We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Share Name | Share Symbol | Market | Type |

|---|---|---|---|

| Hitek Global Inc | NASDAQ:HKIT | NASDAQ | Common Stock |

| Price Change | % Change | Share Price | Bid Price | Offer Price | High Price | Low Price | Open Price | Shares Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0.00 | 0.00% | 1.40 | 1.39 | 1.47 | 1.45 | 1.3897 | 1.45 | 25,801 | 23:55:25 |

As filed with the Securities and Exchange Commission on August 22, 2024

Registration No. 333-_________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM F-3

REGISTRATION STATEMENT

UNDER THE

SECURITIES ACT OF 1933

| HITEK GLOBAL INC. | ||

| (Exact name of registrant as specified in its charter) |

| Cayman Islands | Not Applicable | |

| (State

or other jurisdiction of incorporation or organization) |

(I.R.S.

Employer Identification No.) |

Unit 304, No. 30 Guanri Road, Siming District

Xiamen City, Fujian Province, People’s Republic of China

+86 592-5395967

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Puglisi& Associates

850 Library Avenue, Suite 204

Newark, Delaware 19711

+1- (302) 738-6680 — telephone

(Name, address including zip code, and telephone number, including area code, of agent for service)

With a copy to:

Bradley A. Haneberg, Esq.

Haneberg Hurlbert PLC

1111 East Main Street, Suite 2010

Richmond, Virginia 23219

+1-804-814-2209 — telephone

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement as determined by the registrant.

If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box: ☐

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a registration statement pursuant to General Instruction I.C. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. ☐

If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.C. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission acting pursuant to said section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated August 22, 2024

PROSPECTUS

Up to 14,907,000 Shares of Class A Ordinary Shares

Up to 14,907,000 Shares of Class A Ordinary Shares Issuable Upon Exercise of Warrants

Offered by the Selling Shareholders of

HITEK GLOBAL INC.

This prospectus relates to the resale, from time to time, by the selling shareholders (the “Selling Shareholders”) identified in this prospectus under the caption “Selling Shareholders,” of up to (i) 14,907,000 of our Series A Ordinary Shares, $0.0001 par value per share (the “Class A Ordinary Shares”) and (ii) 14,907,000 Class A Ordinary Shares issuable upon exercise of certain outstanding warrants (the “Warrants”).

The Class A Ordinary Shares and the Warrants were issued to the Selling Shareholders pursuant to the terms of that certain Securities Purchase Agreement, dated as of July 29, 2024. The Selling Shareholders purchased the Class A Ordinary Shares for an aggregate of $8,200,000 ($0.55 per Class A Ordinary Share). The Warrants, which we issued to the Selling Shareholders for nominal consideration, are exercisable for $0.55 per share and also contain a cashless exercise provision.

We are not selling any Class A Ordinary Shares or Warrants under this prospectus and will not receive any proceeds from the sale of Class A Ordinary Shares or Warrants by the Selling Shareholders. We will receive proceeds from cash exercise of the Warrants which, if exercised for cash with respect to all of the Class A Ordinary Shares, would result in gross proceeds of $8,198,850 to us. The Selling Shareholders will bear all commissions and discounts, if any, attributable to the sale of the Class A Ordinary Shares.

The Selling Shareholders may sell the Class A Ordinary Shares offered by this prospectus from time to time on terms to be determined at the time of sale through ordinary brokerage transactions or through any other means described in this prospectus under the caption “Plan of Distribution.” The Class A Ordinary Shares may be sold at fixed prices, at market prices prevailing at the time of sale, at prices related to prevailing market price or at negotiated prices.

Our Class A Ordinary Shares are listed on the Nasdaq Capital Market (“Nasdaq”) under the symbol “HKIT.” On August 22, 2024, the last reported sale price of our Class A Ordinary Shares on Nasdaq was $1.54 per share.

Investing in our securities being offered pursuant to this prospectus involves a high degree of risk. You should carefully read and consider the risk factors beginning on page 4 of this prospectus, as well as those included in the periodic and other reports we file with the Securities and Exchange Commission before you make your investment decision.

Neither the United States Securities and Exchange Commission nor any United States state securities commission, has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is August 22, 2024

TABLE OF CONTENTS

i

You should rely only on the information contained or incorporated by reference in this prospectus or any prospectus supplement. We have not authorized any person to provide you with different or additional information. If anyone provides you with different or inconsistent information, you should not rely on it. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement, as well as information we have previously filed with the SEC and incorporated by reference, is accurate as of the date on the front of those documents only. Our business, financial condition, results of operations and prospects may have changed since those dates.

This prospectus describes the general manner in which the Selling Shareholders may offer from time to time up to an aggregate of 29,814,000 Class A Ordinary Shares (including 14,907,000 Class A Ordinary Shares underlying the Warrants). You should rely only on the information contained in this prospectus and the related exhibits, any prospectus supplement or amendment thereto and the documents incorporated by reference, or to which we have referred you, before making your investment decision. Neither we nor the Selling Shareholders have authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. This prospectus, any prospectus supplement or amendments thereto do not constitute an offer to sell, or a solicitation of an offer to purchase, the Class A Ordinary Shares offered by this prospectus, any prospectus supplement or amendments thereto in any jurisdiction to or from any person to whom or from whom it is unlawful to make such offer or solicitation of an offer in such jurisdiction. You should not assume that the information contained in this prospectus, any prospectus supplement or amendments thereto, or the information we have previously filed with the U.S. Securities and Exchange Commission (the “SEC”), is accurate as of any date other than the date on the front cover of the applicable document.

If necessary, the specific manner in which the Class A Ordinary Shares may be offered and sold will be described in a supplement to this prospectus, which supplement may also add, update or change any of the information contained in this prospectus. To the extent there is a conflict between the information contained in this prospectus and the prospectus supplement, you should rely on the information in the prospectus supplement, provided that if any statement in one of these documents is inconsistent with a statement in another document having a later date - for example, a document incorporated by reference in this prospectus or any prospectus supplement - the statement in the document having the later date modifies or supersedes the earlier statement.

Neither the delivery of this prospectus nor any distribution of Class A Ordinary Shares pursuant to this prospectus shall, under any circumstances, create any implication that there has been no change in the information set forth or incorporated by reference into this prospectus or in our affairs since the date of this prospectus. Our business, financial condition, results of operations and prospects may have changed since such date.

As permitted by SEC rules and regulations, the registration statement of which this prospectus forms a part includes additional information not contained in this prospectus. You may read the registration statement and the other reports we file with the SEC at its website, as described below under “Where You Can Find More Information.”

Except as otherwise indicated by the context, references in this prospectus to “we,” “us,” the “Company,” and “our” refer to HiTek Global, Inc., a Cayman Islands (“BVI”) company limited by shares, and its consolidated subsidiaries.

ii

INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

This prospectus and the documents incorporated by reference herein contain statements of a forward-looking nature. All statements other than statements of historical facts are forward-looking statements. These forward-looking statements are made under the “safe harbor” provision under Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) and as defined in the Private Securities Litigation Reform Act of 1995. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements. In some cases, these forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions. These forward-looking statements relate to, among others:

| ● | future financial and operating results, including revenues, income, expenditures, cash balances and other financial items; | |

| ● | impact of the COVID-19 pandemic on our business, results of operations, financial condition and cash flows; | |

| ● | our ability to execute our growth, expansion and acquisition strategies, including our ability to meet our goals; |

| ● | current and future economic and political conditions; | |

| ● | the response of participants using ACTCS (as such term is defined herein) tax device or its supporting services to any difficulties encountered by companies filing VAT (as such term is defined herein) through these systems; | |

| ● | changes in the regulations of PRC government bodies and agencies relating to VAT collection procedure and ACTCS business; | |

| ● | our ability to provide participants in projects using our services with a secure and acceptable payment method; | |

| ● | our ability to continue to operate through the VIE structure; | |

| ● | our capital requirements and our ability to raise any additional financing which we may require; | |

| ● | our ability to protect our intellectual property rights and secure the right to use other intellectual property that we deem to be essential or desirable to the conduct of our business; | |

| ● | our ability to hire and retain qualified management personnel and key employees in order to enable us to develop our business; | |

| ● | our ability to retain the services of Ms. Xiaoyang Huang, our Chief Executive Officer; | |

| ● | overall industry and market performance; and | |

| ● | other assumptions described in this prospectus underlying or relating to any forward-looking statements. |

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs.

You should read these statements in conjunction with the risks discussed under the heading “Risk Factors” included in the applicable prospectus supplement or under similar headings in other documents which are incorporated by reference in this prospectus. Moreover, we operate in an emerging and evolving environment. New risks may emerge from time to time, and it is not possible for our management to predict all risks, nor can we assess the impact of such risks on our business or the extent to which any risk, or combination of risks, may cause actual results to differ materially from those contained in any forward-looking statements. The forward-looking statements made in this prospectus and the documents incorporated by reference herein relate only to events or information as of the date on which the statements are made in this prospectus and such incorporated documents. Except as required by law, we undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this prospectus and the documents incorporated by reference herein and have filed as exhibits to this prospectus and the incorporated documents, completely and with the understanding that our actual future results may be materially different from what we expect.

iii

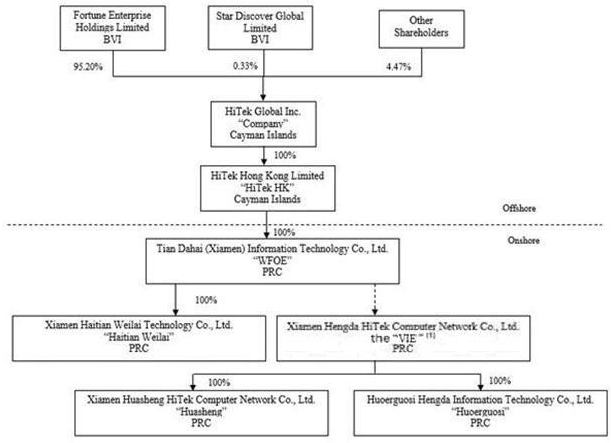

We are an offshore holding company incorporated in the Cayman Islands. As a holding company with no material operations, our operations were conducted in China by (i) Haitian Weilai, our indirect subsidiary, (ii) the VIE, HiTek and the VIE’s subsidiaries, Huasheng and Huoerguosi. Neither we nor our subsidiaries own any equity interests in the VIE. WFOE, the VIE and the shareholders of the VIE entered into a series of contractual arrangements (the “VIE Agreements”) pursuant to which we are able to consolidate the financial results of the VIE in our consolidated financial statements because we are deemed as the primary beneficial of the VIE under generally accepted accounting principles in the U.S. (“U.S. GAAP”), and this structure involves unique risks to investors.

The following diagram illustrates our corporate structure as of August 22, 2024. All percentages in the following diagram reflect the voting ownership interests instead of the equity interests held by each of our shareholders given that each holder of Class B Ordinary Shares will be entitled to 15 votes per one Class B Ordinary Share, and each holder of Class A Ordinary Shares will be entitled to one vote per one Class A Ordinary Share:

Business Overview

We are an information technology (“IT”) consulting and solutions service provider focusing on delivering services to business in various industry sectors in China. As of the date of prospectus, we have two lines of businesses—1) services to small and medium businesses, which consists of Anti-Counterfeiting Tax Control System (“ACTCS”) tax devices, including Golden Tax Disk (“GTD”) and printers, ACTCS services, and IT services, and 2) services to large businesses, which consists of hardware sales and software sales. We expect to actively develop our system integration services and online service platform in the near future. Our vision is to become a one-stop consulting destination for holistic IT and other business consulting services in China.

The VIE is authorized to carry out the sales of GTD and a market leader in the Xiamen metropolitan area with respect to ACTCS tax devices and services since 1996. We provide our customers with the necessary ACTCS for their value added tax (“VAT”) reporting, collection and processing. VAT reporting is mandatory for all business enterprises in China. The ACTCS is one of the two major VAT control systems that a business entity may choose to comply with the VAT reporting requirements. Developed by the PRC government, ACTCS was intended to effectively eliminate counterfeit invoices, providing accurate and complete tax information for the regional and national audit system. We are authorized by the State Taxation Bureau, Xiamen Branch, as one of the first ACTCS service providers in the Xiamen metropolitan area. GTD is an ACTCS device necessary for normal operation of ACTCS software. The purchase of GTD is allowed only in conjunction with the use of the ACTCS software and its supporting services. Since 1996, we have been the number one ACTCS services provider for Xiamen business enterprises according to the data compiled by Xiamen Province Taxation Bureau.

1

Complementing our physical service center, we started developing online service center in 2018 to enable tens of thousands of businesses in the Xiamen metropolitan area to securely process VAT reporting and payment from their desktop virtually anytime and anywhere. Currently, our customers range from small, medium to large enterprises across industries in the Xiamen metropolitan area.

In April 2021, WFOE established a wholly-owned subsidiary, Xiamen Haitian Weilai Technology Co., Ltd. (“Haitian Weilai”) under the laws of the PRC. The strategy purpose of establishing the new subsidiary is for the integration of tax invoicing management services from the VIE to Haitian Weilai.

As part of the services provided to large businesses, the VIE currently sells its Communication Interface System (“CIS”), its self-developed software which provides embedded system interface solutions for large businesses. CIS is a universal embedded interface system used in petrochemical and coal businesses to collect industrial, electricity, facility pressure and temperature statistics and convert to readable format for analytical purposes.

As part of our services provided to large businesses, Huasheng sold hardware such as laptops, printers, desktop computers and associated accessories, together with certain internet servers, cameras and monitors. Huasheng’s major business strategy in its market was to connect and source through exclusive relationships with manufacturers so that Huasheng could offer competitively priced hardware. Huasheng has established its online support system in the beginning of 2018. The online system further enhanced Huasheng’s customer experience, which is complemented by highly trained professionals and attractive physical store environment. From the beginning of 2022, Huasheng transferred the above business to the VIE.

Corporate Information

Our principal executive offices are located at Unit 304, No. 30 Guanri Road, Siming District, Xiamen City, Fujian Province, PRC. Our telephone number at this address is +86 592-5395967. Our registered office in the Cayman Islands is located at the offices of Maples Corporate Services Limited, PO Box 309, Ugland House, Grand Cayman, KY1-1104, Cayman Islands. Our agent for service of process in the United States is Puglisi & Associates, located at 850 Library Avenue, Suite 204, Newark, Delaware 19711.

The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at www.sec.gov. You can also find information on our website at http://www.xmhitek.com. The information contained on our website is not a part of this prospectus.

As a foreign private issuer, we are exempt under the Exchange Act from, among other things, the rules prescribing the furnishing and content of proxy statements, and our executive officers, directors and principal shareholders are exempt from the reporting and short-swing profit recovery provisions contained in Section 16 of the Exchange Act. In addition, we will not be required under the Exchange Act to file periodic reports and financial statements with the SEC as frequently or as promptly as U.S. companies whose securities are registered under the Exchange Act.

2

| Class A Ordinary Shares issued and outstanding as of August 22, 2024 | 21,107,364 Class A Ordinary Shares. | |

| Class A Ordinary Shares offered by the Selling Shareholders | Up to 29,814,000 Class A Ordinary Shares, including 14,907,000 Class A Ordinary Shares and 14,907,000 Class A Ordinary Shares underlying the Warrants. | |

| Class A Ordinary Shares to be outstanding immediately after this offering | 36,014,354 Class A Ordinary Shares, assuming the exercise of all of the Warrants. | |

| Terms of the offering | The Selling Shareholders, including their transferees, donees, pledgees, assignees and successors-in-interest, may sell, transfer or otherwise dispose of any or all of the Class A Ordinary Shares offered by this prospectus from time to time on Nasdaq or any other stock exchange, market or trading facility on which the shares are traded or in private transactions. The Class A Ordinary Shares may be sold at fixed prices, at market prices prevailing at the time of sale, at prices related to prevailing market prices or at negotiated prices. | |

| Use of proceeds | The Selling Shareholders will receive all of the proceeds from the sale of any Ordinary Shares sold by them pursuant to this prospectus. We will not receive any proceeds from the sale of the Ordinary Shares by the Selling Shareholders. We may receive proceeds in the event that any of the Warrants are exercised at their respective exercise prices per share which may result in gross proceeds of up to an aggregate of $8,198,850. Any proceeds that we receive from the exercise of the Warrants will be used for general corporate purposes. See “Use of Proceeds” in this prospectus. | |

|

Listing

|

Our Class A Ordinary Shares are listed on Nasdaq under the symbol “HKIT.” There is no established trading market for the Warrants and we do not intend to list the Warrants on any exchange or other trading system. | |

|

Risk factors

|

Investing in our securities involves a high degree of risk. See “Risk Factors” below, beginning on page 4, and in our Form 20-F for the year ended December 31, 2023, which is incorporated by reference herein, to read about the risks you should consider before investing in our securities. |

3

Before you make a decision to invest in our securities, you should consider carefully the risks described below, together with other information in this prospectus and the information incorporated by reference herein and therein, including our 2023 Form 20-F. If any of the following events actually occur, our business, operating results, prospects or financial condition could be materially and adversely affected. This could cause the trading price of our Class A Ordinary Shares to decline and you may lose all or part of your investment. The risks described below are not the only ones that we face. Additional risks not presently known to us or that we currently deem immaterial may also significantly impair our business operations and could result in a complete loss of your investment.

Risks Related to this Offering

You may experience dilution to the extent that our Class A Ordinary Shares are issued upon the exercise of outstanding Warrants or other securities that we may issue in the future.

You may experience dilution to the extent that our Class A Ordinary Shares are issued upon the exercise of our outstanding Warrants, and if we issue additional equity securities, or there are any issuances and subsequent exercises of stock options issued in the future. Up to 14,907,000 Class A Ordinary Shares may be issued with the exercise of Warrants at a per share exercise price of $0.55 issued to the Selling Shareholders in a private placement (the “July 2024 Private Placement”). These Warrants also bear anti-dilution protections in the event of stock dividends or splits, business combination, sale of assets, similar recapitalization transactions, or other similar transactions.

A large number of Class A Ordinary Shares may be sold in the market following this offering, which may depress the market price of our Ordinary Shares.

The Class A Ordinary Shares sold in this offering will be freely tradable without restriction or further registration under the Securities Act. As a result, a substantial number of our Class A Ordinary Shares may be sold in the public market following this offering. If there are significantly more Class A Ordinary Shares offered for sale than buyers are willing to purchase, then the market price of our Class A Ordinary Shares may decline to a market price at which buyers are willing to purchase the offered Class A Ordinary Shares and sellers remain willing to sell our Class A Ordinary Shares.

On July 29, 2024, we issued and sold (a) 14,907,000 Class A Ordinary Shares and (b) Warrants to purchase up to an aggregate of 14,907,000 Class A Ordinary Shares at an exercise price equal to $0.55 per share in a private placement (the “Private Placement”).

In accordance with the Securities Purchase Agreement relating to the Private Placement, we are required to file a registration statement providing for the resale of the Class A Ordinary Shares and the Class A Ordinary Shares underlying the Warrants. We are complying this requirement by filing this registration statement.

You should review a copy of the Securities Purchase Agreement which is included as an exhibit to the Current Report on Form 6-K that we furnished with the SEC on August 12, 2024, for a complete description of the terms and conditions of such agreements and documents, the Private Placement, this offering and all related transaction agreements.

4

We will not receive any of the proceeds from the sale of the Class A Ordinary Shares or the Class A Ordinary Shares underlying the Warrants by the Selling Shareholders pursuant to this prospectus. We may receive up to $8,198,850 in aggregate gross proceeds from cash exercises of the Warrants, based on the per share exercise price of the Warrants. Any proceeds we receive from the exercise of the Warrants will be used for working capital and general corporate purposes. The Selling Shareholders will pay any agent’s commissions and expenses they incur for brokerage, accounting, tax or legal services or any other expenses that they incur in disposing of such Class A Ordinary Shares. We will bear all other costs, fees and expenses incurred in effecting the registration of such Class A Ordinary Shares covered by this prospectus and any prospectus supplement. These may include, without limitation, all registration and filing fees, SEC filing fees and expenses of compliance with state securities or “blue sky” laws.

We cannot predict when or if the Warrants will be exercised, and it is possible that the Warrants may expire and never be exercised. As a result, we may never receive meaningful, or any, cash proceeds from the exercise of the Warrants, and we cannot plan on any specific uses of any proceeds we may receive beyond the purposes described herein.

See “Plan of Distribution” elsewhere in this prospectus for more information.

The information in this table should be read in conjunction with the financial statements and notes thereto and other financial information incorporated by reference in this prospectus and any prospectus supplement. Our historical results do not necessarily indicate our expected results for any future periods.

| As of December 31, 2023 | ||||||||

| Shareholders’ Equity | Actual | As adjusted* | ||||||

| (Unaudited) | ||||||||

| Ordinary Shares, par value $0.0001 per share, 490,000,000 shares authorized; 14,392,364 shares issued and outstanding as of December 31, 2023** | 1,439 | 2,930 | ||||||

| Additional paid-in capital | 16,721,551 | 24,902,060 | ||||||

| Statutory reserves | 836,215 | 836,215 | ||||||

| Retained earnings | 11,387,748 | 11,387,748 | ||||||

| Accumulated other comprehensive loss | (609,367 | ) | (609,367 | ) | ||||

| Total Shareholders’ Equity | 28,337,586 | 36,519,586 | ||||||

| Total Capitalization | $ | 28,337,586 | $ | 36,519,586 | ||||

| * | Reflects the sale of 14,907,000 Class A Ordinary Shares in the Private Placement at price of $0.55 per share on July 29, 2024. Ordinary shares and additional paid-in capital reflect the net proceeds we expect to receive, after deducting the attorney fees. We estimate that such net proceeds will be $8,182,000. |

| ** | On February 5, 2024, the 2024 annual general meeting of shareholders adopted the resolutions that the issued 14,392,364 ordinary shares of par value of US$0.0001 each are re-designated and re-classified into 6,200,364 Class A Ordinary Shares of par value US$0.0001 each with one vote per share and 8,192,000 Class B Ordinary Shares of par value US$0.0001 each with 15 votes per share on a one for one basis. |

You should read this information together with our financial statements and the notes to those statements incorporated by reference into this prospectus.

We are a Cayman Islands company and our affairs are governed by our memorandum and articles of association and the Companies Act (As Revised) of the Cayman Islands, which we refer to as the Companies Act below. The following description of our memorandum and articles of association, as amended and restated from time to time, are summaries and do not purport to be complete.

As of May 16, 2024, our authorized share capital consists of $50,000 divided into 500,000,000 shares, par value US$0.0001 per share, comprised of 431,808,000 Class A Ordinary Shares, 58,192,000 Class B Ordinary Shares, and 10,000,000 preference shares.

Our directors may, in their absolute discretion and without the approval of our shareholders, create and designate out of the unissued preference shares of our company one or more classes or series of preference shares, comprising such number of preference shares, and having such designations, powers, preferences, privileges and other rights, including dividend rights, voting rights, conversion rights, terms of redemption and liquidation preferences, as our directors may determine. As of the date hereof, there are 6,200,364 Class A Ordinary Shares and 8,192,000 Class B Ordinary Shares issued and outstanding. The following are summaries of material provisions of our amended and restated memorandum and articles of association and the Companies Act insofar as they relate to the material terms of our Class A Ordinary Shares and Class B Ordinary Shares.

5

Ordinary shares

Dividends. Subject to any rights and restrictions of any other class or series of shares, our board of directors may, from time to time, declare dividends on the shares issued and authorize payment of the dividends out of our lawfully available funds. No dividends shall be declared by the board out of our company except the following:

| ● | profits; or |

| ● | “share premium account,” which represents the excess of the price paid to our company on issue of its shares over the par or “nominal” value of those shares, which is similar to the U.S. concept of additional paid in capital. |

However, no dividend shall bear interest against the Company.

Voting Rights. Holders of Class A Ordinary Shares and Class B Ordinary Shares have the same rights except for voting and conversion rights as set forth in our memorandum and articles of association. In respect of matters requiring a vote of all shareholders, each holder of Class A Shares will be entitled to one vote per one Class A Share and each holder of Class B Ordinary Shares will be entitled to 15 votes per one Class B Ordinary Share. The Class B Ordinary Shares are convertible into Class A Ordinary Shares at any time after issuance at the option of the holder on a one-to-one basis.

On a show of hands, every shareholder who is present in person and every person representing a shareholder by proxy shall have one vote for each Class A Ordinary Share and 15 votes for each Class B Ordinary Share of which he or the person represented by proxy is the holder. On a poll, a Class A shareholder shall have one vote for each Class A Ordinary Share he holds whereas a Class B Ordinary shareholder shall have 15 votes for each Class B Ordinary Share he holds, unless any share carries special voting rights. In addition, all shareholders holding shares of a particular class are entitled to vote at a meeting of the holders of that class of shares. Votes may be given either personally or by proxy.

Any ordinary resolution to be made by the shareholders requires the affirmative vote of a simple majority of the votes cast in a general meeting, while a special resolution requires the affirmative vote of no less than two-thirds of the votes cast.

Under Cayman Islands law, some matters, such as amending the memorandum and articles of association, changing the name or resolving to be registered by way of continuation in a jurisdiction outside the Cayman Islands, require approval of shareholders by a special resolution.

There are no limitations on non-residents or foreign shareholders in the memorandum and articles of association to hold or exercise voting rights on the Class A Ordinary Shares or Class B Ordinary Shares imposed by foreign law or by the charter or other constituent document of our company. However, no person will be entitled to vote at any general meeting or at any separate meeting of the holders of the Class A Ordinary Shares or Class B Ordinary Shares unless the person is registered as of the record date for such meeting and unless all calls or other sums presently payable by the person in respect of Class A Ordinary Shares or Class B Ordinary Shares in the Company have been paid.

Winding Up; Liquidation. Upon the winding up of our company, after the full amount that holders of any issued shares ranking senior to the Class A Ordinary Shares or Class B Ordinary Shares as to distribution on liquidation or winding up are entitled to receive has been paid or set aside for payment, the holders of our Class A Ordinary Shares or Class B Ordinary Shares are entitled to receive any remaining assets of the Company available for distribution as determined by the liquidator. The assets received by the holders of our Class A Ordinary Shares or Class B Ordinary Shares in a liquidation may consist in whole or in part of property, which is not required to be of the same kind for all shareholders.

Calls on Ordinary Shares and Forfeiture of Ordinary Shares. Our board of directors may from time to time make calls upon shareholders for any amounts unpaid on their Class A Ordinary Shares or Class B Ordinary Shares in a notice served to such shareholders at least 14 days prior to the specified time and place of payment. Any Class A Ordinary Shares or Class B Ordinary Shares that have been called upon and remain unpaid are subject to forfeiture.

Redemption of Ordinary Shares. We may issue shares that are, or at its option or at the option of the holders are, subject to redemption on such terms and in such manner as it may, before the issue of the shares, determine. Under the Companies Act, shares of a Cayman Islands company may be redeemed or repurchased out of profits of the company, out of the proceeds of a fresh issue of shares made for that purpose or out of capital, provided the memorandum and articles of association authorize this and it has the ability to pay its debts as they come due in the ordinary course of business.

6

No Preemptive Rights. Holders of Class A Ordinary Shares or Class B Ordinary Shares will have no preemptive or preferential right to purchase any securities of our company.

Variation of Rights Attaching to Shares. If at any time the share capital is divided into different classes of shares, the rights attaching to any class (unless otherwise provided by the terms of issue of the shares of that class) may, subject to the memorandum and articles of association, be varied or abrogated with the consent in writing of the holders of three-fourth of the issued shares of that class or with the sanction of a special resolution passed at a general meeting of the holders of the shares of that class.

Anti-Takeover Provisions. Some provisions of our current memorandum and articles of association may discourage, delay or prevent a change of control of our company or management that shareholders may consider favorable, including provisions that authorize our board of directors to issue preference shares in one or more Class And to designate the price, rights, preferences, privileges and restrictions of such preference shares without any further vote or action by our shareholders.

Exempted Company. We are an exempted company with limited liability under the Companies Act. The Companies Act distinguishes between ordinary resident companies and exempted companies. Any company that is registered in the Cayman Islands but conducts business mainly outside of the Cayman Islands may apply to be registered as an exempted company. The requirements for an exempted company are essentially the same as for an ordinary company except that an exempted company:

| ● | does not have to file an annual return of its shareholders with the Registrar of Companies; | |

| ● | is not required to open its register of members for inspection; | |

| ● | does not have to hold an annual general meeting; | |

| ● | may issue shares with no par value; | |

| ● | may obtain an undertaking against the imposition of any future taxation (such undertakings are usually given for 20 years in the first instance); | |

| ● | may register by way of continuation in another jurisdiction and be deregistered in the Cayman Islands; | |

| ● | may register as a limited duration company; and | |

| ● | may register as a segregated portfolio company. |

“Limited liability” means that the liability of each shareholder is limited to the amount unpaid by the shareholder on the shares of the company (except in exceptional circumstances, such as involving fraud, the establishment of an agency relationship or an illegal or improper purpose or other circumstances in which a court may be prepared to pierce or lift the corporate veil).

7

Register of Members

Under Cayman Islands law, we must keep a register of members and there shall be entered therein:

| (a) | the names and addresses of the members, a statement of the shares held by each member, and of the amount paid or agreed to be considered as paid, on the shares of each member; |

| (b) | the date on which the name of any person was entered on the register as a member; |

| (c) | the date on which any person ceased to be a member; and |

| (d) | whether voting rights are attached to the share in issue. |

Under Cayman Islands law, the register of members of our company is prima facie evidence of the matters set out therein (i.e. the register of members will raise a presumption of fact on the matters referred to above unless rebutted) and a member registered in the register of members shall be deemed as a matter of Cayman Islands law to have legal title to the shares as set against its name in the register of members. Upon the closing of this public offering, the register of members shall be immediately updated to reflect the issue of shares by us. Once our register of members has been updated, the shareholders recorded in the register of members shall be deemed to have legal title to the shares set against their name.

However, there are certain limited circumstances where an application may be made to a Cayman Islands court for a determination on whether the register of members reflects the correct legal position. Further, the Cayman Islands court has the power to order that the register of members maintained by a company should be rectified where it considers that the register of members does not reflect the correct legal position. If an application for an order for rectification of the register of members were made in respect of our Class A Ordinary Shares or Class B Ordinary Shares, then the validity of such shares may be subject to re-examination by a Cayman Islands court.

Preference shares

Our amended and restated memorandum and articles of association authorizes the issuance of 10,000,000 preference shares with such designation, rights and preferences as may be determined from time to time by our board of directors. Accordingly, our board of directors is empowered, without shareholder approval, to issue preference shares with dividend, liquidation, redemption, voting or other rights which could adversely affect the voting power or other rights of the holders of our Class A Ordinary Shares and Class B Ordinary Shares. We may issue some or all of the preference shares to effect a business combination. In addition, the preference shares could be utilized as a method of discouraging, delaying or preventing a change in control of us. Although we do not currently intend to issue any preference shares, we cannot assure you that we will not do so in the future.

Warrants

As of the date of this prospectus, there are outstanding Warrants to purchase up to 14,907,000 Class A Ordinary Shares of the Company. The Warrants have an exercise price of $0.55 per Class A Ordinary Share. The Warrants became exercisable on July 29, 2024 and will expire on January 28, 2026. The exercise price and number of Class A Ordinary Shares issuable upon exercise of the Warrants is subject to appropriate adjustment upon the occurrence of certain events, including, but not limited to, stock dividends or splits, business combination, sale of assets, similar recapitalization transactions or other similar transactions. The Warrants also have a cashless exercise provision.

8

Certain Differences in Corporate Law

Cayman Islands companies are governed by the Companies Act. The Companies Act is modeled on English Law but does not follow recent English Law statutory enactments, and differs from laws applicable to United States corporations and their shareholders. Set forth below is a summary of the material differences between the provisions of the Companies Act applicable to us and the laws applicable to companies incorporated in the United States and their shareholders.

Mergers and Similar Arrangements.

In certain circumstances, the Companies Act allows for mergers or consolidations between two Cayman Islands companies, or between a Cayman Islands company and a company incorporated in another jurisdiction (provided that is facilitated by the laws of that other jurisdiction).

Where the merger or consolidation is between two Cayman Islands companies, the directors of each company must approve a written plan of merger or consolidation containing certain prescribed information. That plan or merger or consolidation must then be authorized by either (a) a special resolution (usually a majority of 66.6% in value) of the shareholders of each company; or (b) such other authorization, if any, as may be specified in such constituent company’s articles of association. No shareholder resolution is required for a merger between a parent company (i.e., a company that owns at least 90% of the issued shares of each class in a subsidiary company) and its subsidiary company. The consent of each holder of a fixed or floating security interest of a constituent company must be obtained unless the court waives such requirement. If the Cayman Islands Registrar of Companies is satisfied that the requirements of the Companies Act (which includes certain other formalities) have been complied with, the Registrar of Companies will register the plan of merger or consolidation.

Where the merger or consolidation involves a foreign company, the procedure is similar, save that with respect to the foreign company, the director of the Cayman Islands company is required to make a declaration to the effect that, having made due enquiry, he is of the opinion that the requirements set out below have been met: (i) that the merger or consolidation is permitted or not prohibited by the constitutional documents of the foreign company and by the laws of the jurisdiction in which the foreign company is incorporated, and that those laws and any requirements of those constitutional documents have been or will be complied with; (ii) that no petition or other similar proceeding has been filed and remains outstanding or order made or resolution adopted to wind up or liquidate the foreign company in any jurisdictions; (iii) that no receiver, trustee, administrator or other similar person has been appointed in any jurisdiction and is acting in respect of the foreign company, its affairs or its property or any part thereof; (iv) that no scheme, order, compromise or other similar arrangement has been entered into or made in any jurisdiction whereby the rights of creditors of the foreign company are and continue to be suspended or restricted.

Where the surviving company is the Cayman Islands company, the director of the Cayman Islands company is further required to make a declaration to the effect that, having made due enquiry, he is of the opinion that the requirements set out below have been met: (i) that the foreign company is able to pay its debts as they fall due and that the merger or consolidated is bona fide and not intended to defraud unsecured creditors of the foreign company; (ii) that in respect of the transfer of any security interest granted by the foreign company to the surviving or consolidated company (a) consent or approval to the transfer has been obtained, released or waived; (b) the transfer is permitted by and has been approved in accordance with the constitutional documents of the foreign company; and (c) the laws of the jurisdiction of the foreign company with respect to the transfer have been or will be complied with; (iii) that the foreign company will, upon the merger or consolidation becoming effective, cease to be incorporated, registered or exist under the laws of the relevant foreign jurisdiction; and (iv) that there is no other reason why it would be against the public interest to permit the merger or consolidation.

9

Where the above procedures are adopted, the Companies Act provides for a right of dissenting shareholders to be paid a payment of the fair value of his shares upon their dissenting to the merger or consolidation if they follow a prescribed procedure. In essence, that procedure is as follows (a) the shareholder must give his written objection to the merger or consolidation to the constituent company before the vote on the merger or consolidation, including a statement that the shareholder proposes to demand payment for his shares if the merger or consolidation is authorized by the vote; (b) within 20 days following the date on which the merger or consolidation is approved by the shareholders, the constituent company must give written notice to each shareholder who made a written objection; (c) a shareholder must within 20 days following receipt of such notice from the constituent company, give the constituent company a written notice of his intention to dissent including, among other details, a demand for payment of the fair value of his shares; (d) within seven days following the date of the expiration of the period set out in paragraph (b) above or seven days following the date on which the plan of merger or consolidation is filed, whichever is later, the constituent company, the surviving company or the consolidated company must make a written offer to each dissenting shareholder to purchase his shares at a price that the company determines is the fair value and if the company and the shareholder agree the price within 30 days following the date on which the offer was made, the company must pay the shareholder such amount; if the company and the shareholder fail to agree a price within such 30 day period, within 20 days following the date on which such 30 day period expires, the company (and any dissenting shareholder) must file a petition with the Cayman Islands Grand Court to determine the fair value and such petition must be accompanied by a list of the names and addresses of the dissenting shareholders with whom agreements as to the fair value of their shares have not been reached by the company. At the hearing of that petition, the court has the power to determine the fair value of the shares together with a fair rate of interest, if any, to be paid by the company upon the amount determined to be the fair value. Any dissenting shareholder whose name appears on the list filed by the company may participate fully in all proceedings until the determination of fair value is reached. These rights of a dissenting shareholder are not available in certain circumstances, for example, to dissenters holding shares of any class in respect of which an open market exists on a recognized stock exchange or recognized interdealer quotation system at the relevant date or where the consideration for such shares to be contributed are shares of any company listed on a national securities exchange or shares of the surviving or consolidated company.

Moreover, Cayman Islands law also has separate statutory provisions that facilitate the reconstruction or amalgamation of companies in certain circumstances, schemes of arrangement will generally be more suited for complex mergers or other transactions involving widely held companies, commonly referred to in the Cayman Islands as a “scheme of arrangement” which may be tantamount to a merger. In the event that a merger was sought pursuant to a scheme of arrangement (the procedure of which are more rigorous and take longer to complete than the procedures typically required to consummate a merger in the United States), the arrangement in question must be approved by a majority in number of each class of shareholders and creditors with whom the arrangement is to be made and who must in addition represent three-fourths in value of each such class of shareholders or creditors, as the case may be, that are present and voting either in person or by proxy at a meeting, or meeting summoned for that purpose. The convening of the meetings and subsequently the terms of the arrangement must be sanctioned by the Grand Court of the Cayman Islands. While a dissenting shareholder would have the right to express to the court the view that the transaction should not be approved, the court can be expected to approve the arrangement if it satisfies itself that:

| ● | we are not proposing to act illegally or beyond the scope of our corporate authority and the statutory provisions as to majority vote have been complied with; |

| ● | the shareholders have been fairly represented at the meeting in question; |

| ● | the arrangement is such as a businessman would reasonably approve; and |

| ● | the arrangement is not one that would more properly be sanctioned under some other provision of the Companies Act or that would amount to a “fraud on the minority.” |

If a scheme of arrangement or takeover offer (as described below) is approved, any dissenting shareholder would have no rights comparable to appraisal rights, which would otherwise ordinarily be available to dissenting shareholders of U.S. corporations, providing rights to receive payment in cash for the judicially determined value of the shares.

Squeeze-out Provisions.

When a takeover offer is made and accepted by holders of 90% of the shares to whom the offer relates within four months, the offeror may, within a two-month period, require the holders of the remaining shares to transfer such shares on the terms of the offer. An objection can be made to the Grand Court of the Cayman Islands but this is unlikely to succeed unless there is evidence of fraud, bad faith, collusion or inequitable treatment of the shareholders.

Further, transactions similar to a merger, reconstruction and/or an amalgamation may in some circumstances be achieved through other means to these statutory provisions, such as a share capital exchange, asset acquisition or control, through contractual arrangements, of an operating business.

10

Shareholders’ Suits.

Maples and Calder (Cayman ) LLP, our Cayman Islands legal counsel, is not aware of any reported class action having been brought in a Cayman Islands court. Derivative actions have been brought in the Cayman Islands courts, and the Cayman Islands courts have confirmed the availability for such actions. In most cases, we will be the proper plaintiff in any claim based on a breach of duty owed to us, and a claim against (for example) our officers or directors usually may not be brought by a shareholder. However, based both on Cayman Islands authorities and on English authorities, which would in all likelihood be of persuasive authority and be applied by a court in the Cayman Islands, exceptions to the foregoing principle apply in circumstances in which:

| ● | a company is acting, or proposing to act, illegally or beyond the scope of its authority; |

| ● | the act complained of, although not beyond the scope of the authority, could be effected if duly authorized by more than the number of votes which have actually been obtained; or |

| ● | those who control the company are perpetrating a “fraud on the minority.” |

A shareholder may have a direct right of action against us where the individual rights of that shareholder have been infringed or are about to be infringed.

Enforcement of civil liabilities.

The Cayman Islands has a different body of securities laws as compared to the United States and may provide less protection to investors. Additionally, Cayman Islands companies may not have standing to sue before the Federal courts of the United States.

We were advised by Maples and Calder (Cayman) LLP, our Cayman Islands legal counsel, that the courts of the Cayman Islands are unlikely (i) to recognize or enforce against us judgments of courts of the U.S. predicated upon the civil liability provisions of the federal securities laws of the U.S. or any state; and (ii) in original actions brought in the Cayman Islands, to impose liabilities against us predicated upon the civil liability provisions of the federal securities laws of the U.S. or any state, so far as the liabilities imposed by those provisions are penal in nature. In those circumstances, although there is no statutory enforcement in the Cayman Islands of judgments obtained in the U.S., the courts of the Cayman Islands will recognize and enforce a foreign money judgment of a foreign court of competent jurisdiction without retrial on the merits based on the principle that a judgment of a competent foreign court imposes upon the judgment debtor an obligation to pay the sum for which judgment has been given provided certain conditions are met. For a foreign judgment to be enforced in the Cayman Islands, such judgment must be final and conclusive and for a liquidated sum, and must not be in respect of taxes or a fine or penalty, inconsistent with a Cayman Islands judgment in respect of the same matter, impeachable on the grounds of fraud or obtained in a manner, and or be of a kind the enforcement of which is, contrary to natural justice or the public policy of the Cayman Islands (awards of punitive or multiple damages may well be held to be contrary to public policy). A Cayman Islands Court may stay enforcement proceedings if concurrent proceedings are being brought elsewhere.

11

Special Considerations for Exempted Companies.

We are an exempted company with limited liability under the Companies Act. The Companies Act distinguishes between ordinary resident companies and exempted companies. Any company that is registered in the Cayman Islands but conducts business mainly outside of the Cayman Islands may apply to be registered as an exempted company. The requirements for an exempted company are essentially the same as for an ordinary company except for the exemptions and privileges listed below:

| ● | annual reporting requirements are minimal and consist mainly of a statement that the company has conducted its operations mainly outside of the Cayman Islands and has complied with the provisions of the Companies Act; |

| ● | an exempted company’s register of members is not open to inspection; |

| ● | an exempted company does not have to hold an annual general meeting; |

| ● | an exempted company may issue negotiable or bearer shares or shares with no par value; |

| ● | an exempted company may obtain an undertaking against the imposition of any future taxation (such undertakings are usually given for 20 years in the first instance); |

| ● | an exempted company may register by way of continuation in another jurisdiction and be deregistered in the Cayman Islands; |

| ● | an exempted company may register as a limited duration company; and |

| ● | an exempted company may register as a segregated portfolio company. |

“Limited liability” means that the liability of each shareholder is limited to the amount unpaid by the shareholder on the shares of the company (except in exceptional circumstances, such as involving fraud, the establishment of an agency relationship or an illegal or improper purpose or other circumstances in which a court may be prepared to pierce or lift the corporate veil).

Vstock Transfer, LLC is the transfer agent and registrar for our Class A Shares and Class B Ordinary Shares. Its principal office is at 18 Lafayette Place, Woodmere, New York 11598.

The following summary of the material Cayman Islands, PRC and U.S. tax consequences of an investment in our Class A Shares is based upon laws and relevant interpretations thereof in effect as of the date hereof, all of which are subject to change, possibly with retroactive effect. This summary is not intended to be, nor should it be construed as, legal or tax advice and is not exhaustive of all possible tax considerations. This summary also does not deal with all possible tax consequences relating to an investment in our Class A Shares, such as the tax consequences under state, local, non-U.S., non-PRC, and non-Cayman Islands tax laws. Investors should consult their own tax advisors with respect to the tax consequences of the acquisition, ownership and disposition of our Class A Ordinary Shares.

People’s Republic of China Enterprise Taxation (the “EIT Law”)

The following brief description of Chinese enterprise laws is designed to highlight the enterprise-level taxation on our earnings, which will affect the amount of dividends, if any, we are ultimately able to pay to our shareholders.

We are a holding company incorporated in the Cayman Islands and we gain substantial income by way of dividends paid to us from our subsidiaries in China. The EIT Law and its implementation rules provide that China-sourced income of foreign companies, such as dividends paid by a PRC subsidiary to its equity holders that are non-resident companies, will normally be subject to PRC withholding tax at a rate of 10%, unless any such foreign investor’s jurisdiction of incorporation has a tax treaty with China that provides for a preferential tax rate or a tax exemption.

Under the EIT Law, an enterprise established outside of China with a “de facto management body” within China is considered a “resident enterprise,” which means that it is treated in a manner similar to a Chinese enterprise for enterprise income tax purposes. Although the implementation rules of the EIT Law define “de facto management body” as a managing body that actually, comprehensively manage and control the production and operation, staff, accounting, property and other aspects of an enterprise, the only official guidance for this definition currently available is set forth in SAT Notice 82, which provides guidance on the determination of the tax residence status of a Chinese-controlled offshore incorporated enterprise, defined as an enterprise that is incorporated under the laws of a foreign country or territory and that has a PRC enterprise or enterprise group as its primary controlling shareholder. Although we do not have a PRC enterprise or enterprise group as our primary controlling shareholder and are therefore not a Chinese-controlled offshore incorporated enterprise within the meaning of SAT Notice 82, in the absence of guidance specifically applicable to us, we have applied the guidance set forth in SAT Notice 82 to evaluate the tax residence status of the Company and its subsidiaries organized outside the PRC.

12

According to SAT Notice 82, a Chinese-controlled offshore incorporated enterprise will be regarded as a PRC tax resident by virtue of having a “de facto management body” in China and will be subject to PRC enterprise income tax on its worldwide income only if all of the following criteria are met: (i) the places where senior management and senior management departments that are responsible for daily production, operation and management of the enterprise perform their duties are mainly located within the territory of China; (ii) financial decisions (such as money borrowing, lending, financing and financial risk management) and personnel decisions (such as appointment, dismissal and salary and wages) are decided or need to be decided by organizations or persons located within the territory of China; (iii) main property, accounting books, corporate seal, the board of directors and files of the minutes of shareholders’ meetings of the enterprise are located or preserved within the territory of China; and (iv) one half (or more) of the directors or senior management staff having the right to vote habitually reside within the territory of China.

We believe we do not meet some of the conditions outlined in the immediately preceding paragraph. For example, as a holding company, the key assets and records of our company including the resolutions and meeting minutes of our board of directors and the resolutions and meeting minutes of our shareholders, are located and maintained outside the PRC. In addition, we are not aware of any offshore holding companies with a corporate structure similar to ours that has been deemed a PRC “resident enterprise” by the PRC tax authorities. Accordingly, we believe we and our offshore subsidiaries should not be treated as a “resident enterprise” for PRC tax purposes if the criteria for “de facto management body” as set forth in SAT Notice 82 were deemed applicable to us. However, as the tax residency status of an enterprise is subject to determination by the PRC tax authorities and uncertainties remain with respect to the interpretation of the term “de facto management body” as applicable to our offshore entities, we will continue to monitor our tax status.

The implementation rules of the EIT Law provide that, (i) if the enterprise that distributes dividends is domiciled in the PRC or (ii) if gains are realized from transferring equity interests of companies domiciled in the PRC, then such dividends or gains are treated as China-sourced income. It is not clear how “domicile” may be interpreted under the EIT Law, and it may be interpreted as the jurisdiction where the enterprise is a tax resident. Therefore, if we are considered as a PRC tax resident enterprise for PRC tax purposes, any dividends we pay to our overseas shareholders which are non-resident companies as well as gains realized by such shareholders from the transfer of our shares may be regarded as China-sourced income and as a result become subject to PRC withholding tax of up to 10%. We are unable to provide a “will” opinion because Jingtian & Gongcheng, our PRC counsel, believes it is possible but unlikely the Company and its offshore subsidiaries would be treated as a “resident enterprise” for PRC tax purposes because they do not meet some of the conditions outlined in SAT Notice 82. In addition, we are not aware of any offshore holding companies with a corporate structure similar to ours that has been deemed a PRC “resident enterprise” by the PRC tax authorities as of the date of this annual report. Therefore, it is possible but highly unlikely that the income received by our overseas shareholders will be regarded as China-sourced income.

Cayman Islands Tax Considerations

The following is a discussion on certain Cayman Islands income tax consequences of an investment in the securities of the Company. The discussion is a general summary of present law, which is subject to prospective and retroactive change. It is not intended as tax advice, does not consider any investor’s particular circumstances, and does not consider tax consequences other than those arising under Cayman Islands law.

13

Under Existing Cayman Islands Laws:

Payments of dividends and capital in respect of our securities will not be subject to taxation in the Cayman Islands and no withholding will be required on the payment of a dividend or capital to any holder of the securities nor will gains derived from the disposal of the securities be subject to Cayman Islands income or corporation tax. The Cayman Islands currently have no income, corporate or capital gains tax and no estate duty, inheritance tax or gift tax.

No stamp duty is payable in respect of the issue of the warrants. An instrument of transfer in respect of a warrant is stampable if executed in or brought into the Cayman Islands.

No stamp duty is payable in respect of the issue of our Class A Shares or on an instrument of transfer in respect of such shares.

The Company has been incorporated under the laws of the Cayman Islands as an exempted company with limited liability and, as such, has applied for and received an undertaking from the Financial Secretary of the Cayman Islands in the following form:

The Tax Concessions Act (As Revised)

Undertaking as to Tax Concessions

In accordance with the provision of Section 6 of The Tax Concessions Act (As Revised), the Financial Secretary undertakes with the Company:

| 1. | That no law which is hereafter enacted in the Islands imposing any tax to be levied on profits, income, gains or appreciations shall apply to the Company or its operations; and |

| 2. | In addition, that no tax to be levied on profits, income, gains or appreciations or which is in the nature of estate duty or inheritance tax shall be payable: |

| a. | On or in respect of the shares, debentures or other obligations of the Company; or |

| b. | by way of the withholding in whole or part, of any relevant payment as defined in Section 6(3) of the Tax Concessions Act (As Revised). |

These concessions shall be for a period of twenty years from the date hereof.

United States Federal Income Taxation

The following does not address the tax consequences to any particular investor or to persons in special tax situations such as:

| ● | banks; | |

| ● | financial institutions; | |

| ● | insurance companies; | |

| ● | regulated investment companies; |

| ● | real estate investment trusts; |

14

| ● | broker-dealers; | |

| ● | traders that elect to mark-to-market; | |

| ● | U.S. expatriates; | |

| ● | tax-exempt entities; | |

| ● | persons liable for alternative minimum tax; | |

| ● | persons holding our Class A Shares as part of a straddle, hedging, conversion or integrated transaction; | |

| ● | persons that actually or constructively own 10% or more of our voting shares; | |

| ● | persons who acquired our Class A Shares pursuant to the exercise of any employee share option or otherwise as consideration; or | |

| ● | persons holding our Class A Shares through partnerships or other pass-through entities. |

Prospective purchasers are urged to consult their own tax advisors about the application of the U.S. Federal tax rules to their particular circumstances as well as the state, local, foreign and other tax consequences to them of the purchase, ownership and disposition of our Class A Shares.

Taxation of Dividends and Other Distributions on our Class A Ordinary Shares

Subject to the passive foreign investment company rules discussed below, the gross amount of distributions made by us to you with respect to the Class A Shares (including the amount of any taxes withheld therefrom) will generally be includable in your gross income as dividend income on the date of receipt by you, but only to the extent that the distribution is paid out of our current or accumulated earnings and profits (as determined under U.S. federal income tax principles). With respect to corporate U.S. Holders, the dividends will not be eligible for the dividends-received deduction allowed to corporations in respect of dividends received from other U.S. corporations.

With respect to non-corporate U.S. Holders, including individual U.S. Holders, dividends will be taxed at the lower capital gains rate applicable to qualified dividend income, provided that (1) the Class A Shares are readily tradable on an established securities market in the U.S., or we are eligible for the benefits of an approved qualifying income tax treaty with the U.S. that includes an exchange of information program, (2) we are not a passive foreign investment company (as discussed below) for either our taxable year in which the dividend is paid or the preceding taxable year, and (3) certain holding period requirements are met. Under U.S. Internal Revenue Service authority, Class A Shares are considered for purpose of clause (1) above to be readily tradable on an established securities market in the U.S. because they are listed on the Nasdaq Capital Market. You are urged to consult your tax advisors regarding the availability of the lower rate for dividends paid with respect to our Class A Shares, including the effects of any change in law after the date of this annual report.

Dividends will constitute foreign source income for foreign tax credit limitation purposes. If the dividends are taxed as qualified dividend income (as discussed above), the amount of the dividend taken into account for purposes of calculating the foreign tax credit limitation will be limited to the gross amount of the dividend, multiplied by the reduced rate divided by the highest rate of tax normally applicable to dividends. The limitation on foreign taxes eligible for credit is calculated separately with respect to specific classes of income. For this purpose, dividends distributed by us with respect to our Class A Shares will constitute “passive category income” but could, in the case of certain U.S. Holders, constitute “general category income.”

For the year ended December 31, 2023, we have not declared any dividends on our Class A Ordinary Shares or Class B Ordinary Shares. To the extent the distribution exceeds our current and accumulated earnings and profits (as determined under U.S. federal income tax principles), it will be treated first as a tax-free return of your tax basis in your Class A Shares, and to the extent the distribution exceeds your tax basis, the excess will be taxed as capital gain. We do not intend to calculate our earnings and profits under U.S. federal income tax principles. Therefore, a U.S. Holder should expect that a distribution will be treated as a dividend even if that distribution would otherwise be treated as a non-taxable return of capital or as capital gain under the rules described above.

15

Taxation of Dispositions of Class A Shares

Subject to the passive foreign investment company (“PFIC”) rules discussed below, you will recognize taxable gain or loss on any sale, exchange or other taxable disposition of a share equal to the difference between the amount realized (in U.S. dollars) for the share and your tax basis (in U.S. dollars) in the Class A Shares. The gain or loss will be capital gain or loss. If you are a non-corporate U.S. Holder, including an individual U.S. Holder, who has held the Class A Shares for more than one year, you will be eligible for (a) reduced tax rates of 0% (for individuals in the 10% or 15% tax brackets), (b) higher tax rates of 20% (for individuals in the 39.6% tax bracket) or (c) 15% for all other individuals. The deductibility of capital losses is subject to limitations. Any such gain or loss that you recognize will generally be treated as United States source income or loss for foreign tax credit limitation purposes.

Passive Foreign Investment Company (PFIC) Consequences

Based on our current and anticipated operations and the composition of our assets, we do not expect to be treated as a PFIC for U.S. federal income tax purposes for our current taxable year. PFIC status is a factual determination for each taxable year which cannot be made until the close of the taxable year. A non-U.S. corporation is considered a PFIC for any taxable year if either:

| ● | at least 75% of its gross income is passive income; or | |

| ● | at least 50% of the value of its assets (based on an average of the quarterly values of the assets during a taxable year) is attributable to assets that produce or are held for the production of passive income (the “asset test”). |

We will be treated as owning our proportionate share of the assets and earning our proportionate share of the income of any other corporation in which we own, directly or indirectly, at least 25% (by value) of the stock.

We must make a separate determination each year as to whether we are a PFIC. As a result, our PFIC status may change from no to yes. In particular, because the value of our assets for purposes of the asset test will generally be determined based on the market price of our Class A Shares, our PFIC status will depend in large part on the market price of our Class A Shares. Accordingly, fluctuations in the market price of the Class A Shares may cause us to become a PFIC. In addition, the application of the PFIC rules is subject to uncertainty in several respects and the composition of our income and assets will be affected by how, and how quickly, we spend the cash we raise in our initial public offering. If we are a PFIC for any year during which you hold Class A Shares, we will continue to be treated as a PFIC for all succeeding years during which you hold Class A Shares. However, if we cease to be a PFIC, you may avoid some of the adverse effects of the PFIC regime by making a “deemed sale” election with respect to the Class A Shares.

If we are a PFIC for any taxable year during which you hold Class A Shares, you will be subject to special tax rules with respect to any “excess distribution” that you receive and any gain you realize from a sale or other disposition (including a pledge) of the Class A Shares, unless you make a “mark-to-market” election as discussed below. Distributions you receive in a taxable year that are greater than 125% of the average annual distributions you received during the shorter of the three preceding taxable years or your holding period for the Class A Shares will be treated as an excess distribution. Under these special tax rules:

| ● | the excess distribution or gain will be allocated ratably over your holding period for the Class A Shares; |

| ● | the amount allocated to the current taxable year, and any taxable year prior to the first taxable year in which we were a PFIC, will be treated as ordinary income, and |

| ● | the amount allocated to each other year will be subject to the highest tax rate in effect for that year and the interest charge generally applicable to underpayments of tax will be imposed on the resulting tax attributable to each such year. |

16

The tax liability for amounts allocated to years prior to the year of disposition or “excess distribution” cannot be offset by any net operating losses for such years, and gains (but not losses) realized on the sale of the Class A Shares cannot be treated as capital, even if you hold the Class A Shares as capital assets.