We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Share Name | Share Symbol | Market | Type |

|---|---|---|---|

| SouthState Corporation | NASDAQ:SSB | NASDAQ | Common Stock |

| Price Change | % Change | Share Price | Bid Price | Offer Price | High Price | Low Price | Open Price | Shares Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0.00 | 0.00% | 85.74 | 35.06 | 87.45 | 0 | 01:00:00 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

(Exact name of registrant as specified in its charter)

(State or Other Jurisdiction of Incorporation) | (Commission File Number) | (IRS Employer Identification No.) |

(Address of principal executive offices) | (Zip Code) |

(

(Registrant’s telephone number, including area code)

Not Applicable

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 2.02 | Results of Operations and Financial Condition. |

On April 25, 2024, SouthState Corporation (“SouthState” or the “Company”) issued a press release announcing its financial results for the three-month period ended March 31, 2024, along with certain other financial information. Copies of the Company’s press release and presentation are attached as Exhibit 99.1 and 99.2, respectively, to this report and incorporated herein by reference.

SouthState will host a conference call on April 26, 2023 at 9 a.m. (ET) to discuss the Company’s first quarter 2024 results. Investors may call in (toll free) by dialing (888) 350-3899 within the U.S. and (646) 960-0343 for all other locations (passcode 4200408; host: Will Matthews, CFO). The numbers for international participants are listed at https://events.q4irportal.com/custom/access/2324/. Participants may also pre-register for the conference by navigating to https://events.q4inc.com/attendee/271118037. Access detail will be provided via email upon completion of registration.

Item 7.01 | Regulation FD Disclosure. | |||||

On April 25, 2024, the Company also made available the presentation (“Presentation”) prepared for use with the press release during the earnings conference call on April 26, 2024. Attached hereto and incorporated herein as Exhibit 99.2 is the text of that presentation.

The information contained in this Item 7.01 of this Current Report, including the information set forth in the Presentation filed as Exhibit 99.2 to, and incorporated in, this Current Report, is being "furnished" and shall not be deemed to be “filed” for purposes of Section 18 of the Exchange Act, or otherwise subject to the liability of that section, and shall not be incorporated by reference into any registration statement or other document filed under the Securities Act or the Exchange Act, except as shall be expressly set forth by specific reference in such filing.

Item 8.01 | Other Events. |

Second Quarter 2024 Shareholder Dividend

The Board of Directors of the Company declared a quarterly cash dividend on its common stock of $0.52 per share, payable on May 17, 2024 to shareholders of record as of May 10, 2024.

Item 9.01 | Financial Statements and Exhibits. | |||

(d) | Exhibits: | |||

Exhibit No. | Description | |||

104 | Cover Page Interactive Data File (embedded within the Inline XBRL document) | |||

2

Cautionary Statement Regarding Forward Looking Statements

Statements included in this communication, which are not historical in nature are intended to be, and are hereby identified as, forward-looking statements for purposes of the safe harbor provided by Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements are based on, among other things, management’s beliefs, assumptions, current expectations, estimates and projections about the financial services industry, the economy and SouthState. Words and phrases such as “may,” “approximately,” “continue,” “should,” “expects,” “projects,” “anticipates,” “is likely,” “look ahead,” “look forward,” “believes,” “will,” “intends,” “estimates,” “strategy,” “plan,” “could,” “potential,” “possible” and variations of such words and similar expressions are intended to identify such forward-looking statements.

SouthState cautions readers that forward-looking statements are subject to certain risks, uncertainties and assumptions that are difficult to predict with regard to, among other things, timing, extent, likelihood and degree of occurrence, which could cause actual results to differ materially from anticipated results. Such risks, uncertainties and assumptions, include, among others, the following: (1) economic downturn risk, potentially resulting in deterioration in the credit markets, inflation, greater than expected noninterest expenses, excessive loan losses and other negative consequences, which risks could be exacerbated by potential negative economic developments resulting from federal spending cuts and/or one or more federal budget-related impasses or actions; (2) risks related to the ability of the Company to pursue its strategic plans which depend upon certain growth goals in our lines of business; (3) risks relating to the ability to retain our culture and attract and retain qualified people, which could be exacerbated by the continuing work from remote environment; (4) credit risks associated with an obligor’s failure to meet the terms of any contract with the Bank or otherwise fail to perform as agreed under the terms of any loan-related document; (5) interest rate risk primarily resulting from our inability to effectively manage the risk, and their impact on the Bank’s earnings, including from the correspondent and mortgage divisions, housing demand, the market value of the Bank’s loan and securities portfolios, and the market value of SouthState’s equity; (6) a decrease in our net interest income due to the interest rate environment; (7) liquidity risk affecting the Bank’s ability to meet its obligations when they come due; (8) unexpected outflows of uninsured deposits may require us to sell investment securities at a loss; (9) potential deterioration in real estate values; (10) the loss of value of our investment portfolio could negatively impact market perceptions of us and could lead to deposit withdrawals; (11) price risk focusing on changes in market factors that may affect the value of traded instruments in “mark-to-market” portfolios; (12) transaction risk arising from problems with service or product delivery; (13) the impact of increasing digitization of the banking industry and movement of customers to on-line platforms, and the possible impact on the Bank’s results of operations, customer base, expenses, suppliers and operations; (14) controls and procedures risk, including the potential failure or circumvention of our controls and procedures or failure to comply with regulations related to controls and procedures; (15) volatility in the financial services industry (including failures or rumors of failures of other depository institutions), along with actions taken by governmental agencies to address such turmoil, could affect the ability of depository institutions, including us, to attract and retain depositors and to borrow or raise capital; (16) the impact of competition with other financial institutions, including deposit and loan pricing pressures and the resulting impact, including as a result of compression to net interest margin; (17) compliance risk involving risk to earnings or capital resulting from violations of or nonconformance with laws, rules, regulations, prescribed practices, or ethical standards, and contractual obligations regarding data privacy and cybersecurity; (18) regulatory change risk resulting from new laws, rules, regulations, accounting principles, proscribed practices or ethical standards, including, without limitation, the possibility that regulatory agencies may require higher levels of capital above the current regulatory-mandated minimums and including the impact of special FDIC assessments, the Consumer Financial Protection Bureau regulations or other guidance, and the possibility of changes in accounting standards, policies, principles and practices; (19) strategic risk resulting from adverse business decisions or improper implementation of business decisions; (20) reputation risk that adversely affects earnings or capital arising from negative public opinion including the effects of social media on market perceptions of us and banks generally; (21) cybersecurity risk related to the dependence of SouthState on internal computer systems and the technology of outside service providers, as well as the potential impacts of internal or external security breaches, which may subject the Company to potential business disruptions or financial losses resulting from deliberate attacks or unintentional events; (22) reputational and operational risks associated with environment, social and governance (ESG) matters, including the impact of changes in federal and state laws, regulations and guidance relating to climate change; (23) excessive loan losses; (24) reputational risk and possible higher than estimated reduced revenue from previously announced or proposed regulatory changes in the Bank’s consumer programs and products; (25) operational, technological, cultural, regulatory, legal, credit and other risks associated with the exploration, consummation and integration of potential future acquisitions, whether involving stock or cash consideration; (26) catastrophic events such as hurricanes, tornados, earthquakes, floods or other natural or human disasters, including public health crises and infectious disease outbreaks, as well as any government actions in response to such events, and the related disruption to local, regional and global economic activity and financial markets, and the impact that any of the foregoing may have on SouthState and its customers and other constituencies; (27) geopolitical risk from terrorist activities and armed conflicts that may result in economic and supply disruptions, and loss of market and consumer confidence; (28) the risks of fluctuations in market prices for SouthState common stock that may or may not reflect economic condition or performance of SouthState; (29) the payment of dividends on SouthState common stock, which is subject to legal and regulatory limitations as well as the discretion of the board of directors of SouthState, SouthState’s performance and other factors; (30) ownership dilution risk associated with potential acquisitions in which SouthState’s stock may be issued as consideration for an acquired company; and (31) other factors that may affect future results of SouthState, as disclosed in SouthState’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K, filed by SouthState with the U.S.

3

Securities and Exchange Commission (“SEC”) and available on the SEC’s website at http://www.sec.gov, any of which could cause actual results to differ materially from future results expressed, implied or otherwise anticipated by such forward-looking statements.

All forward-looking statements speak only as of the date they are made and are based on information available at that time. SouthState does not undertake any obligation to update or otherwise revise any forward-looking statements, whether as a result of new information, future events, or otherwise, except as required by federal securities laws. As forward-looking statements involve significant risks and uncertainties, caution should be exercised against placing undue reliance on such statements.

4

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

SOUTHSTATE CORPORATION | ||

(Registrant) | ||

By: | /s/ William E. Matthews, V | |

Dated: April 25, 2024

5

Exhibit 99.1

SouthState Corporation Reports First Quarter 2024 Results Declares Quarterly Cash Dividend | For Immediate Release | |

Media Contact | ||

Jackie Smith, 803.231.3486 | ||

WINTER HAVEN, FL – April 25, 2024 – SouthState Corporation (NYSE: SSB) today released its unaudited results of operations and other financial information for the three-month period ended March 31, 2024.

“In the midst of a transition year for the US economy, SouthState produced first quarter revenue and earnings per share in line with our guidance", commented John C. Corbett, SouthState’s Chief Executive Officer. "Loans and deposits grew in the low-single digit percent range and asset quality remains stable with strong reserves. Our markets are resilient, and people are migrating to the South as an attractive place to live and grow a business."

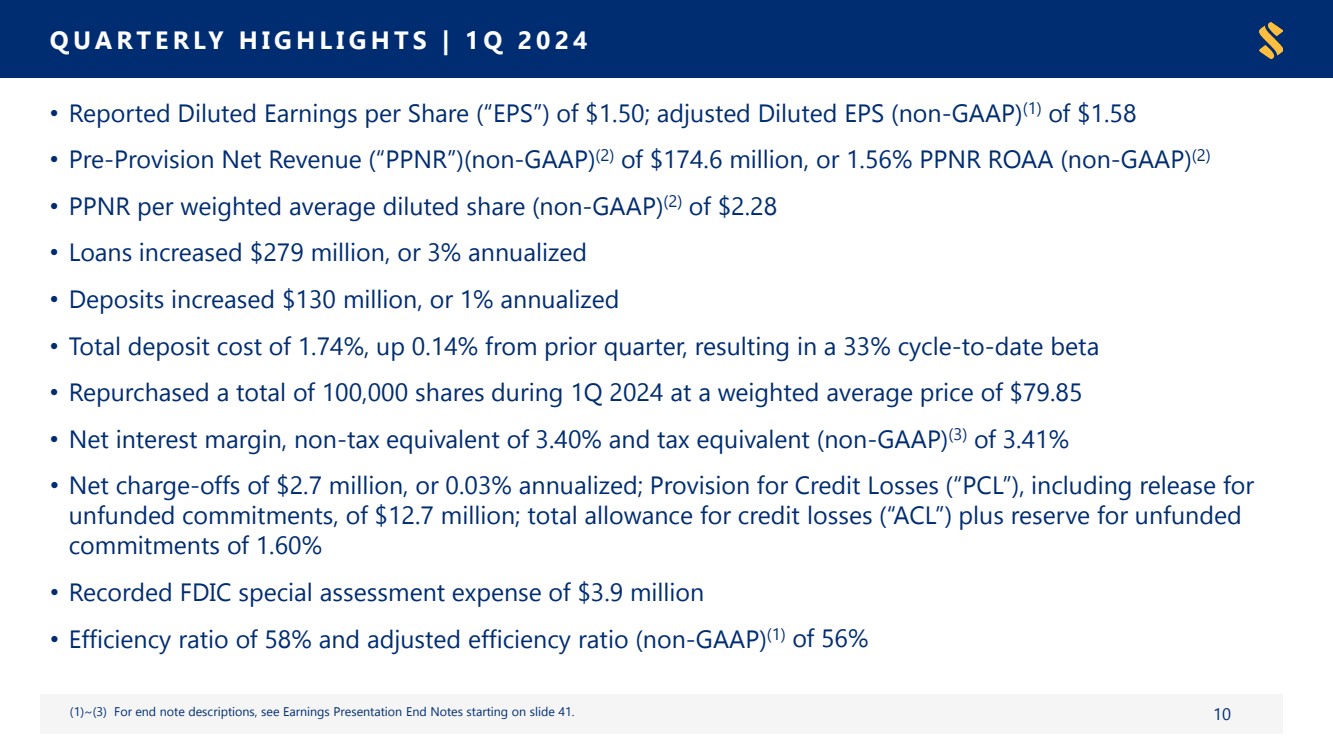

Highlights of the first quarter of 2024 include:

Returns

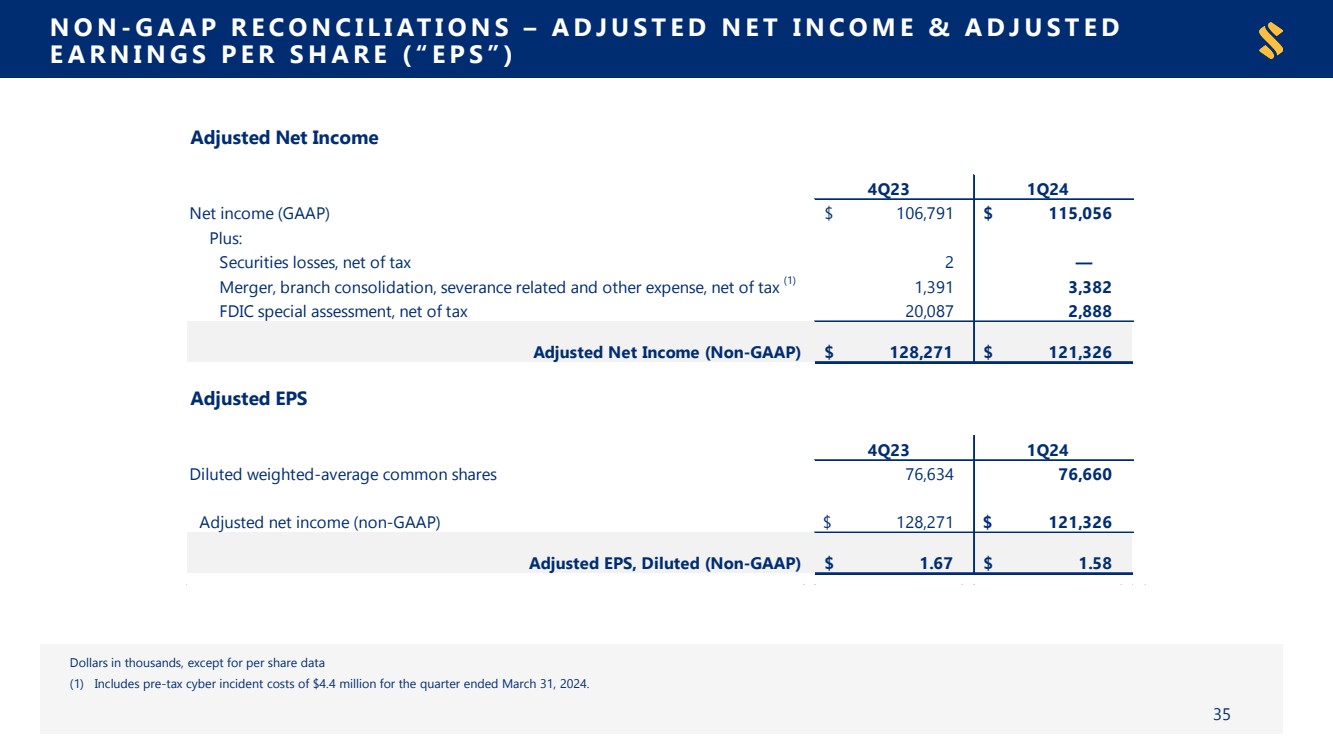

| ● | Reported Diluted Earnings per Share (“EPS”) of $1.50; Adjusted Diluted EPS (Non-GAAP) of $1.58 |

| ● | Net Income of $115.1 million; Adjusted Net Income (Non-GAAP) of $121.3 million |

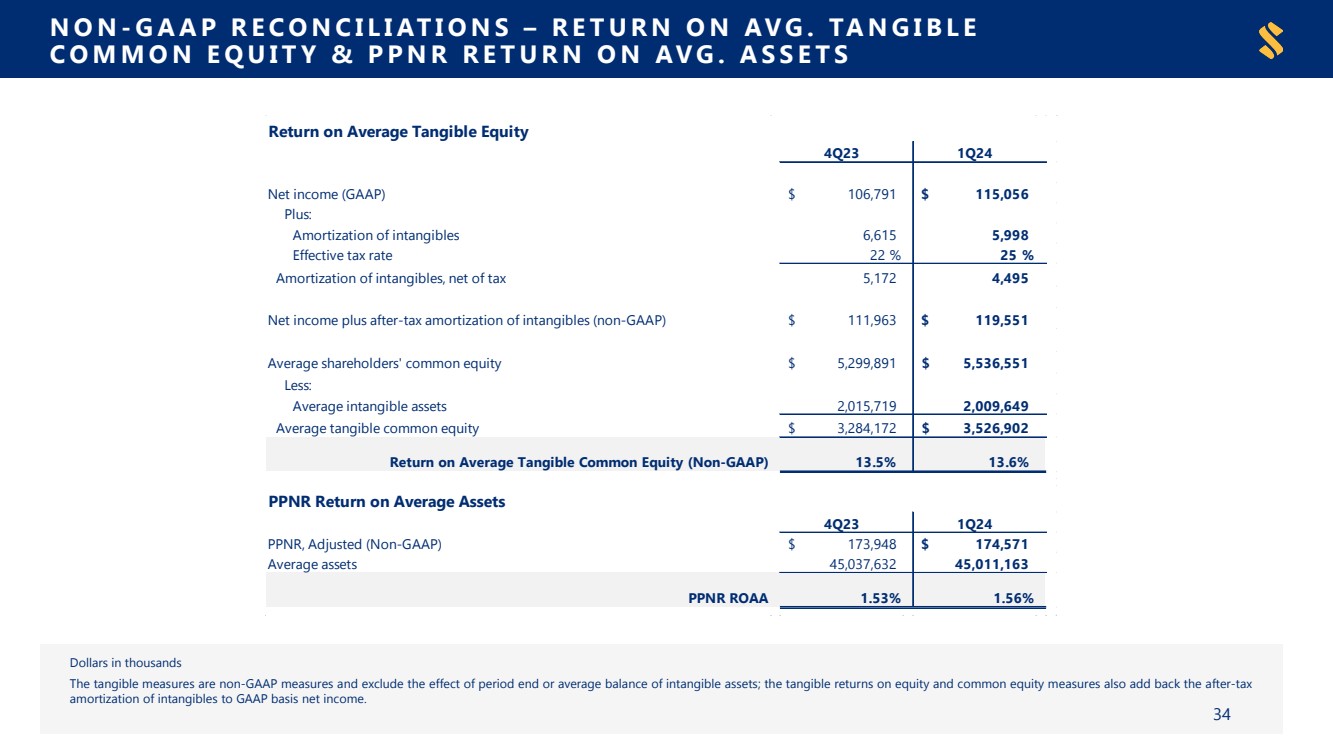

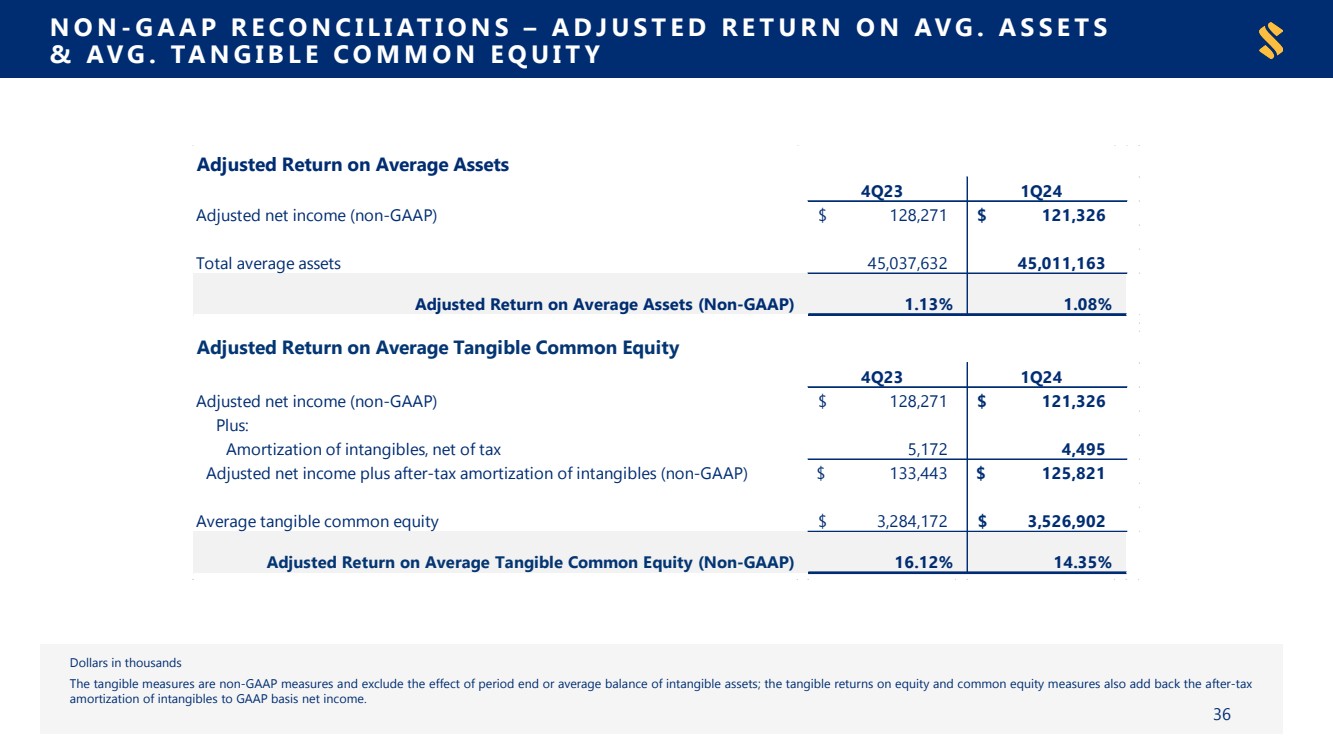

| ● | Return on Average Common Equity of 8.4%; Return on Average Tangible Common Equity (Non-GAAP) of 13.6% and Adjusted Return on Average Tangible Common Equity (Non-GAAP) of 14.4%* |

| ● | Return on Average Assets (“ROAA”) of 1.03% and Adjusted ROAA (Non-GAAP) of 1.08%* |

| ● | Pre-Provision Net Revenue (“PPNR”) per Weighted Average Diluted Share (Non-GAAP) of $2.28 |

| ● | Book Value per Share of $72.82; Tangible Book Value (“TBV”) per Share (Non-GAAP) of $46.48 |

Performance

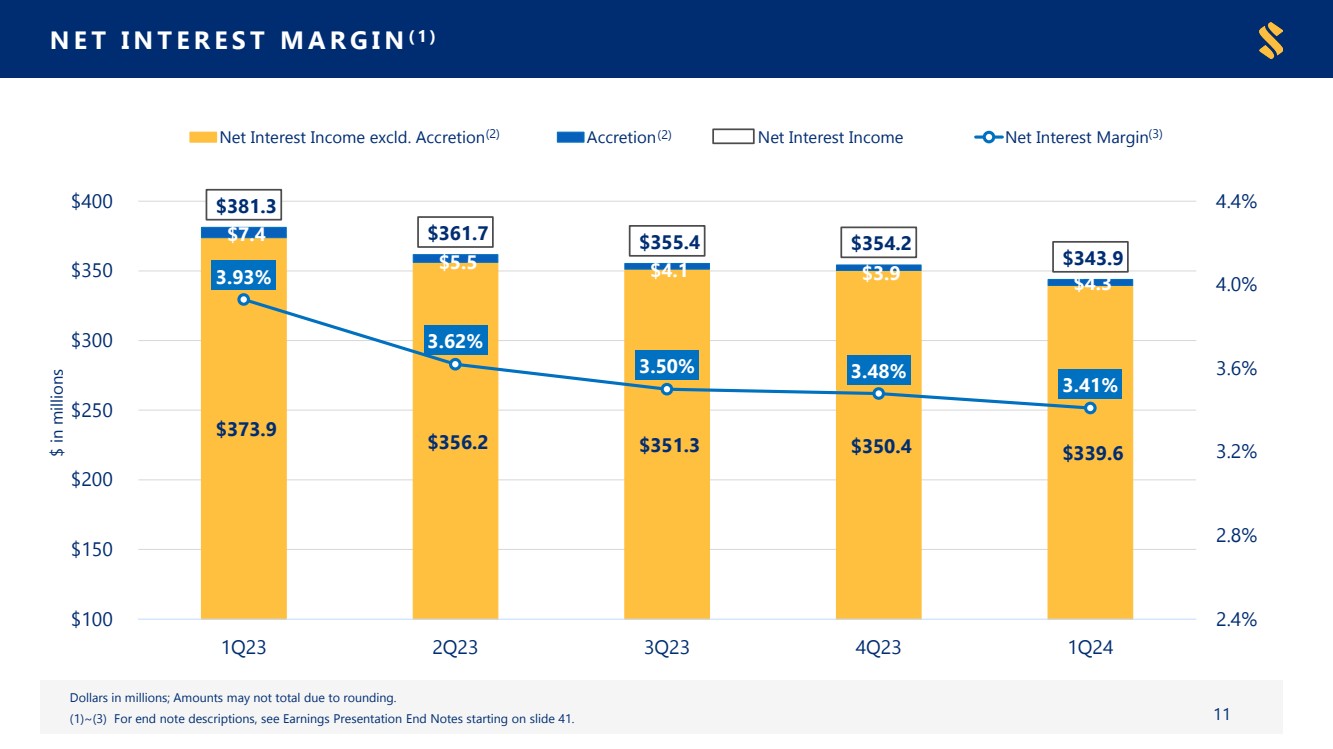

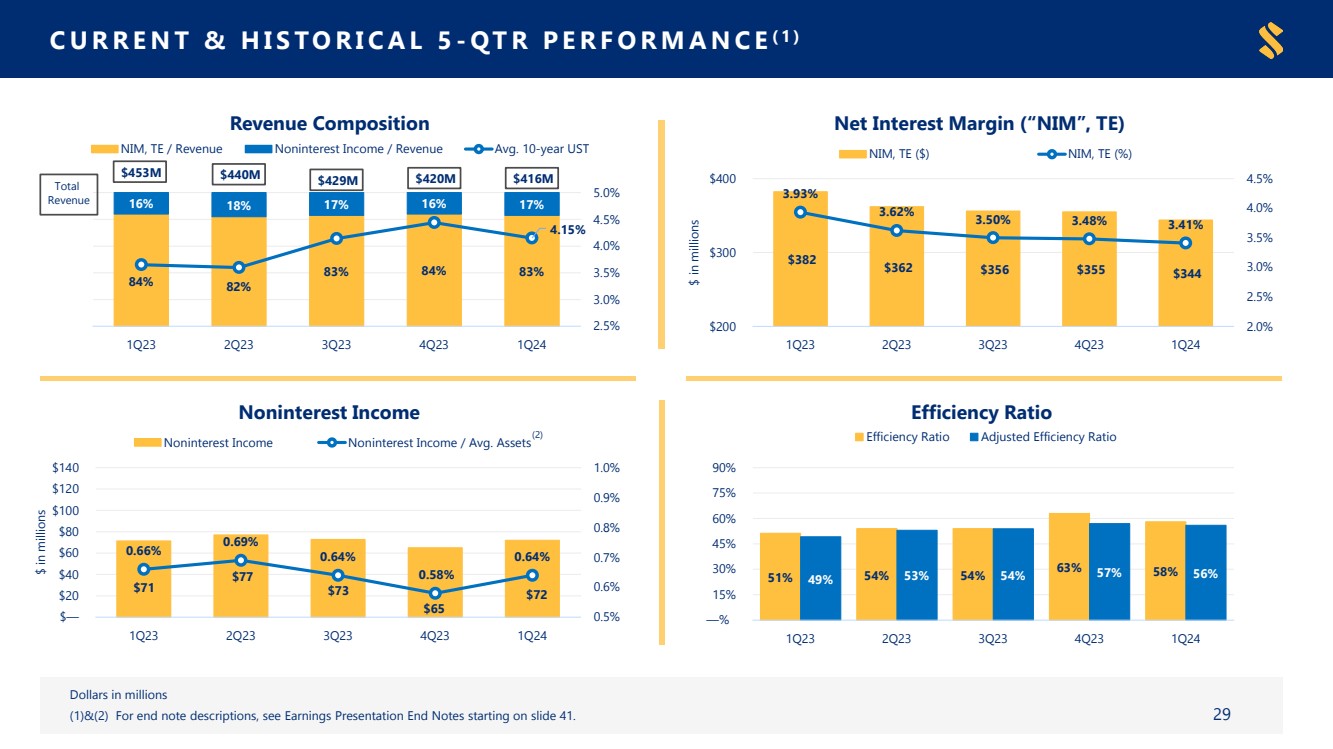

| ● | Net Interest Income of $344 million; Core Net Interest Income (excluding loan accretion) (Non-GAAP) of $340 million |

| ● | Net Interest Margin (“NIM”), non-tax equivalent of 3.40% and tax equivalent (Non-GAAP) of 3.41% |

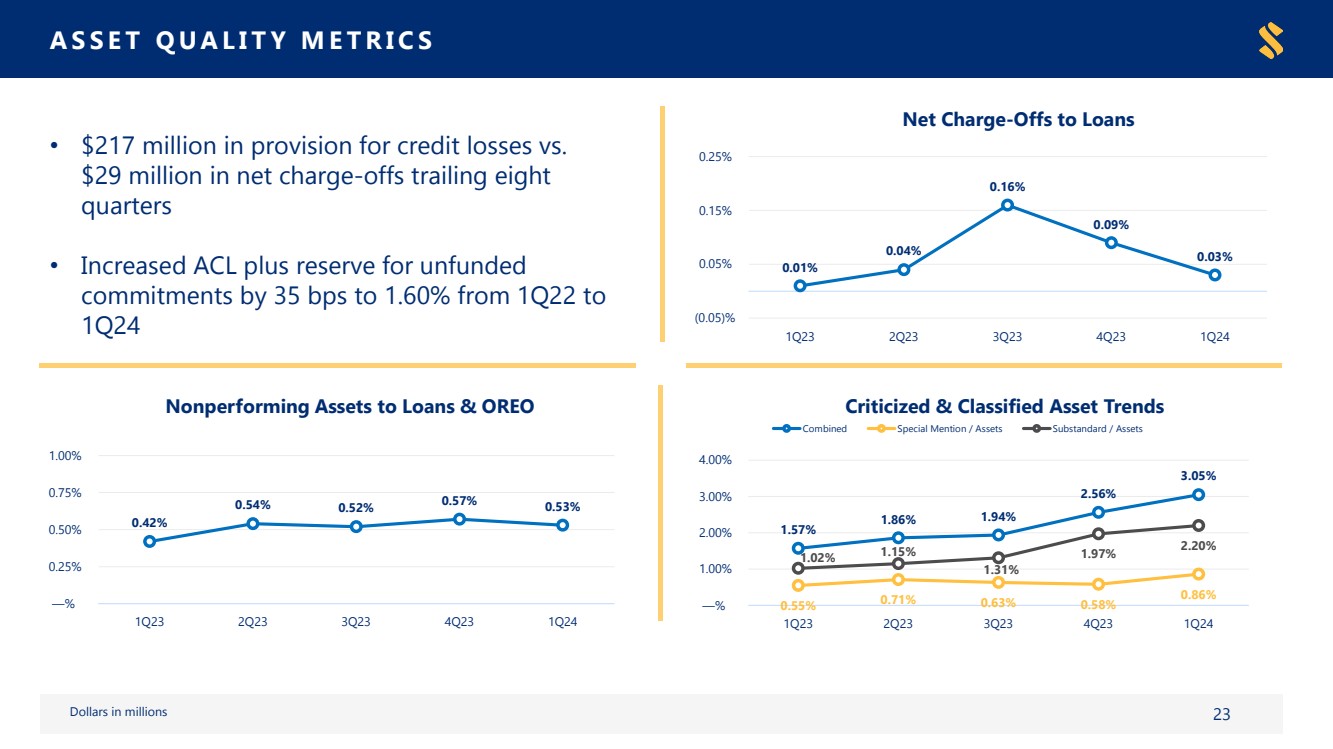

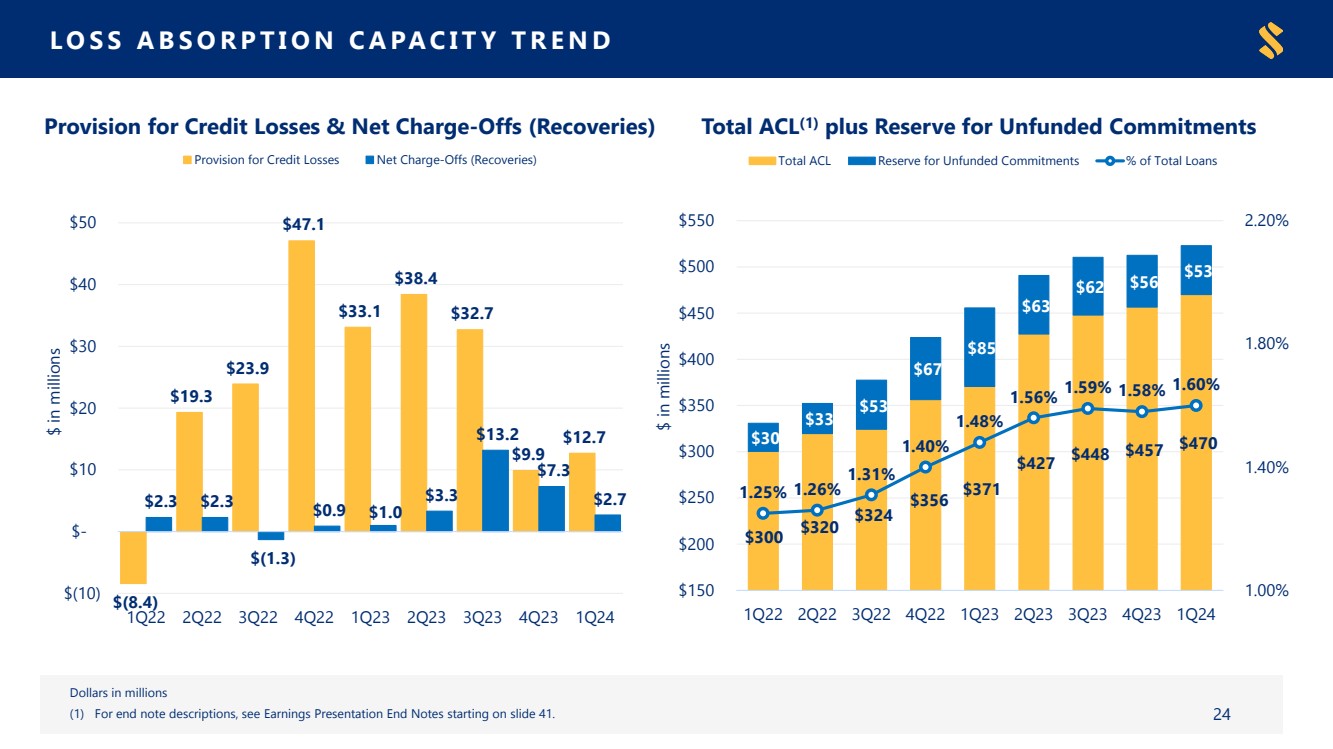

| ● | Net charge-offs of $2.7 million, or 0.03% annualized; $12.7 million Provision for Credit Losses (“PCL”), including release for unfunded commitments; total allowance for credit losses (“ACL”) plus reserve for unfunded commitments of 1.60% |

| ● | Noninterest Income of $72 million; Noninterest Income represented 0.64% of average assets for the first quarter of 2024 |

| ● | Recorded FDIC special assessment expense of $3.9 million |

| ● | Efficiency Ratio of 58% and Adjusted Efficiency Ratio (Non-GAAP) of 56% |

Balance Sheet

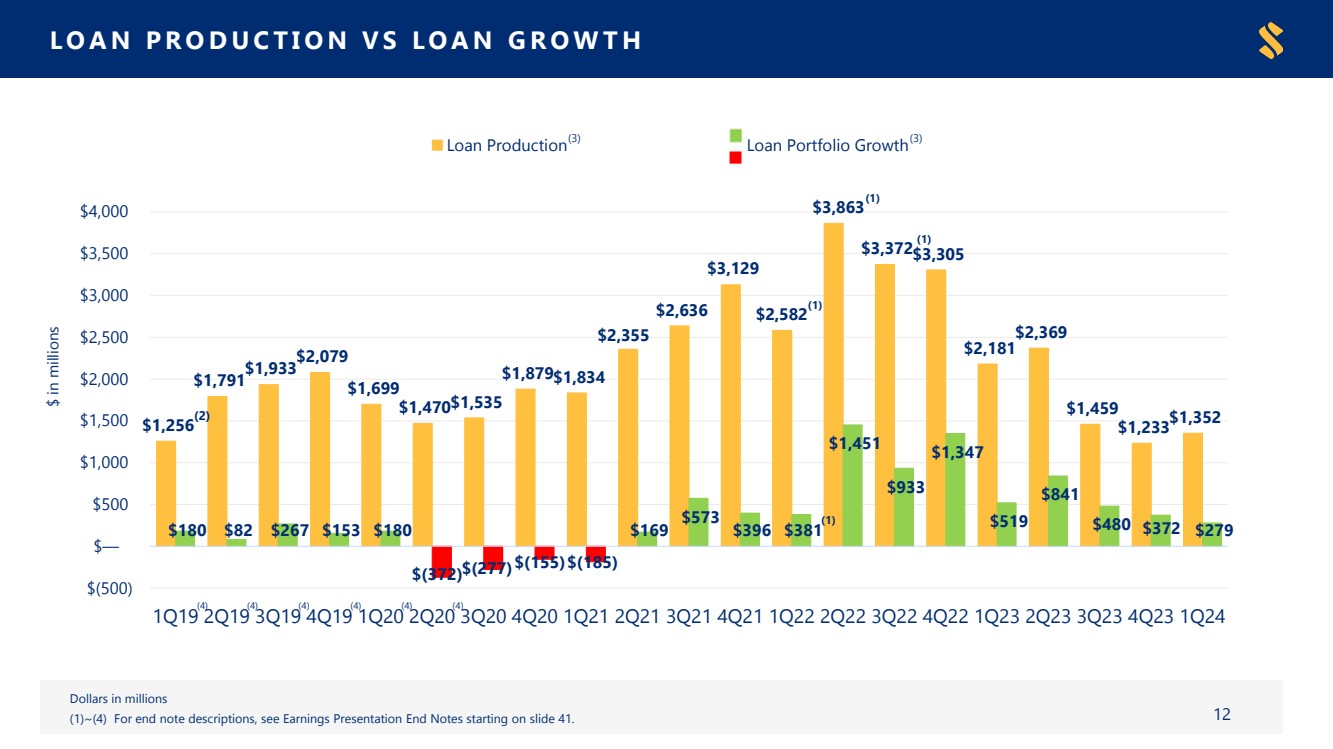

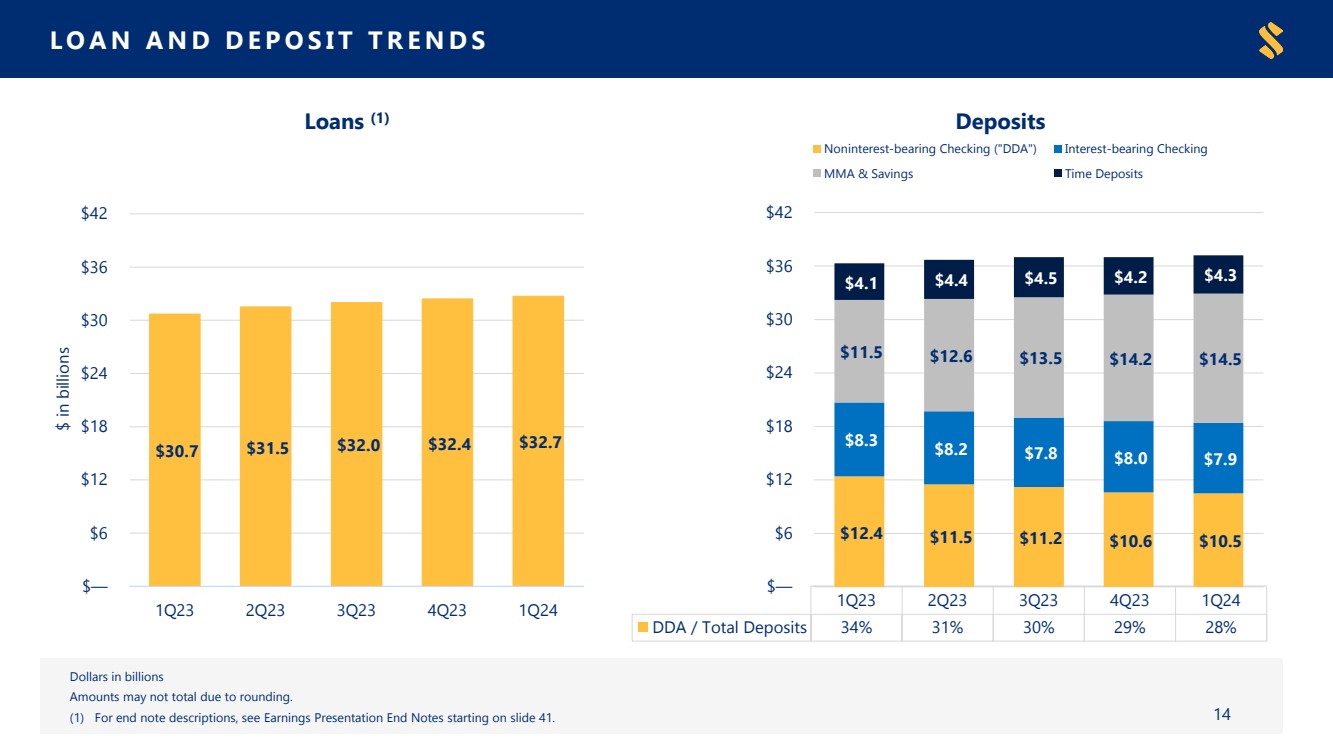

| ● | Loans increased $279 million, or 3% annualized, led by consumer real estate; ending loan to deposit ratio of 88% |

| ● | Deposits increased $130 million, or 1% annualized |

| ● | Total deposit cost of 1.74%, up 0.14% from prior quarter, resulting in a 33% cycle-to-date beta |

| ● | Repurchased a total of 100,000 shares during 1Q 2024 at a weighted average price of $79.85 |

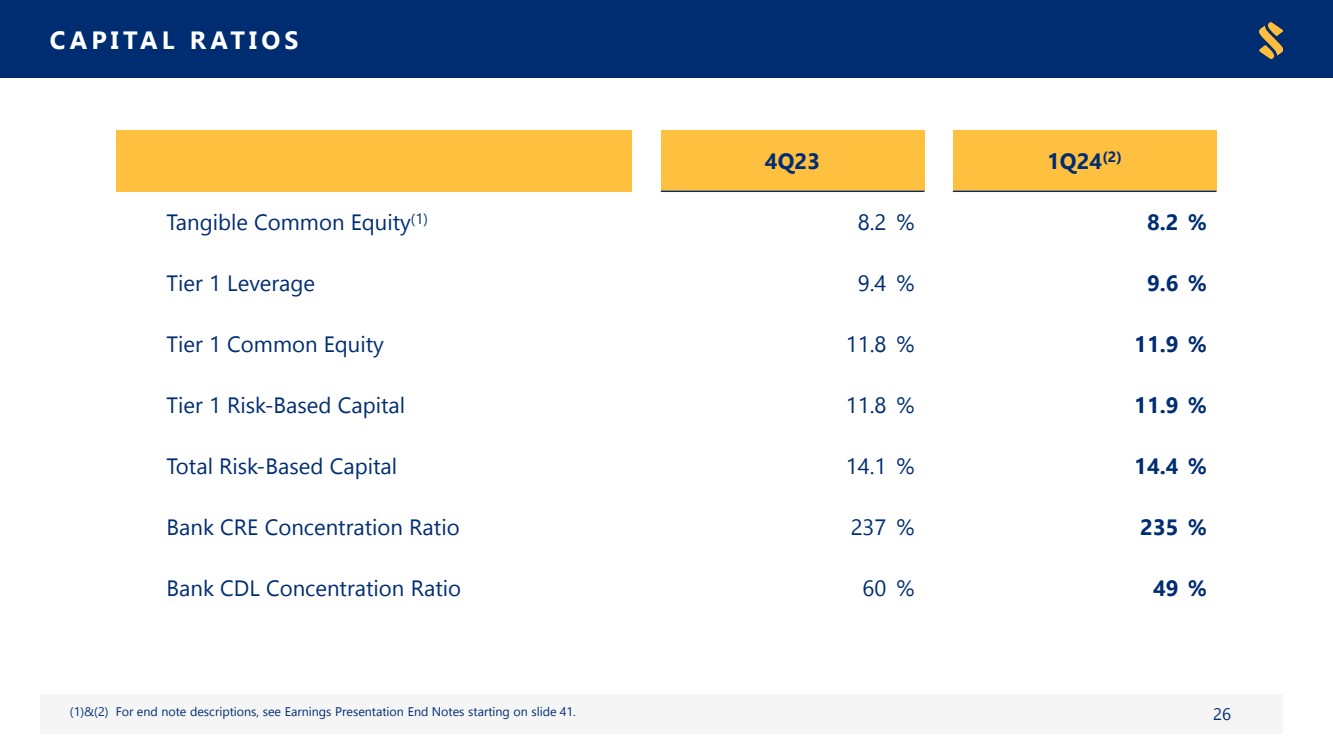

| ● | Strong capital position with Tangible Common Equity, Total Risk-Based Capital, Tier 1 Leverage, and Tier 1 Common Equity ratios of 8.2%, 14.4%, 9.6%, and 11.9%, respectively† |

Subsequent Events

| ● | The Board of Directors of the Company declared a quarterly cash dividend on its common stock of $0.52 per share, payable on May 17, 2024 to shareholders of record as of May 10, 2024 |

∗ Annualized percentages

† Preliminary

Financial Performance

| | Three Months Ended | | |||||||||||||

(Dollars in thousands, except per share data) | | Mar. 31, | | Dec. 31, | | Sep. 30, | | Jun. 30, | | Mar. 31, | | |||||

INCOME STATEMENT | | 2024 | | 2023 | | 2023 | | 2023 | | 2023 | | |||||

Interest Income | | | | | | | | | | | | | | | | |

Loans, including fees (1) | | $ | 463,688 | | $ | 459,880 | | $ | 443,805 | | $ | 419,355 | | $ | 393,366 | |

Investment securities, trading securities, federal funds sold and securities | | | | | | | | | | | | | | | | |

purchased under agreements to resell | | | 53,567 | | | 55,555 | | | 56,704 | | | 58,698 | | | 57,043 | |

Total interest income | | | 517,255 | | | 515,435 | | | 500,509 | | | 478,053 | | | 450,409 | |

Interest Expense | | | | | | | | | | | | | | | | |

Deposits | | | 160,162 | | | 149,584 | | | 133,944 | | | 100,787 | | | 55,942 | |

Federal funds purchased, securities sold under agreements | | | | | | | | | | | | | | | | |

to repurchase, and other borrowings | | | 13,157 | | | 11,620 | | | 11,194 | | | 15,523 | | | 13,204 | |

Total interest expense | | | 173,319 | | | 161,204 | | | 145,138 | | | 116,310 | | | 69,146 | |

Net Interest Income | | | 343,936 | | | 354,231 | | | 355,371 | | | 361,743 | | | 381,263 | |

Provision for credit losses | | | 12,686 | | | 9,893 | | | 32,709 | | | 38,389 | | | 33,091 | |

Net Interest Income after Provision for Credit Losses | | | 331,250 | | | 344,338 | | | 322,662 | | | 323,354 | | | 348,172 | |

Noninterest Income | | | 71,558 | | | 65,489 | | | 72,848 | | | 77,214 | | | 71,355 | |

Noninterest Expense | | | | | | | | | | | | | | | | |

Operating expense | | | 240,923 | | | 245,774 | | | 238,042 | | | 240,818 | | | 231,093 | |

Merger, branch consolidation, severance related and other expense (8) | | | 4,513 | | | 1,778 | | | 164 | | | 1,808 | | | 9,412 | |

FDIC special assessment | | | 3,854 | | | 25,691 | | | — | | | — | | | — | |

Total noninterest expense | | | 249,290 | | | 273,243 | | | 238,206 | | | 242,626 | | | 240,505 | |

Income before Income Taxes Provision | | | 153,518 | | | 136,584 | | | 157,304 | | | 157,942 | | | 179,022 | |

Income taxes provision | | | 38,462 | | | 29,793 | | | 33,160 | | | 34,495 | | | 39,096 | |

Net Income | | $ | 115,056 | | $ | 106,791 | | $ | 124,144 | | $ | 123,447 | | $ | 139,926 | |

| | | | | | | | | | | | | | | | |

Adjusted Net Income (non-GAAP) (2) | | | | | | | | | | | | | | | | |

Net Income (GAAP) | | $ | 115,056 | | $ | 106,791 | | $ | 124,144 | | $ | 123,447 | | $ | 139,926 | |

Securities losses (gains), net of tax | | | — | | | 2 | | | — | | | — | | | (35) | |

Merger, branch consolidation, severance related and other expense, net of tax (8) | | | 3,382 | | | 1,391 | | | 130 | | | 1,414 | | | 7,356 | |

FDIC special assessment, net of tax | | | 2,888 | | | 20,087 | | | — | | | — | | | — | |

Adjusted Net Income (non-GAAP) | | $ | 121,326 | | $ | 128,271 | | $ | 124,274 | | $ | 124,861 | | $ | 147,247 | |

| | | | | | | | | | | | | | | | |

Basic earnings per common share | | $ | 1.51 | | $ | 1.40 | | $ | 1.63 | | $ | 1.62 | | $ | 1.84 | |

Diluted earnings per common share | | $ | 1.50 | | $ | 1.39 | | $ | 1.62 | | $ | 1.62 | | $ | 1.83 | |

Adjusted net income per common share - Basic (non-GAAP) (2) | | $ | 1.59 | | $ | 1.69 | | $ | 1.63 | | $ | 1.64 | | $ | 1.94 | |

Adjusted net income per common share - Diluted (non-GAAP) (2) | | $ | 1.58 | | $ | 1.67 | | $ | 1.62 | | $ | 1.63 | | $ | 1.93 | |

Dividends per common share | | $ | 0.52 | | $ | 0.52 | | $ | 0.52 | | $ | 0.50 | | $ | 0.50 | |

Basic weighted-average common shares outstanding | | | 76,301,411 | | | 76,100,187 | | | 76,139,170 | | | 76,057,977 | | | 75,902,440 | |

Diluted weighted-average common shares outstanding | | | 76,660,081 | | | 76,634,100 | | | 76,571,430 | | | 76,417,537 | | | 76,388,954 | |

Effective tax rate | | | 25.05% | | | 21.81% | | | 21.08% | | | 21.84% | | | 21.84% | |

2

Performance and Capital Ratios

| | Three Months Ended | | | |||||||||||||

| | Mar. 31, | | Dec. 31, | | Sep. 30, | | Jun. 30, | | Mar. 31, | | | |||||

| | 2024 | | 2023 | | 2023 | | 2023 | | 2023 | | | |||||

PERFORMANCE RATIOS | | | | | | | | | | | | | | | | | |

Return on average assets (annualized) | | | 1.03 | % | | 0.94 | % | | 1.10 | % | | 1.11 | % | | 1.29 | % | |

Adjusted return on average assets (annualized) (non-GAAP) (2) | | | 1.08 | % | | 1.13 | % | | 1.10 | % | | 1.12 | % | | 1.35 | % | |

Return on average common equity (annualized) | | | 8.36 | % | | 7.99 | % | | 9.24 | % | | 9.34 | % | | 10.96 | % | |

Adjusted return on average common equity (annualized) (non-GAAP) (2) | | | 8.81 | % | | 9.60 | % | | 9.25 | % | | 9.45 | % | | 11.53 | % | |

Return on average tangible common equity (annualized) (non-GAAP) (3) | | | 13.63 | % | | 13.53 | % | | 15.52 | % | | 15.81 | % | | 18.81 | % | |

Adjusted return on average tangible common equity (annualized) (non-GAAP) (2) (3) | | | 14.35 | % | | 16.12 | % | | 15.54 | % | | 15.98 | % | | 19.75 | % | |

Efficiency ratio (tax equivalent) | | | 58.48 | % | | 63.43 | % | | 54.00 | % | | 53.59 | % | | 51.41 | % | |

Adjusted efficiency ratio (non-GAAP) (4) | | | 56.47 | % | | 56.89 | % | | 53.96 | % | | 53.18 | % | | 49.34 | % | |

Dividend payout ratio (5) | | | 34.42 | % | | 37.01 | % | | 31.84 | % | | 30.75 | % | | 27.09 | % | |

Book value per common share | | $ | 72.82 | | $ | 72.78 | | $ | 68.81 | | $ | 69.61 | | $ | 69.19 | | |

Tangible book value per common share (non-GAAP) (3) | | $ | 46.48 | | $ | 46.32 | | $ | 42.26 | | $ | 42.96 | | $ | 42.40 | | |

| | | | | | | | | | | | | | | | | |

CAPITAL RATIOS | | | | | | | | | | | | | | | | | |

Equity-to-assets | | | 12.3 | % | | 12.3 | % | | 11.6 | % | | 11.8 | % | | 11.7 | % | |

Tangible equity-to-tangible assets (non-GAAP) (3) | | | 8.2 | % | | 8.2 | % | | 7.5 | % | | 7.6 | % | | 7.5 | % | |

Tier 1 leverage (6) | | | 9.6 | % | | 9.4 | % | | 9.3 | % | | 9.2 | % | | 9.1 | % | |

Tier 1 common equity (6) | | | 11.9 | % | | 11.8 | % | | 11.5 | % | | 11.3 | % | | 11.1 | % | |

Tier 1 risk-based capital (6) | | | 11.9 | % | | 11.8 | % | | 11.5 | % | | 11.3 | % | | 11.1 | % | |

Total risk-based capital (6) | | | 14.4 | % | | 14.1 | % | | 13.8 | % | | 13.5 | % | | 13.3 | % | |

3

Balance Sheet

| | Ending Balance | | |||||||||||||

(Dollars in thousands, except per share and share data) | | Mar. 31, | | Dec. 31, | | Sep. 30, | | Jun. 30, | | Mar. 31, | | |||||

BALANCE SHEET | | 2024 | | 2023 | | 2023 | | 2023 | | 2023 | | |||||

Assets | | | | | | | | | | | | | | | | |

Cash and due from banks | | $ | 478,271 | | $ | 510,922 | | $ | 514,917 | | $ | 552,900 | | $ | 558,158 | |

Federal funds sold and interest-earning deposits with banks | | | 731,186 | | | 487,955 | | | 814,220 | | | 960,849 | | | 1,438,504 | |

Cash and cash equivalents | | | 1,209,457 | | | 998,877 | | | 1,329,137 | | | 1,513,749 | | | 1,996,662 | |

| | | | | | | | | | | | | | | | |

Trading securities, at fair value | | | 66,188 | | | 31,321 | | | 114,154 | | | 56,580 | | | 16,039 | |

Investment securities: | | | | | | | | | | | | | | | | |

Securities held to maturity | | | 2,446,589 | | | 2,487,440 | | | 2,533,713 | | | 2,585,155 | | | 2,636,673 | |

Securities available for sale, at fair value | | | 4,598,400 | | | 4,784,388 | | | 4,623,618 | | | 4,949,334 | | | 5,159,999 | |

Other investments | | | 187,285 | | | 192,043 | | | 187,152 | | | 196,728 | | | 217,991 | |

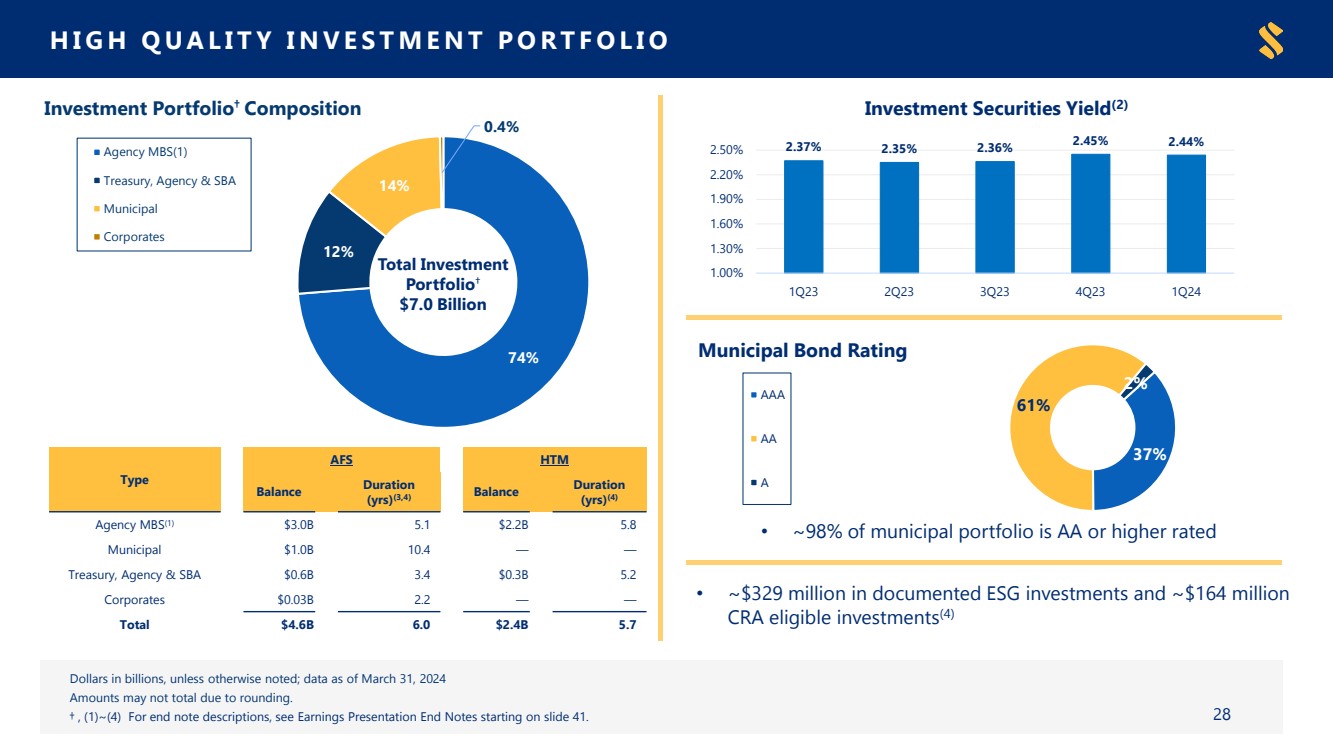

Total investment securities | | | 7,232,274 | | | 7,463,871 | | | 7,344,483 | | | 7,731,217 | | | 8,014,663 | |

Loans held for sale | | | 56,553 | | | 50,888 | | | 27,443 | | | 42,951 | | | 27,289 | |

Loans: | | | | | | | | | | | | | | | | |

Purchased credit deteriorated | | | 1,031,283 | | | 1,108,813 | | | 1,171,543 | | | 1,269,983 | | | 1,325,400 | |

Purchased non-credit deteriorated | | | 4,534,583 | | | 4,796,913 | | | 5,064,254 | | | 5,275,913 | | | 5,620,290 | |

Non-acquired | | | 27,101,444 | | | 26,482,763 | | | 25,780,875 | | | 24,990,889 | | | 23,750,452 | |

Less allowance for credit losses | | | (469,654) | | | (456,573) | | | (447,956) | | | (427,392) | | | (370,645) | |

Loans, net | | | 32,197,656 | | | 31,931,916 | | | 31,568,716 | | | 31,109,393 | | | 30,325,497 | |

Premises and equipment, net | | | 512,635 | | | 519,197 | | | 516,583 | | | 518,353 | | | 517,146 | |

Bank owned life insurance | | | 997,562 | | | 991,454 | | | 984,881 | | | 979,494 | | | 967,750 | |

Mortgage servicing rights | | | 87,970 | | | 85,164 | | | 89,476 | | | 87,539 | | | 85,406 | |

Core deposit and other intangibles | | | 83,193 | | | 88,776 | | | 95,094 | | | 102,256 | | | 109,603 | |

Goodwill | | | 1,923,106 | | | 1,923,106 | | | 1,923,106 | | | 1,923,106 | | | 1,923,106 | |

Other assets | | | 778,244 | | | 817,454 | | | 996,055 | | | 875,694 | | | 940,666 | |

Total assets | | $ | 45,144,838 | | $ | 44,902,024 | | $ | 44,989,128 | | $ | 44,940,332 | | $ | 44,923,827 | |

| | | | | | | | | | | | | | | | |

Liabilities and Shareholders' Equity | | | | | | | | | | | | | | | | |

Deposits: | | | | | | | | | | | | | | | | |

Noninterest-bearing | | $ | 10,546,410 | | $ | 10,649,274 | | $ | 11,158,431 | | $ | 11,489,483 | | $ | 12,422,583 | |

Interest-bearing | | | 26,632,024 | | | 26,399,635 | | | 25,776,767 | | | 25,252,395 | | | 23,979,009 | |

Total deposits | | | 37,178,434 | | | 37,048,909 | | | 36,935,198 | | | 36,741,878 | | | 36,401,592 | |

Federal funds purchased and securities | | | | | | | | | | | | | | | | |

sold under agreements to repurchase | | | 554,691 | | | 489,185 | | | 513,304 | | | 581,446 | | | 544,108 | |

Other borrowings | | | 391,812 | | | 491,904 | | | 391,997 | | | 792,090 | | | 1,292,182 | |

Reserve for unfunded commitments | | | 53,229 | | | 56,303 | | | 62,347 | | | 63,399 | | | 85,068 | |

Other liabilities | | | 1,419,663 | | | 1,282,625 | | | 1,855,295 | | | 1,471,509 | | | 1,351,873 | |

Total liabilities | | | 39,597,829 | | | 39,368,926 | | | 39,758,141 | | | 39,650,322 | | | 39,674,823 | |

| | | | | | | | | | | | | | | | |

Shareholders' equity: | | | | | | | | | | | | | | | | |

Common stock - $2.50 par value; authorized 160,000,000 shares | | | 190,443 | | | 190,055 | | | 190,043 | | | 189,990 | | | 189,649 | |

Surplus | | | 4,230,345 | | | 4,240,413 | | | 4,238,753 | | | 4,228,910 | | | 4,224,503 | |

Retained earnings | | | 1,749,215 | | | 1,685,166 | | | 1,618,080 | | | 1,533,508 | | | 1,448,636 | |

Accumulated other comprehensive loss | | | (622,994) | | | (582,536) | | | (815,889) | | | (662,398) | | | (613,784) | |

Total shareholders' equity | | | 5,547,009 | | | 5,533,098 | | | 5,230,987 | | | 5,290,010 | | | 5,249,004 | |

Total liabilities and shareholders' equity | | $ | 45,144,838 | | $ | 44,902,024 | | $ | 44,989,128 | | $ | 44,940,332 | | $ | 44,923,827 | |

| | | | | | | | | | | | | | | | |

Common shares issued and outstanding | | | 76,177,163 | | | 76,022,039 | | | 76,017,366 | | | 75,995,979 | | | 75,859,665 | |

4

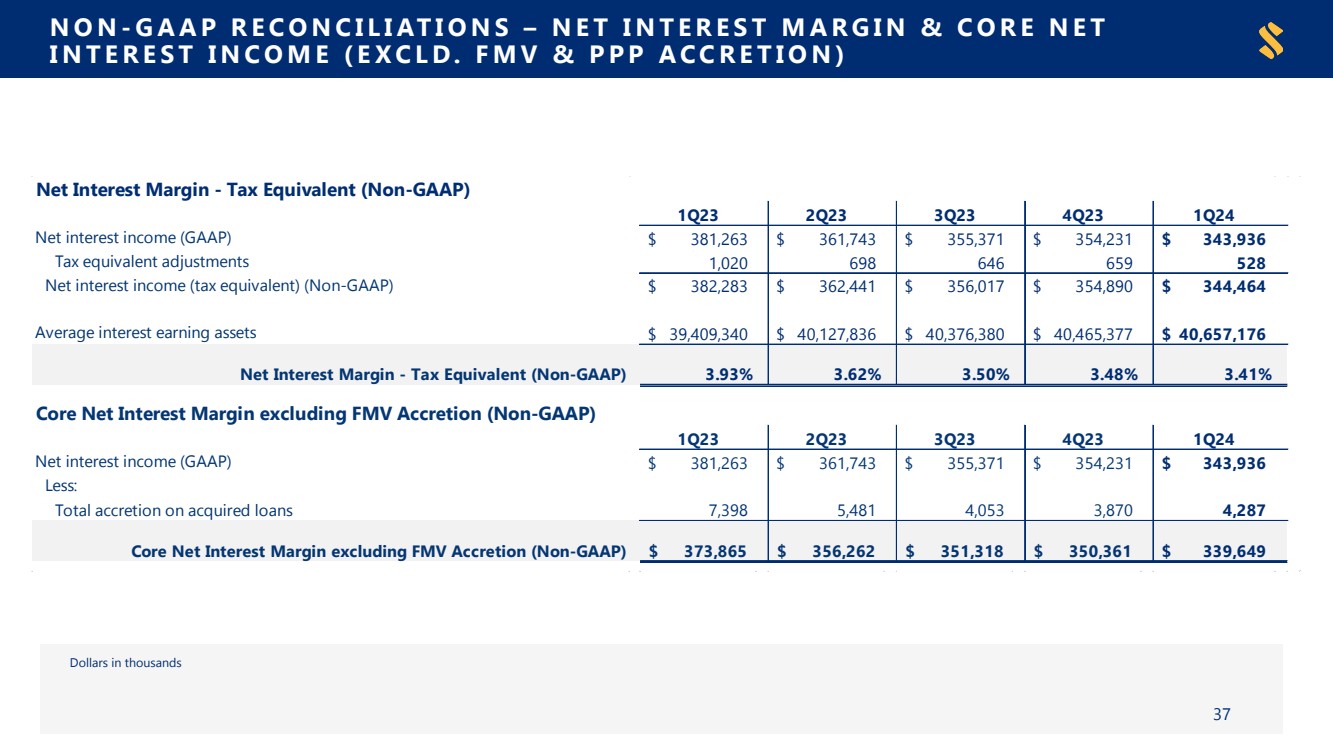

Net Interest Income and Margin

| | Three Months Ended | | ||||||||||||||||||||||

| | Mar. 31, 2024 | | Dec. 31, 2023 | | Mar. 31, 2023 | | ||||||||||||||||||

(Dollars in thousands) | | Average | | Income/ | | Yield/ | | Average | | Income/ | | Yield/ | | Average | | Income/ | | Yield/ | | ||||||

YIELD ANALYSIS | | Balance | | Expense | | Rate | | Balance | | Expense | | Rate | | Balance | | Expense | | Rate | | ||||||

Interest-Earning Assets: | | | | | | | | | | | | | | | | | | | | | | | | | |

Federal funds sold and interest-earning deposits with banks | | $ | 668,349 | | $ | 8,254 | | 4.97% | | $ | 814,244 | | $ | 10,029 | | 4.89% | | $ | 759,239 | | $ | 8,921 | | 4.77% | |

Investment securities | | | 7,465,735 | | | 45,313 | | 2.44% | | | 7,382,800 | | | 45,526 | | 2.45% | | | 8,232,582 | | | 48,122 | | 2.37% | |

Loans held for sale | | | 42,872 | | | 681 | | 6.39% | | | 28,878 | | | 552 | | 7.58% | | | 23,123 | | | 402 | | 7.05% | |

Total loans held for investment | | | 32,480,220 | | | 463,007 | | 5.73% | | | 32,239,455 | | | 459,328 | | 5.65% | | | 30,394,396 | | | 392,964 | | 5.24% | |

Total interest-earning assets | | | 40,657,176 | | | 517,255 | | 5.12% | | | 40,465,377 | | | 515,435 | | 5.05% | | | 39,409,340 | | | 450,409 | | 4.64% | |

Noninterest-earning assets | | | 4,353,987 | | | | | | | | 4,572,255 | | | | | | | | 4,695,138 | | | | | | |

Total Assets | | $ | 45,011,163 | | | | | | | $ | 45,037,632 | | | | | | | $ | 44,104,478 | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Interest-Bearing Liabilities ("IBL"): | | | | | | | | | | | | | | | | | | | | | | | | | |

Transaction and money market accounts | | $ | 19,544,019 | | $ | 117,292 | | 2.41% | | $ | 18,957,647 | | $ | 107,994 | | 2.26% | | $ | 16,874,909 | | $ | 40,516 | | 0.97% | |

Savings deposits | | | 2,589,251 | | | 1,818 | | 0.28% | | | 2,680,065 | | | 1,888 | | 0.28% | | | 3,298,221 | | | 1,756 | | 0.22% | |

Certificates and other time deposits | | | 4,282,749 | | | 41,052 | | 3.86% | | | 4,294,555 | | | 39,702 | | 3.67% | | | 3,114,354 | | | 13,670 | | 1.78% | |

Federal funds purchased | | | 256,506 | | | 3,369 | | 5.28% | | | 256,672 | | | 3,453 | | 5.34% | | | 193,259 | | | 2,187 | | 4.59% | |

Repurchase agreements | | | 280,674 | | | 1,358 | | 1.95% | | | 265,839 | | | 1,458 | | 2.18% | | | 373,563 | | | 666 | | 0.72% | |

Other borrowings | | | 563,848 | | | 8,430 | | 6.01% | | | 438,701 | | | 6,709 | | 6.07% | | | 785,571 | | | 10,351 | | 5.34% | |

Total interest-bearing liabilities | | | 27,517,047 | | | 173,319 | | 2.53% | | | 26,893,479 | | | 161,204 | | 2.38% | | | 24,639,877 | | | 69,146 | | 1.14% | |

Noninterest-bearing liabilities ("Non-IBL") | | | 11,957,565 | | | | | | | | 12,844,262 | | | | | | | | 14,287,553 | | | | | | |

Shareholders' equity | | | 5,536,551 | | | | | | | | 5,299,891 | | | | | | | | 5,177,048 | | | | | | |

Total Non-IBL and shareholders' equity | | | 17,494,116 | | | | | | | | 18,144,153 | | | | | | | | 19,464,601 | | | | | | |

Total Liabilities and Shareholders' Equity | | $ | 45,011,163 | | | | | | | $ | 45,037,632 | | | | | | | $ | 44,104,478 | | | | | | |

Net Interest Income and Margin (Non-Tax Equivalent) | | | | | $ | 343,936 | | 3.40% | | | | | $ | 354,231 | | 3.47% | | | | | $ | 381,263 | | 3.92% | |

Net Interest Margin (Tax Equivalent) (non-GAAP) | | | | | | | | 3.41% | | | | | | | | 3.48% | | | | | | | | 3.93% | |

Total Deposit Cost (without Debt and Other Borrowings) | | | | | | | | 1.74% | | | | | | | | 1.60% | | | | | | | | 0.63% | |

Overall Cost of Funds (including Demand Deposits) | | | | | | | | 1.83% | | | | | | | | 1.69% | | | | | | | | 0.75% | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Total Accretion on Acquired Loans (1) | | | | | $ | 4,287 | | | | | | | $ | 3,870 | | | | | | | $ | 7,398 | | | |

Tax Equivalent ("TE") Adjustment | | | | | $ | 528 | | | | | | | $ | 659 | | | | | | | $ | 1,020 | | | |

| ● | The remaining loan discount on acquired loans to be accreted into loan interest income totals $47.0 million as of March 31, 2024. |

5

Noninterest Income and Expense

| | Three Months Ended | | |||||||||||||

| | Mar. 31, | | Dec. 31, | | Sep. 30, | | Jun. 30, | | Mar. 31, | | |||||

(Dollars in thousands) | | 2024 | | 2023 | | 2023 | | 2023 | | 2023 | | |||||

Noninterest Income: | | | | | | | | | | | | | | | | |

Fees on deposit accounts | | $ | 33,145 | | $ | 33,225 | | $ | 32,830 | | $ | 33,101 | | $ | 29,859 | |

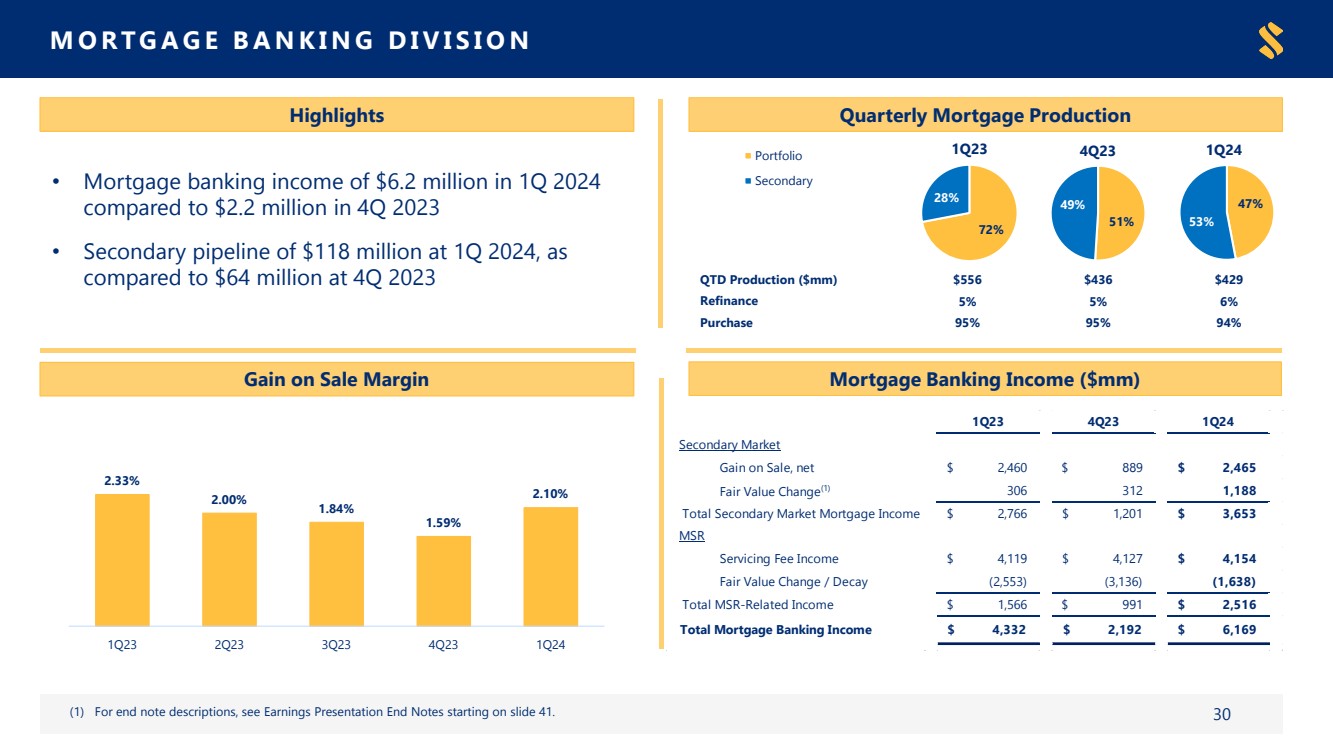

Mortgage banking income | | | 6,169 | | | 2,191 | | | 2,478 | | | 4,354 | | | 4,332 | |

Trust and investment services income | | | 10,391 | | | 10,131 | | | 9,556 | | | 9,823 | | | 9,937 | |

Securities (losses) gains, net | | | — | | | (2) | | | — | | | — | | | 45 | |

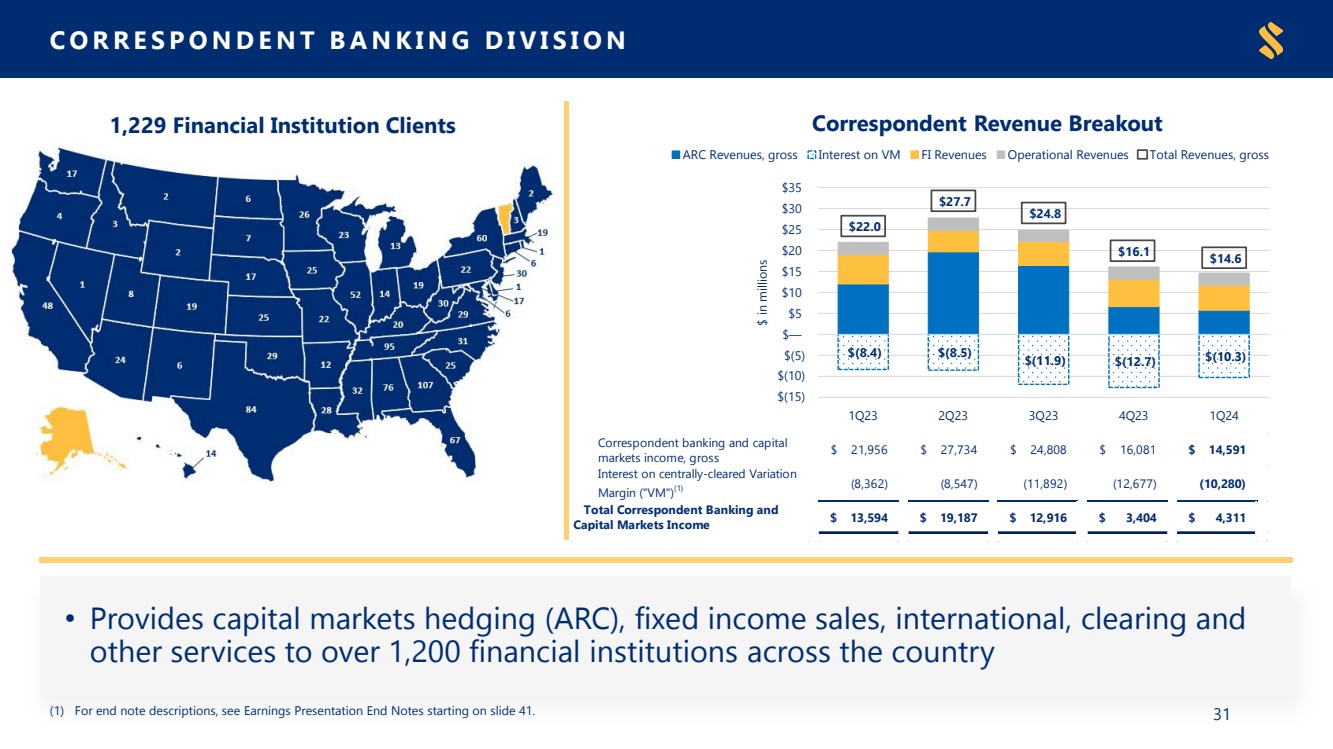

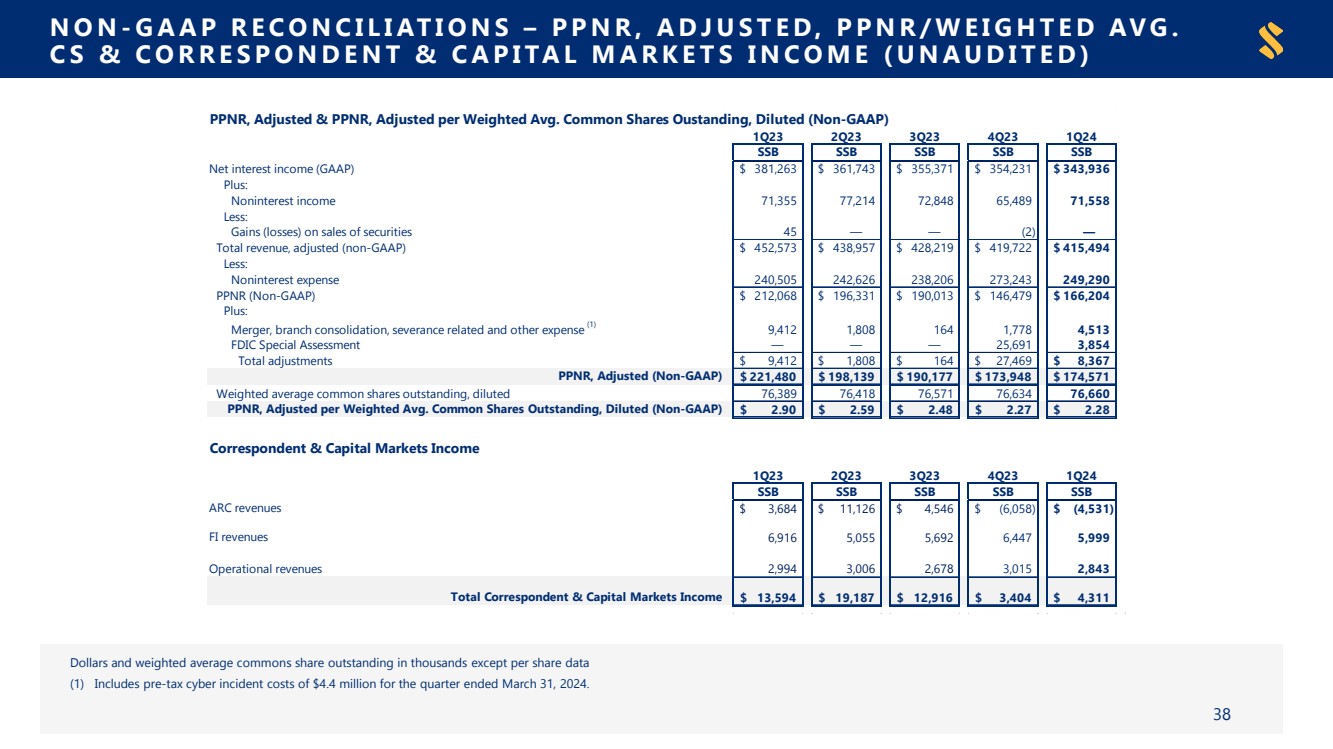

Correspondent banking and capital markets income | | | 14,591 | | | 16,081 | | | 24,808 | | | 27,734 | | | 21,956 | |

Expense on centrally-cleared variation margin | | | (10,280) | | | (12,677) | | | (11,892) | | | (8,547) | | | (8,362) | |

Total correspondent banking and capital markets income | | | 4,311 | | | 3,404 | | | 12,916 | | | 19,187 | | | 13,594 | |

Bank owned life insurance income | | | 6,892 | | | 6,567 | | | 7,039 | | | 6,271 | | | 6,813 | |

Other | | | 10,650 | | | 9,973 | | | 8,029 | | | 4,478 | | | 6,775 | |

Total Noninterest Income | | $ | 71,558 | | $ | 65,489 | | $ | 72,848 | | $ | 77,214 | | $ | 71,355 | |

| | | | | | | | | | | | | | | | |

Noninterest Expense: | | | | | | | | | | | | | | | | |

Salaries and employee benefits | | $ | 150,453 | | $ | 145,850 | | $ | 146,146 | | $ | 147,342 | | $ | 144,060 | |

Occupancy expense | | | 22,577 | | | 22,715 | | | 22,251 | | | 22,196 | | | 21,533 | |

Information services expense | | | 22,353 | | | 22,000 | | | 21,428 | | | 21,119 | | | 19,925 | |

OREO and loan related expense (income) | | | 606 | | | 948 | | | 613 | | | (14) | | | 169 | |

Business development and staff related | | | 5,799 | | | 7,492 | | | 5,995 | | | 6,672 | | | 5,957 | |

Amortization of intangibles | | | 5,998 | | | 6,615 | | | 6,616 | | | 7,028 | | | 7,299 | |

Professional fees | | | 3,115 | | | 7,025 | | | 3,456 | | | 4,364 | | | 3,702 | |

Supplies and printing expense | | | 2,540 | | | 2,761 | | | 2,623 | | | 2,554 | | | 2,640 | |

FDIC assessment and other regulatory charges | | | 8,534 | | | 8,325 | | | 8,632 | | | 9,819 | | | 6,294 | |

Advertising and marketing | | | 1,984 | | | 2,826 | | | 3,009 | | | 1,521 | | | 2,118 | |

Other operating expenses | | | 16,964 | | | 19,217 | | | 17,273 | | | 18,217 | | | 17,396 | |

Merger, branch consolidation, severance related and other expense (8) | | | 4,513 | | | 1,778 | | | 164 | | | 1,808 | | | 9,412 | |

FDIC special assessment | | | 3,854 | | | 25,691 | | | — | | | — | | | — | |

Total Noninterest Expense | | $ | 249,290 | | $ | 273,243 | | $ | 238,206 | | $ | 242,626 | | $ | 240,505 | |

6

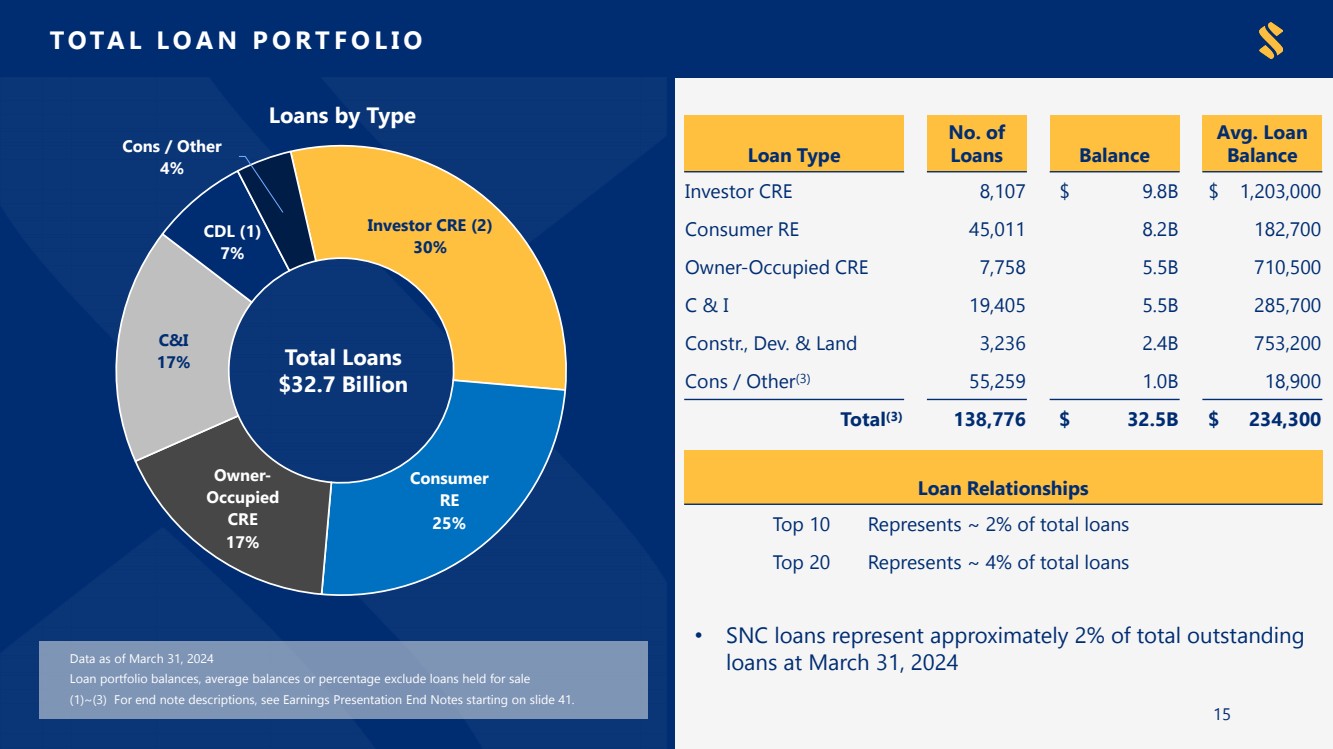

Loans and Deposits

The following table presents a summary of the loan portfolio by type:

| | Ending Balance | | |||||||||||||

(Dollars in thousands) | | Mar. 31, | | Dec. 31, | | Sep. 30, | | Jun. 30, | | Mar. 31, | | |||||

LOAN PORTFOLIO (7) | | 2024 | | 2023 | | 2023 | | 2023 | | 2023 | | |||||

Construction and land development * † | | $ | 2,437,343 | | $ | 2,923,514 | | $ | 2,776,241 | | $ | 2,817,125 | | $ | 2,749,290 | |

Investor commercial real estate* | | | 9,752,529 | | | 9,227,968 | | | 9,372,683 | | | 9,187,948 | | | 8,957,507 | |

Commercial owner occupied real estate | | | 5,511,855 | | | 5,497,671 | | | 5,539,097 | | | 5,585,951 | | | 5,522,514 | |

Commercial and industrial | | | 5,544,131 | | | 5,504,539 | | | 5,458,229 | | | 5,378,294 | | | 5,321,306 | |

Consumer real estate * | | | 8,223,066 | | | 7,993,450 | | | 7,608,145 | | | 7,275,495 | | | 6,860,831 | |

Consumer/other | | | 1,198,386 | | | 1,241,347 | | | 1,262,277 | | | 1,291,972 | | | 1,284,694 | |

Total Loans | | $ | 32,667,310 | | $ | 32,388,489 | | $ | 32,016,672 | | $ | 31,536,785 | | $ | 30,696,142 | |

* Single family home construction-to-permanent loans originated by the Company’s mortgage banking division are included in construction and land development category until completion. Investor commercial real estate loans include commercial non-owner occupied real estate and other income producing property. Consumer real estate includes consumer owner occupied real estate and home equity loans.

† Includes single family home construction-to-permanent loans of $623.9 million, $715.5 million, $863.1 million, $928.4 million, and $893.7 million for the quarters ended March 31, 2024, December 31, 2023, September 30, 2023, June 30, 2023, and March 31, 2023, respectively.

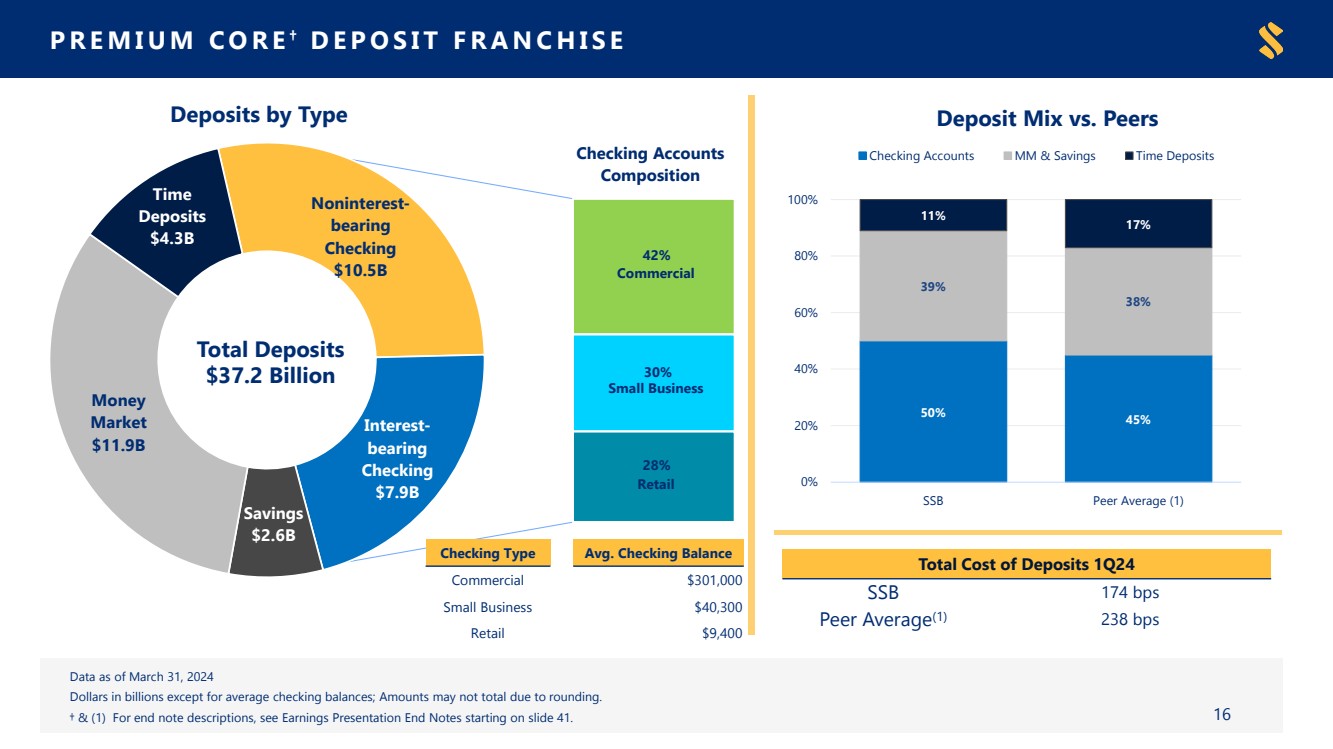

| | Ending Balance | | |||||||||||||

(Dollars in thousands) | | Mar. 31, | | Dec. 31, | | Sep. 30, | | Jun. 30, | | Mar. 31, | | |||||

DEPOSITS | | 2024 | | 2023 | | 2023 | | 2023 | | 2023 | | |||||

Noninterest-bearing checking | | $ | 10,546,410 | | $ | 10,649,274 | | $ | 11,158,431 | | $ | 11,489,483 | | $ | 12,422,583 | |

Interest-bearing checking | | | 7,898,835 | | | 7,978,799 | | | 7,806,243 | | | 8,185,609 | | | 8,316,023 | |

Savings | | | 2,557,203 | | | 2,632,212 | | | 2,760,166 | | | 2,931,320 | | | 3,156,214 | |

Money market | | | 11,895,385 | | | 11,538,671 | | | 10,756,431 | | | 9,710,032 | | | 8,388,275 | |

Time deposits | | | 4,280,601 | | | 4,249,953 | | | 4,453,927 | | | 4,425,434 | | | 4,118,497 | |

Total Deposits | | $ | 37,178,434 | | $ | 37,048,909 | | $ | 36,935,198 | | $ | 36,741,878 | | $ | 36,401,592 | |

| | | | | | | | | | | | | | | | |

Core Deposits (excludes Time Deposits) | | $ | 32,897,833 | | $ | 32,798,956 | | $ | 32,481,271 | | $ | 32,316,444 | | $ | 32,283,095 | |

7

Asset Quality

| | Ending Balance | | |||||||||||||

| | Mar. 31, | | Dec. 31, | | Sep. 30, | | Jun. 30, | | Mar. 31, | | |||||

(Dollars in thousands) | | 2024 | | 2023 | | 2023 | | 2023 | | 2023 | | |||||

NONPERFORMING ASSETS: | | | | | | | | | | | | | | | | |

Non-acquired | | | | | | | | | | | | | | | | |

Non-acquired nonaccrual loans and restructured loans on nonaccrual | | $ | 106,189 | | $ | 110,467 | | $ | 105,856 | | $ | 104,772 | | $ | 68,176 | |

Accruing loans past due 90 days or more | | | 2,497 | | | 11,305 | | | 783 | | | 3,620 | | | 2,667 | |

Non-acquired OREO and other nonperforming assets | | | 1,589 | | | 711 | | | 449 | | | 227 | | | 186 | |

Total non-acquired nonperforming assets | | | 110,275 | | | 122,483 | | | 107,088 | | | 108,619 | | | 71,029 | |

Acquired | | | | | | | | | | | | | | | | |

Acquired nonaccrual loans and restructured loans on nonaccrual | | | 63,451 | | | 59,755 | | | 57,464 | | | 60,734 | | | 52,795 | |

Accruing loans past due 90 days or more | | | 135 | | | 1,174 | | | 1,821 | | | 571 | | | 983 | |

Acquired OREO and other nonperforming assets | | | 655 | | | 712 | | | 378 | | | 981 | | | 3,446 | |

Total acquired nonperforming assets | | | 64,241 | | | 61,641 | | | 59,663 | | | 62,286 | | | 57,224 | |

Total nonperforming assets | | $ | 174,516 | | $ | 184,124 | | $ | 166,751 | | $ | 170,905 | | $ | 128,253 | |

| | Three Months Ended | | |||||||||||||

| | Mar. 31, | | Dec. 31, | | Sep. 30, | | Jun. 30, | | Mar. 31, | | |||||

| | 2024 | | 2023 | | 2023 | | 2023 | | 2023 | | |||||

ASSET QUALITY RATIOS (7): | | | | | | | | | | | | | | | | |

Allowance for credit losses as a percentage of loans | | | 1.44% | | | 1.41% | | | 1.40% | | | 1.36% | | | 1.21% | |

Allowance for credit losses, including reserve for unfunded commitments, as a percentage of loans | | | 1.60% | | | 1.58% | | | 1.59% | | | 1.56% | | | 1.48% | |

Allowance for credit losses as a percentage of nonperforming loans | | | 272.62% | | | 249.90% | | | 269.98% | | | 251.86% | | | 297.42% | |

Net charge-offs as a percentage of average loans (annualized) | | | 0.03% | | | 0.09% | | | 0.16% | | | 0.04% | | | 0.01% | |

Total nonperforming assets as a percentage of total assets | | | 0.39% | | | 0.41% | | | 0.37% | | | 0.38% | | | 0.29% | |

Nonperforming loans as a percentage of period end loans | | | 0.53% | | | 0.56% | | | 0.52% | | | 0.54% | | | 0.41% | |

Current Expected Credit Losses (“CECL”)

Below is a table showing the roll forward of the ACL and UFC for the first quarter of 2024:

| | Allowance for Credit Losses ("ACL and UFC") | | ||||||||||

(Dollars in thousands) | | NonPCD ACL | | PCD ACL | | Total ACL | | UFC | | ||||

Ending balance 12/31/2023 | | $ | 423,876 | | $ | 32,697 | | $ | 456,573 | | $ | 56,303 | |

Charge offs | | | (4,829) | | | — | | | (4,829) | | | — | |

Acquired charge offs | | | (2,889) | | | (222) | | | (3,111) | | | — | |

Recoveries | | | 2,703 | | | — | | | 2,703 | | | — | |

Acquired recoveries | | | 272 | | | 2,286 | | | 2,558 | | | — | |

Provision (recovery) for credit losses | | | 20,055 | | | (4,295) | | | 15,760 | | | (3,074) | |

Ending balance 3/31/2024 | | $ | 439,188 | | $ | 30,466 | | $ | 469,654 | | $ | 53,229 | |

| | | | | | | | | | | | | |

Period end loans | | $ | 31,636,027 | | $ | 1,031,283 | | $ | 32,667,310 | | | N/A | |

Allowance for Credit Losses to Loans | | | 1.39% | | | 2.95% | | | 1.44% | | | N/A | |

Unfunded commitments (off balance sheet) * | | | | | | | | | | | $ | 8,160,594 | |

Reserve to unfunded commitments (off balance sheet) | | | | | | | | | | | | 0.65% | |

* Unfunded commitments exclude unconditionally cancelable commitments and letters of credit.

Conference Call

The Company will host a conference call to discuss its first quarter results at 9:00 a.m. Eastern Time on April 26, 2024. Callers wishing to participate may call toll-free by dialing (888) 350-3899 within the US and (646) 960-0343 for all other locations. The numbers for international participants are listed at https://events.q4irportal.com/custom/access/2324/. The conference ID number is 4200408. Alternatively, individuals may listen to the live webcast of the presentation by visiting SouthStateBank.com. An audio replay of the live webcast is expected to be available by the evening of April 26, 2024 on the Investor Relations section of SouthStateBank.com.

SouthState Corporation is a financial services company headquartered in Winter Haven, Florida. SouthState Bank, N.A., the Company’s nationally chartered bank subsidiary, provides consumer, commercial, mortgage and wealth management solutions to more than one million customers throughout Florida, Alabama, Georgia, the Carolinas and Virginia. The Bank also serves clients coast to coast through its correspondent banking division. Additional information is available at SouthStateBank.com.

###

8

Non-GAAP Measures

Statements included in this press release include non-GAAP measures and should be read along with the accompanying tables that provide a reconciliation of non-GAAP measures to GAAP measures. Although other companies may use calculation methods that differ from those used by SouthState for non-GAAP measures, management believes that these non-GAAP measures provide additional useful information, which allows readers to evaluate the ongoing performance of the Company. Non-GAAP measures should not be considered as an alternative to any measure of performance or financial condition as promulgated under GAAP, and investors should consider the Company's performance and financial condition as reported under GAAP and all other relevant information when assessing the performance or financial condition of the Company. Non-GAAP measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of the Company's results or financial condition as reported under GAAP.

(Dollars and shares in thousands, except per share data) | | Three Months Ended | | |||||||||||||||||

PRE-PROVISION NET REVENUE ("PPNR") (NON-GAAP) | | Mar. 31, 2024 | | | Dec. 31, 2023 | | | Sep. 30, 2023 | | | Jun. 30, 2023 | | | Mar. 31, 2023 | | |||||

Net income (GAAP) | | $ | 115,056 | | | $ | 106,791 | | | $ | 124,144 | | | $ | 123,447 | | | $ | 139,926 | |

Provision for credit losses | | | 12,686 | | | | 9,893 | | | | 32,709 | | | | 38,389 | | | | 33,091 | |

Tax provision | | | 38,462 | | | | 29,793 | | | | 33,160 | | | | 34,495 | | | | 39,096 | |

Merger, branch consolidation, severance related and other expense (8) | | | 4,513 | | | | 1,778 | | | | 164 | | | | 1,808 | | | | 9,412 | |

FDIC special assessment | | | 3,854 | | | | 25,691 | | | | — | | | | — | | | | — | |

Securities losses (gains) | | | — | | | | 2 | | | | — | | | | — | | | | (45) | |

Pre-provision net revenue (PPNR) (Non-GAAP) | | $ | 174,571 | | | $ | 173,948 | | | $ | 190,177 | | | $ | 198,139 | | | $ | 221,480 | |

| | | | | | | | | | | | | | | | | | | | |

Average asset balance (GAAP) | | $ | 45,011,163 | | | $ | 45,037,632 | | | $ | 44,841,319 | | | $ | 44,628,124 | | | $ | 44,104,478 | |

PPNR ROAA | | | 1.56 | % | | | 1.53 | % | | | 1.68 | % | | | 1.78 | % | | | 2.04 | % |

| | | | | | | | | | | | | | | | | | | | |

Diluted weighted-average common shares outstanding | | | 76,660 | | | | 76,634 | | | | 76,571 | | | | 76,418 | | | | 76,389 | |

PPNR per weighted-average common shares outstanding | | $ | 2.28 | | | $ | 2.27 | | | $ | 2.48 | | | $ | 2.59 | | | $ | 2.90 | |

(Dollars in thousands) | | Three Months Ended | | |||||||||||||||||

CORE NET INTEREST INCOME (NON-GAAP) | | Mar. 31, 2024 | | | Dec. 31, 2023 | | | Sep. 30, 2023 | | | Jun. 30, 2023 | | | Mar. 31, 2023 | | |||||

Net interest income (GAAP) | | $ | 343,936 | | | $ | 354,231 | | | $ | 355,371 | | | $ | 361,743 | | | $ | 381,263 | |

Less: | | | | | | | | | | | | | | | | | | | | |

Total accretion on acquired loans | | | 4,287 | | | | 3,870 | | | | 4,053 | | | | 5,481 | | | | 7,398 | |

Core net interest income (Non-GAAP) | | $ | 339,649 | | | $ | 350,361 | | | $ | 351,318 | | | $ | 356,262 | | | $ | 373,865 | |

| | | | | | | | | | | | | | | | | | | | |

NET INTEREST MARGIN ("NIM"), TE (NON-GAAP) | | | | | | | | | | | | | | | | | | | | |

Net interest income (GAAP) | | $ | 343,936 | | | $ | 354,231 | | | $ | 355,371 | | | $ | 361,743 | | | $ | 381,263 | |

Total average interest-earning assets | | | 40,657,176 | | | | 40,465,377 | | | | 40,376,380 | | | | 40,127,836 | | | | 39,409,340 | |

NIM, non-tax equivalent | | | 3.40 | % | | | 3.47 | % | | | 3.49 | % | | | 3.62 | % | | | 3.92 | % |

| | | | | | | | | | | | | | | | | | | | |

Tax equivalent adjustment (included in NIM, TE) | | | 528 | | | | 659 | | | | 646 | | | | 698 | | | | 1,020 | |

Net interest income, tax equivalent (Non-GAAP) | | $ | 344,464 | | | $ | 354,890 | | | $ | 356,017 | | | $ | 362,441 | | | $ | 382,283 | |

NIM, TE (Non-GAAP) | | | 3.41 | % | | | 3.48 | % | | | 3.50 | % | | | 3.62 | % | | | 3.93 | % |

9

| | Three Months Ended | | |||||||||||||||||

(Dollars in thousands, except per share data) | | Mar. 31, | | | Dec. 31, | | | Sep. 30, | | | Jun. 30, | | | Mar. 31, | | |||||

RECONCILIATION OF GAAP TO NON-GAAP | | 2024 | | | 2023 | | | 2023 | | | 2023 | | | 2023 | | |||||

Adjusted Net Income (non-GAAP) (2) | | | | | | | | | | | | | | | | | | | | |

Net income (GAAP) | | $ | 115,056 | | | $ | 106,791 | | | $ | 124,144 | | | $ | 123,447 | | | $ | 139,926 | |

Securities losses (gains), net of tax | | | — | | | | 2 | | | | — | | | | — | | | | (35) | |

Merger, branch consolidation, severance related and other expense, net of tax (8) | | | 3,382 | | | | 1,391 | | | | 130 | | | | 1,414 | | | | 7,356 | |

FDIC special assessment, net of tax | | | 2,888 | | | | 20,087 | | | | — | | | | — | | | | — | |

Adjusted net income (non-GAAP) | | $ | 121,326 | | | $ | 128,271 | | | $ | 124,274 | | | $ | 124,861 | | | $ | 147,247 | |

| | | | | | | | | | | | | | | | | | | | |

Adjusted Net Income per Common Share - Basic (2) | | | | | | | | | | | | | | | | | | | | |

Earnings per common share - Basic (GAAP) | | $ | 1.51 | | | $ | 1.40 | | | $ | 1.63 | | | $ | 1.62 | | | $ | 1.84 | |

Effect to adjust for securities losses (gains), net of tax | | | — | | | | 0.00 | | | | — | | | | — | | | | (0.00) | |

Effect to adjust for merger, branch consolidation, severance related and other expense, net of tax (8) | | | 0.04 | | | | 0.03 | | | | 0.00 | | | | 0.02 | | | | 0.10 | |

Effect to adjust for FDIC special assessment, net of tax | | | 0.04 | | | | 0.26 | | | | — | | | | — | | | | — | |

Adjusted net income per common share - Basic (non-GAAP) | | $ | 1.59 | | | $ | 1.69 | | | $ | 1.63 | | | $ | 1.64 | | | $ | 1.94 | |

| | | | | | | | | | | | | | | | | | | | |

Adjusted Net Income per Common Share - Diluted (2) | | | | | | | | | | | | | | | | | | | | |

Earnings per common share - Diluted (GAAP) | | $ | 1.50 | | | $ | 1.39 | | | $ | 1.62 | | | $ | 1.62 | | | $ | 1.83 | |

Effect to adjust for securities losses (gains), net of tax | | | — | | | | — | | | | — | | | | — | | | | (0.00) | |

Effect to adjust for merger, branch consolidation, severance related and other expense, net of tax (8) | | | 0.04 | | | | 0.02 | | | | 0.00 | | | | 0.01 | | | | 0.10 | |

Effect to adjust for FDIC special assessment, net of tax | | | 0.04 | | | | 0.26 | | | | — | | | | — | | | | — | |

Adjusted net income per common share - Diluted (non-GAAP) | | $ | 1.58 | | | $ | 1.67 | | | $ | 1.62 | | | $ | 1.63 | | | $ | 1.93 | |

| | | | | | | | | | | | | | | | | | | | |

Adjusted Return on Average Assets (2) | | | | | | | | | | | | | | | | | | | | |

Return on average assets (GAAP) | | | 1.03 | % | | | 0.94 | % | | | 1.10 | % | | | 1.11 | % | | | 1.29 | % |

Effect to adjust for securities losses (gains), net of tax | | | — | % | | | 0.00 | % | | | — | % | | | — | % | | | (0.00) | % |

Effect to adjust for merger, branch consolidation, severance related and other expense, net of tax (8) | | | 0.02 | % | | | 0.01 | % | | | — | % | | | 0.01 | % | | | 0.06 | % |

Effect to adjust for FDIC special assessment, net of tax | | | 0.03 | % | | | 0.18 | % | | | — | % | | | — | % | | | — | % |

Adjusted return on average assets (non-GAAP) | | | 1.08 | % | | | 1.13 | % | | | 1.10 | % | | | 1.12 | % | | | 1.35 | % |

| | | | | | | | | | | | | | | | | | | | |

Adjusted Return on Average Common Equity (2) | | | | | | | | | | | | | | | | | | | | |

Return on average common equity (GAAP) | | | 8.36 | % | | | 7.99 | % | | | 9.24 | % | | | 9.34 | % | | | 10.96 | % |

Effect to adjust for securities losses (gains), net of tax | | | — | % | | | 0.00 | % | | | — | % | | | — | % | | | (0.00) | % |

Effect to adjust for merger, branch consolidation, severance related and other expense, net of tax (8) | | | 0.24 | % | | | 0.11 | % | | | 0.01 | % | | | 0.11 | % | | | 0.57 | % |

Effect to adjust for FDIC special assessment, net of tax | | | 0.21 | % | | | 1.50 | % | | | — | % | | | — | % | | | — | % |

Adjusted return on average common equity (non-GAAP) | | | 8.81 | % | | | 9.60 | % | | | 9.25 | % | | | 9.45 | % | | | 11.53 | % |

| | | | | | | | | | | | | | | | | | | | |

Return on Average Common Tangible Equity (3) | | | | | | | | | | | | | | | | | | | | |

Return on average common equity (GAAP) | | | 8.36 | % | | | 7.99 | % | | | 9.24 | % | | | 9.34 | % | | | 10.96 | % |

Effect to adjust for intangible assets | | | 5.27 | % | | | 5.54 | % | | | 6.28 | % | | | 6.47 | % | | | 7.85 | % |

Return on average tangible equity (non-GAAP) | | | 13.63 | % | | | 13.53 | % | | | 15.52 | % | | | 15.81 | % | | | 18.81 | % |

| | | | | | | | | | | | | | | | | | | | |

Adjusted Return on Average Common Tangible Equity (2) (3) | | | | | | | | | | | | | | | | | | | | |

Return on average common equity (GAAP) | | | 8.36 | % | | | 7.99 | % | | | 9.24 | % | | | 9.34 | % | | | 10.96 | % |

Effect to adjust for securities losses (gains), net of tax | | | — | % | | | 0.00 | % | | | — | % | | | — | % | | | (0.00) | % |

Effect to adjust for merger, branch consolidation, severance related and other expense, net of tax (8) | | | 0.25 | % | | | 0.10 | % | | | 0.01 | % | | | 0.11 | % | | | 0.58 | % |

Effect to adjust for FDIC special assessment, net of tax | | | 0.21 | % | | | 1.50 | % | | | — | % | | | — | % | | | — | % |

Effect to adjust for intangible assets, net of tax | | | 5.53 | % | | | 6.53 | % | | | 6.29 | % | | | 6.53 | % | | | 8.21 | % |

Adjusted return on average common tangible equity (non-GAAP) | | | 14.35 | % | | | 16.12 | % | | | 15.54 | % | | | 15.98 | % | | | 19.75 | % |

| | | | | | | | | | | | | | | | | | | | |

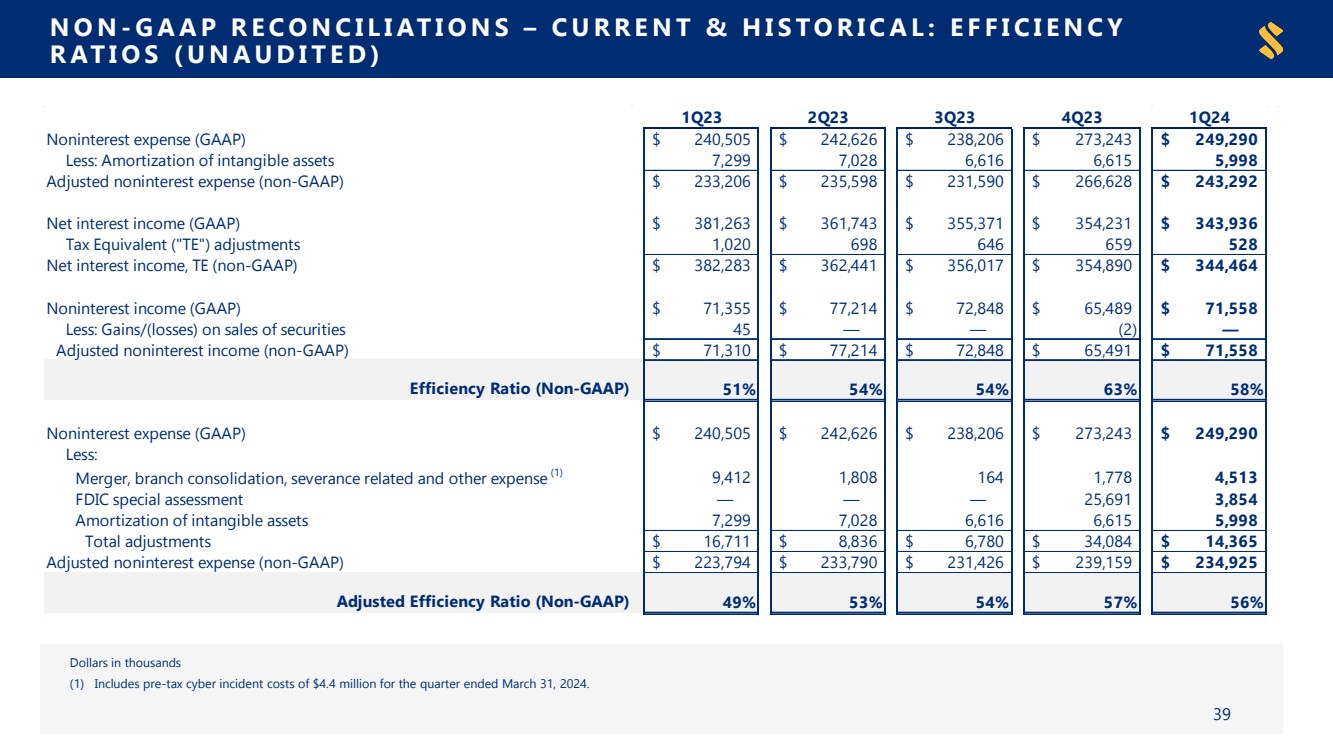

Adjusted Efficiency Ratio (4) | | | | | | | | | | | | | | | | | | | | |

Efficiency ratio | | | 58.48 | % | | | 63.43 | % | | | 54.00 | % | | | 53.59 | % | | | 51.41 | % |

Effect to adjust for merger, branch consolidation, severance related and other expense (8) | | | (1.08) | % | | | (0.43) | % | | | (0.04) | % | | | (0.41) | % | | | (2.07) | % |

Effect to adjust for FDIC special assessment | | | (0.93) | % | | | (6.11) | % | | | — | % | | | — | % | | | — | % |

Adjusted efficiency ratio | | | 56.47 | % | | | 56.89 | % | | | 53.96 | % | | | 53.18 | % | | | 49.34 | % |

| | | | | | | | | | | | | | | | | | | | |

Tangible Book Value Per Common Share (3) | | | | | | | | | | | | | | | | | | | | |

Book value per common share (GAAP) | | $ | 72.82 | | | $ | 72.78 | | | $ | 68.81 | | | $ | 69.61 | | | $ | 69.19 | |

Effect to adjust for intangible assets | | | (26.34) | | | | (26.46) | | | | (26.55) | | | | (26.65) | | | | (26.79) | |

Tangible book value per common share (non-GAAP) | | $ | 46.48 | | | $ | 46.32 | | | $ | 42.26 | | | $ | 42.96 | | | $ | 42.40 | |

| | | | | | | | | | | | | | | | | | | | |

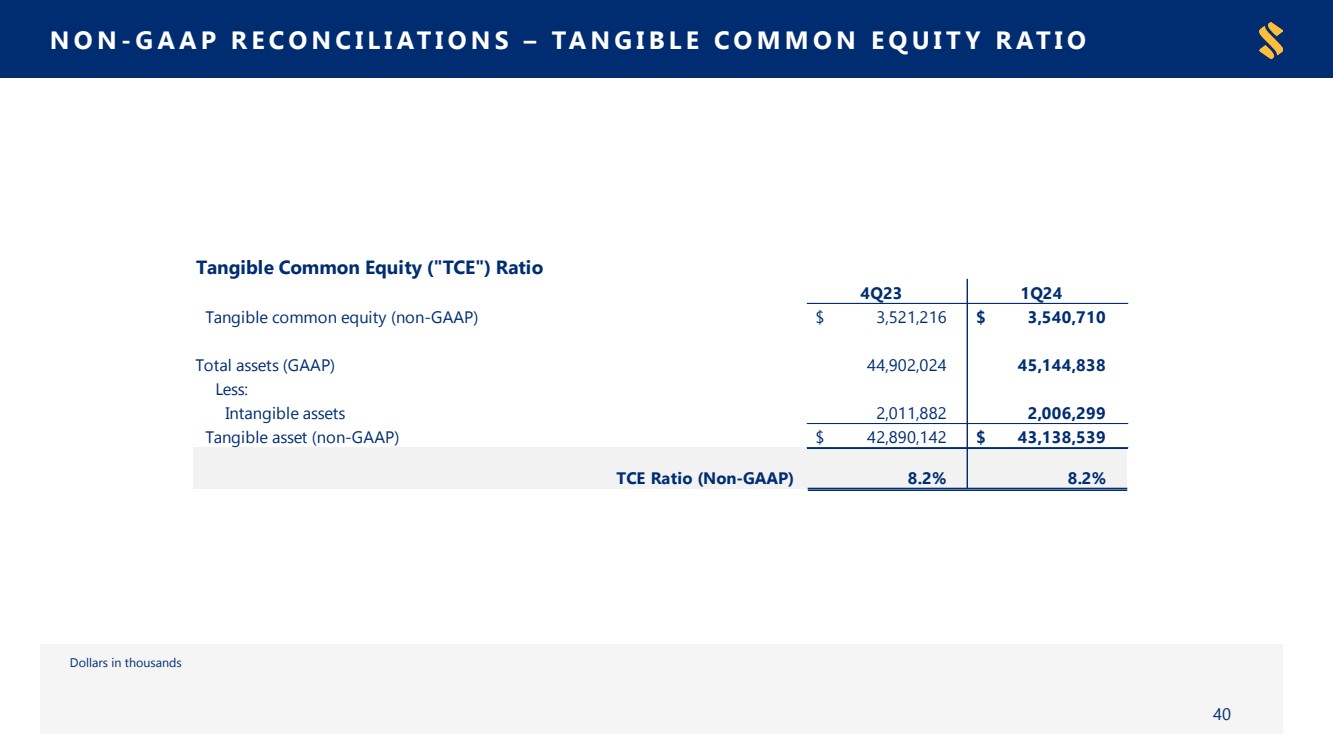

Tangible Equity-to-Tangible Assets (3) | | | | | | | | | | | | | | | | | | | | |

Equity-to-assets (GAAP) | | | 12.29 | % | | | 12.32 | % | | | 11.63 | % | | | 11.77 | % | | | 11.68 | % |

Effect to adjust for intangible assets | | | (4.08) | % | | | (4.11) | % | | | (4.15) | % | | | (4.16) | % | | | (4.18) | % |

Tangible equity-to-tangible assets (non-GAAP) | | | 8.21 | % | | | 8.21 | % | | | 7.48 | % | | | 7.61 | % | | | 7.50 | % |

10

Footnotes to tables:

| (1) | Includes loan accretion (interest) income related to the discount on acquired loans of $4.3 million, $3.9 million, $4.1 million, $5.5 million, and $7.4 million during the quarters ended March 31, 2024, December 31, 2023, September 30, 2023, June 30, 2023, and March 31, 2023, respectively. |

| (2) | Adjusted earnings, adjusted return on average assets, adjusted EPS, and adjusted return on average equity are non-GAAP measures and exclude the gains or losses on sales of securities, merger, branch consolidation, severance related and other expense, and FDIC special assessments. Management believes that non-GAAP adjusted measures provide additional useful information that allows readers to evaluate the ongoing performance of the Company. Non-GAAP measures should not be considered as an alternative to any measure of performance or financial condition as promulgated under GAAP, and investors should consider the Company's performance and financial condition as reported under GAAP and all other relevant information when assessing the performance or financial condition of the Company. Non-GAAP measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of the Company's results or financial condition as reported under GAAP. Adjusted earnings and the related adjusted return measures (non-GAAP) exclude the following from net income (GAAP) on an after-tax basis: (a) pre-tax merger, branch consolidation, severance related and other expense of $4.5 million, $1.8 million, $164,000, $1.8 million, and $9.4 million for the quarters ended March 31, 2024, December 31, 2023, September 30, 2023, June 30, 2023, and March 31, 2023, respectively; (b) pre-tax net securities (losses) gains of $(2,000) and $45,000 for the quarters ended December 31, 2023 and March 31, 2023, respectively; and (c) pre-tax FDIC special assessment of $3.9 million and $25.7 million for the quarters ended March 31, 2024 and December 31, 2023, respectively. |

| (3) | The tangible measures are non-GAAP measures and exclude the effect of period end or average balance of intangible assets. The tangible returns on equity and common equity measures also add back the after-tax amortization of intangibles to GAAP basis net income. Management believes that these non-GAAP tangible measures provide additional useful information, particularly since these measures are widely used by industry analysts for companies with prior merger and acquisition activities. Non-GAAP measures should not be considered as an alternative to any measure of performance or financial condition as promulgated under GAAP, and investors should consider the Company's performance and financial condition as reported under GAAP and all other relevant information when assessing the performance or financial condition of the Company. Non-GAAP measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of the Company's results or financial condition as reported under GAAP. The sections titled "Reconciliation of GAAP to Non-GAAP" provide tables that reconcile GAAP measures to non-GAAP. |

| (4) | Adjusted efficiency ratio is calculated by taking the noninterest expense excluding merger, branch consolidation, severance related and other expense, FDIC special assessment and amortization of intangible assets, divided by net interest income and noninterest income excluding securities gains (losses). The pre-tax amortization expenses of intangible assets were $6.0 million, $6.6 million, $6.6 million, $7.0 million, and $7.3 million for the quarters ended March 31, 2024, December 31, 2023, September 30, 2023, June 30, 2023, and March 31, 2023, respectively. |

| (5) | The dividend payout ratio is calculated by dividing total dividends paid during the period by the total net income for the same period. |

| (6) | March 31, 2024 ratios are estimated and may be subject to change pending the final filing of the FR Y-9C; all other periods are presented as filed. |

| (7) | Loan data excludes mortgage loans held for sale. |

| (8) | Includes pre-tax cyber incident costs of $4.4 million for the quarter ended March 31, 2024. |

11

Cautionary Statement Regarding Forward Looking Statements

Statements included in this communication, which are not historical in nature are intended to be, and are hereby identified as, forward-looking statements for purposes of the safe harbor provided by Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements are based on, among other things, management’s beliefs, assumptions, current expectations, estimates and projections about the financial services industry, the economy and SouthState. Words and phrases such as “may,” “approximately,” “continue,” “should,” “expects,” “projects,” “anticipates,” “is likely,” “look ahead,” “look forward,” “believes,” “will,” “intends,” “estimates,” “strategy,” “plan,” “could,” “potential,” “possible” and variations of such words and similar expressions are intended to identify such forward-looking statements.

SouthState cautions readers that forward-looking statements are subject to certain risks, uncertainties and assumptions that are difficult to predict with regard to, among other things, timing, extent, likelihood and degree of occurrence, which could cause actual results to differ materially from anticipated results. Such risks, uncertainties and assumptions, include, among others, the following: (1) economic downturn risk, potentially resulting in deterioration in the credit markets, inflation, greater than expected noninterest expenses, excessive loan losses and other negative consequences, which risks could be exacerbated by potential negative economic developments resulting from federal spending cuts and/or one or more federal budget-related impasses or actions; (2) risks related to the ability of the Company to pursue its strategic plans which depend upon certain growth goals in our lines of business; (3) risks relating to the ability to retain our culture and attract and retain qualified people, which could be exacerbated by the continuing work from remote environment; (4) credit risks associated with an obligor’s failure to meet the terms of any contract with the Bank or otherwise fail to perform as agreed under the terms of any loan-related document; (5) interest rate risk primarily resulting from our inability to effectively manage the risk, and their impact on the Bank’s earnings, including from the correspondent and mortgage divisions, housing demand, the market value of the Bank’s loan and securities portfolios, and the market value of SouthState’s equity; (6) a decrease in our net interest income due to the interest rate environment; (7) liquidity risk affecting the Bank’s ability to meet its obligations when they come due; (8) unexpected outflows of uninsured deposits may require us to sell investment securities at a loss; (9) potential deterioration in real estate values; (10) the loss of value of our investment portfolio could negatively impact market perceptions of us and could lead to deposit withdrawals; (11) price risk focusing on changes in market factors that may affect the value of traded instruments in “mark-to-market” portfolios; (12) transaction risk arising from problems with service or product delivery; (13) the impact of increasing digitization of the banking industry and movement of customers to on-line platforms, and the possible impact on the Bank’s results of operations, customer base, expenses, suppliers and operations; (14) controls and procedures risk, including the potential failure or circumvention of our controls and procedures or failure to comply with regulations related to controls and procedures; (15) volatility in the financial services industry (including failures or rumors of failures of other depository institutions), along with actions taken by governmental agencies to address such turmoil, could affect the ability of depository institutions, including us, to attract and retain depositors and to borrow or raise capital; (16) the impact of competition with other financial institutions, including deposit and loan pricing pressures and the resulting impact, including as a result of compression to net interest margin; (17) compliance risk involving risk to earnings or capital resulting from violations of or nonconformance with laws, rules, regulations, prescribed practices, or ethical standards, and contractual obligations regarding data privacy and cybersecurity; (18) regulatory change risk resulting from new laws, rules, regulations, accounting principles, proscribed practices or ethical standards, including, without limitation, the possibility that regulatory agencies may require higher levels of capital above the current regulatory-mandated minimums and including the impact of special FDIC assessments, the Consumer Financial Protection Bureau regulations or other guidance, and the possibility of changes in accounting standards, policies, principles and practices; (19) strategic risk resulting from adverse business decisions or improper implementation of business decisions; (20) reputation risk that adversely affects earnings or capital arising from negative public opinion including the effects of social media on market perceptions of us and banks generally; (21) cybersecurity risk related to the dependence of SouthState on internal computer systems and the technology of outside service providers, as well as the potential impacts of internal or external security breaches, which may subject the Company to potential business disruptions or financial losses resulting from deliberate attacks or unintentional events; (22) reputational and operational risks associated with environment, social and governance (ESG) matters, including the impact of changes in federal and state laws, regulations and guidance relating to climate change; (23) excessive loan losses; (24) reputational risk and possible higher than estimated reduced revenue from previously announced or proposed regulatory changes in the Bank’s consumer programs and products; (25) operational, technological, cultural, regulatory, legal, credit and other risks associated with the exploration, consummation and integration of potential future acquisitions, whether involving stock or cash consideration; (26) catastrophic events such as hurricanes, tornados, earthquakes, floods or other natural or human disasters, including public health crises and infectious disease outbreaks, as well as any government actions in response to such events, and the related disruption to local, regional and global economic activity and financial markets, and the impact that any of the foregoing may have on SouthState and its customers and other constituencies; (27) geopolitical risk from terrorist activities and armed conflicts that may result in economic and supply disruptions, and loss of market and consumer confidence; (28) the risks of fluctuations in market prices for SouthState common stock that may or may not reflect economic condition or performance of SouthState; (29) the payment of dividends on SouthState common stock, which is subject to legal and regulatory limitations as well as the discretion of the board of directors of SouthState, SouthState’s performance and other factors; (30) ownership dilution risk associated with potential acquisitions in which SouthState’s stock may be issued as consideration for an acquired company; and (31) other factors that may affect future results of SouthState, as disclosed in SouthState’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K, filed by SouthState with the U.S. Securities and Exchange Commission (“SEC”) and available on the SEC’s website at http://www.sec.gov, any of which could cause actual results to differ materially from future results expressed, implied or otherwise anticipated by such forward-looking statements.

All forward-looking statements speak only as of the date they are made and are based on information available at that time. SouthState does not undertake any obligation to update or otherwise revise any forward-looking statements, whether as a result of new information, future events, or otherwise, except as required by federal securities laws. As forward-looking statements involve significant risks and uncertainties, caution should be exercised against placing undue reliance on such statements.

12

| Earnings Call 1Q 2024 April 26, 2024 Exhibit 99.2 |

| DISCLAIMER 2 Statements included in this communication, which are not historical in nature are intended to be, and are hereby identified as, forward-looking statements for purposes of the safe harbor provided by Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements are based on, among other things, management’s beliefs, assumptions, current expectations, estimates and projections about the financial services industry, the economy and SouthState. Words and phrases such as “may,” “approximately,” “continue,” “should,” “expects,” “projects,” “anticipates,” “is likely,” “look ahead,” “look forward,” “believes,” “will,” “intends,” “estimates,” “strategy,” “plan,” “could,” “potential,” “possible” and variations of such words and similar expressions are intended to identify such forward-looking statements. SouthState cautions readers that forward-looking statements are subject to certain risks, uncertainties and assumptions that are difficult to predict with regard to, among other things, timing, extent, likelihood and degree of occurrence, which could cause actual results to differ materially from anticipated results. Such risks, uncertainties and assumptions, include, among others, the following: (1) economic downturn risk, potentially resulting in deterioration in the credit markets, inflation, greater than expected noninterest expenses, excessive loan losses and other negative consequences, which risks could be exacerbated by potential negative economic developments resulting from federal spending cuts and/or one or more federal budget-related impasses or actions; (2) risks related to the ability of the Company to pursue its strategic plans which depend upon certain growth goals in our lines of business; (3) risks relating to the ability to retain our culture and attract and retain qualified people, which could be exacerbated by the continuing work from remote environment; (4) credit risks associated with an obligor’s failure to meet the terms of any contract with the Bank or otherwise fail to perform as agreed under the terms of any loan-related document; (5) interest rate risk primarily resulting from our inability to effectively manage the risk, and their impact on the Bank’s earnings, including from the correspondent and mortgage divisions, housing demand, the market value of the Bank’s loan and securities portfolios, and the market value of SouthState’s equity; (6) a decrease in our net interest income due to the interest rate environment; (7) liquidity risk affecting the Bank’s ability to meet its obligations when they come due; (8) unexpected outflows of uninsured deposits may require us to sell investment securities at a loss; (9) potential deterioration in real estate values; (10) the loss of value of our investment portfolio could negatively impact market perceptions of us and could lead to deposit withdrawals; (11) price risk focusing on changes in market factors that may affect the value of traded instruments in “mark-to-market” portfolios; (12) transaction risk arising from problems with service or product delivery; (13) the impact of increasing digitization of the banking industry and movement of customers to on-line platforms, and the possible impact on the Bank’s results of operations, customer base, expenses, suppliers and operations; (14) controls and procedures risk, including the potential failure or circumvention of our controls and procedures or failure to comply with regulations related to controls and procedures; (15) volatility in the financial services industry (including failures or rumors of failures of other depository institutions), along with actions taken by governmental agencies to address such turmoil, could affect the ability of depository institutions, including us, to attract and retain depositors and to borrow or raise capital; (16) the impact of competition with other financial institutions, including deposit and loan pricing pressures and the resulting impact, including as a result of compression to net interest margin; (17) compliance risk involving risk to earnings or capital resulting from violations of or nonconformance with laws, rules, regulations, prescribed practices, or ethical standards, and contractual obligations regarding data privacy and cybersecurity; (18) regulatory change risk resulting from new laws, rules, regulations, accounting principles, proscribed practices or ethical standards, including, without limitation, the possibility that regulatory agencies may require higher levels of capital above the current regulatory-mandated minimums and including the impact of special FDIC assessments, the Consumer Financial Protection Bureau regulations or other guidance, and the possibility of changes in accounting standards, policies, principles and practices; (19) strategic risk resulting from adverse business decisions or improper implementation of business decisions; (20) reputation risk that adversely affects earnings or capital arising from negative public opinion including the effects of social media on market perceptions of us and banks generally; (21) cybersecurity risk related to the dependence of SouthState on internal computer systems and the technology of outside service providers, as well as the potential impacts of internal or external security breaches, which may subject the Company to potential business disruptions or financial losses resulting from deliberate attacks or unintentional events; (22) reputational and operational risks associated with environment, social and governance (ESG) matters, including the impact of changes in federal and state laws, regulations and guidance relating to climate change; (23) excessive loan losses; (24) reputational risk and possible higher than estimated reduced revenue from previously announced or proposed regulatory changes in the Bank’s consumer programs and products; (25) operational, technological, cultural, regulatory, legal, credit and other risks associated with the exploration, consummation and integration of potential future acquisitions, whether involving stock or cash consideration; (26) catastrophic events such as hurricanes, tornados, earthquakes, floods or other natural or human disasters, including public health crises and infectious disease outbreaks, as well as any government actions in response to such events, and the related disruption to local, regional and global economic activity and financial markets, and the impact that any of the foregoing may have on SouthState and its customers and other constituencies; (27) geopolitical risk from terrorist activities and armed conflicts that may result in economic and supply disruptions, and loss of market and consumer confidence; (28) the risks of fluctuations in market prices for SouthState common stock that may or may not reflect economic condition or performance of SouthState; (29) the payment of dividends on SouthState common stock, which is subject to legal and regulatory limitations as well as the discretion of the board of directors of SouthState, SouthState’s performance and other factors; (30) ownership dilution risk associated with potential acquisitions in which SouthState’s stock may be issued as consideration for an acquired company; and (31) other factors that may affect future results of SouthState, as disclosed in SouthState’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K, filed by SouthState with the U.S. Securities and Exchange Commission (“SEC”) and available on the SEC’s website at http://www.sec.gov, any of which could cause actual results to differ materially from future results expressed, implied or otherwise anticipated by such forward-looking statements. All forward-looking statements speak only as of the date they are made and are based on information available at that time. SouthState does not undertake any obligation to update or otherwise revise any forward-looking statements, whether as a result of new information, future events, or otherwise, except as required by federal securities laws. As forward-looking statements involve significant risks and uncertainties, caution should be exercised against placing undue reliance on such statements. |

| (1) Financial metrics as of March 31, 2024; market cap as of April 24, 2024 SouthState Corporation Overview of Franchise (1) (251) $37 Billion in deposits $33 Billion in loans $45 Billion in assets $6.1 Billion market cap 3 17 Greenwich Excellence & Best Brand Awards for Small Business Banking from Coalition Greenwich Ranked #14 by S&P Global |

| Local Market Leadership Our business model supports the unique character of the communities we serve and encourages decision making by the banker that is closest to the customer. Long-Term Horizon We think and act like owners and measure success over entire economic cycles. We prioritize soundness before short-term profitability and growth. Remarkable Experiences We will make our customers’ lives better by anticipating their needs and responding with a sense of urgency. Each of us has the freedom, authority and responsibility to do the right thing for our customers. Meaningful and Lasting Relationships We communicate with candor and transparency. The relationship is more valuable than the transaction. Greater Purpose We enable our team members to pursue their ultimate purpose in life—their personal faith, their family, their service to community. The WHAT The HOW Guiding Principles Core Values Leadership The WHY To invest in the entrepreneurial spirit, pursue excellence and inspire a greater purpose. 4 |

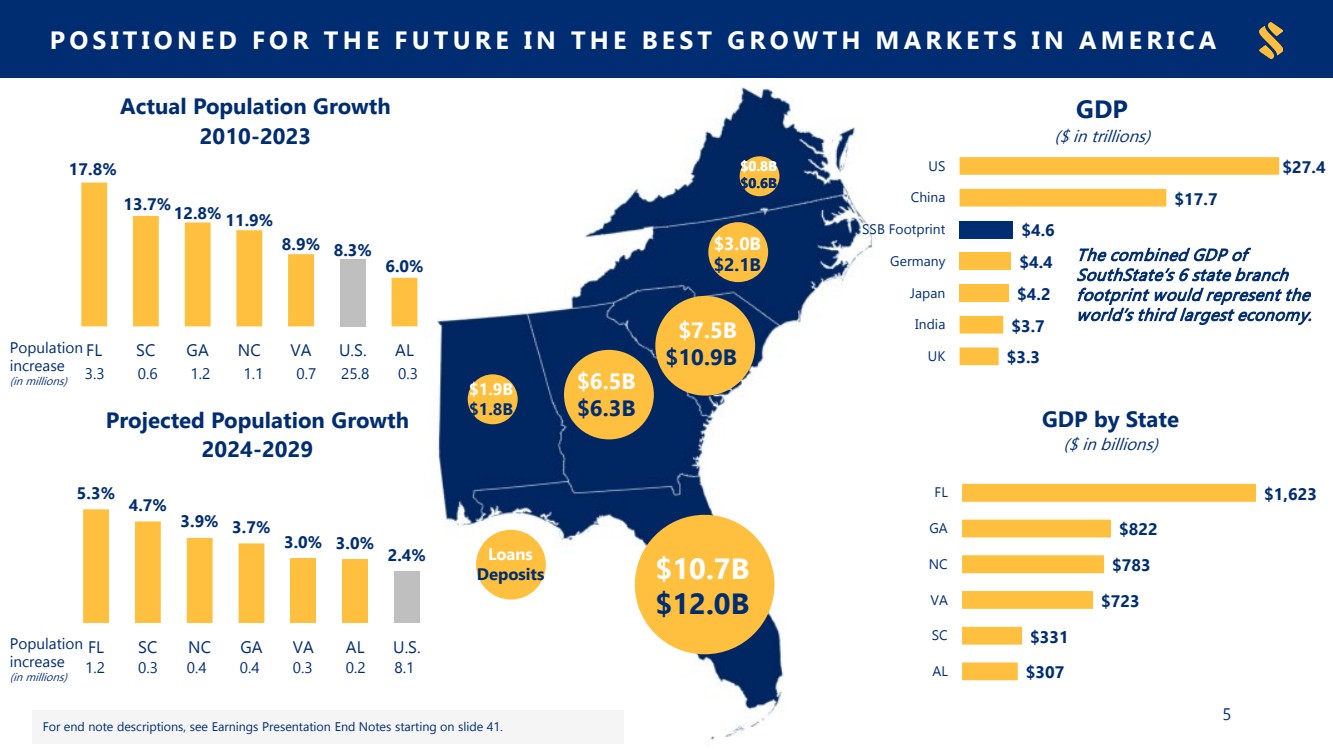

| 17.8% 13.7%12.8% 11.9% 8.9% 8.3% 6.0% FL SC GA NC VA U.S. AL Actual Population Growth 2010-2023 $1.9B $1.8B $0.8B $0.6B $3.0B $2.1B POSITIONED FOR THE FUTURE IN THE BEST GROWTH MARKETS IN AMERICA 5 $307 $331 $723 $783 $822 $1,623 AL SC VA NC GA FL GDP by State ($ in billions) 5.3% 4.7% 3.9% 3.7% 3.0% 3.0% 2.4% FL SC NC GA VA AL U.S. Projected Population Growth 2024-2029 $3.3 $3.7 $4.2 $4.4 $4.6 $17.7 $27.4 UK India Japan Germany SSB Footprint China US GDP ($ in trillions) The combined GDP of SouthState’s 6 state branch footprint would represent the world’s third largest economy. 1.2 0.3 0.4 0.4 0.3 0.2 8.1 Population increase (in millions) For end note descriptions, see Earnings Presentation End Notes starting on slide 41. Population increase (in millions) 3.3 0.6 1.2 1.1 0.7 25.8 0.3 $10.7B $12.0B $7.5B $10.9B $0.8B $0.6B $6.5B $6.3B Loans Deposits |

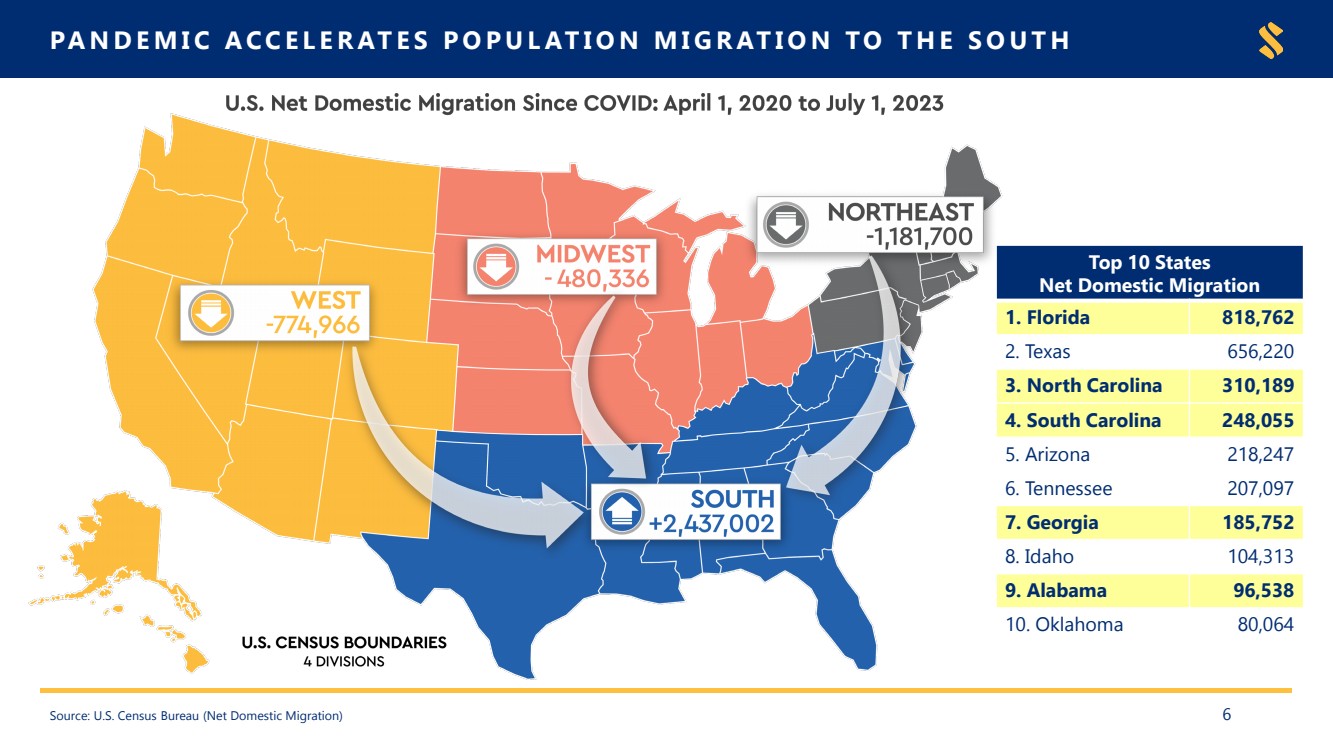

| Source: U.S. Census Bureau (Net Domestic Migration) PANDEMIC ACCELERATES POPULATION MIGRATION TO THE SOUTH Top 10 States Net Domestic Migration 1. Florida 818,762 2. Texas 656,220 3. North Carolina 310,189 4. South Carolina 248,055 5. Arizona 218,247 6. Tennessee 207,097 7. Georgia 185,752 8. Idaho 104,313 9. Alabama 96,538 10. Oklahoma 80,064 6 |

| INVESTMENT THESIS 7 • High growth markets • Granular, low-cost core deposit base • Diversified revenue streams • Strong credit quality and disciplined underwriting • Energetic and experienced management team with entrepreneurial ownership culture • True alternative to the largest banks with capital markets platform and upgraded technology solutions |

| Quarterly Results |

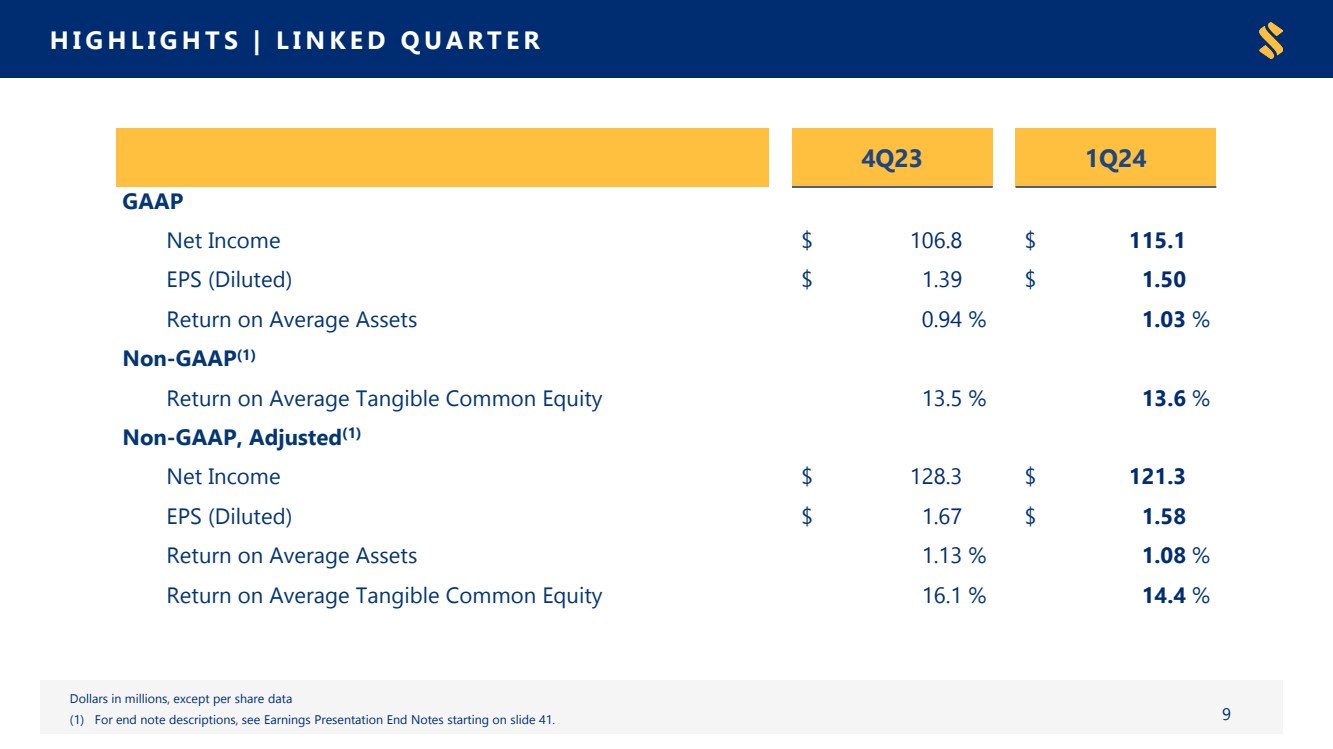

| HIGHLIGHTS | LINKED QUARTER Dollars in millions, except per share data (1) For end note descriptions, see Earnings Presentation End Notes starting on slide 41. 9 4Q23 1Q24 GAAP Net Income $ 106.8 $ 115.1 EPS (Diluted) $ 1.39 $ 1.50 Return on Average Assets 0.94 % 1.03 % Non-GAAP(1) Return on Average Tangible Common Equity 13.5 % 13.6 % Non-GAAP, Adjusted(1) Net Income $ 128.3 $ 121.3 EPS (Diluted) $ 1.67 $ 1.58 Return on Average Assets 1.13 % 1.08 % Return on Average Tangible Common Equity 16.1 % 14.4 % |