, levels of activity, performance, or achievements. Except as required by applicable law, including

the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements

to actual results.

USE

OF CERTAIN DEFINED TERMS

Unless

the context otherwise requires, in this annual report on Form 10-K references to:

| |

● |

the

“Company,” “INNO,” the “registrant,” “we,” “our,” or “us”

mean INNO HOLDINGS INC. and its subsidiaries; |

| |

|

|

| |

● |

“year”

or “fiscal year” means the year ending September 30; |

| |

|

|

| |

● |

all

dollar or $ references, when used in this prospectus, refer to United States dollars; |

| |

|

|

| |

● |

“framing”

means the process of connecting building materials together to create a structure; |

| |

|

|

| |

● |

“stud”

means a vertical framing member which forms part of a wall or partition, also known as a wall stud, a fundamental component of frame

construction; |

| |

|

|

| |

● |

“truss”

means a web-like roof design that uses tension and compression to create strong, light components that can span a long distance; |

| |

|

|

| |

● |

“joist”

means a horizontal structural member used in framing to span an open space, often between beams that subsequently transfer loads

to vertical members; |

| |

|

|

| |

● |

“cold-formed

steel” or “CFS” or “light-gauge steel” or “LGS” means steel products shaped by cold-working

processes carried out near room temperature, such as rolling, pressing, stamping, bending, etc.; |

| |

|

|

| |

● |

“turnkey

cost” is the total cost that must be covered before a product or service is ready to be sold and used by consumers; |

| |

|

|

| |

● |

“prefab”

means a building manufactured in sections to enable assembly on site. |

PART

I

ITEM

1. BUSINESS

Overview

INNO

HOLDINGS INC. (“INNO,” “we,” “us,” or “Company”) is an innovative building-technology

company with a mission to transform the construction industry with our proprietary cold-formed steel-framing technology and other building

innovations. INNO recognized the inherent inefficiency and waste in traditional lumber-based construction techniques and sought to develop

steel-based construction technologies to solve the problems. INNO takes its name from “innovation” and is committed to the

research and development of steel studs/tracks/headers, providing higher performance and greater efficiencies in all aspects of construction,

making better structural solutions for both commercial and residential buildings, resulting in substantial labor cost savings, in our

view. The Company’s products are created using a combination of intelligent machines and cutting-edge techniques to provide an

optimal design solution of framing for engineers, builders, and construction companies. We are currently a manufacturer of cold-formed-steel

members and we offer a full range of services required to transform raw materials into precise steel framing products and prefabricated

homes. We sell these finished products either to businesses or directly to customers. The finished products and cold-formed-steel members

are used in a variety of building types, including residential, commercial, industrial, and infrastructure. We hope to transform the

building industry by reducing construction times while providing more affordable, environmentally sustainable, and durable solutions

compared to traditional construction materials and methods. We believe we are also well positioned to disrupt the construction industry,

which now accounts for $10 trillion of the global economy.

We

work with our customers to manufacture products in accordance with the customers’ drawings and specifications. Our work complies

with specific national and international codes and standards applicable to the construction industry. We believe that we have earned

our reputation through outstanding technical expertise, attention to detail, and a total commitment to excellence in customer service.

Our

primary manufacturing operations are located on approximately five acres in Brookshire, Texas. Our facility houses state-of-the-art equipment

that gives us the capability to manufacture 15,000 linear feet of product per day. We offer a full range of services such as structural

designs, metal stud production, and preassembly of metal studs into steel wall panels, which are required to transform raw materials

into finished products that are compliant with local building codes. Our manufacturing capabilities include fabrication operations, such

as cutting, punching, forming and assembling, and machine operations, which includes computer numerical controlled (“CNC”)

machine operations. We also provide support services for our manufacturing capabilities: manufacturing engineering (planning, fixture

and tooling development, and manufacturing), quality control (inspection and testing), materials procurement, production control (scheduling,

project management, and expediting), and final assembly.

All

manufacturing at our facility is done in accordance with our written quality assurance program, which meets specific national codes as

well as international codes, standards, and specifications. For example, we have ICC-ES evaluation reports (ESR-4641) that show that

our cold-formed steel-framing members are compliant with the 2018 and 2015 International Building Code (“IBC”), 2019 California

Building Code (“CBC”), and 2020 Florida Building Code. The standards used for each customer project are specific to each

customer’s needs, and we have implemented those standards into our manufacturing operations.

In

2024, we successfully launched a new revenue stream through our newly established subsidiary, Inno AI Tech Corp., which specializes in

research and consulting services.

Our

Products

Cold-Formed

Steel Framing

Cold-formed

steel is the material of choice to lower building costs and adapt to modular or off-site buildings. It is consistent in quality and

form, and it can be shipped preassembled or it can be assembled on-site by workers with little training. Our steel roof trusses,

wall panels, and joist systems are a cost-effective noncombustible alternative to traditional building materials. They are

now commonly used to build apartments, hotels, temporary housing, nursing homes, commercial buildings, industrial buildings, and

single-family detached homes. These types of structures are expected to be the targets of our Company’s sales and marketing

team.

Our

proprietary cold-formed roller machines are equipped with proprietary software, which optimizes production efficiency and supports individual

part customization to ensure each cold-formed-steel member is produced to the exact specifications of the plans. Our intelligent machines

can precisely cut and punch out steel studs, leaving channels for the mechanical, electrical, and plumbing designs. We arrive at an accurate,

comprehensive, and information-rich design model with the utilization of light-gauge steel-framing engineering software, which

creates a digital model of the project that includes all functional systems, geometric features, and aesthetics, such as electrical wiring,

air conditioning, doors, and windows. The light-gauge steel-framing engineering software is a shared multidisciplinary resource that

allows collaborators to achieve maximum efficiency and effectiveness by compressing design lead time. We have created a full BIM solution

that instructs our advanced cold-formed roller machines to produce each steel-framing piece to certain specifications.

After

the design phase, our top-quality raw materials are processed on several production lines, each with made-to-order specific dimensions,

screw holes, and cross-cut stitching. These customizations reduce the need for on-site manual calculations and simplify the assembling

steps, both of which increase construction efficiency and reduce labor costs. All steel-framing products produced by our Company are

International Code Council (ICC) certified. The International Code Council is the leading global source of model codes and standards

and building safety solutions that include product evaluation, accreditation, technology, training, and certification. The Code Council’s

codes, standards, and solutions are used to ensure safe, affordable, and sustainable communities and buildings worldwide.

Our

modular steel building framing systems avoid construction delays caused by partial or unsynchronized delivery of different building components.

By breaking away from the methods of traditional stick-built building, our customers report that their construction timelines have been

reduced by at least 20%.

Castor

Cube

Due

to high housing prices, some are having difficulties purchasing a home. Housing market trends have shown a gradual preference for modular

homes, which is a prefabricated building that consists of repeated sections called modules, and involves constructing sections away from

the building site, then delivering them to the intended site where the installation is completed. We believe demand for prefab homes

is on an upward growth trend in the United States. According to the Straits Research Institute, North America’s share of the global

modular building market was valued at $28 billion in 2021 and is expected to grow to $53 billion by 2030, representing a CAGR of 7%.

According to the summary of an IBISWorld report titled, “Prefabricated Home Manufacturing in the US — Market Size 2002-2029,”

the prefabricated home manufacturing market size in the U.S. is expected to be $9.1 billion in 2023. We expect to capitalize on this

trend by providing high-quality and affordable modular homes.

Most

consumers are drawn to prefab homes because of their cost-effectiveness, efficiency, and permanent property characteristics. Castor Cube

is a low-maintenance, single-story, 743-square-foot manufactured home with 4 color options that can resist earthquakes, withstand winds,

and prevent pests. It is a cold-formed-steel building system equipped with honeycomb panels, and it is designed to maximize the strength-to-weight

value. As a result, it yields high structural stability. Castor Cube can be built on a foundation or used as a mobile home.

The

Castor Cube can be built on a foundation steel chassis, which can be single or used as a mobile multi-sectioned. We are expanding and

improving our facility in Texas and anticipate that this modular home product will be completely constructed within the next couple years.

Once built, it will be transported to permanent locations for installation. The timeline for product delivery is not affected by weather

since it will be manufactured in our 100% climate-controlled factory. Furthermore, we expect that streamlined building process will shorten

the completion time.

Mobile

Factory: Off-site Equipment Rental, Sales, Service, and Support

We

believe innovative technology can increase productivity in the building sector. Research and development of more efficient methods in

the manufacturing and building space is at the forefront of our business model.

Our

Mobile Factory is an all-in-one, secured production facility that will produce steel-framing members onsite. It can print wall panels,

floor truss, and roof truss components. The size is customized for a trailer, which enables it to be transported anywhere, ranging from

metropolitan suburbs to remote areas with little to no infrastructure. It is designed to enable immediate stud production on any site.

Our

Mobile Factory is complete with metal stud production equipment and a diesel generator. This generator can supply continuous power to

our cold-formed roller machine. The production capacity of our Mobile Factory is at least 1,000 linear feet per day. We believe this

innovation is the good solution for urgent deployment in disaster areas or remote areas. It is designed to reduce the cost and time of

transportation of metal studs, which we believe can drive a lower carbon footprint for larger projects.

The

Mobile Factory is operated and managed by Internet of Things (“IoT”) technology, a network of physical objects that are embedded

with sensors, software and other technologies for the purpose of connecting and exchanging data with other devices and systems over the

internet. INNO developed its proprietary IoT production management system independently. The system controls equipment and manages the

Mobile Factory via a dashboard, allowing the user to gain a comparative understanding of production parameters, such as operation data,

machinery breakdown data, uptime data and production efficiency.

Related

Services

We

may from time to time participate in land development and contractor services if an opportunity exists to leverage our products. Specifically,

we have evaluated the development of apartment complexes, retirement communities, and remodels for projects that would incorporate our

metal framing studs. For example, we have agreed to provide project development services for our contract with Vision Opportunity Fund

LP (assigned to Vision 101), partially owned by a minority shareholder of the Company, related to the development of an approximately

110,000 square feet retirement community.

In

February 2024, we formed Inno AI Tech Corp., which specializes in research and consulting services. Throughout the year, we successfully

supported a client in establishing a steel technology company. Our services included incorporation assistance, comprehensive training

programs, in-depth market research, and strategic business development guidance. This engagement generated consulting revenue of $205,000.

Our

Customers

We

can serve commercial, residential, and industrial projects. For the cold-formed steel-framing business, the sales model is business-to-business

because the main customers are developers, builders, and contractors. For the Castor Cube prefab home products and the consulting services

performed by Inno AI Tech Corp., the sales model is expected to be either business-to-business or business-to-customer.

On

a year-to-year basis we are generally dependent on a small number of major customers that change year to year. Our written agreements

with major customers normally terminate upon completion, and our major customers change from year to year. For the year ended September

30, 2024, three customers accounted for 90% of the Company’s total revenues, respectively. For the year ended September 30, 2023,

three customers accounted for 53%. As of September 30, 2024, $Nil outstanding of accounts receivable. Accounts receivable from one customer

accounted for 100% of the Company’s total accounts receivable as of September 30, 2023.

These

agreements contain standard construction and supplier agreement terms including payment schedules, performance schedules, the ability

to subcontract, insurance obligations and indemnification provisions, and confidentiality provisions. Our written agreements with these

customers generally terminate upon completion of the project or early terminate upon mutual agreement of the parties and contain provisions

restricting our right to assign the agreement.

Our

Suppliers

Historically

we rely on a limited number of suppliers. For the year ended September 30, 2024, two suppliers accounted for 58% of the Company’s

total purchases. For the year ended September 30, 2023, three suppliers accounted for 57% of the Company’s total purchases. As

of September 30, 2024 and 2023, accounts payable to two suppliers accounted for 51% and 55% of the Company’s total accounts payable,

respectively. We currently do not have written agreements with these suppliers or, generally, with any of our suppliers. All of our purchases

from these suppliers are made by way of individual orders.

Our

Competitive Strengths

Technology

Innovations

INNO

recognizes that no technology or product is completely immune to being copied, and therefore the company is committed to being a pioneer

in the industry by constantly researching and developing new technologies, and being ahead in various aspects of the industry such as

regulations, equipment autonomy, design technology, production efficiency, new product birth, orderly management, coordinated transportation,

remote production, etc. In this way, INNO aims to have the most advanced and comprehensive technology in the industry and be the true

technological barrier for competitors to overcome. INNO focuses on patentable innovative products and commercializing research discoveries

in the cold-formed steel industry in the U.S. and committed to bringing innovation in the field of thin-walled structures, cold-formed

steel building technology, and design methodology for resilient buildings.

Fully

Integrated Manufacturing Process

Compared

to other traditional metal stud manufacturers, INNO differentiates itself by integrating services from design to metal stud production

to prefabrication, utilizing off-site building technology to reduce the need for on-site framing labor. This approach allows INNO to

streamline the production process, increase efficiency, and reduce dependency on labor. By implementing off-site building technologies,

INNO is able to prefabricate and assemble many components of the building in a factory setting, which can lead to improved quality control,

faster construction times and reduced on-site labor costs. This approach allows INNO to be a leader in the metal studs manufacturing

industry in the U.S. and set a new standard for the building industry.

Compared

to other prefab home companies, INNO sets itself apart by making an innovation in the overall structure system and developing our own

patent pending panel material for faster installation. Unlike other prefab home competitors who still use traditional wood-stick building

methods or other unique liquid material (required by 3D printing), which are not as efficient and may not be able to guarantee delivery

times, INNO’s patent pending panel material and overall structure system allows for faster installation, improved efficiency and

guaranteed delivery times. This allows INNO to offer a more efficient and cost-effective solution for prefab home building and maintain

a competitive edge in the market. Additionally, INNO’s patent pending material and system can guarantee the quality and safety

of the building, which is a significant advantage over the other prefab home companies.

Rising

Cost of Traditional Wood Construction Favors Transition to Steel

Utilizing

INNO’s off-site building technology can significantly reduce overall construction costs, even when compared to wood building. The

past several years of western wildfires in the United States have had a significant impact on lumber stocks and mills, leading to disruptions

in supply and fluctuations in lumber prices. A study by the Steel Framing Industry Association (SFIA) indicates that the cost to build

with cold-formed steel is relatively the same as building with wood when the cost comparison includes the construction insurance premiums

associated with using the materials. As the price of wood no longer provides a cost advantage, alternative building materials like steel

have become increasingly popular in the market. By leveraging its off-site building technology, INNO is able to offer a cost-effective

solution that takes advantage of the cost benefits of steel building while also providing faster and more efficient construction.

We

are keeping our prices at a competitive level with traditional wood framing solutions. In a recent internal case study, we found that

INNO’s products delivered real-world cost-savings of 8-16% compared to wood framing. This study compared our solution against wood

for a 2,2663 square feet. home built in 2022, for which we supplied materials. Based on fully quoted materials and estimated labor and

insurance costs, we estimate the contractor saved 16% by using INNO products compared to wood framing. For the “low” scenario,

we recently requested updated wood bids and used the lowest one; in this case, we estimate that INNO products would have provided the

contractor with 8% savings.

Market

Opportunity

Light-Gauge

Steel-Framing Market

According

to the report released by Grand View Research in 2022, titled “Light Gauge Steel Framing Market Size, Share & Trends Analysis

Report By Type (Skeleton Steel Framing, Wall Bearing Steel Framing), By End-use (Commercial, Residential), By Region, And Segment Forecasts,

2023 - 2030”, the global light-gauge steel-framing market was valued at $37.27 billion in 2023 and is expected to reach $52.73

billion by 2030, growing at a CAGR of 5.1% from 2023 to 2030. The substantial rise in construction spending and a shift in trend toward

sustainable materials have contributed to higher energy efficiency at a lower cost, in turn driving the market demand for light-gauge

steel frames. According to KBV Research’s report released in February 2022, titled “North America Light Gauge Steel Framing

Market Size, Share and Industry Trend Analysis Report By Type, By End Use, By Country, Historical Data and Growth Forecast, 2021-2027,”

the U. S. market has dominated the North American cold-formed steel-framing market, and it is expected to continue to be a dominant market

player until 2027; thereby, achieving a market value of $7.2 billion by 2027.

According

to the summary of an IBISWorld report titled, “Wood Framing in the US - Market Size, Industry Analysis, Trends and Forecasts (2024-2029),”

the wood framing market size in the U.S. is expected to be $27.5 billion in 2024. Since the wood structures could be replaced by cold-formed-steel

structures, INNO’s target market size includes the wood-framing market. If we combined the US light gauge steel (which we estimate

to be currently at approximately $6 billion based on the projected market value of $7.2 billion by 2027) and wood framing market ($27.5

billion) opportunities in 2024, we estimate it would amount to a $33.5 billion market opportunity in which INNO competes.

Prefabricated

Building Market

According

to the summary of an IBISWorld report titled, “Prefabricated Home Manufacturing in the US market size (2024-2029),” the prefabricated

home manufacturing market size in the U.S. is expected to be $13.3 billion in 2024. According to the report released by Global Industry

Analysts, Inc, titled “Prefabricated Buildings - Global Strategic Business Report”, the global prefabricated building market,

estimated at $117.4 billion in the year 2022, is projected to reach a revised size of $202.7 billion by 2030, growing at a CAGR of 7.1%

over the analysis period of 2022 through 2030. According to Straits Research Institute, the U.S. modular home market is projected to

be valued at $53 billion in 2030.

Prefabricated

houses are those that are built with the help of prefabricated building materials. These building materials are prefabricated in an off-site

facility and then transported to the desired location for assembly. The building materials used to develop prefabricated houses are divided

into concrete-based and metal-based materials. The market is being driven by factors such as shorter construction times and cost savings.

The market is also benefiting from increased customer interest in reducing CO2 emissions, green building, and waste reduction.

Regulatory

and Governmental Pressures for Change

President

Biden’s Executive Order 14057 on the adoption of the federal Sustainable Development Catalyst for America’s Clean Energy

Industry and Jobs and the accompanying federal Sustainable Development Plan establish the ambitious goal of achieving zero emissions

from building by 2045. The federal government will work on new construction, major renovations, and existing real estate to achieve linked

electrification, reduced energy use, lower water consumption and waste reduction. The federal government will develop data-driven targets

and annual indicators for energy and water reduction by 2030 based on leading performance benchmarks for building type categories and

the composition of institutional building portfolios. As part of this journey, the federal government will use performance contracts

to reduce emissions, improve efficiency, and modernize facilities while providing financial savings.

In

2021, the Los Angeles City Council Public Safety Committee approved a proposal to expand Fire District I, an anachronistic planning overlay

that would effectively ban wood-frame building in much of the city. The motion currently winding its way through City Council would expand

Fire District I to neighborhoods with a population density of 5,000 residents per square mile, among other areas. With nearly all of

Los Angeles comfortably above 5,000 residents per square mile, this expansion would effectively ban timber and wood-frame building in

much of the city, including many rapidly growing neighborhoods near transit.

Sustainability

and Green Building

Manufacturing

of materials for buildings and construction accounted for approximately 11% of global energy-related CO2 emissions in 2017 according

to the Global Status Report 2018, Global Alliance for Buildings and Construction & International Energy Agency. Increased global

awareness of green building has driven efforts among all levels of government. For example, local governments are beginning to regulate

in favor of using alternatives to wood in building projects. To reduce the city’s vulnerability to wildfires, the Los Angeles City

Council voted in early 2021 to explore a proposal that could prohibit the use of wood-frame building for larger developments in some

of its most densely populated neighborhoods. Similarly, the Los Angeles City Council Public Safety Committee approval of a proposal in

2021 to expand Fire District 1, an anachronistic planning overlay that would effectively ban wood-frame building in much of the city.

In most U.S. cities, fire safety is ensured by the International Building Code (IBC), which sets strict rules on allowable building materials

and methods.

Cold-formed

steel framing (“CFS”) is a highly sustainable, green building solution. Through technological advances and processing changes,

steel has drastically reduced its carbon footprint. CFS boasts a high level of recyclability, energy savings and greenhouses gas reduction.

Due to its inherent advantages such as fire-resistance, termite resistance, consistent material quality and sustainability, we believe

cold-formed steel will be the optimal alternative building material.

Marketing

We

are an innovative building-technology company with a mission to transform the construction industry with our proprietary cold-formed

steel-framing technology and other innovations. While we have significant customer concentrations, we endeavor to broaden our customer

base as well as the industries we serve. Our marketing strategy is a long-term plan to achieve our Company’s mission by understanding

the needs of customers and creating a distinct and sustainable competitive advantage. We position ourselves as the leader in intelligent

steel-framing building systems. We intend to leverage our marketing and sales efforts to establish new potential customers. We also intend

to leverage customer referrals, which in the past have been a source of new business. A significant portion of our business is the result

of competitive bidding processes, and a significant portion of our business is from contract negotiation. We believe that the reputation

we have developed with our current customers represents an important part of our marketing effort.

Quotation

requests from customers are reviewed to determine the specific requirements and our ability to meet such requirements. Quotations are

prepared by estimating the material and labor costs and assessing our current production schedule to determine our delivery commitments.

Competitive bid quotations are submitted to the customer for review and award of the contract.

We

have several strategic partners, including real estate companies, general contractors, builders and developers. Our strategic partners

connect our Company with potential customers who are either potential homeowners or developers.

Through

the several architecture, builder and contractor associations that we have joined, we share the advantages of cold-formed steel framing

with others, and we educate and encourage construction industry practitioners to move out of their wood-framing comfort zone to embrace

steel-framing technology.

We

have a digital market channel and a social media presence. Also, we are actively conducting market research to determine the viability

of our new products and new patents. We have increased our marketing budget and formed a professional sales team to increase our online

marketing, which we believe can help us grow our revenue.

Research

and Product Development/Innovations

We

are a building technology company that is dedicated to research and product development innovation. Our scientists and engineers are

committed to developing sturdier steel studs, tracks, headers, and other components, resulting in superior strength while maintaining

the lowest costs possible. Our cold-formed roller machine is acquired from an original equipment manufacturer with certain modifications

to the standard version of the machine that are unique and proprietary to INNO. When we refer to our “proprietary” cold-formed

roller machines, we are referring to the modified machine with the intellectual property and process techniques we have developed. INNO

uses CAD (Computer Aided Design) technology to arrive at the most accurate, comprehensive and information-rich design model within its

parameters with the utilization of Vertex to ensure each member is produced to the exact specifications of called for in the design.

The digital model of the project includes all functional systems and aesthetics, such as electrical wiring, air conditioning, doors,

windows etc., as well as geometric features. It is a shared multi-disciplinary resource allowing all those working on a project to share

information and working processes in order to achieve maximum efficiency and effectiveness, thus reducing all phases — design,

pre-construction and construction — of the construction timeline. The platform gives us open communication, true collaboration,

and aligned understanding. Taken all together, INNO has created a full BIM solution that works together to inform our state of the art

light-gauge roll forming machines the instructions to automatically produce each steel framing member to exact specification.

We

have continued making improvements to our cold-formed roller machines to optimally increase the printing speed. We are actively working

on a list of 100 potential patentable products. Our goal is to commercialize patents and technologies that we own.

For

example, the CFS portal frame system invented by us could replace current shear wall systems to provide adequate lateral resistance against

strong winds and severe earthquakes. The standard lateral force resisting systems in light frame cold-formed steel building are shear

walls either sheathed by structural panels such as OSB, Plywood, and steel sheets or braced by steel straps. These systems require a

large amount interior walls to be load bearing walls which limits flexibility for room layout and may not support large openings for

windows and doors. The steel portal frame system is a novel long span framing system to replace the traditional hot-rolled structural

steel frame. The new technologies in the portal frame system include optimized stiffened holes on cold-formed steel frame members to

increase structural stability and span capacity and special moment joint technology using adhesive and rivet connections which enable

superior energy dissipation capacity and fast fabrication.

This

new CFS moment frame does not require any interior shear walls for the Castor Cube, our modular home product. It will allow the Cube

to have various room layouts. The homeowners will also be able to change the room layout in the future. The new CFS moment frame can

also be used for long-span residential and mid-rise commercial buildings. The new technology should improve the structural integrity

of building structures, increase the lateral resistance, and lower the overall costs.

Another

innovation, the cold-formed steel truss system, utilizes a strong axis of cold-formed steel stud members for both chords and webs which

allow longer spans and lighter weight than the conventional type trusses. The steel truss system has wide applications in storage and

education buildings.

We

believe the steel truss system and steel portal framing system will also allow INNO to enter the high-rise commercial and large span

industrial building markets (Type I and Type II buildings) and deliver more competitive and cost-effective building structures than the

traditional structural steel frame and concrete masonry systems.

Honeycomb

aluminum panel is a metal composite panel product series developed in combination with the composite honeycomb panel technology developed

by the aviation industry. The panel is a box-type structure with surrounding edges, which has good airtightness and improves the safety

and service life of the panel. The product adopts a “honeycomb sandwich” structure, that is, a composite plate made of high-strength

alloy aluminum plate coated with a decorative coating with excellent weather resistance as the surface, bottom plate and aluminum honeycomb

core through high temperature and high pressure. This product series has the advantages of excellent material selection, advanced technology,

and reasonable structure. It not only has excellent performance in large scale and flatness, but also has many choices in terms of shape,

surface treatment, color and installation system. This advanced technology enables the Company to manufacture high-strength and light-weight

wall panel products. These siding products have very flat surfaces and tightly controlled seam widths, which allow architects to design

very straight and beautiful walls with large panels. Except for certain technical restrictions, there is no standard size for honeycomb

aluminum panels, and all wall panels are factory-made according to design drawings. Our production method allows the panels to be highly

flexible in size and shape, such as curved panels and folded panels. This flexibility creates a complete and multi-functional highly

competitive wall panel system that can be installed on almost any joist and are extremely simple to install.

Revenue

Model

Our

revenue model currently consists of sales of the following:

| |

● |

Light-gauged

studs and tracks; |

| |

|

|

| |

● |

Prefabricated

wall panels and trusses; |

| |

|

|

| |

● |

Structure

framing work on site; |

| |

|

|

| |

● |

Services; |

| |

|

|

| |

● |

Machine

sales; and |

| |

|

|

| |

● |

Replicable

Apartment product. |

Light-gauged

studs and tracks

We

supply metal studs from 12GA to 24GA depending on the structure engineering requirements and city building codes. The model for selling

cold-formed steel studs and tracks is wholesale because it is business-to-business. Given the specific nature of our products, we do

not sell retail. Unlike traditional metal stud suppliers, whose products are “made to stock” with no consideration for engineer

design, our metal studs are typically made-to-order and customized for each project.

Prefabricated

wall panels and trusses

Prefabricated

wall panels and trusses are another option for customers. With these products, the customer can either choose to assemble the panels

themselves or include this prefab service in their contract with us. Most customers typically choose prefab service because of our skilled

team given that most wood framers are not familiar with steel framing.

INNO

also has standardized modular wall products which could be used for all residential and commercial buildings. We design modular walls

in 20 specifications to cover different building requirements. Modular walls are “made to stock” products and participate

in both business-to-business and business-to-customer model channels.

Structure

framing work on site

Steel

structure installation on site is also an optional service. Depending on the project size and scope, we will provide on-site installation

service if customers requested. With our full turnkey solution, all elements of the project construction are included, not just the cold-formed

steel. This may include cabinetry and other items. In cases where the customer simply wants the framing, we bring our expertise in working

with steel to that portion of the project. We are in the process of reducing our on-site work offerings.

Services

Our

engineering services provide stamped and sealed structure design services by our in-house engineer team. Because of the specific nature

of our services, the rates vary case by case depending on the square footage and project complexity. Our engineer team will collaborate

with customer’s architect, civil engineers, and MEP engineers to make sure the final structure design is city approved. To begin

the metal stud production, our engineer team also generates the shop drawings which is a digital file and readable by our intelligent

CNC machine. We also have another option where the customer may outsource the engineer service and contact INNO for metal stud production,

where we do not provide continuous services until the design is city approved.

In

February 2024, we formed Inno AI Tech Corp., which specializes in research and consulting services. In 2024, we successfully supported

a client in establishing a steel technology company. The services included incorporation assistance, comprehensive training programs,

in-depth market research, and strategic business development guidance. This engagement generated consulting revenue of $205,000. The

revenue from the consulting service is recognized upon the described services be provided to customers.

Machine

sales

We

may sell or lease our machines. We provide technical and design support at relatively low costs, including industry compliance license

and permits, as well as shop drawings and structural design. We also offer administration, operation, and management consulting support,

including directing and assisting factory set-up, operation procedures, equipment installation, machine maintenance, repairs, and efficiency

improvement. The training for such operations and installations are also provided. We will recommend, select, and advise pricings for

material suppliers and other vendors.

Replicable

Apartment Product

Our

flagship product within this series is Village 101, a smart senior living apartment comprising 155 units with a floor area of 110,000

square feet. The architectural plan package for Village 101 is complete and ready for implementation. The project is currently pending

for permits. Village 101 serves as a prototype building tech community, showcasing our innovative approach to senior living.

Our

pipeline includes various apartment product options with different unit sizes, ranging from 15 to 150 units. These products are under

active research and development, with the aim of creating replicable housing complexes across the United States. By leveraging our expertise

in building technology and innovative design, we target to provide scalable and high-quality housing solutions that meet the evolving

needs of residents including but not limited to senior citizen, college students and Gen Z etc.

Through

our revenue model, we anticipate generating sustainable income by catering to the demand for replicable apartment products. By expanding

our product line and continually advancing our research and development efforts, we aim to capture a significant market share in the

housing industry while delivering superior value to our clients.

Cost

of Sales

Cost

of Sales primarily consist below components.

| |

● |

Materials

— Rolled steel represents the single largest cost. We manage our relationship with suppliers (primarily US Steel) very adroitly

by building in purchase orders and their associated costs to the customer to minimize our exposure to changes in steel prices for

any specific project. We manage our purchases and deliveries as close to “just in time” as possible. |

| |

|

|

| |

● |

Labor

— Labor is potentially the most variable component of cost of sales. We have a team of hourly workers who largely work onsite

at the factory producing parts from raw steel and assembling them into prefabricated pieces to be delivered to job sites. Contractors

are non-employee hourly workers who largely work in our turnkey projects. As-needed hourly labor is largely available in our markets. |

| |

|

|

| |

● |

Freight

and Shipping — Our policy is to include any freight incurred to ship the product from our vendors to warehouses as a part of

cost of goods sold. Outbound freight costs related to shipping costs to customers are considered periodic costs and are reflected

in selling expenses. |

Other

Expenses

Other

expenses are typically comprised of payroll of salaried and hourly workers. We pride ourselves on running lean and efficiently. We operate

in a business-friendly state with a large and available workforce. Rent, utilities, insurance, consulting service and other normal expenses

are all competitive in the commercial area where we are based.

Our

Growth Strategy

We

seek to leverage the trend toward off-site and modular building techniques to increase productivity, reduce errors on-site, and decrease

costs. With both Castor Cube and Mobile Factory as our featured products in the coming years, we seek to become leaders in the industry.

As the market continues to move toward panelized construction, we seek to have an edge in the industry as a large-scale pioneer of the

overall cost-reducing process.

INNO’s

business growth strategy combines the following three parts: revenue growth strategy, profit growth strategy and technology growth strategy.

Revenue

Growth Strategy

Our

revenue growth strategy is composed of the following.

Capacity

expansion and in-house research and development. We are expanding factory operations and manufacturing capabilities in line with

demand. We are also investing in R&D to ensure a pipeline of competitive and innovative building-technology products.

Multiple

products and services. We are in the process of developing the Castor Cube, a 743-square-foot modular house product with the goal

of mass producing. We are also working on developing Village 101, a smart senior living apartment comprising 155 units with a floor area

of 110,000 square feet. The architectural plan package for Village 101 is complete and awaits permits approval for implementation. We’ve

expanded our business to include consulting services offered by our new entity-AI Tech Corp.

Marketing

investment. We are in the process of optimizing our online sales and marketing efforts by recruiting marketing talent and engaging

consultants for marketing and promotional events.

Potential

Acquisitions and investments. In accordance with our growth strategy, our company intends to pursue vertical integration by acquiring

or investing several companies operating within the construction industry in the United States. The objective of this vertical integration

is to strengthen our position as a prominent building-technology developer and expand our capabilities within the market. We will position

ourselves to offer a comprehensive range of solutions encompassing the entire building. The expanded scope of our offerings includes

prefab structure systems, centralized MEP (mechanical, electrical, plumbing) systems, integrated wall systems, integrated floor systems,

roofing systems, and prefab cabinets, sinks, and countertops. This integration allows us to deliver a single-cycle turnkey solution,

streamlining the traditional linear process employed by traditional developers. To fortify our supply chain and augment our capabilities,

we will consider the strategic acquisition or investment of construction vendors/suppliers. The targeted companies would include the

ones that enjoy the popularities in the industry, including but not limited to the companies that can supply the interior finish, exterior

wall panels, insulation materials and roof system etc. By incorporating the targeted companies into our operations, we will establish

a comprehensive one-stop-shop solution for the multi-family apartments, thereby further solidifying our market position and value proposition.

Consistent with our growth strategy, we are firmly committed to implementing a robust product life cycle management approach, encompassing

all stages from procurement to delivery. Through our pursuit of vertical integration and strategic acquisitions, we are poised for substantial

growth to assume a leadership role within the market. By expanding our product offerings, strengthening our supply chain, and cultivating

key partnerships, we are well-positioned to provide comprehensive building solutions that effectively meet the evolving needs of our

clients while concurrently driving revenue growth and delivering enhanced shareholder value.

Profit

Growth Strategy

Our

profit growth strategy is composed of the following.

Improving

assembly automation. We plan to source and develop production robots and to expand automation where possible, to further increase

our production efficiency.

Reducing

transportation costs by utilizing Mobile Factory. Our Mobile Factory is equipped with our proprietary machines and can be transported

to any jobsite. Mobile Factory utilizes Inno Statlink Data System which is ideal for remote production management. Mobile Factory saves

significant transportation costs and as such, our goal is to increase the use of Mobile Factory.

Optimizing

artificial intelligence design capabilities. We intend to optimize the artificial intelligence design capabilities by utilizing machine

learning to get the wisest structure supporting data and running several models for all types of walls. The model we tested could reduce

the raw materials used in different projects.

Technology

Growth Strategy

Our

technology growth strategy is composed of the following.

Develop

EQ products to replace existing building materials with thinner and lighter products. We are developing technology in an effort to

replace existing building materials with thinner materials. Once this technology matures, it is expected to save approximately 10% in

raw materials.

Develop

stainless steel as a building material for the high-end building market. We are developing technology to replace the current galvanized

steel sheets with stainless steel. The new patent pending material could be used in extreme climate conditions for high-end customers.

Leverage

module wall technology to increase the range of applications. We are in the process of developing different types of module wall

products to expand our customer reach.

Strategic

Partnerships

We

have partnerships with at least 10 regional and national developers and builders. INNO’s customers include national real-estate

developers and some local builders in both Texas and California. The regional/national developers and builders have a strong pipeline

of projects coming each year. Their project types cover residential, commercial, and industrial. They either intend to use steel framing

for structure or to develop land with Castor Cube and Village 101 projects, as their strategic partners, INNO will provide customized

offer and have higher probability to bid and win projects. The cold-formed steel framing business is categorized as business-to-business

model, and the Castor Cube as well as Village 101 projects will be either to business or to customers.

Competitive

Outlook

Lumber-Based

vs. Cold-Formed Steel

Our

primary competitors (or segment with which we are most often compared) are traditional lumber-based building products solutions in certain

categories, particularly buildings below six floors and residential. The accessibility and proficiency in assembling lumber-based structures

can make practitioners in the construction industry unwilling to move out of the wood framing comfort zone. Further, lumber prices were

generally lower than the price of metal studs. The switch to cold-formed Steel is being driven by materials price and several market-based

advantages of steel. Steel is strong, safe, durable, versatile, and cost-effective. Steel has the exceptional environmental advantage

of being highly recycled and infinitely recyclable. Steel is tough and does not rot, spawl, split, or absorb moisture, and it is resistant

to pests, unlike wood building materials.

Inherent

Benefits of Steel Framing

| |

● |

Steel

has the highest strength-to-weight ratio of any framing material. |

| |

|

|

| |

● |

Non-combustible.

Steel will not contribute fuel to the spread of fire. |

| |

|

|

| |

● |

Steel

is termite and rodent resistant. |

| |

|

|

| |

● |

Steel

ensures dimensional stability. Will not rot, warp, crack or shrink. |

| |

|

|

| |

● |

Lower

builder’s risk insurance. |

| |

|

|

| |

● |

Permanently

straight walls. No call backs for nail pops. |

| |

● |

No

toxicity contribution. Free of resins, adhesives, and chemicals normally present in other framing material. |

| |

|

|

| |

● |

Consistent

material quality. No regional variation. |

| |

|

|

| |

● |

Grounded

against electrical storms. |

| |

|

|

| |

● |

Steel

is inorganic. Unlike traditional framing products, steel is not vulnerable to mold. |

| |

|

|

| |

● |

Steel

is the most recycled product in the world. Optimum sustainability. |

The

SFIA has conducted studies of construction costs in two different locations using two identical buildings — one designed with wood

and the other with cold-formed steel (CFS) framing. The mixed-use, 49,900 square foot building used in the studies is representative

of many residential buildings constructed in the mid-rise market today and includes:

| |

● |

A

first floor non-combustible (concrete) podium with parking and retail space |

| |

|

|

| |

● |

Residential

dwellings on levels 2-5 |

| |

|

|

| |

● |

Roof-top/penthouse

space atop level 5 housing building services. |

The

first location for the study was a building constructed in Chicago in late 2017. Results include hard construction costs only. In this

case, cold-formed steel cost 2.6% more than traditional wood construction.

The

second location was in Morristown, New Jersey. It takes a deeper look at costs by including the impact of lower insurance premiums available

for CFS construction compared to combustible framing (wood). The insurance costs from major insurers operating in New Jersey were converted

to a cost per square foot and evaluated in terms of their impact on the overall building costs. In this case, cold-formed steel cost

0.9% more than traditional wood construction.

The

two case studies mentioned above are taken from the official SFIA website. We believe INNO’s product cost is less than that of

the preceding case studies, with the overall cost less than that of traditional wood.

Others

Participating in Cold-formed Steel

The

second category of competitors are divided into two groups: traditional manufacturers of metal studs and suppliers of cold-roller machines.

Traditional manufacturers, such as Clark Dietrich and CEMCO, pre-punch their metal studs with punchouts at regular intervals for pipe

installation, but the number of punchouts is fixed and not customized for each project. INNO employs proprietary software to calculate

the minimum punchouts for MEP pipe installation that are consistent with the architectural plan set to ensure the structure’s load-bearing

capability to the greatest extent possible. The load-bearing capability gradually decreases as the number of punchouts increases. Traditional

steel framing manufacturers are unable to automatically make punchouts for screw holes, so manual drilling holes at the jobsite for metal

stud connections are still required. The screw holes are precisely located and punched by the INNO CNC machines.

Screw

hole punchouts are left for panel assembly, and the stud spacing should be building code compliant. The number of screw holes for each

panel is calculated systematically, and the screws are included in the product package. We prefabricate the wall panels, joists, and

trusses in the factory, eliminating the need for on-site manual labor to measure stud intervals and drill holes for metal stud connection.

These two traditional metal studs profile manufacturers have a nationwide retail network that we cannot compete with. We are using the

Internet to increase the marginal effect of sales, and our future strategy is to use Internet sales to undermine traditional store-based

sales.

In

the cold-formed roller machine market, FRAMECAD is a traditional LGS/CFS machine manufacturer. When compared to their LGS equipment,

INNO CNC machines manufacturing cost is approximately 50% less, based on our estimates. INNO CNC machines currently have three pending

patents, the CUBE 200 (Application number: 63437142), CUBE 300 (Application number: 63427583) and NEW OPTIMIZED DESIGN FOR ROLL FORMER

CNC MACHINE (Application number: 63427583). CUBE 200 is able to form C& U type studs and tracks in the thickness of 16 gauge and

6 inches width studs. CUBE 300 is able to form C&U type studs in the thickness of 12 gauge and 12 inches width studs.

In

addition, mobile factories are an important countermeasure to traditional equipment. We have developed a mobile factory for offsite production

of steel pieces and structures that compete in the traditional prefab and modular building markets. INNO differentiates itself from other

steel framing companies and cold-formed roller machine suppliers by integrating services ranging from metal stud manufacturing to prefabrication.

In this context, we distinguish ourselves through the technologies and innovations we bring to our process and methods for producing

structural components from rolled steel into useful pieces that assemble without error.

3D

“Printing” Technology

Currently,

3D printing technology is widely used for prefab homes; however, cooling time is required for formation because the technical principle

is to melt the material and then wait for it to cool before settling. In contrast to other prefab home companies, which use 3D printing

technology, INNO uses our own cold-formed steel technology to ensure that there is no waiting time for structure formation. 3D printing

necessitates the use of unique liquid raw materials such as LAVACRETE and Light Stone Material (LSM), neither of which are easily accessible.

This could lead to supply chain disruptions and affect delivery time. Furthermore, steel is still commonly used to support the structure