We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Share Name | Share Symbol | Market | Type |

|---|---|---|---|

| Battalion Oil Corporation | AMEX:BATL | AMEX | Common Stock |

| Price Change | % Change | Share Price | High Price | Low Price | Open Price | Shares Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|

| 0.03 | 0.53% | 5.66 | 5.84 | 5.547 | 5.69 | 11,124 | 01:00:00 |

| |

Battalion Oil Corporation

Two Memorial City Plaza 820 Gessner Road, Suite 1100 Houston, Texas 77024 Tel: (832) 538-0300 |

| |

Luminus Management, LLC

Luminus Energy Partners Master Fund, Ltd. c/o of Luminus Management, LLC 1811 Bering Drive, Suite 400 Houston, Texas 77057 Tel: (713) 826-6262 |

| |

Oaktree Capital Group, LLC

Oaktree Fund GP, LLC OCM Holdings I, LLC Oaktree Holdings, LLC OCM HLCN Holdings, L.P. Oaktree Fund GPI, L.P. Oaktree Capital I, L.P. c/o Oak Tree Capital Group, LLC 333 S. Grand Avenue, 28th Floor Los Angeles, California 90071 Tel: (213) 830-6300 |

| |

Ruckus Energy Holdings, LLC

Fury Resources, Inc. Richard H. Little c/o K&L Gates LLP 1 Park Plaza, Twelfth Floor Irvine, CA 92614 |

|

| |

Bruce F. Perce

Ryan H. Ferris Mayer Brown LLP 71 South Wacker Drive Chicago, IL 60606 Tel: (312) 782-0600 |

| |

David B. Cosgrove

Dechert LLP 300 South Tryon Street, Suite 800 Charlotte, NC 28202 Tel: (704) 339-3147 |

| |

Michael A. Hedge

Jason C. Dreibelbis K&L Gates LLP 1 Park Plaza, Twelfth Floor Irvine, CA 92614 Tel: (949) 253-0900 |

|

| | BATTALION OIL CORPORATION | | | | | ||||||

| | By: | | |

/s/ Walter R. Mayer

|

| | | | |||

| | | | | Name: | | | Walter R. Mayer | | | | |

| | | | | Title: | | | Senior Vice President, General Counsel and Corporate Secretary | | | | |

| | LUMINUS ENERGY PARTNERS MASTER FUND, LTD. | | | | | ||||||

| | By: | | |

/s/ Jonathan Barrett

|

| | | | |||

| | | | | Name: | | | Jonathan Barrett | | | | |

| | | | | Title: | | |

President of Luminus Management, LLC

|

| | | |

| | LUMINUS MANAGEMENT, LLC | | | | | ||||||

| | By: | | |

/s/ Jonathan Barrett

|

| | | | |||

| | | | | Name: | | | Jonathan Barrett | | | | |

| | | | | Title: | | | President | | | | |

| | By: | | |

/s/ Henry Orren

|

| | | | |||

| | | | | Name: | | | Henry Orren | | | | |

| | | | | Title: | | | Senior Vice President | | | | |

| | By: | | |

/s/ Henry Orren

|

| | | | |||

| | | | | Name: | | | Henry Orren | | | | |

| | | | | Title: | | | Senior Vice President | | | | |

| | By: | | |

/s/ Henry Orren

|

| | | | |||

| | | | | Name: | | | Henry Orren | | | | |

| | | | | Title: | | | Senior Vice President | | | | |

| | By: | | |

/s/ Henry Orren

|

| | | | |||

| | | | | Name: | | | Henry Orren | | | | |

| | | | | Title: | | | Senior Vice President | | | | |

| | By: | | |

/s/ Henry Orren

|

| | | | |||

| | | | | Name: | | | Henry Orren | | | | |

| | | | | Title: | | | Senior Vice President | | | | |

| | By: | | |

/s/ Henry Orren

|

| | | | |||

| | | | | Name: | | | Henry Orren | | | | |

| | | | | Title: | | | Senior Vice President | | | | |

| | By: | | |

/s/ Henry Orren

|

| | | | |||

| | | | | Name: | | | Henry Orren | | | | |

| | | | | Title: | | | Senior Vice President | | | | |

| | By: | | |

/s/ Henry Orren

|

| | | | |||

| | | | | Name: | | | Henry Orren | | | | |

| | | | | Title: | | | Senior Vice President | | | | |

| | By: | | |

/s/ Ariella Fuchs

|

| | | | |||

| | | | | Name: | | | Ariella Fuchs | | | | |

| | | | | Title: | | | President and General Counsel | | | | |

| | By: | | |

/s/ Ariella Fuchs

|

| | | | |||

| | | | | Name: | | | Ariella Fuchs | | | | |

| | | | | Title: | | | President and General Counsel | | | | |

| | | |

/s/ Richard H. Little

|

| | | | ||||

| | | | | Name: | | | Richard H. Little | | | | |

Exhibit 99.(C)(iv)

| Project San Jacinto DISCUSSION MATERIALS FOR THE BOARD OF DIRECTORS OF BATTALION OIL CORPORATION NOVEMBER 4 , 2023 | CONFIDENTIAL | PRELIMINARY DRAFT | SUBJECT TO FURTHER REVIEW |

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Table of Contents 2 Page 1. Executive Summary 3 2. Financial Analyses 8 3. Selected Public Market Observations 29 4. Appendix 34 Weighted Average Cost of Capital Calculation 35 Observed Premiums Paid Analysis 38 Selected Series A Convertible Preferred Stock Terms 41 Glossary of Selected Terms 44 5. Disclaimer 47 |

| Page 1. Executive Summary 3 2. Financial Analyses 8 3. Selected Public Market Observations 29 4. Appendix 34 5. Disclaimer 47 |

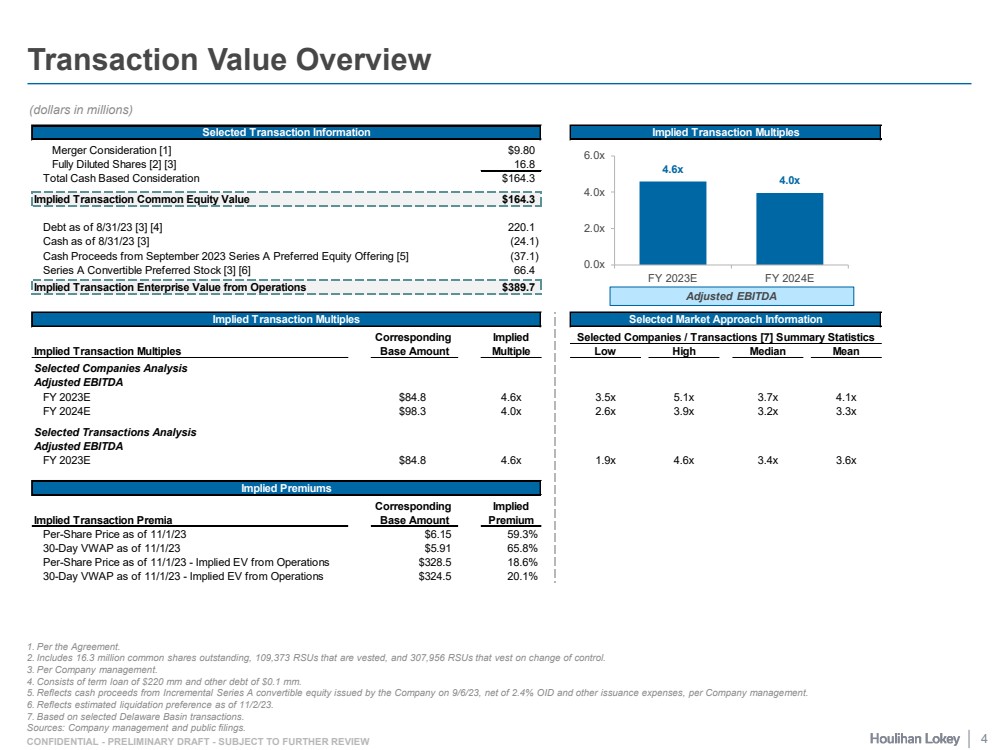

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Transaction Value Overview 1. Per the Agreement. 2. Includes 16.3 million common shares outstanding, 109,373 RSUs that are vested, and 307,956 RSUs that vest on change of control. 3. Per Company management. 4. Consists of term loan of $220 mm and other debt of $0.1 mm. 5. Reflects cash proceeds from Incremental Series A convertible equity issued by the Company on 9/6/23, net of 2.4% OID and other issuance expenses, per Company management. 6. Reflects estimated liquidation preference as of 11/2/23. 7. Based on selected Delaware Basin transactions. Sources: Company management and public filings. (dollars in millions) Selected Transaction Information Implied Transaction Multiples Merger Consideration [1] $9.80 Fully Diluted Shares [2] [3] 16.8 Total Cash Based Consideration $164.3 Implied Transaction Common Equity Value $164.3 Debt as of 8/31/23 [3] [4] 220.1 Cash as of 8/31/23 [3] (24.1) Cash Proceeds from September 2023 Series A Preferred Equity Offering [5] (37.1) Series A Convertible Preferred Stock [3] [6] 66.4 Implied Transaction Enterprise Value from Operations $389.7 Implied Transaction Multiples Selected Market Approach Information Corresponding Implied Selected Companies / Transactions [7] Summary Statistics Implied Transaction Multiples Base Amount Multiple Low High Median Mean Selected Companies Analysis Adjusted EBITDA FY 2023E $84.8 4.6x 3.5x 5.1x 3.7x 4.1x FY 2024E $98.3 4.0x 2.6x 3.9x 3.2x 3.3x Selected Transactions Analysis Adjusted EBITDA FY 2023E $84.8 4.6x 1.9x 4.6x 3.4x 3.6x Implied Premiums Corresponding Implied Implied Transaction Premia Base Amount Premium Per-Share Price as of 11/1/23 $6.15 59.3% 30-Day VWAP as of 11/1/23 $5.91 65.8% Per-Share Price as of 11/1/23 - Implied EV from Operations $328.5 18.6% 30-Day VWAP as of 11/1/23 - Implied EV from Operations $324.5 20.1% 4.6x 4.0x 0.0x 2.0x 4.0x 6.0x FY 2023E FY 2024E Adjusted EBITDA 4 |

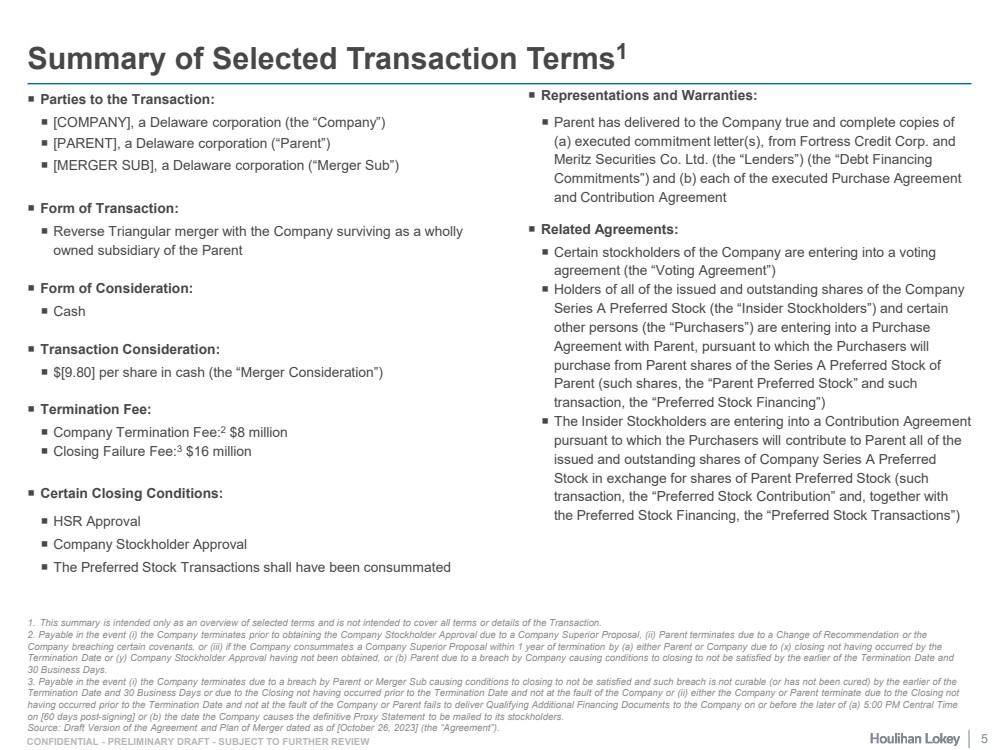

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Parties to the Transaction: [COMPANY], a Delaware corporation (the “Company”) [PARENT], a Delaware corporation (“Parent”) [MERGER SUB], a Delaware corporation (“Merger Sub”) Form of Transaction: Reverse Triangular merger with the Company surviving as a wholly owned subsidiary of the Parent Form of Consideration: Cash Transaction Consideration: $[9.80] per share in cash (the “Merger Consideration”) Termination Fee: Company Termination Fee:2 $8 million Closing Failure Fee:3 $16 million Certain Closing Conditions: HSR Approval Company Stockholder Approval The Preferred Stock Transactions shall have been consummated Representations and Warranties: Parent has delivered to the Company true and complete copies of (a) executed commitment letter(s), from Fortress Credit Corp. and Meritz Securities Co. Ltd. (the “Lenders”) (the “Debt Financing Commitments”) and (b) each of the executed Purchase Agreement and Contribution Agreement Related Agreements: Certain stockholders of the Company are entering into a voting agreement (the “Voting Agreement”) Holders of all of the issued and outstanding shares of the Company Series A Preferred Stock (the “Insider Stockholders”) and certain other persons (the “Purchasers”) are entering into a Purchase Agreement with Parent, pursuant to which the Purchasers will purchase from Parent shares of the Series A Preferred Stock of Parent (such shares, the “Parent Preferred Stock” and such transaction, the “Preferred Stock Financing”) The Insider Stockholders are entering into a Contribution Agreement pursuant to which the Purchasers will contribute to Parent all of the issued and outstanding shares of Company Series A Preferred Stock in exchange for shares of Parent Preferred Stock (such transaction, the “Preferred Stock Contribution” and, together with the Preferred Stock Financing, the “Preferred Stock Transactions”) Summary of Selected Transaction Terms1 1. This summary is intended only as an overview of selected terms and is not intended to cover all terms or details of the Transaction. 2. Payable in the event (i) the Company terminates prior to obtaining the Company Stockholder Approval due to a Company Superior Proposal, (ii) Parent terminates due to a Change of Recommendation or the Company breaching certain covenants, or (iii) if the Company consummates a Company Superior Proposal within 1 year of termination by (a) either Parent or Company due to (x) closing not having occurred by the Termination Date or (y) Company Stockholder Approval having not been obtained, or (b) Parent due to a breach by Company causing conditions to closing to not be satisfied by the earlier of the Termination Date and 30 Business Days. 3. Payable in the event (i) the Company terminates due to a breach by Parent or Merger Sub causing conditions to closing to not be satisfied and such breach is not curable (or has not been cured) by the earlier of the Termination Date and 30 Business Days or due to the Closing not having occurred prior to the Termination Date and not at the fault of the Company or (ii) either the Company or Parent terminate due to the Closing not having occurred prior to the Termination Date and not at the fault of the Company or Parent fails to deliver Qualifying Additional Financing Documents to the Company on or before the later of (a) 5:00 PM Central Time on [60 days post-signing] or (b) the date the Company causes the definitive Proxy Statement to be mailed to its stockholders. Source: Draft Version of the Agreement and Plan of Merger dated as of [October 26, 2023] (the “Agreement”). 5 |

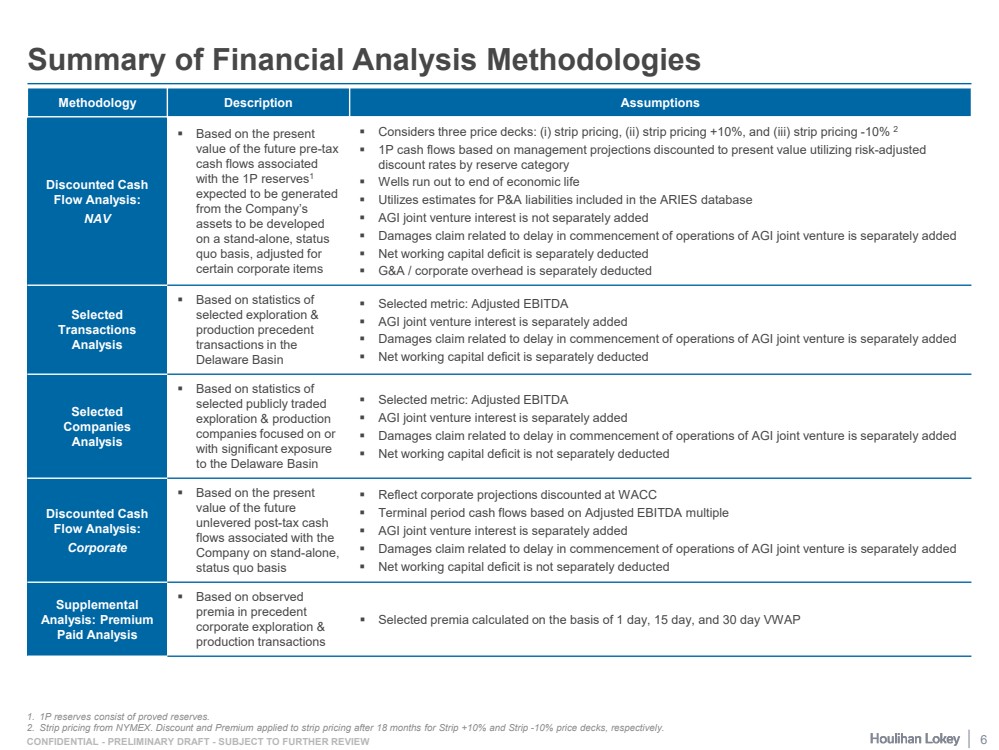

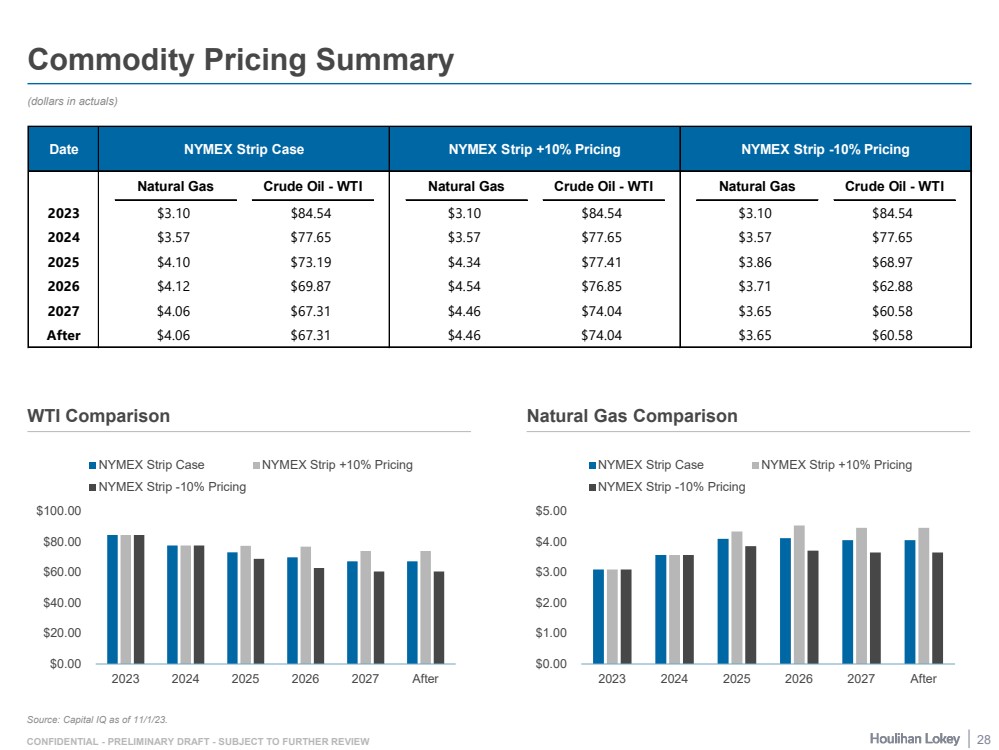

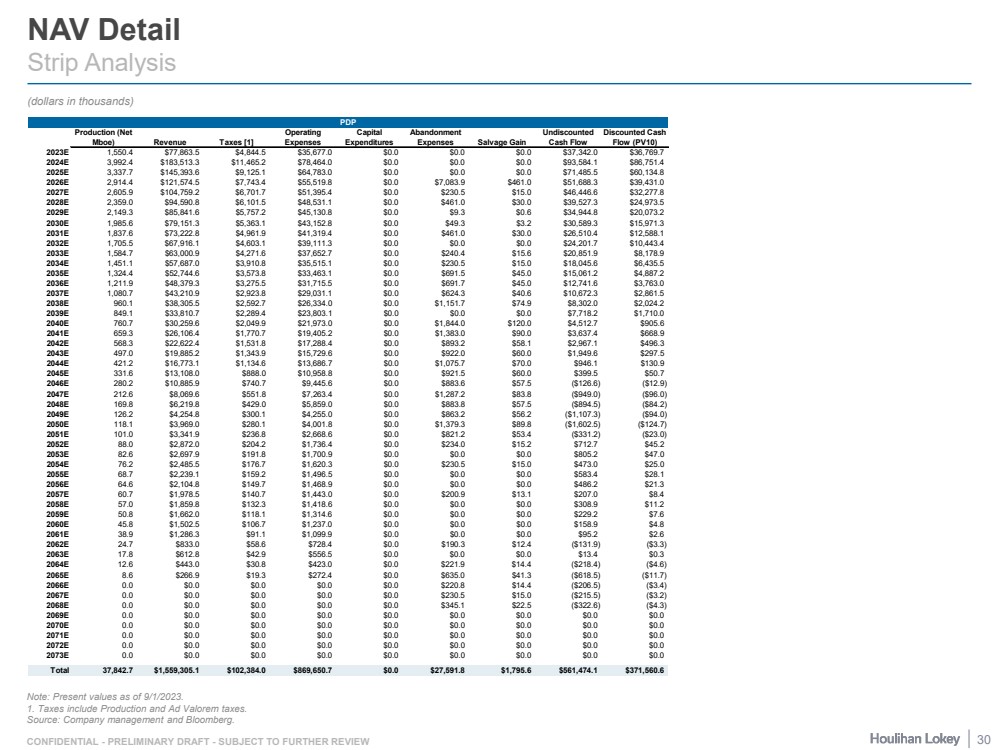

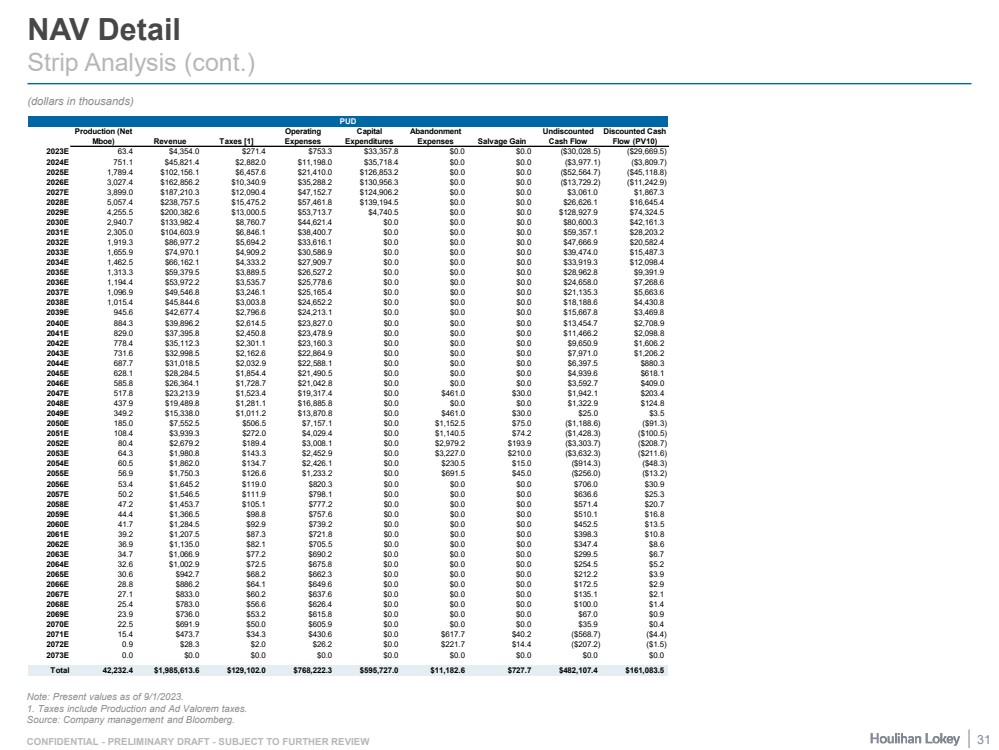

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Summary of Financial Analysis Methodologies Methodology Description Assumptions Discounted Cash Flow Analysis: NAV Based on the present value of the future pre-tax cash flows associated with the 1P reserves1 expected to be generated from the Company’s assets to be developed on a stand-alone, status quo basis, adjusted for certain corporate items Considers three price decks: (i) strip pricing, (ii) strip pricing +10%, and (iii) strip pricing -10% 2 1P cash flows based on management projections discounted to present value utilizing risk-adjusted discount rates by reserve category Wells run out to end of economic life Utilizes estimates for P&A liabilities included in the ARIES database AGI joint venture interest is not separately added Damages claim related to delay in commencement of operations of AGI joint venture is separately added Net working capital deficit is separately deducted G&A / corporate overhead is separately deducted Selected Transactions Analysis Based on statistics of selected exploration & production precedent transactions in the Delaware Basin Selected metric: Adjusted EBITDA AGI joint venture interest is separately added Damages claim related to delay in commencement of operations of AGI joint venture is separately added Net working capital deficit is separately deducted Selected Companies Analysis Based on statistics of selected publicly traded exploration & production companies focused on or with significant exposure to the Delaware Basin Selected metric: Adjusted EBITDA AGI joint venture interest is separately added Damages claim related to delay in commencement of operations of AGI joint venture is separately added Net working capital deficit is not separately deducted Discounted Cash Flow Analysis: Corporate Based on the present value of the future unlevered post-tax cash flows associated with the Company on stand-alone, status quo basis Reflect corporate projections discounted at WACC Terminal period cash flows based on Adjusted EBITDA multiple AGI joint venture interest is separately added Damages claim related to delay in commencement of operations of AGI joint venture is separately added Net working capital deficit is not separately deducted Supplemental Analysis: Premium Paid Analysis Based on observed premia in precedent corporate exploration & production transactions Selected premia calculated on the basis of 1 day, 15 day, and 30 day VWAP 1. 1P reserves consist of proved reserves. 2. Strip pricing from NYMEX. Discount and Premium applied to strip pricing after 18 months for Strip +10% and Strip -10% price decks, respectively. 6 |

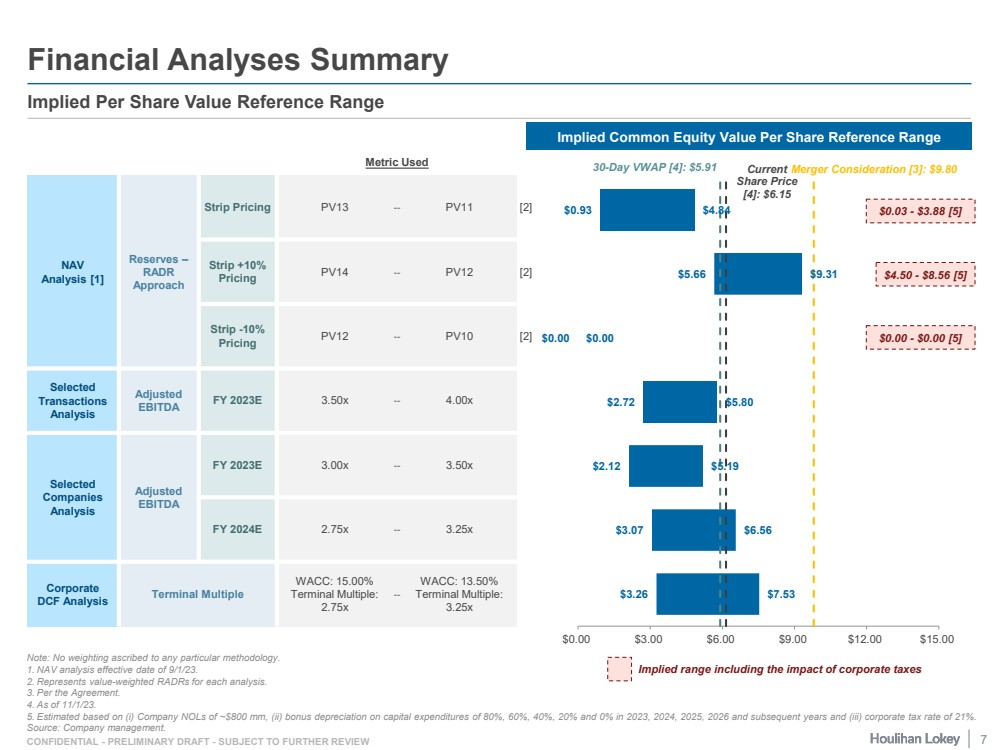

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Note: No weighting ascribed to any particular methodology. 1. NAV analysis effective date of 9/1/23. 2. Represents value-weighted RADRs for each analysis. 3. Per the Agreement. 4. As of 11/1/23. 5. Estimated based on (i) Company NOLs of ~$800 mm, (ii) bonus depreciation on capital expenditures of 80%, 60%, 40%, 20% and 0% in 2023, 2024, 2025, 2026 and subsequent years and (iii) corporate tax rate of 21%. Source: Company management. Financial Analyses Summary Implied Per Share Value Reference Range Metric Used NAV Analysis [1] Reserves – RADR Approach Strip Pricing PV13 -- PV11 [2] Strip +10% Pricing PV14 -- PV12 [2] Strip -10% Pricing PV12 -- PV10 [2] Selected Transactions Analysis Adjusted EBITDA FY 2023E 3.50x -- 4.00x Selected Companies Analysis Adjusted EBITDA FY 2023E 3.00x -- 3.50x FY 2024E 2.75x -- 3.25x Corporate DCF Analysis Terminal Multiple WACC: 15.00% Terminal Multiple: 2.75x -- WACC: 13.50% Terminal Multiple: 3.25x Implied Common Equity Value Per Share Reference Range $4.50 - $8.56 [5] $0.03 - $3.88 [5] $0.00 - $0.00 [5] Implied range including the impact of corporate taxes $3.26 $3.07 $2.12 $2.72 $0.00 $5.66 $0.93 $7.53 $6.56 $5.19 $5.80 $0.00 $9.31 $4.84 Current Merger Consideration [3]: $9.80 Share Price [4]: $6.15 30-Day VWAP [4]: $5.91 $0.00 $3.00 $6.00 $9.00 $12.00 $15.00 7 |

| Page 1. Executive Summary 3 2. Financial Analyses 8 3. Selected Public Market Observations 29 4. Appendix 34 5. Disclaimer 47 |

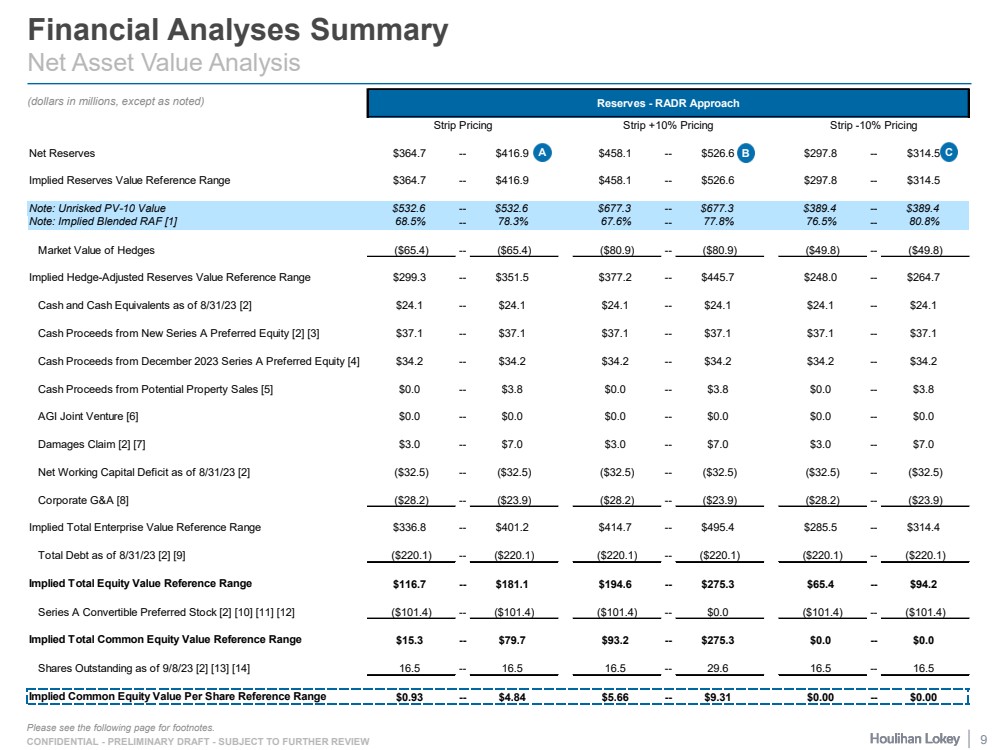

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Financial Analyses Summary Net Asset Value Analysis Please see the following page for footnotes. (dollars in millions, except as noted) Reserves - RADR Approach Strip Pricing Strip +10% Pricing Strip -10% Pricing Net Reserves $364.7 -- $416.9 $458.1 -- $526.6 $297.8 -- $314.5 Implied Reserves Value Reference Range $364.7 -- $416.9 $458.1 -- $526.6 $297.8 -- $314.5 Note: Unrisked PV-10 Value $532.6 -- $532.6 $677.3 -- $677.3 $389.4 -- $389.4 Note: Implied Blended RAF [1] 68.5% -- 78.3% 67.6% -- 77.8% 76.5% -- 80.8% Market Value of Hedges ($65.4) -- ($65.4) ($80.9) -- ($80.9) ($49.8) -- ($49.8) Implied Hedge-Adjusted Reserves Value Reference Range $299.3 -- $351.5 $377.2 -- $445.7 $248.0 -- $264.7 Cash and Cash Equivalents as of 8/31/23 [2] $24.1 -- $24.1 $24.1 -- $24.1 $24.1 -- $24.1 Cash Proceeds from New Series A Preferred Equity [2] [3] $37.1 -- $37.1 $37.1 -- $37.1 $37.1 -- $37.1 Cash Proceeds from December 2023 Series A Preferred Equity [4] $34.2 -- $34.2 $34.2 -- $34.2 $34.2 -- $34.2 Cash Proceeds from Potential Property Sales [5] $0.0 -- $3.8 $0.0 -- $3.8 $0.0 -- $3.8 AGI Joint Venture [6] $0.0 -- $0.0 $0.0 -- $0.0 $0.0 -- $0.0 Damages Claim [2] [7] $3.0 -- $7.0 $3.0 -- $7.0 $3.0 -- $7.0 Net Working Capital Deficit as of 8/31/23 [2] ($32.5) -- ($32.5) ($32.5) -- ($32.5) ($32.5) -- ($32.5) Corporate G&A [8] ($28.2) -- ($23.9) ($28.2) -- ($23.9) ($28.2) -- ($23.9) Implied Total Enterprise Value Reference Range $336.8 -- $401.2 $414.7 -- $495.4 $285.5 -- $314.4 Total Debt as of 8/31/23 [2] [9] ($220.1) -- ($220.1) ($220.1) -- ($220.1) ($220.1) -- ($220.1) Implied Total Equity Value Reference Range $116.7 -- $181.1 $194.6 -- $275.3 $65.4 -- $94.2 Series A Convertible Preferred Stock [2] [10] [11] [12] ($101.4) -- ($101.4) ($101.4) -- $0.0 ($101.4) -- ($101.4) Implied Total Common Equity Value Reference Range $15.3 -- $79.7 $93.2 -- $275.3 $0.0 -- $0.0 Shares Outstanding as of 9/8/23 [2] [13] [14] 16.5 -- 16.5 16.5 -- 29.6 16.5 -- 16.5 Implied Common Equity Value Per Share Reference Range $0.93 -- $4.84 $5.66 -- $9.31 $0.00 -- $0.00 A B C 9 |

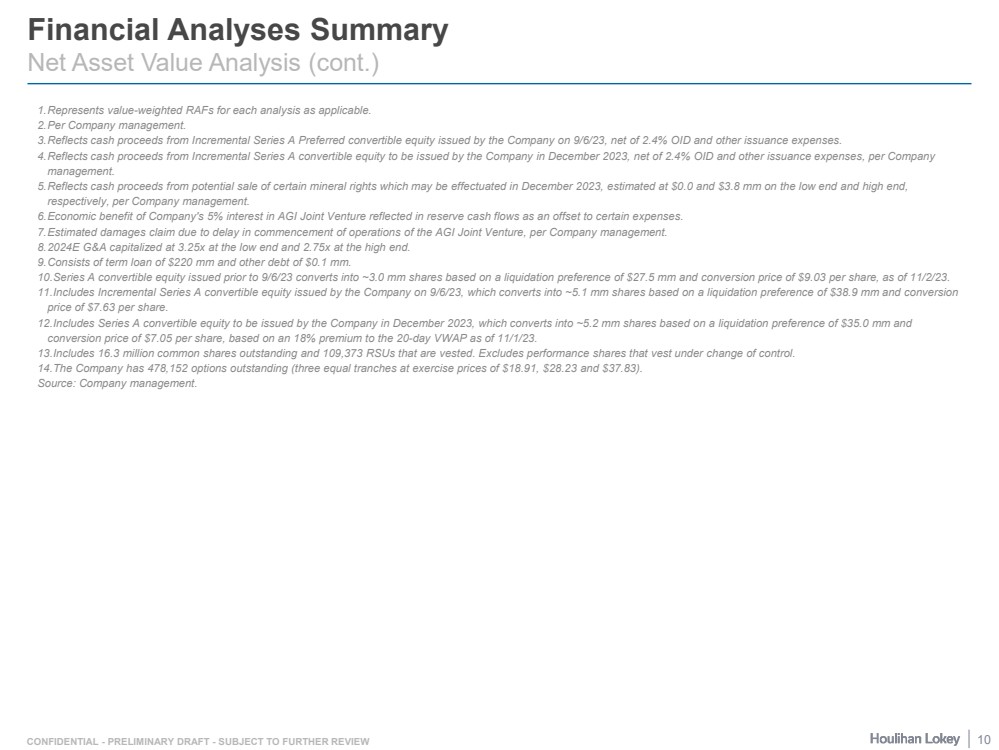

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Financial Analyses Summary Net Asset Value Analysis (cont.) 1.Represents value-weighted RAFs for each analysis as applicable. 2.Per Company management. 3.Reflects cash proceeds from Incremental Series A Preferred convertible equity issued by the Company on 9/6/23, net of 2.4% OID and other issuance expenses. 4.Reflects cash proceeds from Incremental Series A convertible equity to be issued by the Company in December 2023, net of 2.4% OID and other issuance expenses, per Company management. 5.Reflects cash proceeds from potential sale of certain mineral rights which may be effectuated in December 2023, estimated at $0.0 and $3.8 mm on the low end and high end, respectively, per Company management. 6.Economic benefit of Company's 5% interest in AGI Joint Venture reflected in reserve cash flows as an offset to certain expenses. 7.Estimated damages claim due to delay in commencement of operations of the AGI Joint Venture, per Company management. 8.2024E G&A capitalized at 3.25x at the low end and 2.75x at the high end. 9.Consists of term loan of $220 mm and other debt of $0.1 mm. 10.Series A convertible equity issued prior to 9/6/23 converts into ~3.0 mm shares based on a liquidation preference of $27.5 mm and conversion price of $9.03 per share, as of 11/2/23. 11.Includes Incremental Series A convertible equity issued by the Company on 9/6/23, which converts into ~5.1 mm shares based on a liquidation preference of $38.9 mm and conversion price of $7.63 per share. 12.Includes Series A convertible equity to be issued by the Company in December 2023, which converts into ~5.2 mm shares based on a liquidation preference of $35.0 mm and conversion price of $7.05 per share, based on an 18% premium to the 20-day VWAP as of 11/1/23. 13.Includes 16.3 million common shares outstanding and 109,373 RSUs that are vested. Excludes performance shares that vest under change of control. 14.The Company has 478,152 options outstanding (three equal tranches at exercise prices of $18.91, $28.23 and $37.83). Source: Company management. 10 |

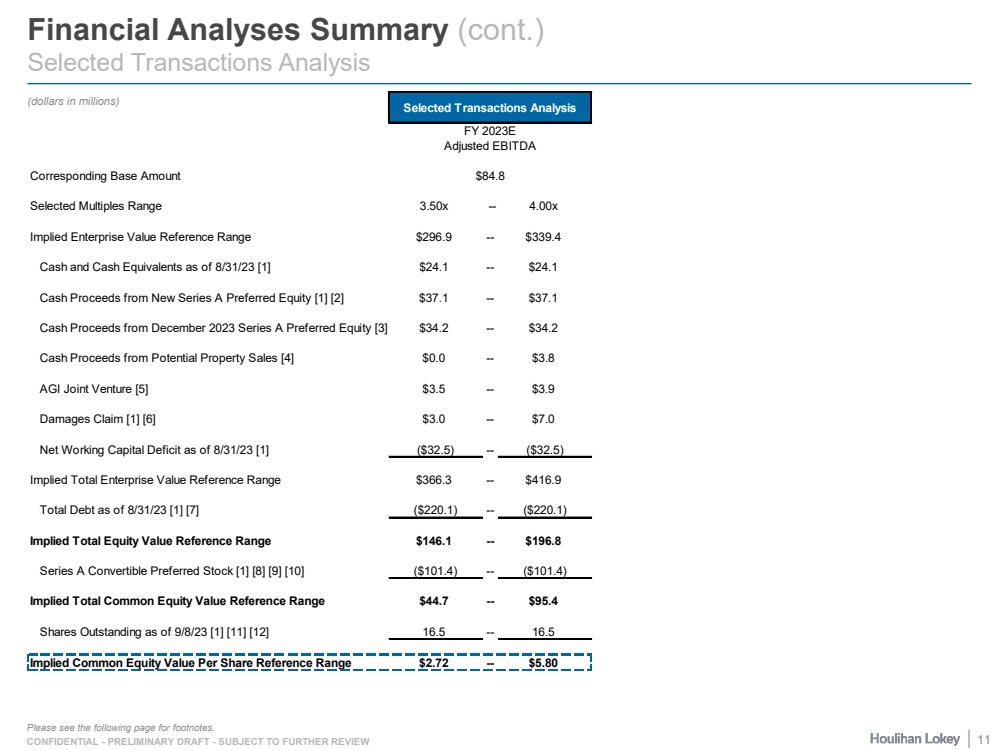

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Financial Analyses Summary (cont.) Selected Transactions Analysis (dollars in millions) Please see the following page for footnotes. Selected Transactions Analysis FY 2023E Adjusted EBITDA Corresponding Base Amount $84.8 Selected Multiples Range 3.50x -- 4.00x Implied Enterprise Value Reference Range $296.9 -- $339.4 Cash and Cash Equivalents as of 8/31/23 [1] $24.1 -- $24.1 Cash Proceeds from New Series A Preferred Equity [1] [2] $37.1 -- $37.1 Cash Proceeds from December 2023 Series A Preferred Equity [3] $34.2 -- $34.2 Cash Proceeds from Potential Property Sales [4] $0.0 -- $3.8 AGI Joint Venture [5] $3.5 -- $3.9 Damages Claim [1] [6] $3.0 -- $7.0 Net Working Capital Deficit as of 8/31/23 [1] ($32.5) -- ($32.5) Implied Total Enterprise Value Reference Range $366.3 -- $416.9 Total Debt as of 8/31/23 [1] [7] ($220.1) -- ($220.1) Implied Total Equity Value Reference Range $146.1 -- $196.8 Series A Convertible Preferred Stock [1] [8] [9] [10] ($101.4) -- ($101.4) Implied Total Common Equity Value Reference Range $44.7 -- $95.4 Shares Outstanding as of 9/8/23 [1] [11] [12] 16.5 -- 16.5 Implied Common Equity Value Per Share Reference Range $2.72 -- $5.80 11 |

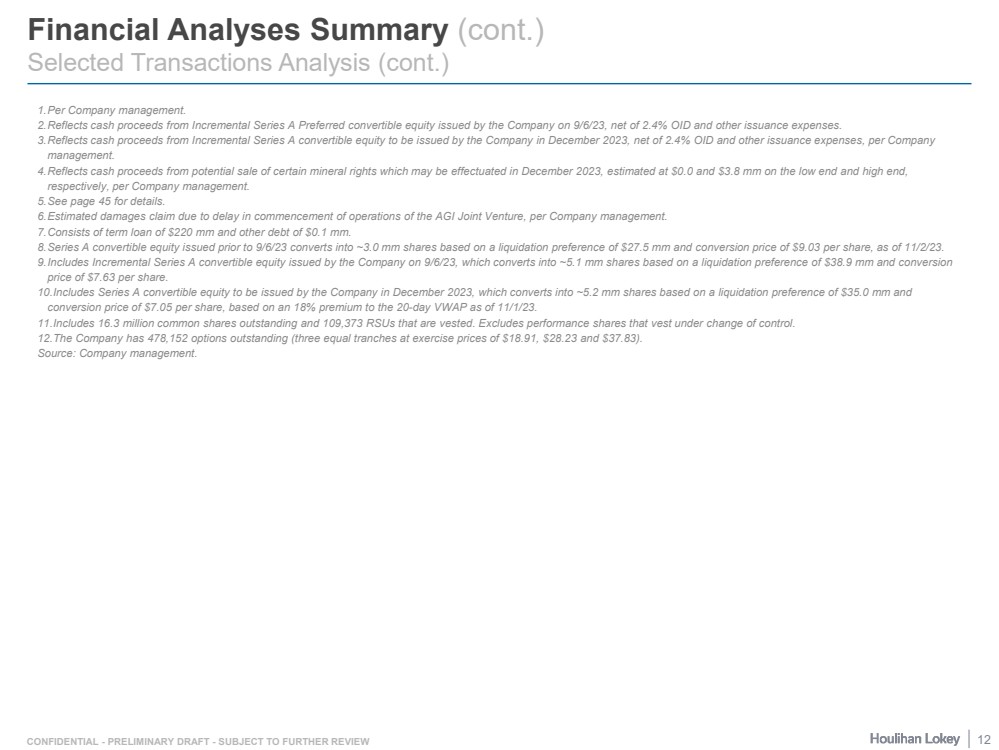

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Financial Analyses Summary (cont.) Selected Transactions Analysis (cont.) 1.Per Company management. 2.Reflects cash proceeds from Incremental Series A Preferred convertible equity issued by the Company on 9/6/23, net of 2.4% OID and other issuance expenses. 3.Reflects cash proceeds from Incremental Series A convertible equity to be issued by the Company in December 2023, net of 2.4% OID and other issuance expenses, per Company management. 4.Reflects cash proceeds from potential sale of certain mineral rights which may be effectuated in December 2023, estimated at $0.0 and $3.8 mm on the low end and high end, respectively, per Company management. 5.See page 45 for details. 6.Estimated damages claim due to delay in commencement of operations of the AGI Joint Venture, per Company management. 7.Consists of term loan of $220 mm and other debt of $0.1 mm. 8.Series A convertible equity issued prior to 9/6/23 converts into ~3.0 mm shares based on a liquidation preference of $27.5 mm and conversion price of $9.03 per share, as of 11/2/23. 9.Includes Incremental Series A convertible equity issued by the Company on 9/6/23, which converts into ~5.1 mm shares based on a liquidation preference of $38.9 mm and conversion price of $7.63 per share. 10.Includes Series A convertible equity to be issued by the Company in December 2023, which converts into ~5.2 mm shares based on a liquidation preference of $35.0 mm and conversion price of $7.05 per share, based on an 18% premium to the 20-day VWAP as of 11/1/23. 11.Includes 16.3 million common shares outstanding and 109,373 RSUs that are vested. Excludes performance shares that vest under change of control. 12.The Company has 478,152 options outstanding (three equal tranches at exercise prices of $18.91, $28.23 and $37.83). Source: Company management. 12 |

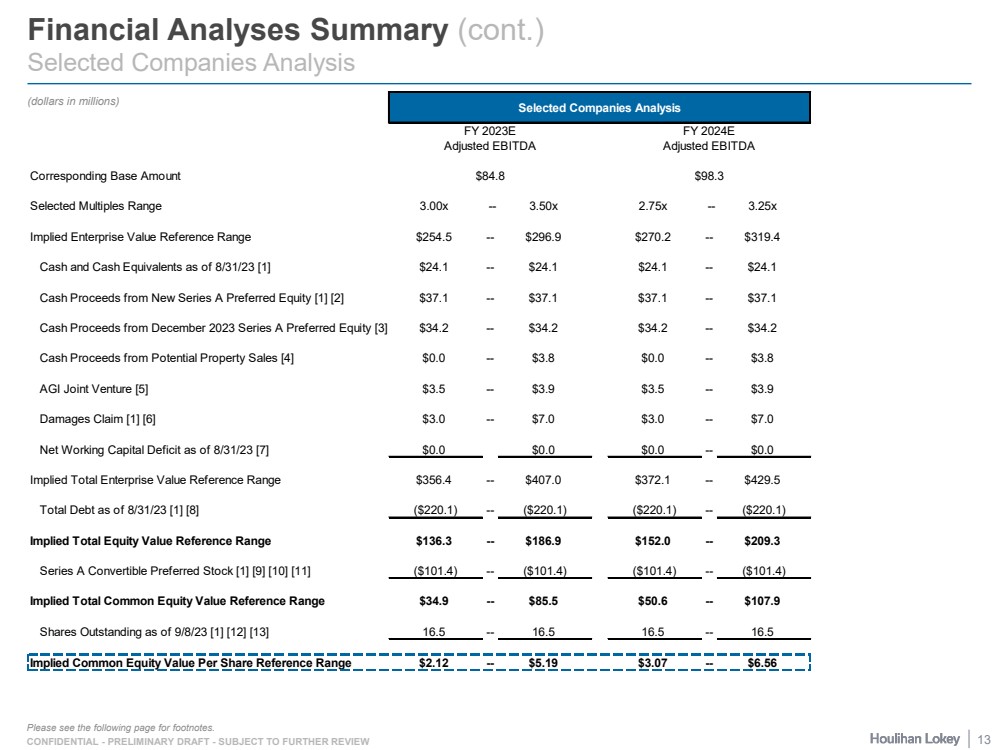

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Financial Analyses Summary (cont.) Selected Companies Analysis (dollars in millions) Please see the following page for footnotes. Selected Companies Analysis FY 2023E FY 2024E Adjusted EBITDA Adjusted EBITDA Corresponding Base Amount $84.8 $98.3 Selected Multiples Range 3.00x -- 3.50x 2.75x -- 3.25x Implied Enterprise Value Reference Range $254.5 -- $296.9 $270.2 -- $319.4 Cash and Cash Equivalents as of 8/31/23 [1] $24.1 -- $24.1 $24.1 -- $24.1 Cash Proceeds from New Series A Preferred Equity [1] [2] $37.1 -- $37.1 $37.1 -- $37.1 Cash Proceeds from December 2023 Series A Preferred Equity [3] $34.2 -- $34.2 $34.2 -- $34.2 Cash Proceeds from Potential Property Sales [4] $0.0 -- $3.8 $0.0 -- $3.8 AGI Joint Venture [5] $3.5 -- $3.9 $3.5 -- $3.9 Damages Claim [1] [6] $3.0 -- $7.0 $3.0 -- $7.0 Net Working Capital Deficit as of 8/31/23 [7] $0.0 $0.0 $0.0 -- $0.0 Implied Total Enterprise Value Reference Range $356.4 -- $407.0 $372.1 -- $429.5 Total Debt as of 8/31/23 [1] [8] ($220.1) -- ($220.1) ($220.1) -- ($220.1) Implied Total Equity Value Reference Range $136.3 -- $186.9 $152.0 -- $209.3 Series A Convertible Preferred Stock [1] [9] [10] [11] ($101.4) -- ($101.4) ($101.4) -- ($101.4) Implied Total Common Equity Value Reference Range $34.9 -- $85.5 $50.6 -- $107.9 Shares Outstanding as of 9/8/23 [1] [12] [13] 16.5 -- 16.5 16.5 -- 16.5 Implied Common Equity Value Per Share Reference Range $2.12 -- $5.19 $3.07 -- $6.56 13 |

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Financial Analyses Summary (cont.) Selected Companies Analysis (cont.) 1. Per Company management. 2.Reflects cash proceeds from Incremental Series A Preferred convertible equity issued by the Company on 9/6/23, net of 2.4% OID and other issuance expenses. 3.Reflects cash proceeds from Incremental Series A convertible equity to be issued by the Company in December 2023, net of 2.4% OID and other issuance expenses, per Company management. 4.Reflects cash proceeds from potential sale of certain mineral rights which may be effectuated in December 2023, estimated at $0.0 and $3.8 mm on the low end and high end, respectively, per Company management. 5.See page 45 for details. 6.Estimated damages claim due to delay in commencement of operations of the AGI Joint Venture, per Company management. 7.Company net working capital deficit is in-line with public peers. 8.Consists of term loan of $220 mm and other debt of $0.1 mm. 9.Series A convertible equity issued prior to 9/6/23 converts into ~3.0 mm shares based on a liquidation preference of $27.5 mm and conversion price of $9.03 per share, as of 11/2/23. 10.Includes Incremental Series A convertible equity issued by the Company on 9/6/23, which converts into ~5.1 mm shares based on a liquidation preference of $38.9 mm and conversion price of $7.63 per share. 11.Includes Series A convertible equity to be issued by the Company in December 2023, which converts into ~5.2 mm shares based on a liquidation preference of $35.0 mm and conversion price of $7.05 per share, based on an 18% premium to the 20-day VWAP as of 11/1/23. 12.Includes 16.3 million common shares outstanding and 109,373 RSUs that are vested. Excludes performance shares that vest under change of control. 13.The Company has 478,152 options outstanding (three equal tranches at exercise prices of $18.91, $28.23 and $37.83). Source: Company management 14 |

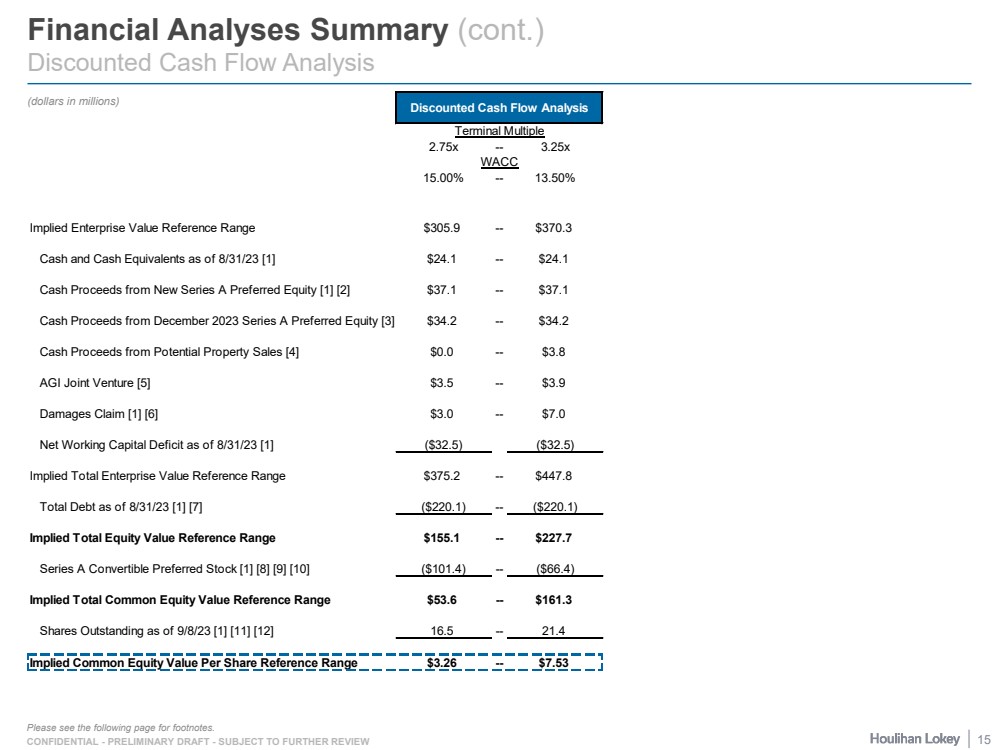

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Financial Analyses Summary (cont.) Discounted Cash Flow Analysis (dollars in millions) Please see the following page for footnotes. Discounted Cash Flow Analysis Terminal Multiple 2.75x -- 3.25x WACC 15.00% -- 13.50% Implied Enterprise Value Reference Range $305.9 -- $370.3 Cash and Cash Equivalents as of 8/31/23 [1] $24.1 -- $24.1 Cash Proceeds from New Series A Preferred Equity [1] [2] $37.1 -- $37.1 Cash Proceeds from December 2023 Series A Preferred Equity [3] $34.2 -- $34.2 Cash Proceeds from Potential Property Sales [4] $0.0 -- $3.8 AGI Joint Venture [5] $3.5 -- $3.9 Damages Claim [1] [6] $3.0 -- $7.0 Net Working Capital Deficit as of 8/31/23 [1] ($32.5) ($32.5) Implied Total Enterprise Value Reference Range $375.2 -- $447.8 Total Debt as of 8/31/23 [1] [7] ($220.1) -- ($220.1) Implied Total Equity Value Reference Range $155.1 -- $227.7 Series A Convertible Preferred Stock [1] [8] [9] [10] ($101.4) -- ($66.4) Implied Total Common Equity Value Reference Range $53.6 -- $161.3 Shares Outstanding as of 9/8/23 [1] [11] [12] 16.5 -- 21.4 Implied Common Equity Value Per Share Reference Range $3.26 -- $7.53 15 |

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Financial Analyses Summary (cont.) Discounted Cash Flow Analysis (cont.) 1.Per Company management. 2.Reflects cash proceeds from Incremental Series A Preferred convertible equity issued by the Company on 9/6/23, net of 2.4% OID and other issuance expenses. 3.Reflects cash proceeds from Incremental Series A convertible equity to be issued by the Company in December 2023, net of 2.4% OID and other issuance expenses, per Company management. 4.Reflects cash proceeds from potential sale of certain mineral rights which may be effectuated in December 2023, estimated at $0.0 and $3.8 mm on the low end and high end, respectively, per Company management. 5.See page 45 for details. 6.Estimated damages claim due to delay in commencement of operations of the AGI Joint Venture, per Company management. 7.Consists of term loan of $220 mm and other debt of $0.1 mm. 8.Series A convertible equity issued prior to 9/6/23 converts into ~3.0 mm shares based on a liquidation preference of $27.5 mm and conversion price of $9.03 per share, as of 11/2/23. 9.Includes Incremental Series A convertible equity issued by the Company on 9/6/23, which converts into ~5.1 mm shares based on a liquidation preference of $38.9 mm and conversion price of $7.63 per share. 10.Includes Series A convertible equity to be issued by the Company in December 2023, which converts into ~5.2 mm shares based on a liquidation preference of $35.0 mm and conversion price of $7.05 per share, based on an 18% premium to the 20-day VWAP as of 11/1/23. 11.Includes 16.3 million common shares outstanding and 109,373 RSUs that are vested. Excludes performance shares that vest under change of control. 12.The Company has 478,152 options outstanding (three equal tranches at exercise prices of $18.91, $28.23 and $37.83). Source: Company management. 16 |

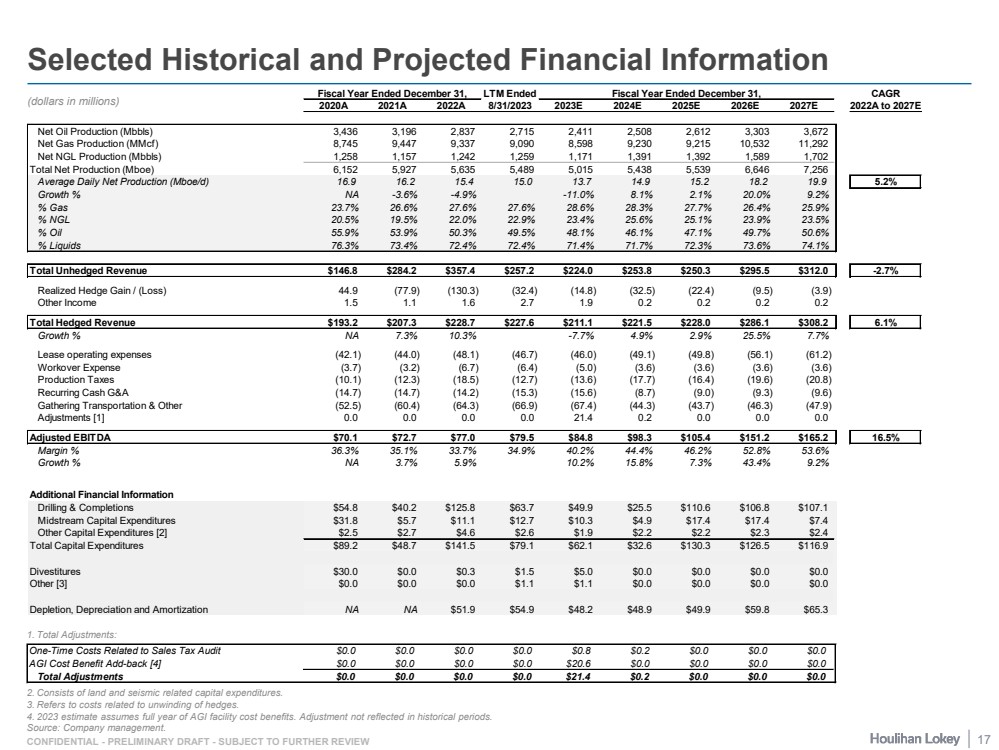

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Selected Historical and Projected Financial Information 1. Total Adjustments: 2. Consists of land and seismic related capital expenditures. 3. Refers to costs related to unwinding of hedges. 4. 2023 estimate assumes full year of AGI facility cost benefits. Adjustment not reflected in historical periods. Source: Company management. (dollars in millions) One-Time Costs Related to Sales Tax Audit $0.0 $0.0 $0.0 $0.0 $0.8 $0.2 $0.0 $0.0 $0.0 AGI Cost Benefit Add-back [4] $0.0 $0.0 $0.0 $0.0 $20.6 $0.0 $0.0 $0.0 $0.0 Total Adjustments $0.0 $0.0 $0.0 $0.0 $21.4 $0.2 $0.0 $0.0 $0.0 Fiscal Year Ended December 31, LTM Ended Fiscal Year Ended December 31, CAGR 2020A 2021A 2022A 8/31/2023 2023E 2024E 2025E 2026E 2027E 2022A to 2027E Net Oil Production (Mbbls) 3,436 3,196 2,837 2,715 2,411 2,508 2,612 3,303 3,672 Net Gas Production (MMcf) 8,745 9,447 9,337 9,090 8,598 9,230 9,215 10,532 11,292 Net NGL Production (Mbbls) 1,258 1,157 1,242 1,259 1,171 1,391 1,392 1,589 1,702 Total Net Production (Mboe) 6,152 5,927 5,635 5,489 5,015 5,438 5,539 6,646 7,256 Average Daily Net Production (Mboe/d) 16.9 16.2 15.4 15.0 13.7 14.9 15.2 18.2 19.9 5.2% Growth % NA -3.6% -4.9% -11.0% 8.1% 2.1% 20.0% 9.2% % Gas 23.7% 26.6% 27.6% 27.6% 28.6% 28.3% 27.7% 26.4% 25.9% % NGL 20.5% 19.5% 22.0% 22.9% 23.4% 25.6% 25.1% 23.9% 23.5% % Oil 55.9% 53.9% 50.3% 49.5% 48.1% 46.1% 47.1% 49.7% 50.6% % Liquids 76.3% 73.4% 72.4% 72.4% 71.4% 71.7% 72.3% 73.6% 74.1% Total Unhedged Revenue $146.8 $284.2 $357.4 $257.2 $224.0 $253.8 $250.3 $295.5 $312.0 -2.7% Realized Hedge Gain / (Loss) 44.9 (77.9) (130.3) (32.4) (14.8) (32.5) (22.4) (9.5) (3.9) Other Income 1.5 1.1 1.6 2.7 1.9 0.2 0.2 0.2 0.2 Total Hedged Revenue $193.2 $207.3 $228.7 $227.6 $211.1 $221.5 $228.0 $286.1 $308.2 6.1% Growth % NA 7.3% 10.3% -7.7% 4.9% 2.9% 25.5% 7.7% Lease operating expenses (42.1) (44.0) (48.1) (46.7) (46.0) (49.1) (49.8) (56.1) (61.2) Workover Expense (3.7) (3.2) (6.7) (6.4) (5.0) (3.6) (3.6) (3.6) (3.6) Production Taxes (10.1) (12.3) (18.5) (12.7) (13.6) (17.7) (16.4) (19.6) (20.8) Recurring Cash G&A (14.7) (14.7) (14.2) (15.3) (15.6) (8.7) (9.0) (9.3) (9.6) Gathering Transportation & Other (52.5) (60.4) (64.3) (66.9) (67.4) (44.3) (43.7) (46.3) (47.9) Adjustments [1] 0.0 0.0 0.0 0.0 21.4 0.2 0.0 0.0 0.0 Adjusted EBITDA $70.1 $72.7 $77.0 $79.5 $84.8 $98.3 $105.4 $151.2 $165.2 16.5% Margin % 36.3% 35.1% 33.7% 34.9% 40.2% 44.4% 46.2% 52.8% 53.6% Growth % NA 3.7% 5.9% 10.2% 15.8% 7.3% 43.4% 9.2% Additional Financial Information Drilling & Completions $54.8 $40.2 $125.8 $63.7 $49.9 $25.5 $110.6 $106.8 $107.1 Midstream Capital Expenditures $31.8 $5.7 $11.1 $12.7 $10.3 $4.9 $17.4 $17.4 $7.4 Other Capital Expenditures [2] $2.5 $2.7 $4.6 $2.6 $1.9 $2.2 $2.2 $2.3 $2.4 Total Capital Expenditures $89.2 $48.7 $141.5 $79.1 $62.1 $32.6 $130.3 $126.5 $116.9 Divestitures $30.0 $0.0 $0.3 $1.5 $5.0 $0.0 $0.0 $0.0 $0.0 Other [3] $0.0 $0.0 $0.0 $1.1 $1.1 $0.0 $0.0 $0.0 $0.0 Depletion, Depreciation and Amortization NA NA $51.9 $54.9 $48.2 $48.9 $49.9 $59.8 $65.3 17 |

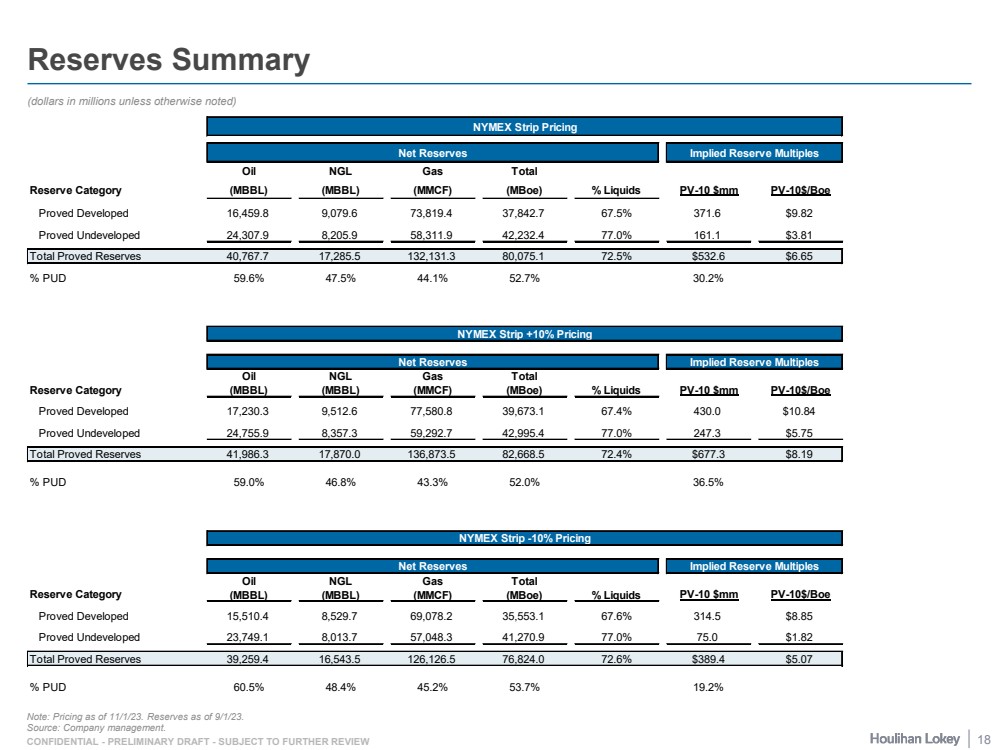

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Reserves Summary (dollars in millions unless otherwise noted) Note: Pricing as of 11/1/23. Reserves as of 9/1/23. Source: Company management. NYMEX Strip Pricing Net Reserves Implied Reserve Multiples Oil NGL Gas Total Reserve Category (MBBL) (MBBL) (MMCF) (MBoe) % Liquids PV-10 $mm PV-10$/Boe Proved Developed 16,459.8 9,079.6 73,819.4 37,842.7 67.5% 371.6 $9.82 Proved Undeveloped 24,307.9 8,205.9 58,311.9 42,232.4 77.0% 161.1 $3.81 Total Proved Reserves 40,767.7 17,285.5 132,131.3 80,075.1 72.5% $532.6 $6.65 % PUD 59.6% 47.5% 44.1% 52.7% 30.2% NYMEX Strip +10% Pricing Net Reserves Implied Reserve Multiples Oil NGL Gas Total Reserve Category (MBBL) (MBBL) (MMCF) (MBoe) % Liquids PV-10 $mm PV-10$/Boe Proved Developed 17,230.3 9,512.6 77,580.8 39,673.1 67.4% 430.0 $10.84 Proved Undeveloped 24,755.9 8,357.3 59,292.7 42,995.4 77.0% 247.3 $5.75 Total Proved Reserves 41,986.3 17,870.0 136,873.5 82,668.5 72.4% $677.3 $8.19 % PUD 59.0% 46.8% 43.3% 52.0% 36.5% NYMEX Strip -10% Pricing Net Reserves Implied Reserve Multiples Oil NGL Gas Total Reserve Category (MBBL) (MBBL) (MMCF) (MBoe) % Liquids PV-10 $mm PV-10$/Boe Proved Developed 15,510.4 8,529.7 69,078.2 35,553.1 67.6% 314.5 $8.85 Proved Undeveloped 23,749.1 8,013.7 57,048.3 41,270.9 77.0% 75.0 $1.82 Total Proved Reserves 39,259.4 16,543.5 126,126.5 76,824.0 72.6% $389.4 $5.07 % PUD 60.5% 48.4% 45.2% 53.7% 19.2% 18 |

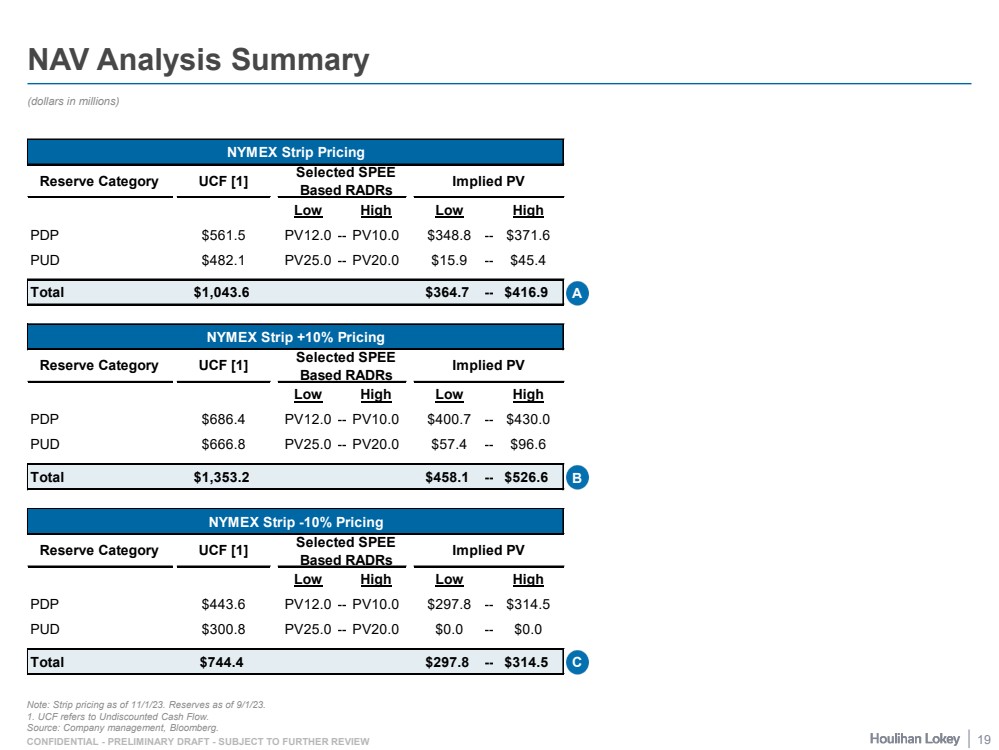

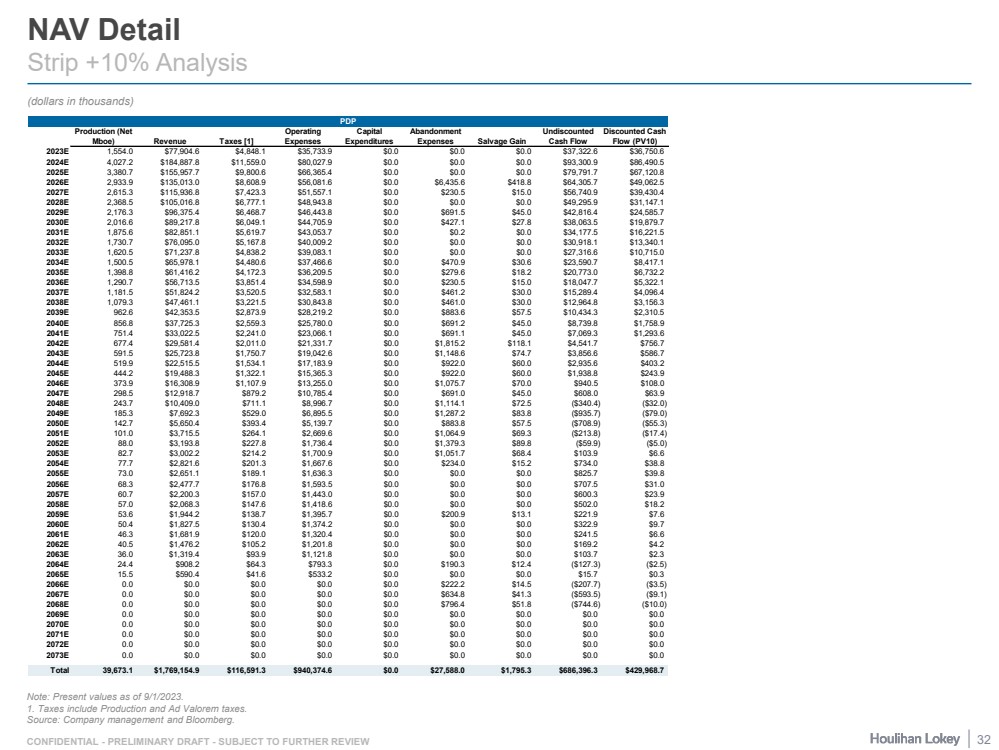

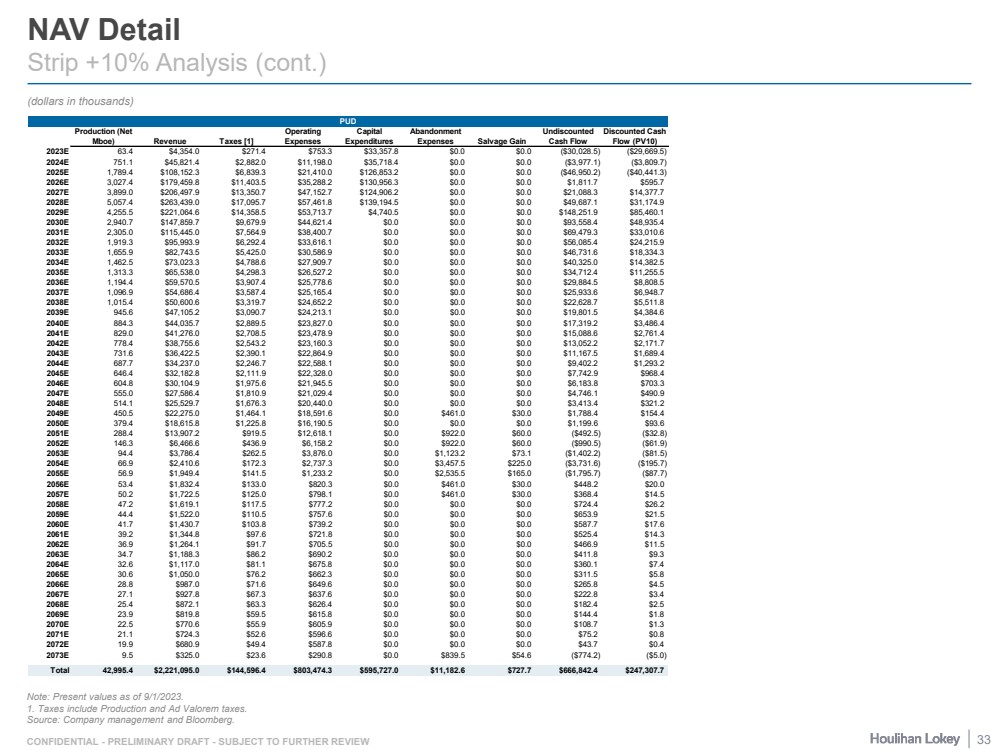

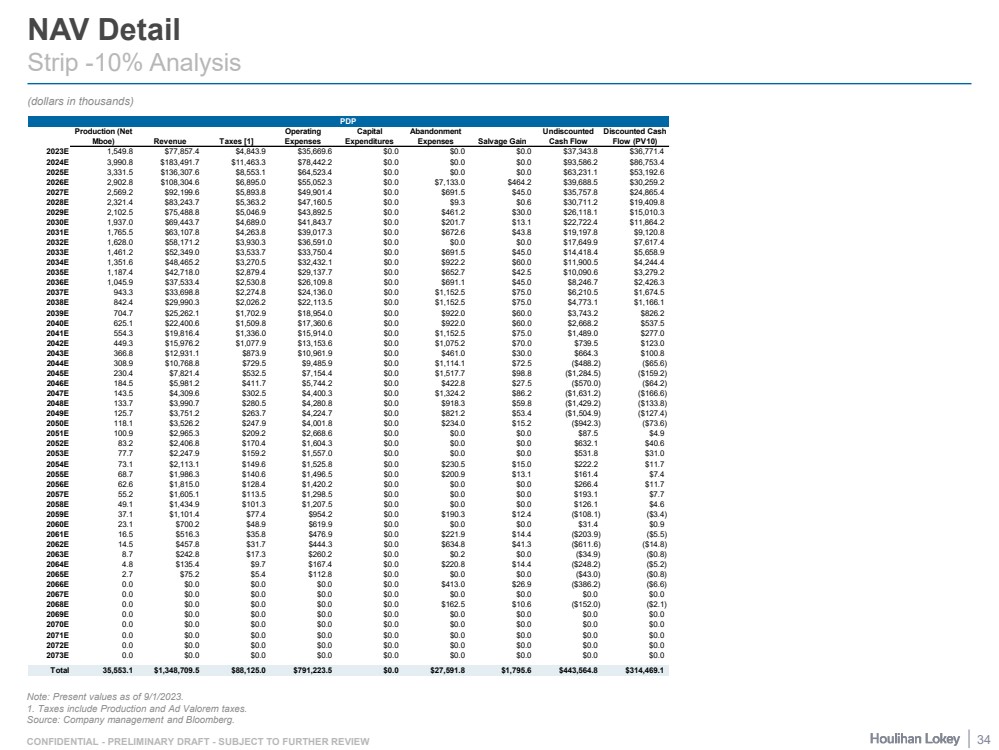

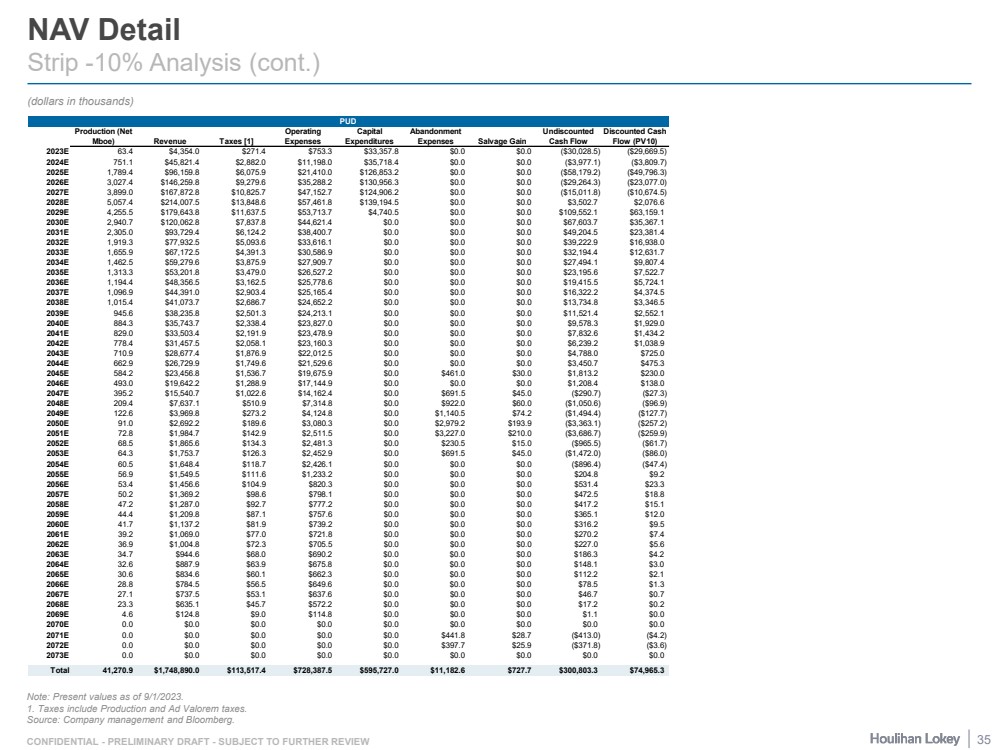

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW NAV Analysis Summary (dollars in millions) Note: Strip pricing as of 11/1/23. Reserves as of 9/1/23. 1. UCF refers to Undiscounted Cash Flow. Source: Company management, Bloomberg. NYMEX Strip Pricing Reserve Category UCF [1] Selected SPEE Based RADRs Implied PV Low High Low High PDP $561.5 PV12.0 -- PV10.0 $348.8 -- $371.6 PUD $482.1 PV25.0 -- PV20.0 $15.9 -- $45.4 Total $1,043.6 $364.7 -- $416.9 A NYMEX Strip +10% Pricing Reserve Category UCF [1] Selected SPEE Based RADRs Implied PV Low High Low High PDP $686.4 PV12.0 -- PV10.0 $400.7 -- $430.0 PUD $666.8 PV25.0 -- PV20.0 $57.4 -- $96.6 Total $1,353.2 $458.1 -- $526.6 B NYMEX Strip -10% Pricing Reserve Category UCF [1] Selected SPEE Based RADRs Implied PV Low High Low High PDP $443.6 PV12.0 -- PV10.0 $297.8 -- $314.5 PUD $300.8 PV25.0 -- PV20.0 $0.0 -- $0.0 Total $744.4 $297.8 -- $314.5 C 19 |

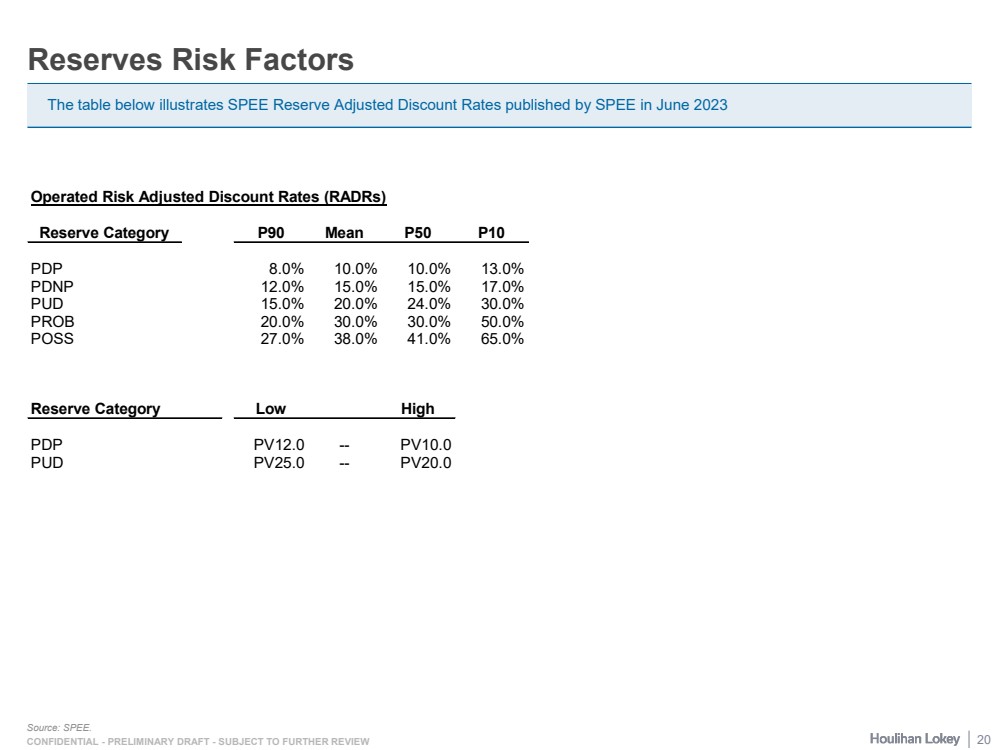

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Reserves Risk Factors Source: SPEE. The table below illustrates SPEE Reserve Adjusted Discount Rates published by SPEE in June 2023 Operated Risk Adjusted Discount Rates (RADRs) Reserve Category P90 Mean P50 P10 PDP 8.0% 10.0% 10.0% 13.0% PDNP 12.0% 15.0% 15.0% 17.0% PUD 15.0% 20.0% 24.0% 30.0% PROB 20.0% 30.0% 30.0% 50.0% POSS 27.0% 38.0% 41.0% 65.0% Reserve Category Low High PDP PV12.0 -- PV10.0 PUD PV25.0 -- PV20.0 20 |

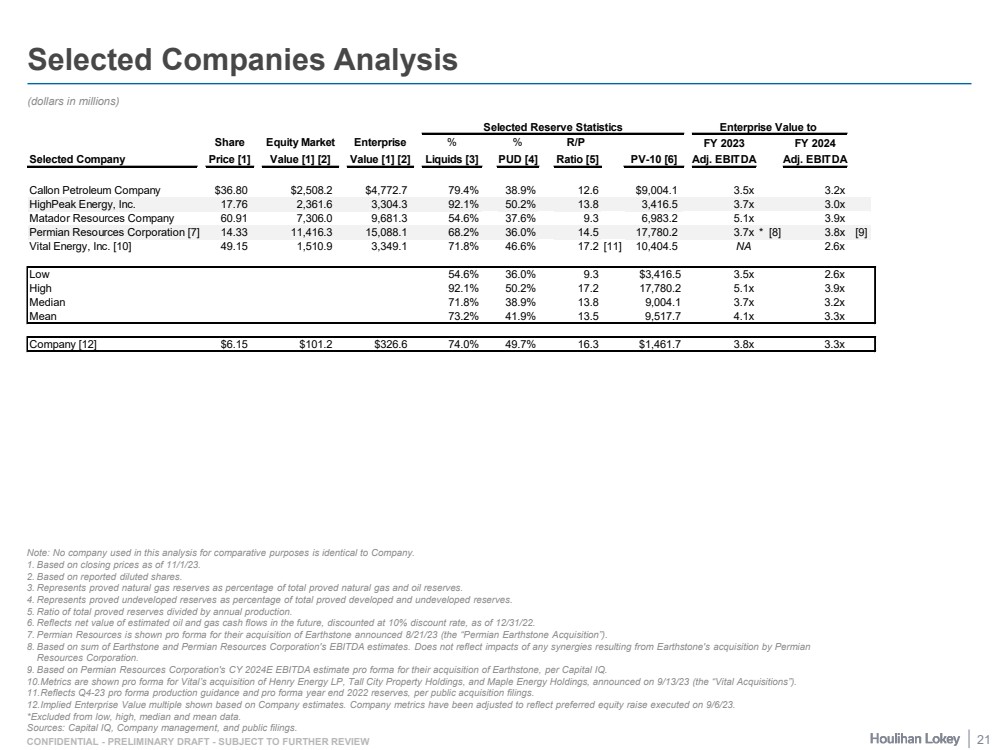

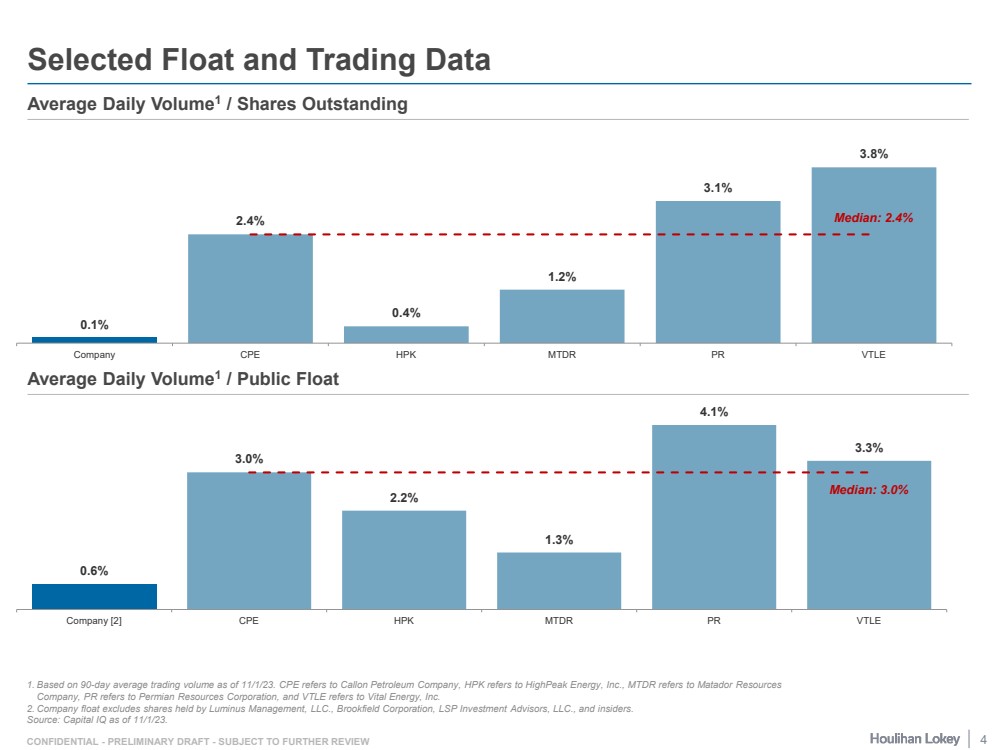

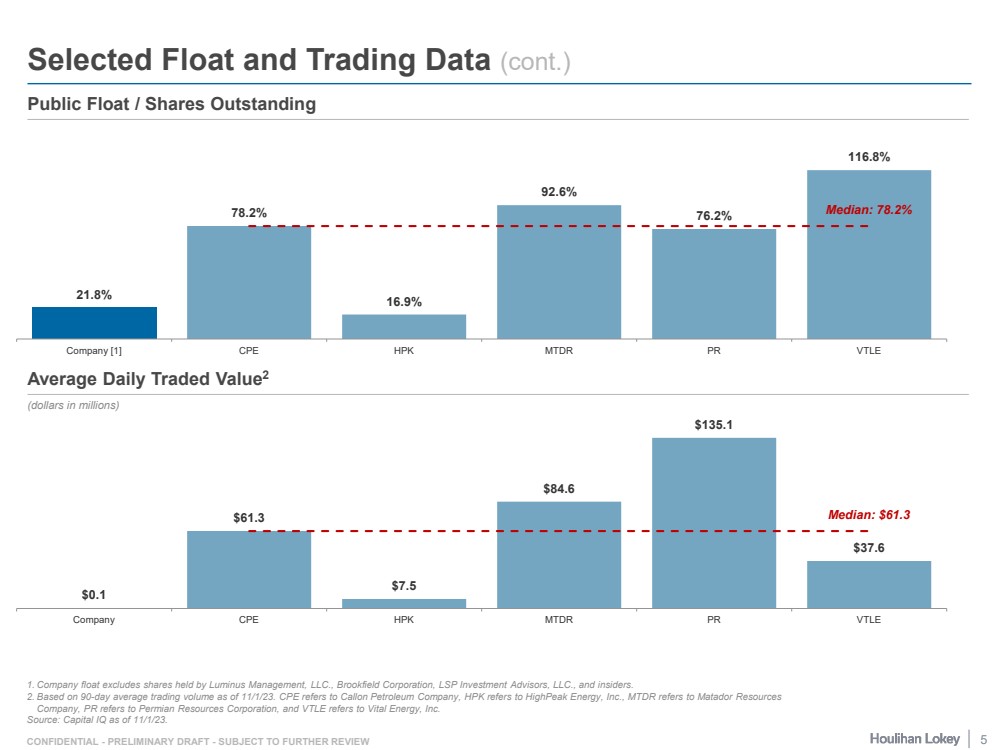

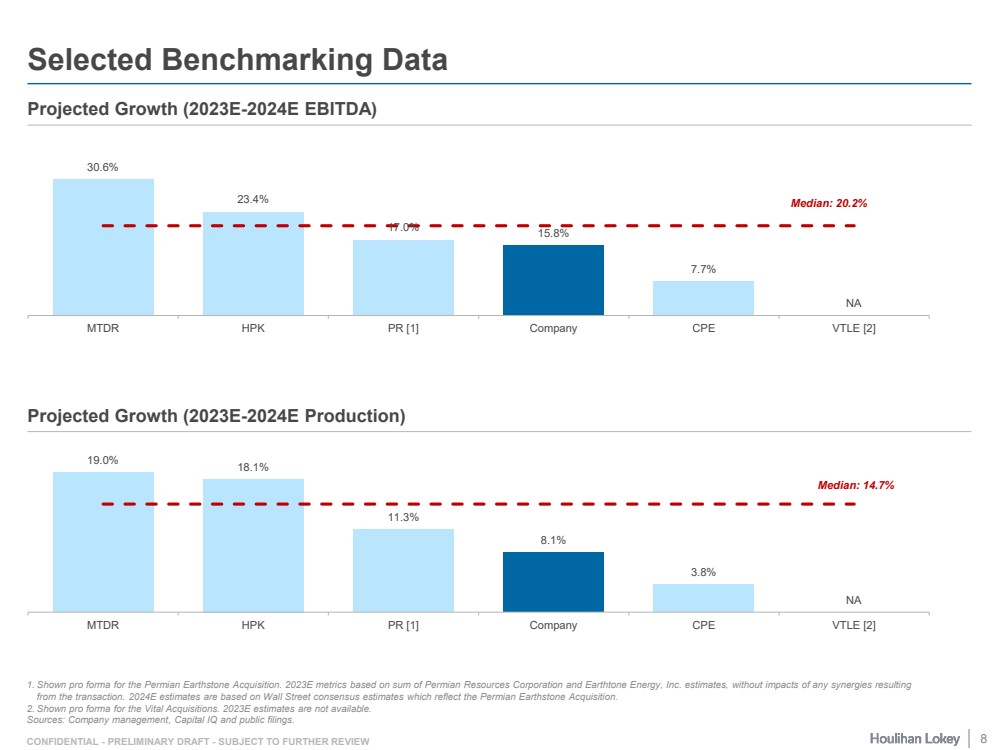

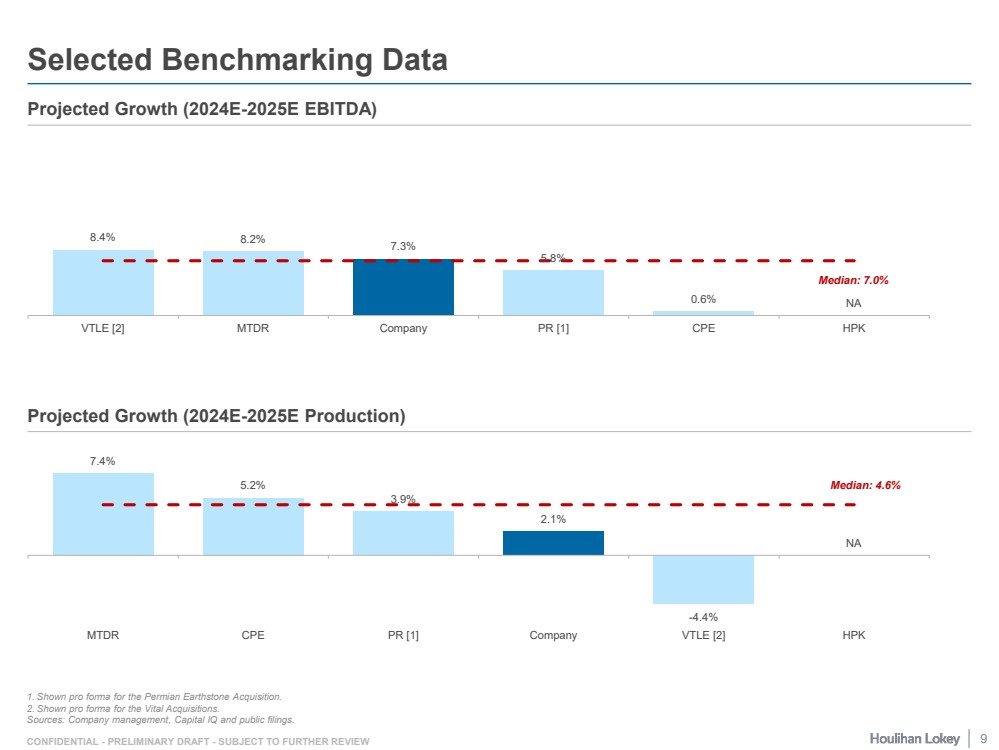

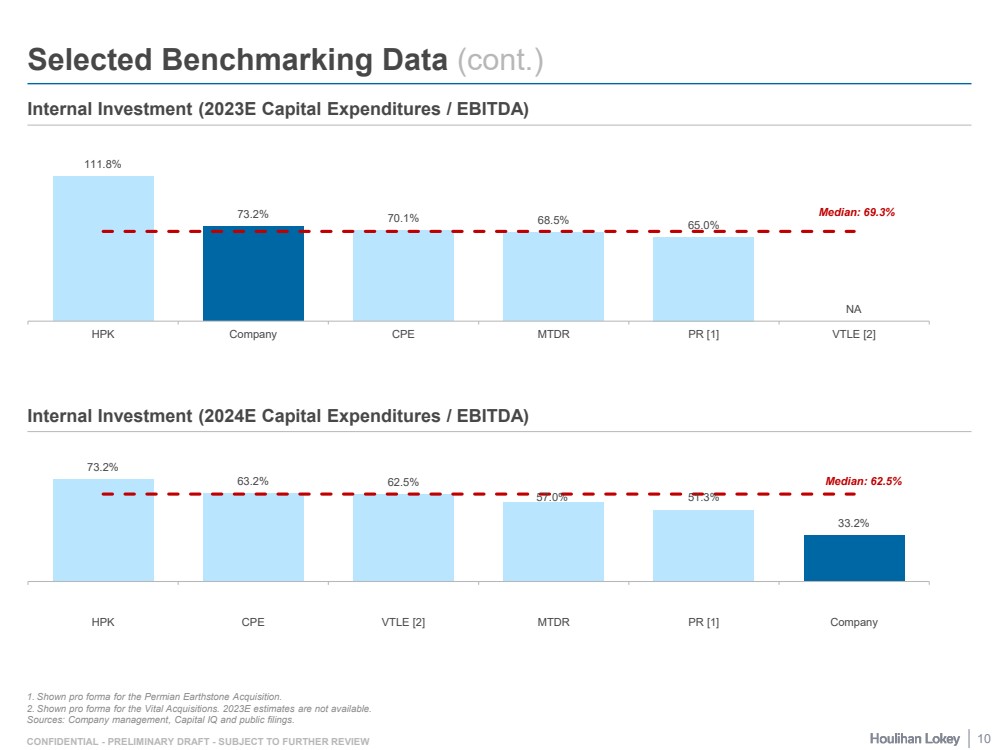

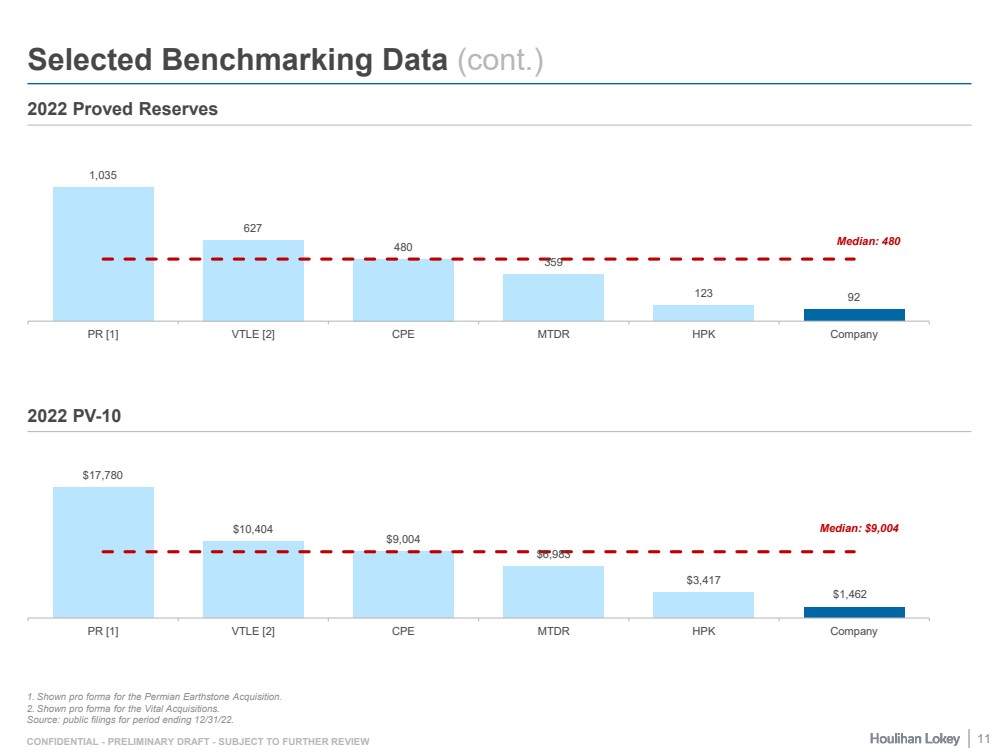

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Selected Companies Analysis (dollars in millions) Note: No company used in this analysis for comparative purposes is identical to Company. 1. Based on closing prices as of 11/1/23. 2. Based on reported diluted shares. 3. Represents proved natural gas reserves as percentage of total proved natural gas and oil reserves. 4. Represents proved undeveloped reserves as percentage of total proved developed and undeveloped reserves. 5. Ratio of total proved reserves divided by annual production. 6. Reflects net value of estimated oil and gas cash flows in the future, discounted at 10% discount rate, as of 12/31/22. 7. Permian Resources is shown pro forma for their acquisition of Earthstone announced 8/21/23 (the “Permian Earthstone Acquisition”). 8. Based on sum of Earthstone and Permian Resources Corporation's EBITDA estimates. Does not reflect impacts of any synergies resulting from Earthstone's acquisition by Permian Resources Corporation. 9. Based on Permian Resources Corporation's CY 2024E EBITDA estimate pro forma for their acquisition of Earthstone, per Capital IQ. 10.Metrics are shown pro forma for Vital’s acquisition of Henry Energy LP, Tall City Property Holdings, and Maple Energy Holdings, announced on 9/13/23 (the “Vital Acquisitions”). 11.Reflects Q4-23 pro forma production guidance and pro forma year end 2022 reserves, per public acquisition filings. 12.Implied Enterprise Value multiple shown based on Company estimates. Company metrics have been adjusted to reflect preferred equity raise executed on 9/6/23. *Excluded from low, high, median and mean data. Sources: Capital IQ, Company management, and public filings. 21 Selected Reserve Statistics Enterprise Value to Share Equity Market Enterprise % % R/P FY 2023 FY 2024 Selected Company Price [1] Value [1] [2] Value [1] [2] Liquids [3] PUD [4] Ratio [5] PV-10 [6] Adj. EBITDA Adj. EBITDA Callon Petroleum Company $36.80 $2,508.2 $4,772.7 79.4% 38.9% 12.6 $9,004.1 3.5x 3.2x HighPeak Energy, Inc. 17.76 2,361.6 3,304.3 92.1% 50.2% 13.8 3,416.5 3.7x 3.0x Matador Resources Company 60.91 7,306.0 9,681.3 54.6% 37.6% 9.3 6,983.2 5.1x 3.9x Permian Resources Corporation [7] 14.33 11,416.3 15,088.1 68.2% 36.0% 14.5 17,780.2 3.7x * [8] 3.8x [9] Vital Energy, Inc. [10] 49.15 1,510.9 3,349.1 71.8% 46.6% 17.2 [11] 10,404.5 NA 2.6x Low 54.6% 36.0% 9.3 $3,416.5 3.5x 2.6x High 92.1% 50.2% 17.2 17,780.2 5.1x 3.9x Median 71.8% 38.9% 13.8 9,004.1 3.7x 3.2x Mean 73.2% 41.9% 13.5 9,517.7 4.1x 3.3x Company [12] $6.15 $101.2 $326.6 74.0% 49.7% 16.3 $1,461.7 3.8x 3.3x |

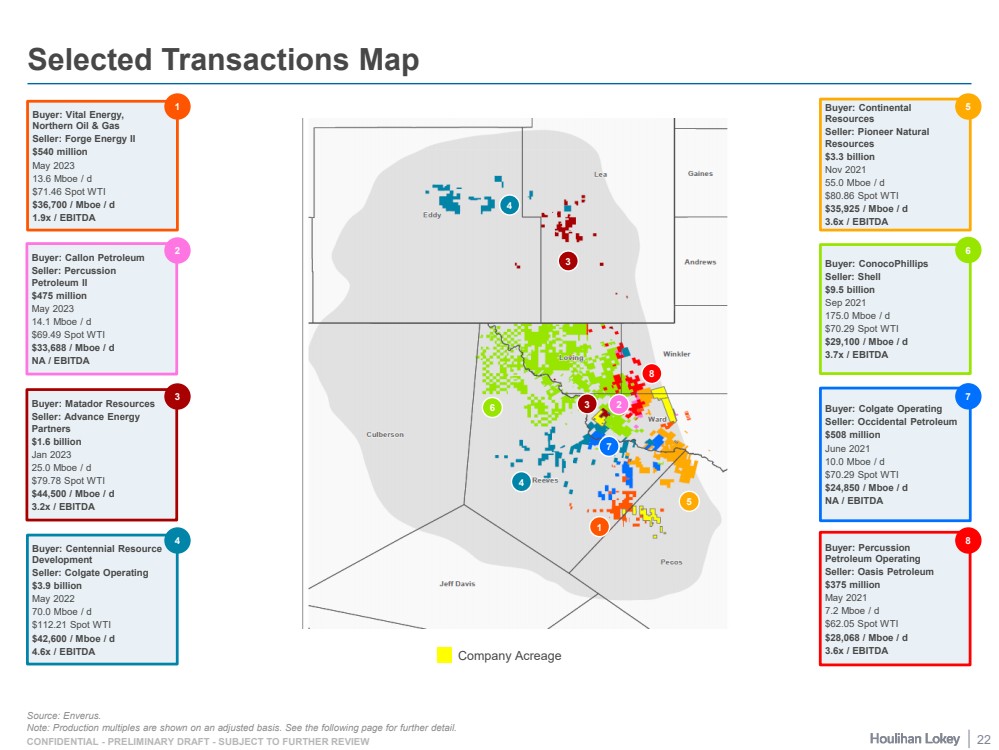

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Selected Transactions Map Buyer: Continental Resources Seller: Pioneer Natural Resources $3.3 billion Nov 2021 55.0 Mboe / d $80.86 Spot WTI $35,925 / Mboe / d 3.6x / EBITDA 5 Buyer: Matador Resources Seller: Advance Energy Partners $1.6 billion Jan 2023 25.0 Mboe / d $79.78 Spot WTI $44,500 / Mboe / d 3.2x / EBITDA 3 Buyer: Vital Energy, Northern Oil & Gas Seller: Forge Energy II $540 million May 2023 13.6 Mboe / d $71.46 Spot WTI $36,700 / Mboe / d 1.9x / EBITDA 1 Buyer: Centennial Resource Development Seller: Colgate Operating $3.9 billion May 2022 70.0 Mboe / d $112.21 Spot WTI $42,600 / Mboe / d 4.6x / EBITDA 4 Company Acreage 3 5 6 Buyer: Callon Petroleum Seller: Percussion Petroleum II $475 million May 2023 14.1 Mboe / d $69.49 Spot WTI $33,688 / Mboe / d NA / EBITDA 2 Buyer: ConocoPhillips Seller: Shell $9.5 billion Sep 2021 175.0 Mboe / d $70.29 Spot WTI $29,100 / Mboe / d 3.7x / EBITDA 6 Buyer: Percussion Petroleum Operating Seller: Oasis Petroleum $375 million May 2021 7.2 Mboe / d $62.05 Spot WTI $28,068 / Mboe / d 3.6x / EBITDA 8 8 Buyer: Colgate Operating Seller: Occidental Petroleum $508 million June 2021 10.0 Mboe / d $70.29 Spot WTI $24,850 / Mboe / d NA / EBITDA 7 1 Source: Enverus .. Note: Production multiples are shown on an adjusted basis. See the following page for further detail. 2 7 4 3 4 22 |

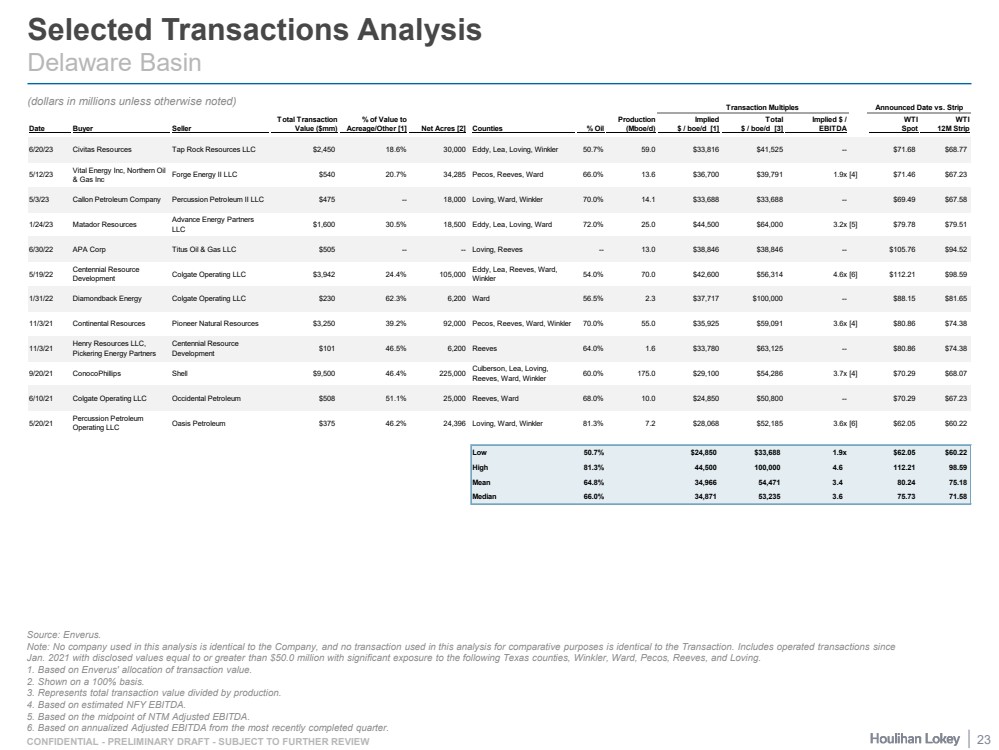

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Selected Transactions Analysis Delaware Basin Source: Enverus. Note: No company used in this analysis is identical to the Company, and no transaction used in this analysis for comparative purposes is identical to the Transaction. Includes operated transactions since Jan. 2021 with disclosed values equal to or greater than $50.0 million with significant exposure to the following Texas counties, Winkler, Ward, Pecos, Reeves, and Loving. 1. Based on Enverus' allocation of transaction value. 2. Shown on a 100% basis. 3. Represents total transaction value divided by production. 4. Based on estimated NFY EBITDA. 5. Based on the midpoint of NTM Adjusted EBITDA. 6. Based on annualized Adjusted EBITDA from the most recently completed quarter. (dollars in millions unless otherwise noted) Transaction Multiples Announced Date vs. Strip Total Transaction % of Value to Production Implied Total Implied $ / WTI WTI Date Buyer Seller Value ($mm) Acreage/Other [1] Net Acres [2] Counties % Oil (Mboe/d) $ / boe/d [1] $ / boe/d [3] EBITDA Spot 12M Strip 6/20/23 Civitas Resources Tap Rock Resources LLC $2,450 18.6% 30,000 Eddy, Lea, Loving, Winkler 50.7% 59.0 $33,816 $41,525 -- $71.68 $68.77 5/12/23 Vital Energy Inc, Northern Oil & Gas Inc Forge Energy II LLC $540 20.7% 34,285 Pecos, Reeves, Ward 66.0% 13.6 $36,700 $39,791 1.9x [4] $71.46 $67.23 5/3/23 Callon Petroleum Company Percussion Petroleum II LLC $475 -- 18,000 Loving, Ward, Winkler 70.0% 14.1 $33,688 $33,688 -- $69.49 $67.58 1/24/23 Matador Resources Advance Energy Partners LLC $1,600 30.5% 18,500 Eddy, Lea, Loving, Ward 72.0% 25.0 $44,500 $64,000 3.2x [5] $79.78 $79.51 6/30/22 APA Corp Titus Oil & Gas LLC $505 -- -- Loving, Reeves -- 13.0 $38,846 $38,846 -- $105.76 $94.52 5/19/22 Centennial Resource Development Colgate Operating LLC $3,942 24.4% 105,000 Eddy, Lea, Reeves, Ward, Winkler 54.0% 70.0 $42,600 $56,314 4.6x [6] $112.21 $98.59 1/31/22 Diamondback Energy Colgate Operating LLC $230 62.3% 6,200 Ward 56.5% 2.3 $37,717 $100,000 -- $88.15 $81.65 11/3/21 Continental Resources Pioneer Natural Resources $3,250 39.2% 92,000 Pecos, Reeves, Ward, Winkler 70.0% 55.0 $35,925 $59,091 3.6x [4] $80.86 $74.38 11/3/21 Henry Resources LLC, Pickering Energy Partners Centennial Resource Development $101 46.5% 6,200 Reeves 64.0% 1.6 $33,780 $63,125 -- $80.86 $74.38 9/20/21 ConocoPhillips Shell $9,500 46.4% 225,000 Culberson, Lea, Loving, Reeves, Ward, Winkler 60.0% 175.0 $29,100 $54,286 3.7x [4] $70.29 $68.07 6/10/21 Colgate Operating LLC Occidental Petroleum $508 51.1% 25,000 Reeves, Ward 68.0% 10.0 $24,850 $50,800 -- $70.29 $67.23 5/20/21 Percussion Petroleum Operating LLC Oasis Petroleum $375 46.2% 24,396 Loving, Ward, Winkler 81.3% 7.2 $28,068 $52,185 3.6x [6] $62.05 $60.22 Low 50.7% $24,850 $33,688 1.9x $62.05 $60.22 High 81.3% 44,500 100,000 4.6 112.21 98.59 Mean 64.8% 34,966 54,471 3.4 80.24 75.18 Median 66.0% 34,871 53,235 3.6 75.73 71.58 23 |

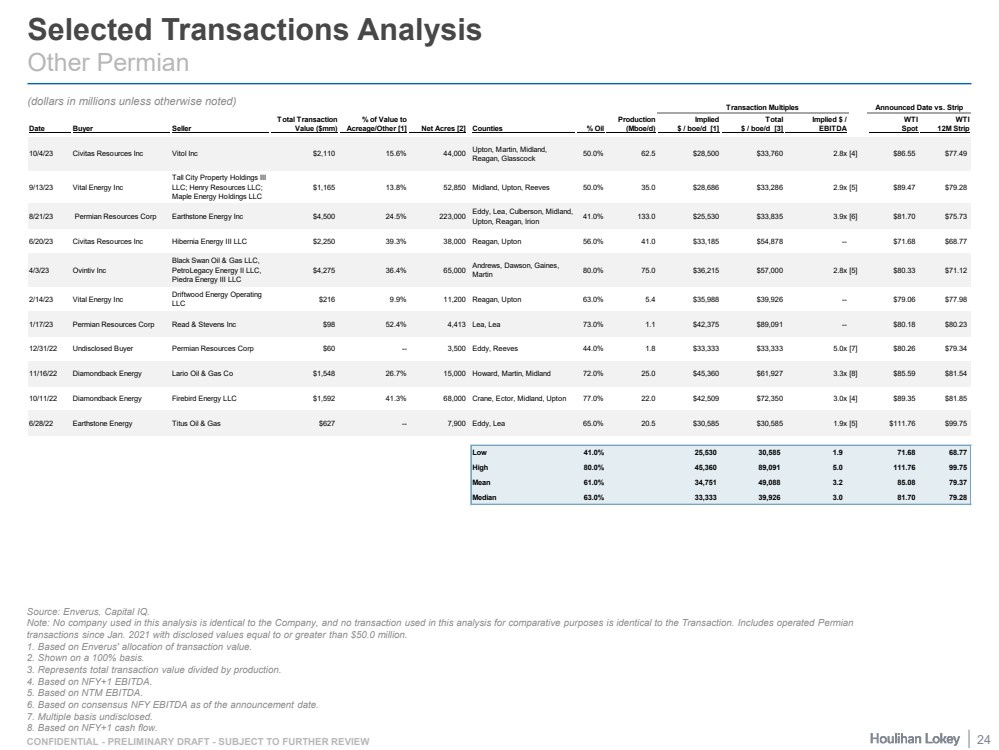

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Selected Transactions Analysis Other Permian Source: Enverus, Capital IQ. Note: No company used in this analysis is identical to the Company, and no transaction used in this analysis for comparative purposes is identical to the Transaction. Includes operated Permian transactions since Jan. 2021 with disclosed values equal to or greater than $50.0 million. 1. Based on Enverus' allocation of transaction value. 2. Shown on a 100% basis. 3. Represents total transaction value divided by production. 4. Based on NFY+1 EBITDA. 5. Based on NTM EBITDA. 6. Based on consensus NFY EBITDA as of the announcement date. 7. Multiple basis undisclosed. 8. Based on NFY+1 cash flow. (dollars in millions unless otherwise noted) Transaction Multiples Announced Date vs. Strip Total Transaction % of Value to Production Implied Total Implied $ / WTI WTI Date Buyer Seller Value ($mm) Acreage/Other [1] Net Acres [2] Counties % Oil (Mboe/d) $ / boe/d [1] $ / boe/d [3] EBITDA Spot 12M Strip 10/4/23 Civitas Resources Inc Vitol Inc $2,110 15.6% 44,000 Upton, Martin, Midland, Reagan, Glasscock 50.0% 62.5 $28,500 $33,760 2.8x [4] $86.55 $77.49 9/13/23 Vital Energy Inc Tall City Property Holdings III LLC; Henry Resources LLC; Maple Energy Holdings LLC $1,165 13.8% 52,850 Midland, Upton, Reeves 50.0% 35.0 $28,686 $33,286 2.9x [5] $89.47 $79.28 8/21/23 Permian Resources Corp Earthstone Energy Inc $4,500 24.5% 223,000 Eddy, Lea, Culberson, Midland, Upton, Reagan, Irion 41.0% 133.0 $25,530 $33,835 3.9x [6] $81.70 $75.73 6/20/23 Civitas Resources Inc Hibernia Energy III LLC $2,250 39.3% 38,000 Reagan, Upton 56.0% 41.0 $33,185 $54,878 -- $71.68 $68.77 4/3/23 Ovintiv Inc Black Swan Oil & Gas LLC, PetroLegacy Energy II LLC, Piedra Energy III LLC $4,275 36.4% 65,000 Andrews, Dawson, Gaines, Martin 80.0% 75.0 $36,215 $57,000 2.8x [5] $80.33 $71.12 2/14/23 Vital Energy Inc Driftwood Energy Operating LLC $216 9.9% 11,200 Reagan, Upton 63.0% 5.4 $35,988 $39,926 -- $79.06 $77.98 1/17/23 Permian Resources Corp Read & Stevens Inc $98 52.4% 4,413 Lea, Lea 73.0% 1.1 $42,375 $89,091 -- $80.18 $80.23 12/31/22 Undisclosed Buyer Permian Resources Corp $60 -- 3,500 Eddy, Reeves 44.0% 1.8 $33,333 $33,333 5.0x [7] $80.26 $79.34 11/16/22 Diamondback Energy Lario Oil & Gas Co $1,548 26.7% 15,000 Howard, Martin, Midland 72.0% 25.0 $45,360 $61,927 3.3x [8] $85.59 $81.54 10/11/22 Diamondback Energy Firebird Energy LLC $1,592 41.3% 68,000 Crane, Ector, Midland, Upton 77.0% 22.0 $42,509 $72,350 3.0x [4] $89.35 $81.85 6/28/22 Earthstone Energy Titus Oil & Gas $627 -- 7,900 Eddy, Lea 65.0% 20.5 $30,585 $30,585 1.9x [5] $111.76 $99.75 Low 41.0% 25,530 30,585 1.9 71.68 68.77 High 80.0% 45,360 89,091 5.0 111.76 99.75 Mean 61.0% 34,751 49,088 3.2 85.08 79.37 Median 63.0% 33,333 39,926 3.0 81.70 79.28 24 |

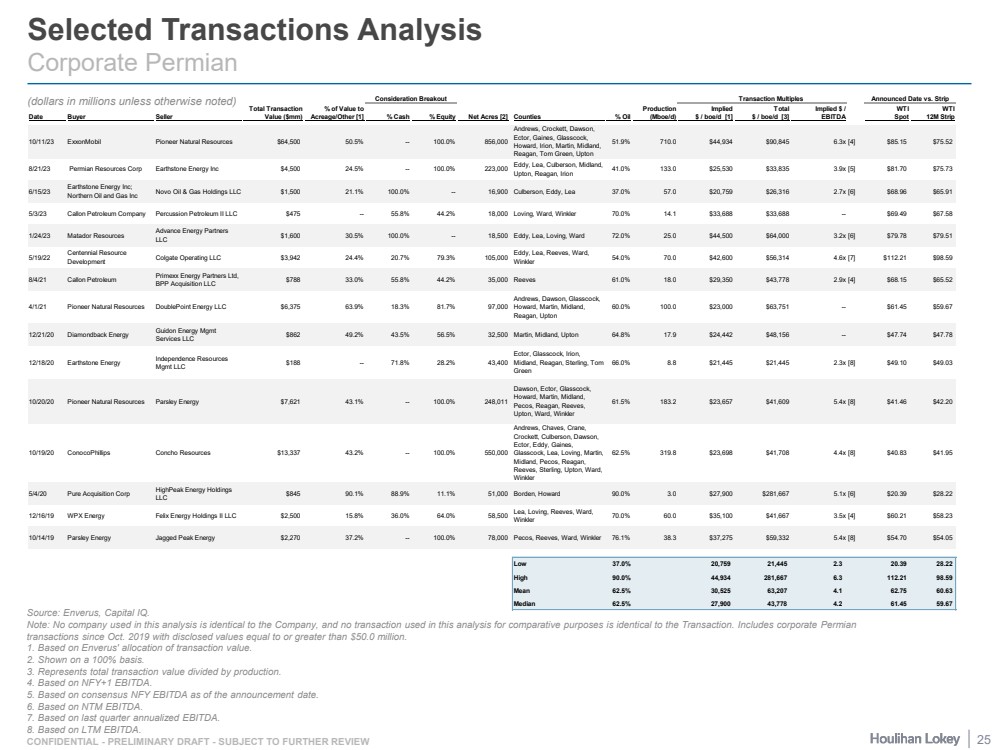

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Selected Transactions Analysis Corporate Permian Source: Enverus, Capital IQ. Note: No company used in this analysis is identical to the Company, and no transaction used in this analysis for comparative purposes is identical to the Transaction. Includes corporate Permian transactions since Oct. 2019 with disclosed values equal to or greater than $50.0 million. 1. Based on Enverus' allocation of transaction value. 2. Shown on a 100% basis. 3. Represents total transaction value divided by production. 4. Based on NFY+1 EBITDA. 5. Based on consensus NFY EBITDA as of the announcement date. 6. Based on NTM EBITDA. 7. Based on last quarter annualized EBITDA. 8. Based on LTM EBITDA. (dollars in millions unless otherwise noted) Consideration Breakout Transaction Multiples Announced Date vs. Strip Total Transaction % of Value to Production Implied Total Implied $ / WTI WTI Date Buyer Seller Value ($mm) Acreage/Other [1] % Cash % Equity Net Acres [2] Counties % Oil (Mboe/d) $ / boe/d [1] $ / boe/d [3] EBITDA Spot 12M Strip 10/11/23 ExxonMobil Pioneer Natural Resources $64,500 50.5% -- 100.0% 856,000 Andrews, Crockett, Dawson, Ector, Gaines, Glasscock, Howard, Irion, Martin, Midland, Reagan, Tom Green, Upton 51.9% 710.0 $44,934 $90,845 6.3x [4] $85.15 $75.52 8/21/23 Permian Resources Corp Earthstone Energy Inc $4,500 24.5% -- 100.0% 223,000 Eddy, Lea, Culberson, Midland, Upton, Reagan, Irion 41.0% 133.0 $25,530 $33,835 3.9x [5] $81.70 $75.73 6/15/23 Earthstone Energy Inc; Northern Oil and Gas Inc Novo Oil & Gas Holdings LLC $1,500 21.1% 100.0% -- 16,900 Culberson, Eddy, Lea 37.0% 57.0 $20,759 $26,316 2.7x [6] $68.96 $65.91 5/3/23 Callon Petroleum Company Percussion Petroleum II LLC $475 -- 55.8% 44.2% 18,000 Loving, Ward, Winkler 70.0% 14.1 $33,688 $33,688 -- $69.49 $67.58 1/24/23 Matador Resources Advance Energy Partners LLC $1,600 30.5% 100.0% -- 18,500 Eddy, Lea, Loving, Ward 72.0% 25.0 $44,500 $64,000 3.2x [6] $79.78 $79.51 5/19/22 Centennial Resource Development Colgate Operating LLC $3,942 24.4% 20.7% 79.3% 105,000 Eddy, Lea, Reeves, Ward, Winkler 54.0% 70.0 $42,600 $56,314 4.6x [7] $112.21 $98.59 8/4/21 Callon Petroleum Primexx Energy Partners Ltd, BPP Acquisition LLC $788 33.0% 55.8% 44.2% 35,000 Reeves 61.0% 18.0 $29,350 $43,778 2.9x [4] $68.15 $65.52 4/1/21 Pioneer Natural Resources DoublePoint Energy LLC $6,375 63.9% 18.3% 81.7% 97,000 Andrews, Dawson, Glasscock, Howard, Martin, Midland, Reagan, Upton 60.0% 100.0 $23,000 $63,751 -- $61.45 $59.67 12/21/20 Diamondback Energy Guidon Energy Mgmt Services LLC $862 49.2% 43.5% 56.5% 32,500 Martin, Midland, Upton 64.8% 17.9 $24,442 $48,156 -- $47.74 $47.78 12/18/20 Earthstone Energy Independence Resources Mgmt LLC $188 -- 71.8% 28.2% 43,400 Ector, Glasscock, Irion, Midland, Reagan, Sterling, Tom Green 66.0% 8.8 $21,445 $21,445 2.3x [8] $49.10 $49.03 10/20/20 Pioneer Natural Resources Parsley Energy $7,621 43.1% -- 100.0% 248,011 Dawson, Ector, Glasscock, Howard, Martin, Midland, Pecos, Reagan, Reeves, Upton, Ward, Winkler 61.5% 183.2 $23,657 $41,609 5.4x [8] $41.46 $42.20 10/19/20 ConocoPhillips Concho Resources $13,337 43.2% -- 100.0% 550,000 Andrews, Chaves, Crane, Crockett, Culberson, Dawson, Ector, Eddy, Gaines, Glasscock, Lea, Loving, Martin, Midland, Pecos, Reagan, Reeves, Sterling, Upton, Ward, Winkler 62.5% 319.8 $23,698 $41,708 4.4x [8] $40.83 $41.95 5/4/20 Pure Acquisition Corp HighPeak Energy Holdings LLC $845 90.1% 88.9% 11.1% 51,000 Borden, Howard 90.0% 3.0 $27,900 $281,667 5.1x [6] $20.39 $28.22 12/16/19 WPX Energy Felix Energy Holdings II LLC $2,500 15.8% 36.0% 64.0% 58,500 Lea, Loving, Reeves, Ward, Winkler 70.0% 60.0 $35,100 $41,667 3.5x [4] $60.21 $58.23 10/14/19 Parsley Energy Jagged Peak Energy $2,270 37.2% -- 100.0% 78,000 Pecos, Reeves, Ward, Winkler 76.1% 38.3 $37,275 $59,332 5.4x [8] $54.70 $54.05 Low 37.0% 20,759 21,445 2.3 20.39 28.22 High 90.0% 44,934 281,667 6.3 112.21 98.59 Mean 62.5% 30,525 63,207 4.1 62.75 60.63 Median 62.5% 27,900 43,778 4.2 61.45 59.67 25 |

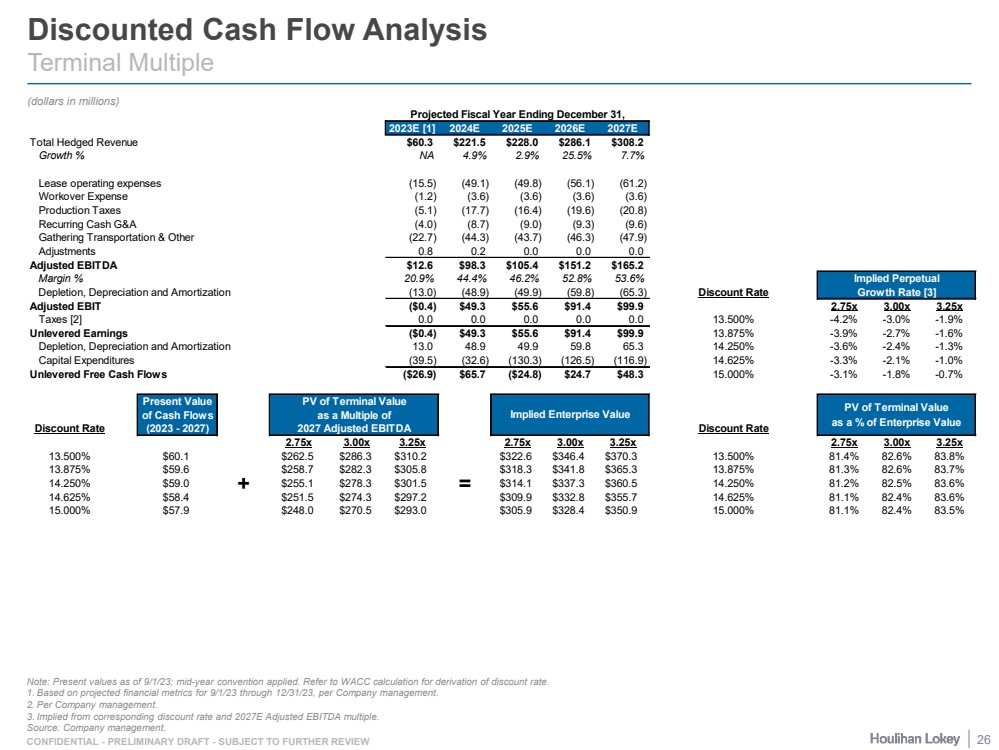

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Discounted Cash Flow Analysis Terminal Multiple (dollars in millions) Note: Present values as of 9/1/23; mid-year convention applied. Refer to WACC calculation for derivation of discount rate. 1. Based on projected financial metrics for 9/1/23 through 12/31/23, per Company management. 2. Per Company management. 3. Implied from corresponding discount rate and 2027E Adjusted EBITDA multiple. Source: Company management. Projected Fiscal Year Ending December 31, 2023E [1] 2024E 2025E 2026E 2027E Total Hedged Revenue $60.3 $221.5 $228.0 $286.1 $308.2 Growth % NA 4.9% 2.9% 25.5% 7.7% Lease operating expenses (15.5) (49.1) (49.8) (56.1) (61.2) Workover Expense (1.2) (3.6) (3.6) (3.6) (3.6) Production Taxes (5.1) (17.7) (16.4) (19.6) (20.8) Recurring Cash G&A (4.0) (8.7) (9.0) (9.3) (9.6) Gathering Transportation & Other (22.7) (44.3) (43.7) (46.3) (47.9) Adjustments 0.8 0.2 0.0 0.0 0.0 Adjusted EBITDA $12.6 $98.3 $105.4 $151.2 $165.2 Margin % 20.9% 44.4% 46.2% 52.8% 53.6% Implied Perpetual Depletion, Depreciation and Amortization (13.0) (48.9) (49.9) (59.8) (65.3) Discount Rate Growth Rate [3] Adjusted EBIT ($0.4) $49.3 $55.6 $91.4 $99.9 2.75x 3.00x 3.25x Taxes [2] 0.0 0.0 0.0 0.0 0.0 13.500% -4.2% -3.0% -1.9% Unlevered Earnings ($0.4) $49.3 $55.6 $91.4 $99.9 13.875% -3.9% -2.7% -1.6% Depletion, Depreciation and Amortization 13.0 48.9 49.9 59.8 65.3 14.250% -3.6% -2.4% -1.3% Capital Expenditures (39.5) (32.6) (130.3) (126.5) (116.9) 14.625% -3.3% -2.1% -1.0% Unlevered Free Cash Flows ($26.9) $65.7 ($24.8) $24.7 $48.3 15.000% -3.1% -1.8% -0.7% Present Value PV of Terminal Value of Cash Flows as a Multiple of Discount Rate (2023 - 2027) 2027 Adjusted EBITDA Discount Rate 2.75x 3.00x 3.25x 2.75x 3.00x 3.25x 2.75x 3.00x 3.25x 13.500% $60.1 $262.5 $286.3 $310.2 $322.6 $346.4 $370.3 13.500% 81.4% 82.6% 83.8% 13.875% $59.6 $258.7 $282.3 $305.8 $318.3 $341.8 $365.3 13.875% 81.3% 82.6% 83.7% 14.250% $59.0 + $255.1 $278.3 $301.5 = $314.1 $337.3 $360.5 14.250% 81.2% 82.5% 83.6% 14.625% $58.4 $251.5 $274.3 $297.2 $309.9 $332.8 $355.7 14.625% 81.1% 82.4% 83.6% 15.000% $57.9 $248.0 $270.5 $293.0 $305.9 $328.4 $350.9 15.000% 81.1% 82.4% 83.5% PV of Terminal Value as a % of Enterprise Value Implied Enterprise Value 26 |

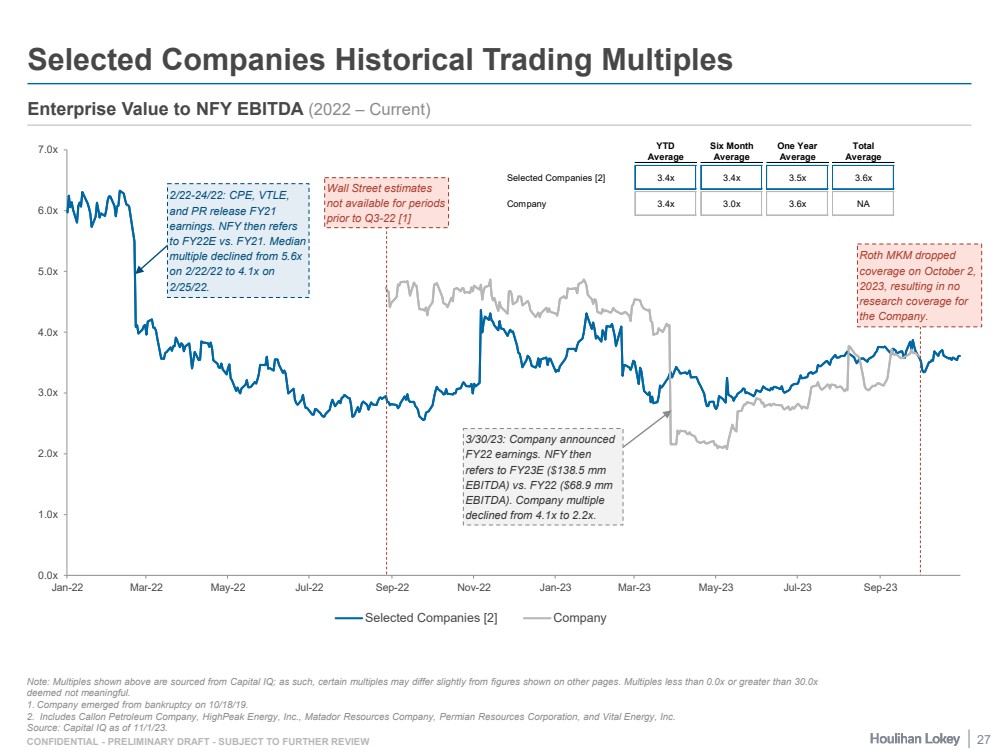

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW 0.0x 1.0x 2.0x 3.0x 4.0x 5.0x 6.0x 7.0x Jan-22 Mar-22 May-22 Jul-22 Sep-22 Nov-22 Jan-23 Mar-23 May-23 Jul-23 Sep-23 Selected Companies [2] Company Selected Companies Historical Trading Multiples Note: Multiples shown above are sourced from Capital IQ; as such, certain multiples may differ slightly from figures shown on other pages. Multiples less than 0.0x or greater than 30.0x deemed not meaningful. 1. Company emerged from bankruptcy on 10/18/19. 2. Includes Callon Petroleum Company, HighPeak Energy, Inc., Matador Resources Company, Permian Resources Corporation, and Vital Energy, Inc. Source: Capital IQ as of 11/1/23. Enterprise Value to NFY EBITDA (2022 – Current) 2/22-24/22: CPE, VTLE, and PR release FY21 earnings. NFY then refers to FY22E vs. FY21. Median multiple declined from 5.6x on 2/22/22 to 4.1x on 2/25/22. Wall Street estimates not available for periods prior to Q3-22 [1] 3/30/23: Company announced FY22 earnings. NFY then refers to FY23E ($138.5 mm EBITDA) vs. FY22 ($68.9 mm EBITDA). Company multiple declined from 4.1x to 2.2x. Roth MKM dropped coverage on October 2, 2023, resulting in no research coverage for the Company. YTD Six Month One Year Total Average Average Average Average Selected Companies [2] 3.4x 3.4x 3.5x 3.6x Company 3.4x 3.0x 3.6x NA 27 |

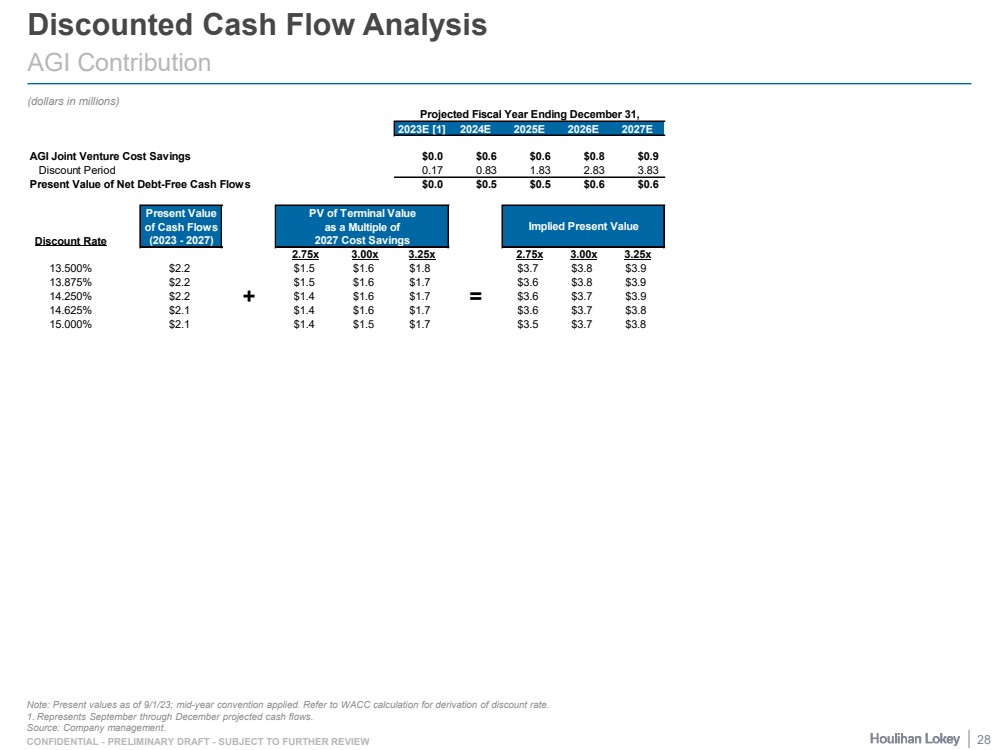

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Discounted Cash Flow Analysis AGI Contribution (dollars in millions) Note: Present values as of 9/1/23; mid-year convention applied. Refer to WACC calculation for derivation of discount rate. 1. Represents September through December projected cash flows. Source: Company management. Projected Fiscal Year Ending December 31, 2023E [1] 2024E 2025E 2026E 2027E AGI Joint Venture Cost Savings $0.0 $0.6 $0.6 $0.8 $0.9 Discount Period 0.17 0.83 1.83 2.83 3.83 Present Value of Net Debt-Free Cash Flows $0.0 $0.5 $0.5 $0.6 $0.6 Present Value PV of Terminal Value of Cash Flows as a Multiple of Discount Rate (2023 - 2027) 2027 Cost Savings 2.75x 3.00x 3.25x 2.75x 3.00x 3.25x 13.500% $2.2 $1.5 $1.6 $1.8 $3.7 $3.8 $3.9 13.875% $2.2 $1.5 $1.6 $1.7 $3.6 $3.8 $3.9 14.250% $2.2 + $1.4 $1.6 $1.7 = $3.6 $3.7 $3.9 14.625% $2.1 $1.4 $1.6 $1.7 $3.6 $3.7 $3.8 15.000% $2.1 $1.4 $1.5 $1.7 $3.5 $3.7 $3.8 Implied Present Value 28 |

| Page 1. Executive Summary 3 2. Financial Analyses 8 3. Selected Public Market Observations 29 4. Appendix 34 5. Disclaimer 47 |

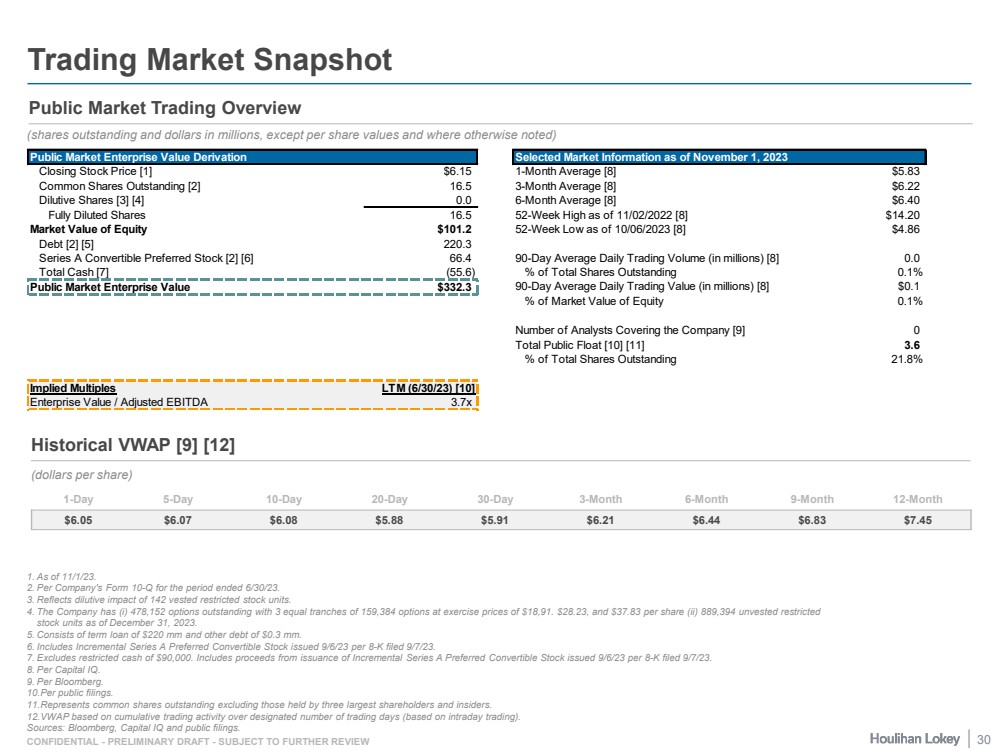

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Trading Market Snapshot Public Market Trading Overview (shares outstanding and dollars in millions, except per share values and where otherwise noted) 1. As of 11/1/23. 2. Per Company's Form 10-Q for the period ended 6/30/23. 3. Reflects dilutive impact of 142 vested restricted stock units. 4. The Company has (i) 478,152 options outstanding with 3 equal tranches of 159,384 options at exercise prices of $18,91. $28.23, and $37.83 per share (ii) 889,394 unvested restricted stock units as of December 31, 2023. 5. Consists of term loan of $220 mm and other debt of $0.3 mm. 6. Includes Incremental Series A Preferred Convertible Stock issued 9/6/23 per 8-K filed 9/7/23. 7. Excludes restricted cash of $90,000. Includes proceeds from issuance of Incremental Series A Preferred Convertible Stock issued 9/6/23 per 8-K filed 9/7/23. 8. Per Capital IQ. 9. Per Bloomberg. 10.Per public filings. 11.Represents common shares outstanding excluding those held by three largest shareholders and insiders. 12.VWAP based on cumulative trading activity over designated number of trading days (based on intraday trading). Sources: Bloomberg, Capital IQ and public filings. Historical VWAP [9] [12] (dollars per share) 1-Day 5-Day 10-Day 20-Day 30-Day 3-Month 6-Month 9-Month 12-Month $6.05 $6.07 $6.08 $5.88 $5.91 $6.21 $6.44 $6.83 $7.45 Public Market Enterprise Value Derivation Selected Market Information as of November 1, 2023 Closing Stock Price [1] $6.15 1-Month Average [8] $5.83 Common Shares Outstanding [2] 16.5 3-Month Average [8] $6.22 Dilutive Shares [3] [4] 0.0 6-Month Average [8] $6.40 Fully Diluted Shares 16.5 52-Week High as of 11/02/2022 [8] $14.20 Market Value of Equity $101.2 52-Week Low as of 10/06/2023 [8] $4.86 Debt [2] [5] 220.3 Series A Convertible Preferred Stock [2] [6] 66.4 90-Day Average Daily Trading Volume (in millions) [8] 0.0 Total Cash [7] (55.6) % of Total Shares Outstanding 0.1% Public Market Enterprise Value $332.3 90-Day Average Daily Trading Value (in millions) [8] $0.1 % of Market Value of Equity 0.1% Number of Analysts Covering the Company [9] 0 Total Public Float [10] [11] 3.6 % of Total Shares Outstanding 21.8% Implied Multiples LTM (6/30/23) [10] CY 2023E [12] CY 2024E [12] Enterprise Value / Adjusted EBITDA 3.7x 4.2x 3.9x 30 |

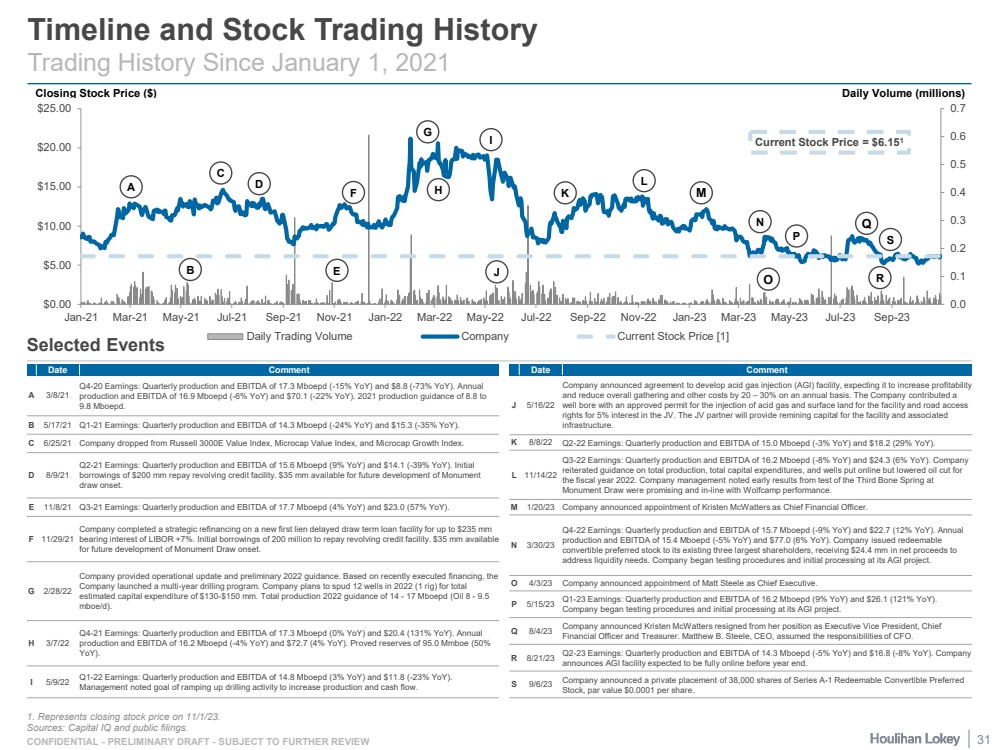

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW 0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 $0.00 $5.00 $10.00 $15.00 $20.00 $25.00 Jan-21 Mar-21 May-21 Jul-21 Sep-21 Nov-21 Jan-22 Mar-22 May-22 Jul-22 Sep-22 Nov-22 Jan-23 Mar-23 May-23 Jul-23 Sep-23 Daily Trading Volume Company Current Stock Price [1] Closing Stock Price ($) Daily Volume (millions) Timeline and Stock Trading History Trading History Since January 1, 2021 Selected Events Date Comment A 3/8/21 Q4-20 Earnings: Quarterly production and EBITDA of 17.3 Mboepd (-15% YoY) and $8.8 (-73% YoY). Annual production and EBITDA of 16.9 Mboepd (-6% YoY) and $70.1 (-22% YoY). 2021 production guidance of 8.8 to 9.8 Mboepd. B 5/17/21 Q1-21 Earnings: Quarterly production and EBITDA of 14.3 Mboepd (-24% YoY) and $15.3 (-35% YoY). C 6/25/21 Company dropped from Russell 3000E Value Index, Microcap Value Index, and Microcap Growth Index. D 8/9/21 Q2-21 Earnings: Quarterly production and EBITDA of 15.6 Mboepd (9% YoY) and $14.1 (-39% YoY). Initial borrowings of $200 mm repay revolving credit facility. $35 mm available for future development of Monument draw onset. E 11/8/21 Q3-21 Earnings: Quarterly production and EBITDA of 17.7 Mboepd (4% YoY) and $23.0 (57% YoY). F 11/29/21 Company completed a strategic refinancing on a new first lien delayed draw term loan facility for up to $235 mm bearing interest of LIBOR +7%. Initial borrowings of 200 million to repay revolving credit facility. $35 mm available for future development of Monument Draw onset. G 2/28/22 Company provided operational update and preliminary 2022 guidance. Based on recently executed financing, the Company launched a multi-year drilling program. Company plans to spud 12 wells in 2022 (1 rig) for total estimated capital expenditure of $130-$150 mm. Total production 2022 guidance of 14 - 17 Mboepd (Oil 8 - 9.5 mboe/d). H 3/7/22 Q4-21 Earnings: Quarterly production and EBITDA of 17.3 Mboepd (0% YoY) and $20.4 (131% YoY). Annual production and EBITDA of 16.2 Mboepd (-4% YoY) and $72.7 (4% YoY). Proved reserves of 95.0 Mmboe (50% YoY). I 5/9/22 Q1-22 Earnings: Quarterly production and EBITDA of 14.8 Mboepd (3% YoY) and $11.8 (-23% YoY). Management noted goal of ramping up drilling activity to increase production and cash flow. Date Comment J 5/16/22 Company announced agreement to develop acid gas injection (AGI) facility, expecting it to increase profitability and reduce overall gathering and other costs by 20 – 30% on an annual basis. The Company contributed a well bore with an approved permit for the injection of acid gas and surface land for the facility and road access rights for 5% interest in the JV. The JV partner will provide remining capital for the facility and associated infrastructure. K 8/8/22 Q2-22 Earnings: Quarterly production and EBITDA of 15.0 Mboepd (-3% YoY) and $18.2 (29% YoY). L 11/14/22 Q3-22 Earnings: Quarterly production and EBITDA of 16.2 Mboepd (-8% YoY) and $24.3 (6% YoY). Company reiterated guidance on total production, total capital expenditures, and wells put online but lowered oil cut for the fiscal year 2022. Company management noted early results from test of the Third Bone Spring at Monument Draw were promising and in-line with Wolfcamp performance. M 1/20/23 Company announced appointment of Kristen McWatters as Chief Financial Officer. N 3/30/23 Q4-22 Earnings: Quarterly production and EBITDA of 15.7 Mboepd (-9% YoY) and $22.7 (12% YoY). Annual production and EBITDA of 15.4 Mboepd (-5% YoY) and $77.0 (6% YoY). Company issued redeemable convertible preferred stock to its existing three largest shareholders, receiving $24.4 mm in net proceeds to address liquidity needs. Company began testing procedures and initial processing at its AGI project. O 4/3/23 Company announced appointment of Matt Steele as Chief Executive. P 5/15/23 Q1-23 Earnings: Quarterly production and EBITDA of 16.2 Mboepd (9% YoY) and $26.1 (121% YoY). Company began testing procedures and initial processing at its AGI project. Q 8/4/23 Company announced Kristen McWatters resigned from her position as Executive Vice President, Chief Financial Officer and Treasurer. Matthew B. Steele, CEO, assumed the responsibilities of CFO. R 8/21/23 Q2-23 Earnings: Quarterly production and EBITDA of 14.3 Mboepd (-5% YoY) and $16.8 (-8% YoY). Company announces AGI facility expected to be fully online before year end. S 9/6/23 Company announced a private placement of 38,000 shares of Series A-1 Redeemable Convertible Preferred Stock, par value $0.0001 per share. A F G E C H J L M N O B K P D I Current Stock Price = $6.151 S R Q 1. Represents closing stock price on 11/1/23. Sources: Capital IQ and public filings. 31 |

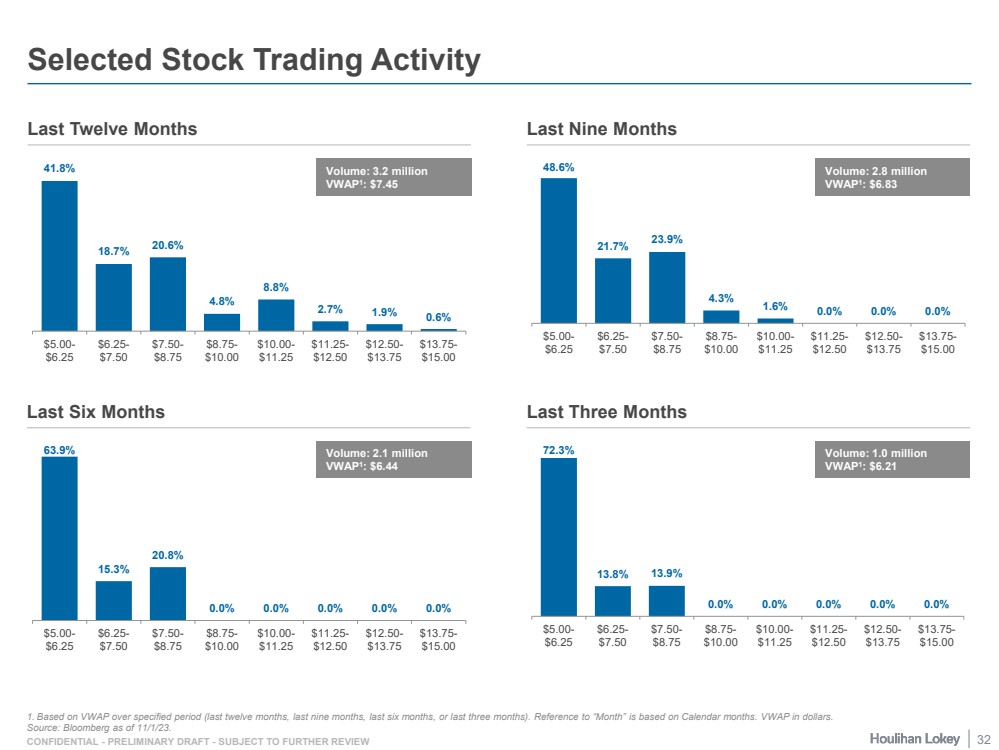

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW 41.8% 18.7% 20.6% 4.8% 8.8% 2.7% 1.9% 0.6% $5.00- $6.25 $6.25- $7.50 $7.50- $8.75 $8.75- $10.00 $10.00- $11.25 $11.25- $12.50 $12.50- $13.75 $13.75- $15.00 48.6% 21.7% 23.9% 4.3% 1.6% 0.0% 0.0% 0.0% $5.00- $6.25 $6.25- $7.50 $7.50- $8.75 $8.75- $10.00 $10.00- $11.25 $11.25- $12.50 $12.50- $13.75 $13.75- $15.00 63.9% 15.3% 20.8% 0.0% 0.0% 0.0% 0.0% 0.0% $5.00- $6.25 $6.25- $7.50 $7.50- $8.75 $8.75- $10.00 $10.00- $11.25 $11.25- $12.50 $12.50- $13.75 $13.75- $15.00 72.3% 13.8% 13.9% 0.0% 0.0% 0.0% 0.0% 0.0% $5.00- $6.25 $6.25- $7.50 $7.50- $8.75 $8.75- $10.00 $10.00- $11.25 $11.25- $12.50 $12.50- $13.75 $13.75- $15.00 Selected Stock Trading Activity Last Twelve Months Last Nine Months Last Six Months Last Three Months 1. Based on VWAP over specified period (last twelve months, last nine months, last six months, or last three months). Reference to “Month” is based on Calendar months. VWAP in dollars. Source: Bloomberg as of 11/1/23. Volume: 3.2 million VWAP1: $7.45 Volume: 2.8 million VWAP1: $6.83 Volume: 2.1 million VWAP1: $6.44 Volume: 1.0 million VWAP1: $6.21 32 |

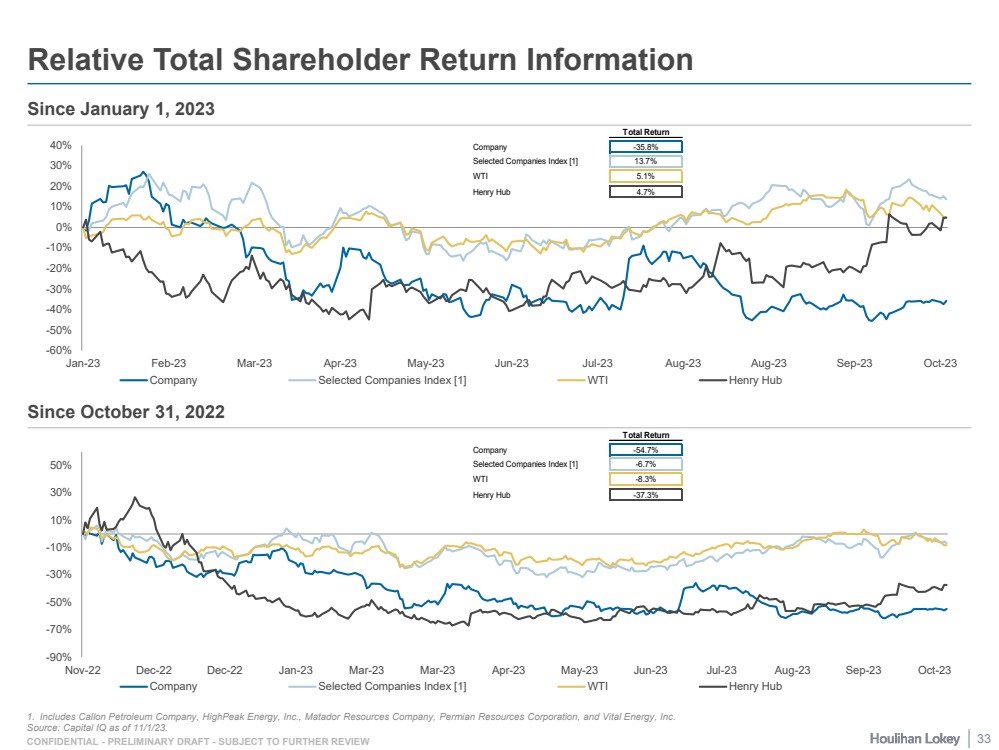

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW -90% -70% -50% -30% -10% 10% 30% 50% Nov-22 Dec-22 Dec-22 Jan-23 Mar-23 Mar-23 Apr-23 May-23 Jun-23 Jul-23 Aug-23 Sep-23 Oct-23 Company Selected Companies Index [1] WTI Henry Hub -60% -50% -40% -30% -20% -10% 0% 10% 20% 30% 40% Jan-23 Feb-23 Mar-23 Apr-23 May-23 Jun-23 Jul-23 Aug-23 Aug-23 Sep-23 Oct-23 Company Selected Companies Index [1] WTI Henry Hub Relative Total Shareholder Return Information Since January 1, 2023 1. Includes Callon Petroleum Company, HighPeak Energy, Inc., Matador Resources Company, Permian Resources Corporation, and Vital Energy, Inc. Source: Capital IQ as of 11/1/23. Since October 31, 2022 Total Return Company -35.8% Selected Companies Index [1] 13.7% WTI 5.1% Henry Hub 4.7% Total Return Company -54.7% Selected Companies Index [1] -6.7% WTI -8.3% Henry Hub -37.3% 33 |

| Page 1. Executive Summary 3 2. Financial Analyses 8 3. Selected Public Market Observations 29 4. Appendix 34 Weighted Average Cost of Capital Calculation 35 Observed Premiums Paid Analysis 38 Selected Series A Convertible Preferred Stock Terms 41 Glossary of Selected Terms 44 5. Disclaimer 47 |

| Page 1. Executive Summary 3 2. Financial Analyses 8 3. Selected Public Market Observations 29 4. Appendix 34 Weighted Average Cost of Capital Calculation 35 Observed Premiums Paid Analysis 38 Selected Series A Convertible Preferred Stock Terms 41 Glossary of Selected Terms 44 5. Disclaimer 47 |

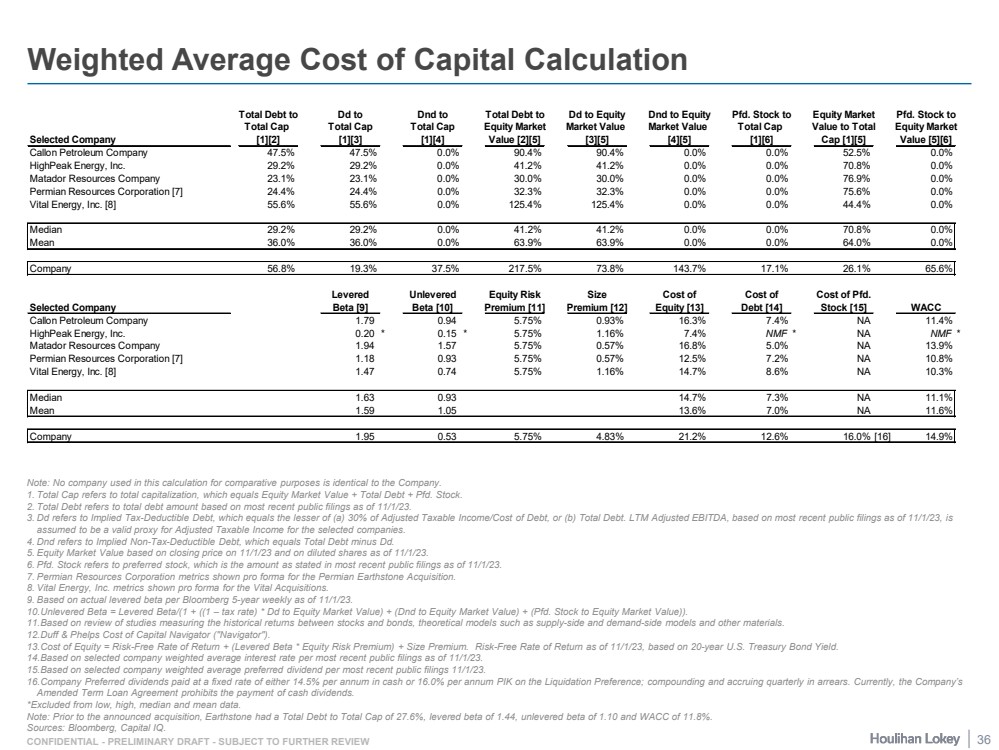

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Weighted Average Cost of Capital Calculation Note: No company used in this calculation for comparative purposes is identical to the Company. 1. Total Cap refers to total capitalization, which equals Equity Market Value + Total Debt + Pfd. Stock. 2. Total Debt refers to total debt amount based on most recent public filings as of 11/1/23. 3. Dd refers to Implied Tax-Deductible Debt, which equals the lesser of (a) 30% of Adjusted Taxable Income/Cost of Debt, or (b) Total Debt. LTM Adjusted EBITDA, based on most recent public filings as of 11/1/23, is assumed to be a valid proxy for Adjusted Taxable Income for the selected companies. 4. Dnd refers to Implied Non-Tax-Deductible Debt, which equals Total Debt minus Dd. 5. Equity Market Value based on closing price on 11/1/23 and on diluted shares as of 11/1/23. 6. Pfd. Stock refers to preferred stock, which is the amount as stated in most recent public filings as of 11/1/23. 7. Permian Resources Corporation metrics shown pro forma for the Permian Earthstone Acquisition. 8. Vital Energy, Inc. metrics shown pro forma for the Vital Acquisitions. 9. Based on actual levered beta per Bloomberg 5-year weekly as of 11/1/23. 10.Unlevered Beta = Levered Beta/(1 + ((1 – tax rate) * Dd to Equity Market Value) + (Dnd to Equity Market Value) + (Pfd. Stock to Equity Market Value)). 11.Based on review of studies measuring the historical returns between stocks and bonds, theoretical models such as supply-side and demand-side models and other materials. 12.Duff & Phelps Cost of Capital Navigator ("Navigator"). 13.Cost of Equity = Risk-Free Rate of Return + (Levered Beta * Equity Risk Premium) + Size Premium. Risk-Free Rate of Return as of 11/1/23, based on 20-year U.S. Treasury Bond Yield. 14.Based on selected company weighted average interest rate per most recent public filings as of 11/1/23. 15.Based on selected company weighted average preferred dividend per most recent public filings 11/1/23. 16.Company Preferred dividends paid at a fixed rate of either 14.5% per annum in cash or 16.0% per annum PIK on the Liquidation Preference; compounding and accruing quarterly in arrears. Currently, the Company’s Amended Term Loan Agreement prohibits the payment of cash dividends. *Excluded from low, high, median and mean data. Note: Prior to the announced acquisition, Earthstone had a Total Debt to Total Cap of 27.6%, levered beta of 1.44, unlevered beta of 1.10 and WACC of 11.8%. Sources: Bloomberg, Capital IQ. Total Debt to Dd to Dnd to Total Debt to Dd to Equity Dnd to Equity Pfd. Stock to Equity Market Pfd. Stock to Total Cap Total Cap Total Cap Equity Market Market Value Market Value Total Cap Value to Total Equity Market Selected Company [1][2] [1][3] [1][4] Value [2][5] [3][5] [4][5] [1][6] Cap [1][5] Value [5][6] Callon Petroleum Company 47.5% ### 47.5% ### 0.0% ### 90.4% ### 90.4% ### 0.0% ### 0.0% ### 52.5% ### 0.0% ### HighPeak Energy, Inc. 29.2% ### 29.2% ### 0.0% ### 41.2% ### 41.2% ### 0.0% ### 0.0% ### 70.8% ### 0.0% ### Matador Resources Company 23.1% ### 23.1% ### 0.0% ### 30.0% ### 30.0% ### 0.0% ### 0.0% ### 76.9% ### 0.0% ### Permian Resources Corporation [7] 24.4% ### 24.4% ### 0.0% ### 32.3% ### 32.3% ### 0.0% ### 0.0% ### 75.6% ### 0.0% ### Vital Energy, Inc. [8] 55.6% ### 55.6% ### 0.0% ### 125.4% ### 125.4% ### 0.0% ### 0.0% ### 44.4% ### 0.0% ### Median 29.2% 29.2% 0.0% 41.2% 41.2% 0.0% 0.0% 70.8% 0.0% Mean 36.0% 36.0% 0.0% 63.9% 63.9% 0.0% 0.0% 64.0% 0.0% Company 56.8% ### 19.3% ### 37.5% ### 217.5% ### 73.8% ### 143.7% ### 17.1% ### 26.1% ### 65.6% ### Debt Levered Unlevered Equity Risk Size Cost of Cost of Cost of Pfd. Selected Company Beta [5] Beta [9] Beta [10] Premium [11] Premium [12] Equity [13] Debt [14] Stock [15] WACC Callon Petroleum Company Input 1.79 ### 0.94 ### 5.75% 0.93% 16.3% ### 7.4% ### NA NA 11.4% ### HighPeak Energy, Inc. Input 0.20 * 0.15 * 5.75% 1.16% 7.4% ### NMF * NA NA NMF * Matador Resources Company Input 1.94 ### 1.57 ### 5.75% 0.57% 16.8% ### 5.0% ### NA NA 13.9% ### Permian Resources Corporation [7] Input 1.18 ### 0.93 ### 5.75% 0.57% 12.5% ### 7.2% ### NA NA 10.8% ### Vital Energy, Inc. [8] Input 1.47 ### 0.74 ### 5.75% 1.16% 14.7% ### 8.6% ### NA NA 10.3% ### Median 1.63 0.93 14.7% 7.3% NA 11.1% Mean 1.59 1.05 13.6% 7.0% NA 11.6% Company Input 1.95 ### 0.53 ### 5.75% 4.83% 21.2% ### 12.6% ### 16.0% [16] 14.9% ### 36 |

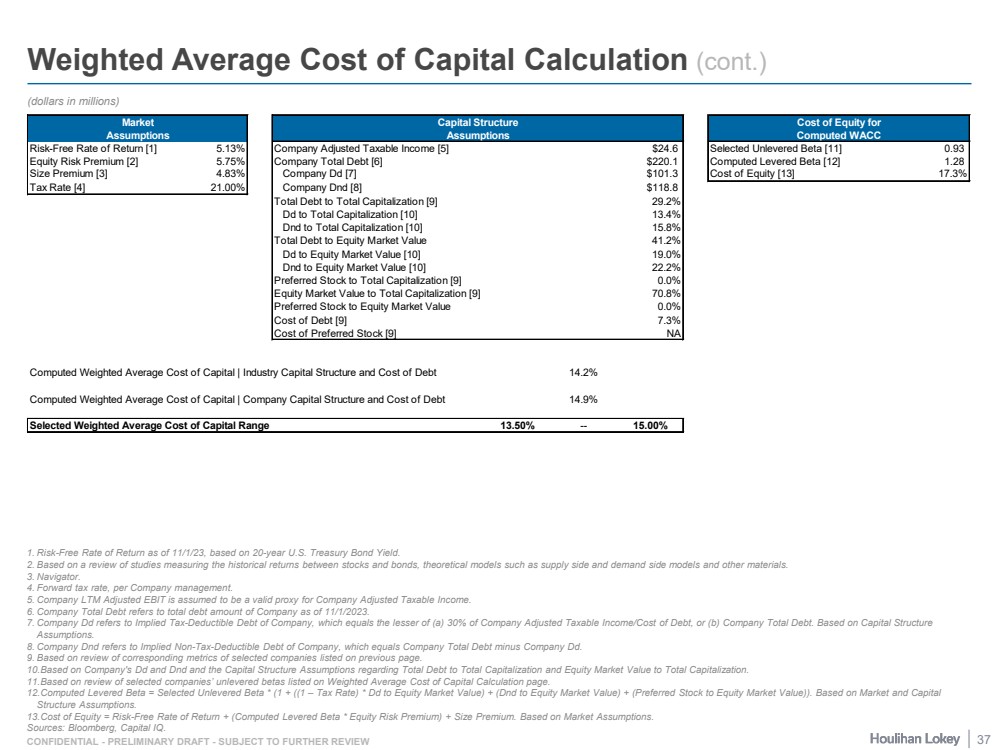

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Weighted Average Cost of Capital Calculation (cont.) 1. Risk-Free Rate of Return as of 11/1/23, based on 20-year U.S. Treasury Bond Yield. 2. Based on a review of studies measuring the historical returns between stocks and bonds, theoretical models such as supply side and demand side models and other materials. 3. Navigator. 4. Forward tax rate, per Company management. 5. Company LTM Adjusted EBIT is assumed to be a valid proxy for Company Adjusted Taxable Income. 6. Company Total Debt refers to total debt amount of Company as of 11/1/2023. 7. Company Dd refers to Implied Tax-Deductible Debt of Company, which equals the lesser of (a) 30% of Company Adjusted Taxable Income/Cost of Debt, or (b) Company Total Debt. Based on Capital Structure Assumptions. 8. Company Dnd refers to Implied Non-Tax-Deductible Debt of Company, which equals Company Total Debt minus Company Dd. 9. Based on review of corresponding metrics of selected companies listed on previous page. 10.Based on Company's Dd and Dnd and the Capital Structure Assumptions regarding Total Debt to Total Capitalization and Equity Market Value to Total Capitalization. 11.Based on review of selected companies’ unlevered betas listed on Weighted Average Cost of Capital Calculation page. 12.Computed Levered Beta = Selected Unlevered Beta * (1 + ((1 – Tax Rate) * Dd to Equity Market Value) + (Dnd to Equity Market Value) + (Preferred Stock to Equity Market Value)). Based on Market and Capital Structure Assumptions. 13.Cost of Equity = Risk-Free Rate of Return + (Computed Levered Beta * Equity Risk Premium) + Size Premium. Based on Market Assumptions. Sources: Bloomberg, Capital IQ. (dollars in millions) Market Capital Structure Cost of Equity for Assumptions Assumptions Computed WACC Risk-Free Rate of Return [1] 5.13% Company Adjusted Taxable Income [5] $24.6 Selected Unlevered Beta [11] 0.93 Equity Risk Premium [2] 5.75% Company Total Debt [6] $220.1 Computed Levered Beta [12] 1.28 Size Premium [3] 4.83% Company Dd [7] $101.3 Cost of Equity [13] 17.3% Tax Rate [4] 21.00% Company Dnd [8] $118.8 Debt Beta [15] Total Debt to Total Capitalization [9] 29.2% Dd to Total Capitalization [10] 13.4% Dnd to Total Capitalization [10] 15.8% Total Debt to Equity Market Value 41.2% Dd to Equity Market Value [10] 19.0% Dnd to Equity Market Value [10] 22.2% Preferred Stock to Total Capitalization [9] 0.0% Equity Market Value to Total Capitalization [9] 70.8% Preferred Stock to Equity Market Value 0.0% Cost of Debt [9] 7.3% Cost of Preferred Stock [9] NA Computed Weighted Average Cost of Capital | Industry Capital Structure and Cost of Debt 14.2% Computed Weighted Average Cost of Capital | Company Capital Structure and Cost of Debt 14.9% Selected Weighted Average Cost of Capital Range 13.50% -- 15.00% 37 |

| Page 1. Executive Summary 3 2. Financial Analyses 8 3. Selected Public Market Observations 29 4. Appendix 34 Weighted Average Cost of Capital Calculation 35 Observed Premiums Paid Analysis 38 Selected Series A Convertible Preferred Stock Terms 41 Glossary of Selected Terms 44 5. Disclaimer 47 |

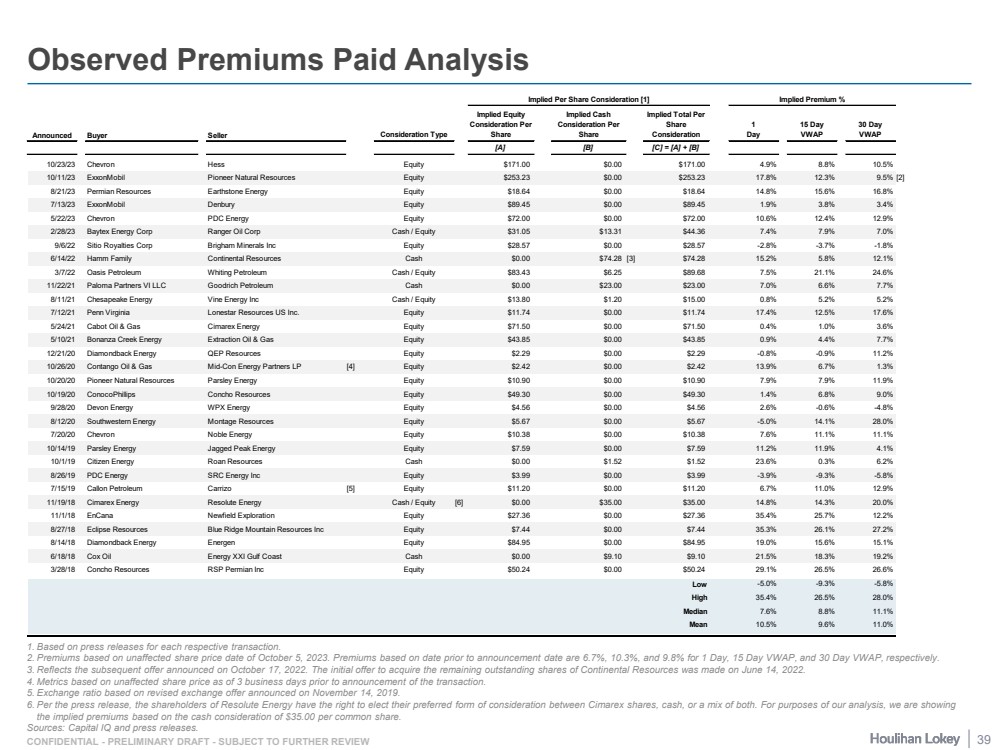

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Observed Premiums Paid Analysis 1. Based on press releases for each respective transaction. 2. Premiums based on unaffected share price date of October 5, 2023. Premiums based on date prior to announcement date are 6.7%, 10.3%, and 9.8% for 1 Day, 15 Day VWAP, and 30 Day VWAP, respectively. 3. Reflects the subsequent offer announced on October 17, 2022. The initial offer to acquire the remaining outstanding shares of Continental Resources was made on June 14, 2022. 4. Metrics based on unaffected share price as of 3 business days prior to announcement of the transaction. 5. Exchange ratio based on revised exchange offer announced on November 14, 2019. 6. Per the press release, the shareholders of Resolute Energy have the right to elect their preferred form of consideration between Cimarex shares, cash, or a mix of both. For purposes of our analysis, we are showing the implied premiums based on the cash consideration of $35.00 per common share. Sources: Capital IQ and press releases. Implied Per Share Consideration [1] Implied Premium % Announced Buyer Seller Consideration Type Implied Equity Consideration Per Share Implied Cash Consideration Per Share Implied Total Per Share Consideration 1 Day 15 Day VWAP 30 Day VWAP [A] [B] [C] = [A] + [B] 10/23/23 Chevron Hess Equity $171.00 $0.00 $171.00 4.9% 8.8% 10.5% 10/11/23 ExxonMobil Pioneer Natural Resources Equity $253.23 $0.00 $253.23 17.8% 12.3% 9.5% [2] 8/21/23 Permian Resources Earthstone Energy Equity $18.64 $0.00 $18.64 14.8% 15.6% 16.8% 7/13/23 ExxonMobil Denbury Equity $89.45 $0.00 $89.45 1.9% 3.8% 3.4% 5/22/23 Chevron PDC Energy Equity $72.00 $0.00 $72.00 10.6% 12.4% 12.9% 2/28/23 Baytex Energy Corp Ranger Oil Corp Cash / Equity $31.05 $13.31 $44.36 7.4% 7.9% 7.0% 9/6/22 Sitio Royalties Corp Brigham Minerals Inc Equity $28.57 $0.00 $28.57 -2.8% -3.7% -1.8% 6/14/22 Hamm Family Continental Resources Cash $0.00 $74.28 [3] $74.28 15.2% 5.8% 12.1% 3/7/22 Oasis Petroleum Whiting Petroleum Cash / Equity $83.43 $6.25 $89.68 7.5% 21.1% 24.6% 11/22/21 Paloma Partners VI LLC Goodrich Petroleum Cash $0.00 $23.00 $23.00 7.0% 6.6% 7.7% 8/11/21 Chesapeake Energy Vine Energy Inc Cash / Equity $13.80 $1.20 $15.00 0.8% 5.2% 5.2% 7/12/21 Penn Virginia Lonestar Resources US Inc. Equity $11.74 $0.00 $11.74 17.4% 12.5% 17.6% 5/24/21 Cabot Oil & Gas Cimarex Energy Equity $71.50 $0.00 $71.50 0.4% 1.0% 3.6% 5/10/21 Bonanza Creek Energy Extraction Oil & Gas Equity $43.85 $0.00 $43.85 0.9% 4.4% 7.7% 12/21/20 Diamondback Energy QEP Resources Equity $2.29 $0.00 $2.29 -0.8% -0.9% 11.2% 10/26/20 Contango Oil & Gas Mid-Con Energy Partners LP [4] Equity $2.42 $0.00 $2.42 13.9% 6.7% 1.3% 10/20/20 Pioneer Natural Resources Parsley Energy Equity $10.90 $0.00 $10.90 7.9% 7.9% 11.9% 10/19/20 ConocoPhillips Concho Resources Equity $49.30 $0.00 $49.30 1.4% 6.8% 9.0% 9/28/20 Devon Energy WPX Energy Equity $4.56 $0.00 $4.56 2.6% -0.6% -4.8% 8/12/20 Southwestern Energy Montage Resources Equity $5.67 $0.00 $5.67 -5.0% 14.1% 28.0% 7/20/20 Chevron Noble Energy Equity $10.38 $0.00 $10.38 7.6% 11.1% 11.1% 10/14/19 Parsley Energy Jagged Peak Energy Equity $7.59 $0.00 $7.59 11.2% 11.9% 4.1% 10/1/19 Citizen Energy Roan Resources Cash $0.00 $1.52 $1.52 23.6% 0.3% 6.2% 8/26/19 PDC Energy SRC Energy Inc Equity $3.99 $0.00 $3.99 -3.9% -9.3% -5.8% 7/15/19 Callon Petroleum Carrizo [5] Equity $11.20 $0.00 $11.20 6.7% 11.0% 12.9% 11/19/18 Cimarex Energy Resolute Energy Cash / Equity [6] $0.00 $35.00 $35.00 14.8% 14.3% 20.0% 11/1/18 EnCana Newfield Exploration Equity $27.36 $0.00 $27.36 35.4% 25.7% 12.2% 8/27/18 Eclipse Resources Blue Ridge Mountain Resources Inc Equity $7.44 $0.00 $7.44 35.3% 26.1% 27.2% 8/14/18 Diamondback Energy Energen Equity $84.95 $0.00 $84.95 19.0% 15.6% 15.1% 6/18/18 Cox Oil Energy XXI Gulf Coast Cash $0.00 $9.10 $9.10 21.5% 18.3% 19.2% 3/28/18 Concho Resources RSP Permian Inc Equity $50.24 $0.00 $50.24 29.1% 26.5% 26.6% Low -5.0% -9.3% -5.8% High 35.4% 26.5% 28.0% Median 7.6% 8.8% 11.1% Mean 10.5% 9.6% 11.0% 39 |

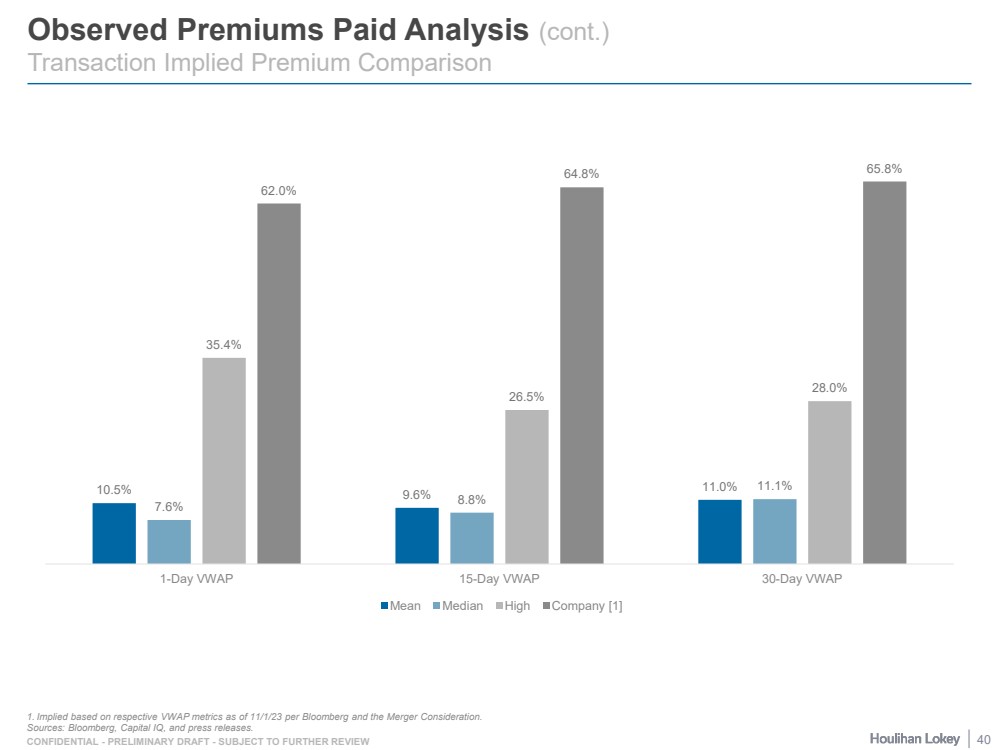

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Observed Premiums Paid Analysis (cont.) Transaction Implied Premium Comparison 1. Implied based on respective VWAP metrics as of 11/1/23 per Bloomberg and the Merger Consideration. Sources: Bloomberg, Capital IQ, and press releases. 10.5% 9.6% 11.0% 7.6% 8.8% 11.1% 35.4% 26.5% 28.0% 62.0% 64.8% 65.8% 1-Day VWAP 15-Day VWAP 30-Day VWAP Mean Median High Company [1] 40 |

| Page 1. Executive Summary 3 2. Financial Analyses 8 3. Selected Public Market Observations 29 4. Appendix 34 Weighted Average Cost of Capital Calculation 35 Observed Premiums Paid Analysis 38 Selected Series A Convertible Preferred Stock Terms 41 Glossary of Selected Terms 44 5. Disclaimer 47 |

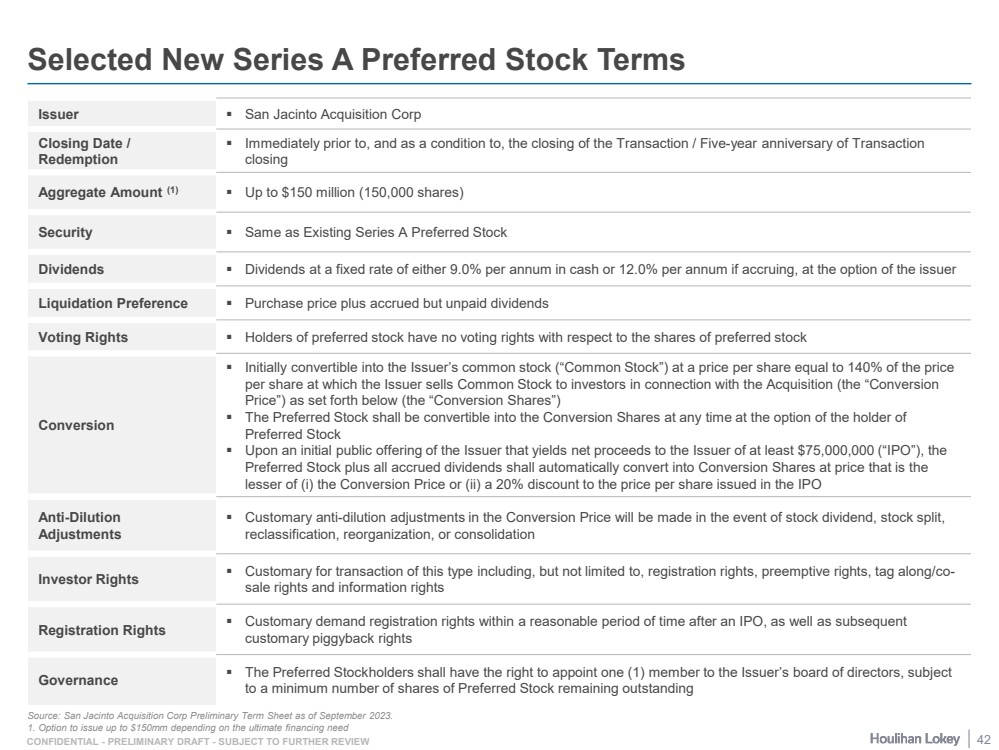

| CONFIDENTIAL - PRELIMINARY DRAFT - SUBJECT TO FURTHER REVIEW Selected New Series A Preferred Stock Terms Source: San Jacinto Acquisition Corp Preliminary Term Sheet as of September 2023. 1. Option to issue up to $150mm depending on the ultimate financing need Issuer San Jacinto Acquisition Corp Closing Date / Redemption Immediately prior to, and as a condition to, the closing of the Transaction / Five-year anniversary of Transaction closing Aggregate Amount (1) Up to $150 million (150,000 shares) Security Same as Existing Series A Preferred Stock Dividends Dividends at a fixed rate of either 9.0% per annum in cash or 12.0% per annum if accruing, at the option of the issuer Liquidation Preference Purchase price plus accrued but unpaid dividends Voting Rights Holders of preferred stock have no voting rights with respect to the shares of preferred stock Conversion Initially convertible into the Issuer’s common stock (“Common Stock”) at a price per share equal to 140% of the price per share at which the Issuer sells Common Stock to investors in connection with the Acquisition (the “Conversion Price”) as set forth below (the “Conversion Shares”) The Preferred Stock shall be convertible into the Conversion Shares at any time at the option of the holder of Preferred Stock Upon an initial public offering of the Issuer that yields net proceeds to the Issuer of at least $75,000,000 (“IPO”), the Preferred Stock plus all accrued dividends shall automatically convert into Conversion Shares at price that is the lesser of (i) the Conversion Price or (ii) a 20% discount to the price per share issued in the IPO Anti-Dilution Adjustments Customary anti-dilution adjustments in the Conversion Price will be made in the event of stock dividend, stock split, reclassification, reorganization, or consolidation Investor Rights Customary for transaction of this type including, but not limited to, registration rights, preemptive rights, tag along/co-sale rights and information rights Registration Rights Customary demand registration rights within a reasonable period of time after an IPO, as well as subsequent customary piggyback rights Governance The Preferred Stockholders shall have the right to appoint one (1) member to the Issuer’s board of directors, subject to a minimum number of shares of Preferred Stock remaining outstanding 42 |