We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Name | Symbol | Market | Type |

|---|---|---|---|

| Bank Nova Scotia Halifax (PK) | USOTC:BNSPF | OTCMarkets | Preference Share |

| Price Change | % Change | Price | Bid Price | Offer Price | High Price | Low Price | Open Price | Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0.00 | 0.00% | 18.71 | 18.59 | 37.74 | 0.00 | 01:00:00 |

|

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-261476 (To Prospectus dated December 29, 2021, Prospectus Supplement dated December 29, 2021 and Product Supplement EQUITY LIRN-1 dated July

28, 2023)

|

|

3,303,601 Units

$10 principal amount per unit

CUSIP No. 06418H600

|

Pricing Date

Settlement Date

Maturity Date

|

April 25, 2024

May 2, 2024

April 24, 2026

|

|||

|

|

|||||

|

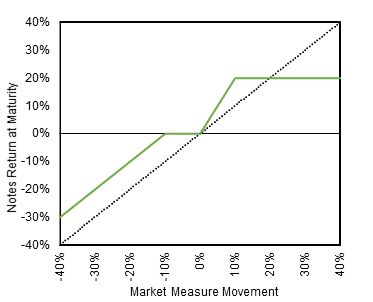

Capped Leveraged Index Return Notes® Linked to the Invesco S&P 500® Equal Weight ETF

◾ Maturity of approximately 2 years

◾ 2-to-1 leveraged upside exposure to increases in the Underlying Fund, subject to a capped return of 20.00%

◾ 1-to-1 downside exposure to decreases in the Underlying Fund beyond a 10.00% decline, with up to 90.00% of your principal at risk

◾ All payments occur at maturity and are subject to the credit risk of The Bank of Nova Scotia

◾ No periodic interest payments

◾ In addition to the underwriting discount set forth below, the notes include a hedging-related charge of $0.075 per unit. See “Structuring the Notes”

◾ Limited secondary market liquidity, with no exchange listing

◾ The notes are unsecured debt securities and are not savings accounts or insured deposits of a bank. The notes are not insured or guaranteed by the Canada Deposit Insurance

Corporation (the “CDIC”), the U.S. Federal Deposit Insurance Corporation (the “FDIC”), or any other governmental agency of Canada, the United States or any other jurisdiction

|

|||||

|

Per Unit

|

Total

|

|

|

Public offering price

|

$10.00

|

$33,036,010.00

|

|

Underwriting discount

|

$0.20

|

$660,720.20

|

|

Proceeds, before expenses, to BNS

|

$9.80

|

$32,375,289.80

|

|

Are Not FDIC Insured

|

Are Not Bank Guaranteed

|

May Lose Value

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Issuer:

|

The Bank of Nova Scotia (“BNS”)

|

||

|

Principal

Amount:

|

$10.00 per unit

|

||

|

Term:

|

Approximately 2 years

|

||

|

Market

Measure:

|

The Invesco S&P 500® Equal Weight ETF (Bloomberg symbol: “RSP”)

|

||

|

Starting

Value:

|

$162.35

|

||

|

Ending Value:

|

The average of the Closing Market Price of the Market Measure multiplied by the Price Multiplier on each calculation day occurring during

the Maturity Valuation Period. The scheduled calculation days are subject to postponement in the event of Market Disruption Events, as described beginning on page PS-27 of product supplement EQUITY LIRN-1.

|

||

|

Threshold

Value:

|

$146.12 (90.00% of the Starting Value, rounded to two decimal places).

|

||

|

Participation

Rate:

|

200.00%

|

||

|

Capped

Value:

|

$12.00 per unit, which represents a return of 20.00% over the principal amount.

|

||

|

Price

Multiplier:

|

1, subject to adjustment for certain corporate events relating to the Underlying Fund, as described beginning on page PS-28 of product

supplement EQUITY LIRN-1.

|

||

|

Maturity

Valuation

Period:

|

April 15, 2026, April 16, 2026, April 17, 2026, April 20, 2026 and April 21, 2026

|

||

|

Fees and

Charges:

|

The underwriting discount of $0.20 per unit listed on the cover page and the hedging related charge of $0.075 per unit described in

“Structuring the Notes” on page TS-14.

|

||

|

Calculation

Agent:

|

BofA Securities, Inc. (“BofAS”).

|

|

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

| ◾ |

Product supplement EQUITY LIRN-1 dated July 28, 2023:

|

| ◾ |

Prospectus supplement dated December 29, 2021:

|

| ◾ |

Prospectus dated December 29, 2021:

|

| ◾ |

You anticipate that the price of the Underlying Fund will increase moderately from the Starting Value to the Ending Value.

|

| ◾ |

You are willing to risk a substantial loss of principal if the price of the Underlying Fund decreases from the Starting Value to an Ending Value that is below the Threshold Value.

|

| ◾ |

You accept that the return on the notes will be capped.

|

| ◾ |

You are willing to forgo interest payments that are paid on conventional interest-bearing debt securities.

|

| ◾ |

You are willing to forgo dividends or other benefits of directly owning the Underlying Fund or the securities included in the Underlying Fund.

|

| ◾ |

You are willing to accept a limited or no market for sales prior to maturity, and understand that the market prices for the notes, if any, will be affected by various factors, including our actual and perceived

creditworthiness, our internal funding rate and fees and charges on the notes.

|

|

◾

|

You are willing to assume our credit risk, as issuer of the notes, for all payments under the notes, including the Redemption Amount.

|

| ◾ |

You believe that the price of the Underlying Fund will decrease from the Starting Value to the Ending Value or that it will not increase sufficiently over the term of the notes to provide you with your desired return.

|

| ◾ |

You seek 100% principal repayment or preservation of capital.

|

| ◾ |

You seek an uncapped return on your investment.

|

| ◾ |

You seek interest payments or other current income on your investment.

|

| ◾ |

You want to receive dividends or other benefits of directly owning the Underlying Fund or the securities included in the Underlying Fund.

|

| ◾ |

You seek an investment for which there will be a liquid secondary market.

|

|

◾

|

You are unwilling or are unable to take market risk on the notes or to take our credit risk as issuer of the notes.

|

|

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

|

|

Ending Value

|

Percentage Change from the

Starting Value to the Ending

Value

|

Redemption Amount per

Unit

|

Total Rate of Return on the

Notes

|

|

0.00

|

-100.00%

|

$1.00

|

-90.00%

|

|

25.00

|

-75.00%

|

$3.50

|

-65.00%

|

|

50.00

|

-50.00%

|

$6.00

|

-40.00%

|

|

60.00

|

-40.00%

|

$7.00

|

-30.00%

|

|

70.00

|

-30.00%

|

$8.00

|

-20.00%

|

|

80.00

|

-20.00%

|

$9.00

|

-10.00%

|

|

90.00(1)

|

-10.00%

|

$10.00

|

0.00%

|

|

95.00

|

-5.00%

|

$10.00

|

0.00%

|

|

100.00(2)

|

0.00%

|

$10.00

|

0.00%

|

|

102.00

|

2.00%

|

$10.40

|

4.00%

|

|

105.00

|

5.00%

|

$11.00

|

10.00%

|

|

107.00

|

7.00%

|

$11.40

|

14.00%

|

|

110.00

|

10.00%

|

$12.00(3)

|

20.00%

|

|

120.00

|

20.00%

|

$12.00

|

20.00%

|

|

130.00

|

30.00%

|

$12.00

|

20.00%

|

|

140.00

|

40.00%

|

$12.00

|

20.00%

|

|

150.00

|

50.00%

|

$12.00

|

20.00%

|

| (1) |

This is the hypothetical Threshold Value.

|

| (2) |

The hypothetical Starting Value of 100.00 used in these examples has been chosen for illustrative purposes only. The actual Starting Value is $162.35, which was the Closing Market Price of

the Underlying Fund on the pricing date.

|

|

(3)

|

The Redemption Amount per unit cannot exceed the Capped Value.

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Example 1

|

|

|

The Ending Value is 60.00, or 60.00% of the Starting Value:

|

|

|

Starting Value:

|

100.00

|

|

Threshold Value:

|

90.00

|

|

Ending Value:

|

60.00

|

|

|

= $7.00 Redemption Amount per unit

|

|

Example 2

|

|

|

The Ending Value is 90.00, or 90.00% of the Starting Value:

|

|

|

Starting Value:

|

100.00

|

|

Threshold Value:

|

90.00

|

|

Ending Value:

|

90.00

|

|

Redemption Amount per unit = $10.00, the principal amount, since the Ending Value is less than the Starting Value but equal to or greater than the Threshold Value.

|

|

|

Example 3

|

|

|

The Ending Value is 102.00, or 102.00% of the Starting Value:

|

|

|

Starting Value:

|

100.00

|

|

Ending Value:

|

102.00

|

|

|

= $10.40 Redemption Amount per unit

|

|

Example 4

|

|

|

The Ending Value is 130.00, or 130.00% of the Starting Value:

|

|

|

Starting Value:

|

100.00

|

|

Ending Value:

|

130.00

|

|

|

= $16.00, however, because the Redemption Amount for the notes cannot exceed the Capped Value, the Redemption Amount will be $12.00 per unit

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

| ◾ |

Depending on the performance of the Underlying Fund as measured shortly before the maturity date, your investment may result in a loss; there is no guaranteed return of principal.

|

| ◾ |

Your return on the notes may be less than the yield you could earn by owning a conventional fixed or floating rate debt security of comparable maturity.

|

| ◾ |

Your investment return is limited to the return represented by the Capped Value and may be less than a comparable investment directly in the Underlying Fund or the securities held by the Underlying Fund.

|

| ◾ |

The sponsor of the Underlying Fund may adjust the Underlying Fund in a way that may adversely affect the value of the notes and the amount payable on the notes, and these entities have no obligation to consider your interests.

|

| ◾ |

The sponsor of the S&P 500® Equal Weight Index (the “Underlying Index”), described below, may adjust the Underlying Index in a way that affects its level, and has no obligation to consider your interests.

|

| ◾ |

You will have no rights of a holder of the Underlying Fund or the securities held by the Underlying Fund, and you will not be entitled to receive any shares of the Underlying Fund or the securities held by the Underlying Fund, or

any dividends or other distributions in respect of the Underlying Fund or the securities held by the Underlying Fund.

|

| ◾ |

While we, MLPF&S, BofAS or their or our respective affiliates may from time to time own shares of the Underlying Fund or the securities held by the Underlying Fund, except to the extent that the common stock of Bank of

America Corporation (the parent company of MLPF&S and BofAS), is held by the Underlying Fund, none of us, MLPF&S, BofAS or our or their respective affiliates control the Underlying Fund or any company held by the Underlying

Fund, and have not verified any disclosure made by the Underlying Fund or any other company.

|

| ◾ |

There are liquidity and management risks associated with the Underlying Fund.

|

| ◾ |

The performance of the Underlying Fund may not correlate with the performance of its Underlying Index as well as the net asset value per share of the Underlying Fund, especially during periods of market volatility when the

liquidity and the market price of the shares of the Underlying Fund and/or the securities held by the Underlying Fund may be adversely affected, sometimes materially.

|

| ◾ |

The Redemption Amount will not be adjusted for all corporate events that could affect the Underlying Fund. See “Description of LIRNs—Anti-Dilution and Discontinuance Adjustments Relating to Underlying Funds” beginning on page

PS-30 of product supplement EQUITY LIRN-1

|

| ◾ |

Our initial estimated value of the notes is lower than the public offering price of the notes. Our initial estimated value of the notes is only an estimate. The public offering price of the notes exceeds our initial estimated

value because it includes costs associated with selling and structuring the notes, as well as hedging our obligations under the notes with a third party, which may include BofAS or one of its affiliates. These costs include the

underwriting discount and an expected hedging related charge, as further described in “Structuring the Notes” on page TS-14.

|

| ◾ |

Our initial estimated value of the notes does not represent future values of the notes and may differ from others’ estimates. Our initial estimated value of the notes is determined by reference to our internal pricing models when

the terms of the notes are set. These pricing models consider certain factors, such as our internal funding rate on the pricing date, the expected term of the notes, market conditions and other relevant factors existing at that

time, and our assumptions about market parameters, which can include volatility, dividend rates, interest rates and other factors. Different pricing models and assumptions could provide valuations for the notes that are different

from our initial estimated value. In addition, market conditions and other relevant factors in the future may change, and any of our assumptions may prove to be incorrect. On future dates, the market value of the notes could change

significantly based on, among other things, the performance of the Underlying Fund, changes in market conditions, our creditworthiness, interest rate movements and other relevant factors. These factors, together with various credit,

market and economic factors over the term of the notes, are expected to reduce the price at which you may be able to sell the notes in any secondary market and will affect the value of the notes in complex and unpredictable ways.

Our initial estimated value does not represent a minimum price at which we or any agents would be willing to buy your notes in any secondary market (if any exists) at any time.

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

| ◾ |

Our initial estimated value is not determined by reference to credit spreads or the borrowing rate we would pay for our conventional fixed-rate debt securities. The internal funding rate used in the determination of our initial

estimated value of the notes generally represents a discount from the credit spreads for our conventional fixed-rate debt securities and the borrowing rate we would pay for our conventional fixed-rate debt securities. If we were to

use the interest rate implied by the credit spreads for our conventional fixed-rate debt securities, or the borrowing rate we would pay for our conventional fixed-rate debt securities, we would expect the economic terms of the notes

to be more favorable to you. Consequently, our use of an internal funding rate for the notes would have an adverse effect on the economic terms of the notes, the initial estimated value of the notes on the pricing date, and the

price at which you may be able to sell the notes in any secondary market.

|

| ◾ |

A trading market is not expected to develop for the notes. None of us, MLPF&S or BofAS is obligated to make a market for, or to repurchase, the notes. There is no assurance that any party will be willing to purchase your

notes at any price in any secondary market.

|

| ◾ |

Our business, hedging and trading activities, and those of MLPF&S, BofAS and our and their respective affiliates (including trades in the Underlying Fund or the securities held by the Underlying Fund), and any hedging and

trading activities we, MLPF&S, BofAS or our or their respective affiliates engage in for our clients’ accounts, may affect the market value of, and return on, the notes and may create conflicts of interest with you.

|

| ◾ |

There may be potential conflicts of interest involving the calculation agent, which is BofAS. We have the right to appoint and remove the calculation agent.

|

| ◾ |

Payments on the notes are subject to our credit risk, and actual or perceived changes in our creditworthiness are expected to affect the value of the notes. If we become insolvent or are unable to pay our obligations, you may

lose your entire investment.

|

| ◾ |

The U.S. federal income tax consequences of the notes are uncertain, and may be adverse to a holder of the notes. See “Summary of U.S. Federal Income Tax Consequences” below.

|

| ◾ |

The conclusion that no portion of the interest paid or credited or deemed to be paid or credited on a note will be “Participating Debt Interest” subject to Canadian withholding tax is based in part on the current published

administrative position of the CRA. There cannot be any assurance that CRA’s current published administrative practice will not be subject to change, including potential expansion in the current administrative interpretation of

Participating Debt Interest subject to Canadian withholding tax. If, at any time, the interest paid or credited or deemed to be paid or credited on a note is subject to Canadian withholding tax, you will receive an amount that is

less than the Redemption Amount. You should consult your own adviser as to the potential for such withholding and the potential for reduction or refund of part or all of such withholding, including under any bilateral Canadian tax

treaty the benefits of which you may be entitled. For a discussion of the Canadian federal income tax consequences of investing in the notes, see “Summary of Canadian Federal Income Tax Consequences” below, “Canadian Taxation—Debt

Securities” on page 66 of the prospectus and “Supplemental Discussion of Canadian Federal Income Tax Consequences” on page PS-40 of product supplement EQUITY LIRN-1.

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

| • |

Domicile. Only common stocks of U.S. companies are eligible. For index purposes, a U.S. company has the following characteristics:

|

| o |

the company files 10-K annual reports;

|

| o |

the U.S. portion of fixed assets and revenues constitutes a plurality of the total, but need not exceed 50%. When these factors are in conflict, fixed assets determine plurality. Revenue determines

plurality when there is incomplete asset information. Geographic information for revenue and fixed asset allocations are determined by the company as reported in its annual filings. If this criteria is not met or is ambiguous, SPDJI

may still deem the company to be a U.S. company for index purposes if its primary listing, headquarters and incorporation are all in the United States and/or “a domicile of convenience” (Bermuda, Channel Islands, Gibraltar, islands

in the Caribbean, Isle of Man, Luxembourg, Liberia or Panama); and

|

| o |

the primary listing is on an eligible U.S. exchange.

|

| • |

Exchange Listing. A primary listing on one of the following U.S. exchanges is required: NYSE, NYSE Arca, NYSE American, Nasdaq Global Select Market, Nasdaq Select Market, Nasdaq Capital

Market, Cboe BZX, Cboe BYX, Cboe EDGA or Cboe EDGX exchanges. Ineligible exchanges include the OTC Bulletin Board and Pink Sheets.

|

| • |

Organizational Structure and Share Type. Eligible organizational structures and share types are corporations (including equity and

mortgage REITS) and common stock (i.e., shares). Ineligible organizational structures and share types include business development companies, limited partnerships, master limited partnerships, limited liability companies,

closed-end funds, exchange-traded funds, exchange-traded notes, royalty trusts, special purpose acquisition companies, preferred and convertible preferred stock, unit trusts, equity warrants, convertible bonds, investment trusts,

rights, American Depositary Receipts and tracking stocks. As of July 31, 2017, companies with multiple share class structures are not eligible to be added to the S&P U.S. Indices, but securities already included in the S&P

U.S. Indices have been grandfathered and will remain in the S&P U.S. Indices.

|

| • |

Market Capitalization. The unadjusted company market capitalization should be within a specified range. Such ranges are reviewed

quarterly and updated as needed to ensure they reflect current market conditions. For spin-offs, S&P U.S. Index membership eligibility is determined using when-issued prices, if available.

|

| • |

Liquidity. Using composite pricing and volume, the ratio of annual dollar value traded (defined as average closing price over the

period multiplied by historical volume over the last 365 calendar days) to float-adjusted market capitalization should be at least 1.00, and the stock should trade a minimum of 250,000 shares in each of the six months leading up

to the evaluation date.

|

| • |

IWF. The IWF for each company represents the portion of the total shares outstanding that are considered part of the public float for purposes of the S&P U.S. Indices. An IWF of at

least 0.10 is required.

|

| • |

Financial Viability. The sum of the most recent four consecutive quarters’ Generally Accepted Accounting Principles (GAAP) earnings

(net income excluding discontinued operations) should be positive as should the most recent quarter. For REITs, financial viability is based on GAAP earnings and/or Funds From Operations (FFO), if reported.

|

| • |

Treatment of IPOs. Initial public offerings should be traded on an eligible exchange for at least 12 months before being considered

for addition to an S&P U.S. Index. Spin-offs or in-specie distributions from existing constituents do not need to be seasoned for 12 months prior to their inclusion in an S&P U.S. Index.

|

| • |

Sector Balance. A company is evaluated for its contribution to sector balance maintenance, as measured by a comparison of each GICS® sector’s weight in an index with its weight in the S&P U.S. Total Market Index, in the relevant market capitalization range. The S&P Total Market Index is

a float-adjusted, market-capitalization weighted index designed to track the broad U.S. equity market, including large-, mid-, small- and micro-cap stocks.

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

| • |

A company involved in a merger, acquisition or significant restructuring such that it no longer meets the eligibility criteria is deleted from the S&P U.S. Indices at a time announced by SPDJI,

normally at the close of the last day of trading or expiration of a tender offer. Constituents that are halted from trading may be kept in the index until trading resumes, at the discretion of the Index Committee. If a stock is

moved to the pink sheets or the bulletin board, the stock is removed.

|

| • |

A company that substantially violates one or more of the eligibility criteria may be deleted at the Index Committee’s discretion.

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

|

Capped Leveraged Index Return Notes®

Linked to the Invesco S&P 500® Equal Weight ETF due April 24, 2026

|

1 Year Bank Nova Scotia Halifax (PK) Chart |

1 Month Bank Nova Scotia Halifax (PK) Chart |

It looks like you are not logged in. Click the button below to log in and keep track of your recent history.

Support: +44 (0) 203 8794 460 | support@advfn.com

By accessing the services available at ADVFN you are agreeing to be bound by ADVFN's Terms & Conditions

Hot Features

Hot Features