We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Share Name | Share Symbol | Market | Type |

|---|---|---|---|

| California BanCorp | NASDAQ:CALB | NASDAQ | Common Stock |

| Price Change | % Change | Share Price | Bid Price | Offer Price | High Price | Low Price | Open Price | Shares Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0.00 | 0.00% | 22.13 | 8.86 | 25.47 | 0 | 13:00:19 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported):

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation) |

(Commission File Number) |

(IRS Employer Identification Number) |

| (Address of Principal Executive Offices) | (Zip Code) |

(Registrant’s Telephone Number, Including Area Code)

N/A

(Former name or former address, if changed since last report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading |

Name of each exchange on | ||

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

| Item 2.02 | Results of Operations and Financial Condition |

On January 30, 2024, California BanCorp (the “Company”) issued a press release setting forth its unaudited financial results for the quarter and twelve months ended December 31, 2023. A copy of the Company’s press release is furnished as Exhibit 99.1 and is hereby incorporated by reference.

| Item 7.01 | Regulation FD Disclosure. |

Over the upcoming weeks, members of management will be presenting to or conducting one-on-one meetings with investors, analysts or other third parties about the Company and its latest financial results. A copy of the presentation slides, updated with the Company’s financial results for the fourth quarter and twelve months ended December 31, 2023, substantially in the form expected to be used in such presentations and meetings, is attached hereto as Exhibit 99.2 and is incorporated herein by reference.

The information furnished under this Item 2.02 and Item 7.01 and the related Exhibits 99.1 and 99.2 of this Current Report on Form 8-K shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to liabilities under that Section, nor shall it be deemed incorporated by reference in any registration statement or other filings of the Company under the Securities Act of 1933, as amended (the “Securities Act”) or the Exchange Act, except as shall be set forth by specific reference in such filing.

| Item 9.01 | Financial Statements and Exhibits |

| Exhibit |

Description | |

| 99.1 | Press Release dated January 30, 2024 | |

| 99.2 | Investor Presentation dated December 31, 2023 | |

| 104 | Cover Page Interactive Date File (embedded within the Inline XBRL document) | |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| CALIFORNIA BANCORP | ||||||

| Date: January 30, 2024 | By: | /s/ THOMAS A. SA | ||||

| Thomas A. Sa President, Chief Financial Officer and Chief Operating Officer | ||||||

Exhibit 99.1

California BanCorp Reports Financial Results for the Fourth Quarter and Twelve Months Ended December 31, 2023

Oakland, CA – January 30, 2024 – California BanCorp (NASDAQ: CALB) (the “Company”), whose subsidiary is California Bank of Commerce, announced today its financial results for the fourth quarter and twelve months ended December 31, 2023.

The Company reported net income of $5.3 million for the fourth quarter of 2023, compared to $5.4 million for the third quarter of 2023 and $7.7 million for the fourth quarter of 2022. For the twelve months ended December 31, 2023, net income was $21.6 million, representing an increase of $525,000, or 2%, compared to $21.1 million for the same period in 2022.

Diluted earnings per share were $0.63 for the fourth quarter of 2023, compared to $0.64 for the third quarter of 2023 and $0.91 for the fourth quarter of 2022. For the twelve months ended December 31, 2023, diluted earnings per share were $2.56, compared to $2.51 for the same period in 2022.

“Despite a challenging year for the banking industry, we generated a record level of earnings in 2023, which reflects the strength of the franchise we have built and our ability to perform well in a variety of economic conditions,” said Steven Shelton, Chief Executive Officer of California BanCorp. “While maintaining our conservative approach to new loan production and prudent balance sheet management, we continued to deliver strong financial performance in the fourth quarter with our return on assets remaining above 1%. As expected, our balance sheet remained relatively flat with the prior quarter, although we continue to have success in adding new full banking relationships that provide operating deposit accounts that have helped to offset seasonal outflows from existing clients and high-quality commercial lending opportunities that have offset the level of payoffs that we are seeing in the portfolio.

“Given the strength of our balance sheet, with a high level of capital, liquidity, and reserves, along with a conservatively underwritten loan portfolio, we believe we are well positioned to continue delivering strong financial performance in 2024 even if the macroeconomic environment remains challenging. As the banking industry has stabilized, we are seeing more businesses looking to move their deposit relationships from the larger banks to a smaller commercial bank that provides a higher level of responsiveness and service. This is creating opportunities for us to add attractive new client relationships given the strong balance sheet, robust treasury management solutions, and superior level of service that we can provide. We have a strong deposit pipeline that we believe should result in continued growth in our client roster during 2024, further improvement in our level of profitability in the years ahead, and an increase in the value of our franchise,” said Mr. Shelton.

-1-

Financial Highlights:

Profitability - three months ended December 31, 2023 compared to September 30, 2023

| • | Net income of $5.3 million and $0.63 per diluted share, compared to $5.4 million and $0.64 per diluted share, respectively. |

| • | Revenue was $19.9 million for both the fourth and third quarters of 2023. |

| • | Net interest income was $18.6 million for both the fourth and third quarters of 2023. |

| • | Provision for credit losses of $181,000 decreased $133,000, or 42%, from $314,000 for the third quarter of 2023. |

| • | Non-interest income was $1.3 million for both the fourth and third quarters of 2023. |

| • | Non-interest expense, excluding capitalized loan origination costs, of $13.0 million increased $523,000, or 4%, compared to $12.5 million for the third quarter of 2023. |

Profitability - twelve months ended December 31, 2023 compared to December 31, 2022

| • | Net income of $21.6 million and $2.56 per diluted share, compared to $21.1 million and $2.51 per diluted share, respectively. |

| • | Revenue of $79.4 million increased $1.1 million, or 1%, compared to $78.3 million in the prior year. |

| • | Net interest income of $74.6 million increased $3.6 million, or 5%, compared to $71.0 million for the same period in the prior year. |

| • | Provision for credit losses of $1.3 million decreased $2.5 million, or 66%, from $3.8 million for the twelve months ended December 31, 2022. |

| • | Non-interest income of $4.9 million decreased $2.5 million, or 34%, from $7.4 million for the same period in the prior year. |

| • | Non-interest expense, excluding capitalized loan origination costs, of $50.4 million decreased $1.6 million, or 3%, compared to $48.8 million for the twelve months ended December 31, 2022. |

Financial Position – December 31, 2023 compared to September 30, 2023

| • | Total assets increased by $2.0 million, or 0%, to $1.99 billion. |

| • | Total gross loans decreased by $13.6 million, or 1%, to $1.56 billion; average total gross loans increased by $20.3 million to $1.57 billion. |

| • | Total deposits decreased by $81.8 million, or 5%, to $1.63 billion; average total deposits decreased by $18.8 million to $1.70 billion. |

| • | Other borrowings were $75.0 million at December 31, 2023 compared to no balances outstanding at September 30, 2023. |

| • | Capital ratios remain healthy with a tier I leverage ratio of 9.61%, tier I capital ratio of 9.53% and total risk-based capital ratio of 13.16%. |

| • | Book value per share of $23.38 increased by $0.74, or 3%. |

| • | Tangible book value per share of $22.50 increased by $0.74, or 3%. |

-2-

Net Interest Income and Margin:

Net interest income for the quarters ended December 31, 2023 and September 30, 2023 was $18.6 million, compared to $21.9 million for the three months ended December 31, 2022. Net interest income for the twelve months ended December 31, 2023 was $74.6 million, an increase of $3.6 million, or 5% over $71.0 million for the twelve months ended December 31, 2022. The decrease in net interest income for the quarters ended December 31, 2023 and September 30, 2023 compared to the fourth quarter of 2022 was primarily due to an increase in the cost of interest-bearing deposits. The increase in net interest income for the year ended December 31, 2023 compared to the year ended December 31, 2022 was primarily attributable to an increase in interest income as the result of a more favorable mix of earning assets combined with higher yields on those assets.

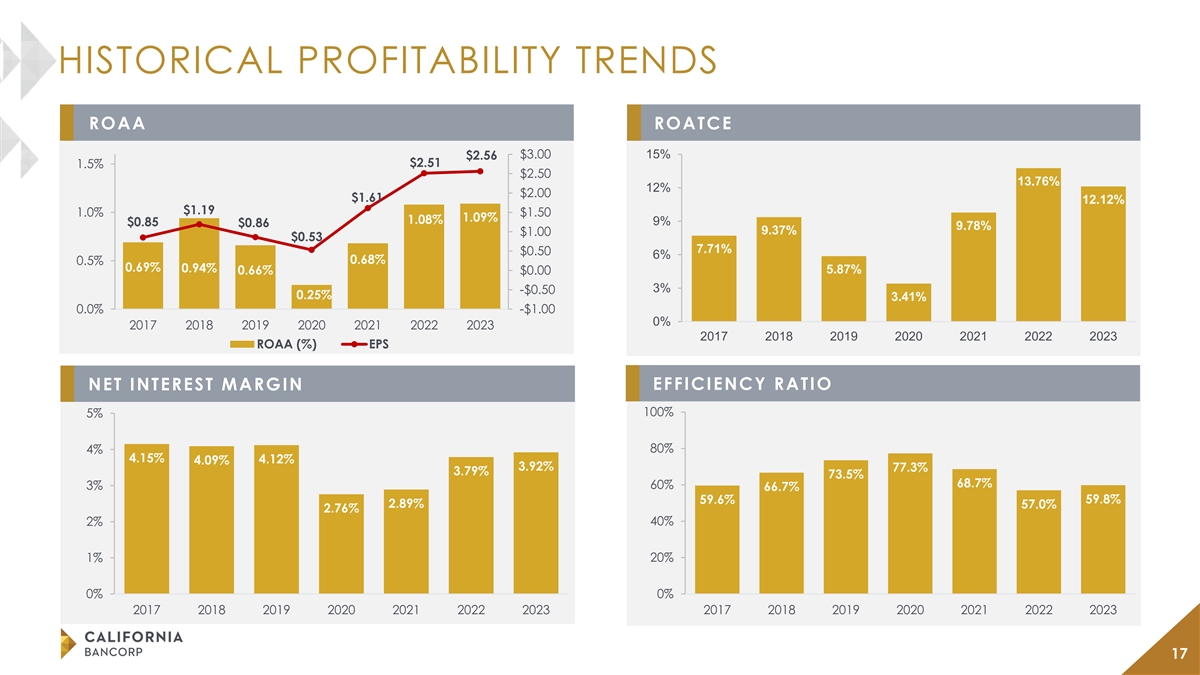

The Company’s net interest margin for the fourth quarter of 2023 was 3.88%, compared to 3.86% for the third quarter of 2023 and 4.32% for the same period in 2022. The decrease in margin from the same period last year was primarily the result of an increase in the cost of deposits, partially offset by a more favorable mix of earning assets with higher yields.

The Company’s net interest margin for the twelve months ended December 31, 2023 was 3.92% compared to 3.79% for the same period in 2022. The increase in margin compared to prior year was primarily due to loan growth and increased yields on earnings assets, partially offset by an increase in the cost of deposits and other borrowings.

Non-Interest Income:

The Company’s non-interest income for the quarters ended December 31, 2023, September 30, 2023, and December 31, 2022 was $1.3 million, $1.3 million and $2.0 million, respectively. For the twelve months ended December 31, 2023, non-interest income of $4.9 million compared to $7.4 million for the same period of 2022. The decrease in non-interest income from prior year was the result of a decrease in service charges and loan related fees combined with a $1.4 million gain recognized in the first quarter of 2022 on the sale of a portion of our solar loan portfolio.

Net interest income and non-interest income comprised total revenue of $19.9 million, $19.9 million, and $23.8 million for the quarters ended December 31, 2023, September 30, 2023, and December 31, 2022, respectively. Total revenue for the twelve months ended December 31, 2023 and 2022 was $79.4 million and $78.3 million, respectively.

Non-Interest Expense:

The Company’s non-interest expense for the quarters ended December 31, 2023, September 30, 2023, and December 31, 2022 was $12.2 million, $11.9 million, and $11.7 million, respectively. The increase in non-interest expense from the third quarter of 2023 and fourth quarter of 2022 was primarily due to an increase in salaries and benefits combined with an increase in premises and equipment, partially offset by a decrease in data processing expense. Excluding capitalized loan origination costs, non-interest expense for the fourth quarter of 2023, the third quarter of 2023 and the fourth quarter of 2022 was $13.0 million, $12.5 million, and $12.7 million, respectively.

Non-interest expense of $47.5 million for the twelve months ended December 31, 2023 increased by $2.8 million, or 6%, compared to $44.7 million for the same period of 2022. Excluding capitalized loan origination costs, non-interest expense was $50.4 million for the twelve months ended December 31, 2023 and $48.8 million for the same period in 2022 which reflects investment in infrastructure to support the growth of the Company.

-3-

The Company’s efficiency ratio, the ratio of non-interest expense to revenues, was 61.36%, 59.64%, and 49.17% for the quarters ended December 31, 2023, September 30, 2023, and December 31, 2022, respectively. For the twelve months ended December 31, 2023 and 2022, the Company’s efficiency ratio was 59.82% and 57.01%, respectively.

Balance Sheet:

Total assets of $1.99 billion as of December 31, 2023, represented an increase of $2.0 million, or 0%, compared to $1.98 billion at September 30, 2023 and a decrease of $56.3 million, or 3%, compared to $2.04 billion at December 31, 2022. Compared to the same period in the prior year, total assets decreased primarily due to conservative new loan production during 2023 and decreased liquidity as a result of a reduction in total deposits, partially offset by an increase in short-term borrowings.

Total gross loans decreased by $13.6 million, or 1%, to $1.56 billion at December 31, 2023, from $1.57 billion at September 30, 2023 and decreased by $33.9 million, or 2%, compared to $1.59 billion at December 31, 2022. During the fourth quarter of 2023, the reduction in gross loans was primarily the result of commercial loans decreasing by $16.6 million, or 1%, partially offset by an increase in construction and land loans of $4.2 million, or 10%. Compared to the same period in the prior year, the reduction in gross loans was primarily the result of construction and land loans decreasing by $19.5 million, or 31%, due to the completion of a large construction project.

Total deposits decreased by $81.8 million, or 5%, to $1.63 billion at December 31, 2023 from $1.71 billion at September 30, 2023, and decreased by $166.5 million, or 9%, from $1.79 billion at December 31, 2022. The decrease in total deposits from the end of the third quarter of 2023 was primarily due to a decrease in demand deposits of $31.2 million, or 4%, a decrease in money market and savings accounts of $41.1 million, of 6%, and a decrease in time deposits of $9.5 million, or 3%. Noninterest-bearing deposits, primarily commercial business operating accounts, represented 40.4% of total deposits at December 31, 2023, compared to 40.2% at September 30, 2023 and 45.3% at December 31, 2022.

At December 31, 2023, the Company had $75.0 million in outstanding borrowings, excluding junior subordinated debt securities, compared to no outstanding borrowings at September 30, 2023 and December 31, 2022.

Asset Quality:

The provision for credit losses on loans decreased to $87,000 for the fourth quarter of 2023 compared to $121,000 for the third quarter of 2023, and $1.1 million for the fourth quarter of 2022. The Company had loan recoveries of $20,000 during the fourth quarter of 2023, loan charge-offs of $156,000 and recoveries of $234,000 during the third quarter of 2023, and loan charge-offs of $650,000 and no recoveries during the fourth quarter of 2022.

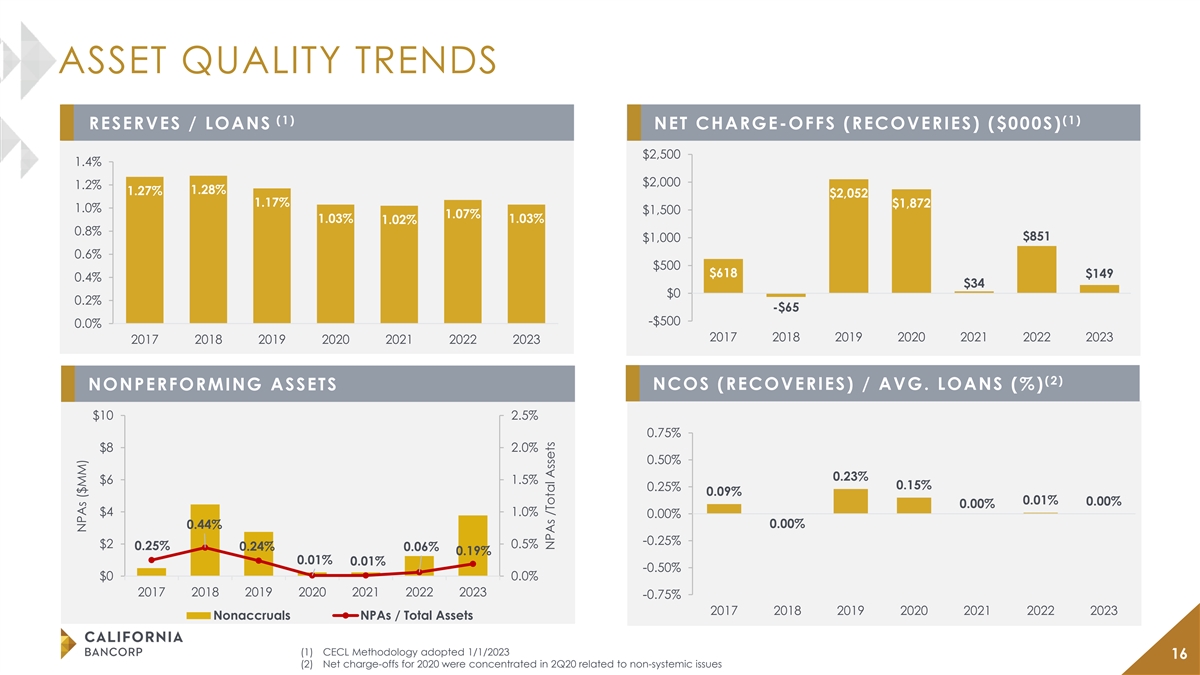

Non-performing assets (“NPAs”) to total assets were 0.19% at December 31, 2023, 0.06% at September 30, 2023 and 0.06% at December 31, 2022, with non-performing loans of $3.8 million, $1.2 million and $1.3 million, respectively, on those dates. The increase in non-performing loans during the fourth quarter of 2023 was due to one loan relationship within our commercial portfolio. The borrower is currently in the process of liquidating its assets and the Company does not anticipate a loss associated with this loan as of December 31, 2023.

-4-

The allowance for credit losses on loans increased by $107,000 to $16.0 million, or 1.03% of total loans, at December 31, 2023, compared to $15.9 million, or 1.01% of total loans, at September 30, 2023 and $17.0 million, or 1.07% of total loans, at December 31, 2022. On January 1, 2023, the Company adopted the new current expected credit losses (CECL) standard. The Company’s allowance for credit losses on loans was 0.95% upon adoption on January 1, 2023 compared to 1.07% at December 31, 2022.

The allowance for credit losses on unfunded loan commitments increased by $120,000 to $2.2 million, or 0.32% of total unfunded loan commitments, at December 31, 2023, compared to $2.1 million, or 0.32% of total unfunded loan commitments, at September 30, 2023 and $430,000, or 0.07% of total unfunded loan commitments at December 31, 2022. The Company’s allowance for credit losses on unfunded loan commitments was 0.28% upon the adoption of CECL on January 1, 2023 compared to 0.07% at December 31, 2022.

Capital Adequacy:

At December 31, 2023, shareholders’ equity totaled $196.5 million compared to $190.1 million at September 30, 2023 and $172.3 million one year ago. As a result, the Company’s total risk-based capital ratio, tier I capital ratio and tier I leverage ratio of 13.16%, 9.53%, and 9.61%, respectively, were all above the regulatory standards for “well-capitalized” institutions of 10.00%, 8.00% and 5.00% respectively.

“With our strong financial performance and prudent balance sheet management, we continued to increase our capital ratios and tangible book value per share, and during 2023, our tangible book value per share increased 14%,” said Thomas A. Sa, President, Chief Financial Officer and Chief Operating Officer of California BanCorp. “With our high level of capital, we are well positioned to continue growing our franchise and creating long-term value for shareholders.”

About California BanCorp:

California BanCorp, the parent company for California Bank of Commerce, offers a broad range of commercial banking services to closely held businesses and professionals located throughout Northern California. The Company’s common stock trades on the Nasdaq Global Select marketplace under the symbol CALB. For more information on California BanCorp, please visit our website at www.californiabankofcommerce.com.

Contacts:

Steven E. Shelton, (510) 457-3751

Chief Executive Officer

seshelton@bankcbc.com

Thomas A. Sa, (510) 457-3775

President, Chief Financial Officer and Chief Operating Officer

tsa@bankcbc.com

-5-

Use of Non-GAAP Financial Information:

This press release contains both financial measures based on GAAP and non-GAAP. Non-GAAP financial measures are used where management believes them to be helpful in understanding the Company’s results of operations or financial position. Where non-GAAP financial measures are used, the comparable GAAP financial measure can be found in this press release, and a reconciliation to the comparable GAAP financial measure is provided on the final page of this press release. These disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies.

Forward-Looking Statements:

Statements in this news release regarding expectations and beliefs about future financial performance and financial condition, as well as trends in the Company’s business and markets are “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements often include words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” “project,” “outlook,” or words of similar meaning, or future or conditional verbs such as “will,” “would,” “should,” “could,” or “may.” The forward-looking statements in this news release are based on current information and on assumptions that the Company makes about future events and circumstances that are subject to a number of risks and uncertainties that are often difficult to predict and beyond the Company’s control. As a result of those risks and uncertainties, the Company’s actual future performance or financial results could differ, possibly materially, from those expressed in or implied by the forward-looking statements contained in this news release and could cause the Company to make changes to future plans. Those risks and uncertainties include, but are not limited to, the risk of incurring loan losses, which is an inherent risk of the banking business; the risk that the Company will not be able to continue its internal growth rate; the risk that the United States economy will experience slowed growth or recession or will be adversely affected by domestic or international economic conditions and risks associated with the Federal Reserve Board taking actions with respect to interest rates, any of which could adversely affect, among other things, the values of real estate collateral supporting many of the Company’s loans, interest income and interest rate margins and, therefore, the Company’s future operating results; the impacts of the failure of other depository institutions on investor and depositor sentiments and preferences; the Company’s ability to manage its liquidity; risks associated with changes in income tax laws and regulations; and risks associated with seeking new client relationships and maintaining existing client relationships. Readers of this news release are encouraged to review the additional information regarding these and other risks and uncertainties to which our business is subject that are contained in our Annual Report on Form 10-K for the year ended December 31, 2022 which is on file with the Securities and Exchange Commission (the “SEC”). Additional information will be set forth in our Annual Report on Form 10-K for the year ended December 31, 2023, which we expect to file with the SEC during the first quarter of 2024, and readers of this release are urged to review the additional information that will be contained in that report.

Due to these and other possible uncertainties and risks, readers are cautioned not to place undue reliance on the forward-looking statements contained in this news release, which speak only as of today’s date, or to make predictions based solely on historical financial performance. The Company disclaims any obligation to update forward-looking statements contained in this news release, whether as a result of new information, future events or otherwise, except as may be required by law.

-6-

FINANCIAL TABLES FOLLOW

-7-

CALIFORNIA BANCORP AND SUBSIDIARY

SELECTED FINANCIAL INFORMATION (UNAUDITED)—PROFITABILITY

(Dollars in Thousands, Except Per Share Data)

| Change | Change | |||||||||||||||||||||||||||||||

| QUARTERLY HIGHLIGHTS: | Q4 2023 | Q3 2023 | $ | % | Q4 2022 | $ | % | |||||||||||||||||||||||||

| Interest income |

$ | 28,405 | $ | 28,094 | $ | 311 | 1 | % | $ | 27,480 | $ | 925 | 3 | % | ||||||||||||||||||

| Interest expense |

9,831 | 9,516 | 315 | 3 | % | 5,620 | 4,211 | 75 | % | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Net interest income |

18,574 | 18,578 | (4 | ) | 0 | % | 21,860 | (3,286 | ) | -15 | % | |||||||||||||||||||||

| Provision for credit losses |

181 | 314 | (133 | ) | -42 | % | 1,100 | (919 | ) | -84 | % | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Net interest income after provision for credit losses |

18,393 | 18,264 | 129 | 1 | % | 20,760 | (2,367 | ) | -11 | % | ||||||||||||||||||||||

| Non-interest income |

1,339 | 1,294 | 45 | 3 | % | 1,962 | (623 | ) | -32 | % | ||||||||||||||||||||||

| Non-interest expense |

12,218 | 11,851 | 367 | 3 | % | 11,713 | 505 | 4 | % | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Income before income taxes |

7,514 | 7,707 | (193 | ) | -3 | % | 11,009 | (3,495 | ) | -32 | % | |||||||||||||||||||||

| Income tax expense |

2,173 | 2,306 | (133 | ) | -6 | % | 3,340 | (1,167 | ) | -35 | % | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Net income |

$ | 5,341 | $ | 5,401 | $ | (60 | ) | -1 | % | $ | 7,669 | $ | (2,328 | ) | -30 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Diluted earnings per share |

$ | 0.63 | $ | 0.64 | $ | (0.01 | ) | -2 | % | $ | 0.91 | $ | (0.28 | ) | -31 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Net interest margin |

3.88 | % | 3.86 | % | +2 Basis Points | 4.32 | % | -44 Basis Points | ||||||||||||||||||||||||

| Efficiency ratio |

61.36 | % | 59.64 | % | +172 Basis Points | 49.17 | % | +1219 Basis Points | ||||||||||||||||||||||||

| Change | ||||||||||||||||

| YEAR-TO-DATE HIGHLIGHTS: | 2023 | 2022 | $ | % | ||||||||||||

| Interest income |

$ | 109,210 | $ | 82,278 | $ | 26,932 | 33 | % | ||||||||

| Interest expense |

34,655 | 11,306 | 23,349 | 207 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net interest income |

74,555 | 70,972 | 3,583 | 5 | % | |||||||||||

| Provision for credit losses |

1,297 | 3,775 | (2,478 | ) | -66 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net interest income after provision for credit losses |

73,258 | 67,197 | 6,061 | 9 | % | |||||||||||

| Non-interest income |

4,875 | 7,374 | (2,499 | ) | -34 | % | ||||||||||

| Non-interest expense |

47,515 | 44,665 | 2,850 | 6 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income before income taxes |

30,618 | 29,906 | 712 | 2 | % | |||||||||||

| Income tax expense |

8,985 | 8,798 | 187 | 2 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

$ | 21,633 | $ | 21,108 | $ | 525 | 2 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted earnings per share |

$ | 2.56 | $ | 2.51 | $ | 0.05 | 2 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net interest margin |

3.92 | % | 3.79 | % | +13 Basis Points | |||||||||||

| Efficiency ratio |

59.82 | % | 57.01 | % | +281 Basis Points | |||||||||||

-8-

CALIFORNIA BANCORP AND SUBSIDIARY

SELECTED FINANCIAL INFORMATION (UNAUDITED)—FINANCIAL POSITION

(Dollars in Thousands, Except Per Share Data)

| Change | Change | |||||||||||||||||||||||||||||||

| PERIOD-END HIGHLIGHTS: | Q4 2023 | Q3 2023 | $ | % | Q4 2022 | $ | % | |||||||||||||||||||||||||

| Total assets |

$ | 1,985,905 | $ | 1,983,917 | $ | 1,988 | 0 | % | $ | 2,042,215 | $ | (56,310 | ) | -3 | % | |||||||||||||||||

| Gross loans |

1,559,533 | 1,573,115 | (13,582 | ) | -1 | % | 1,593,421 | (33,888 | ) | -2 | % | |||||||||||||||||||||

| Deposits |

1,625,244 | 1,707,081 | (81,837 | ) | -5 | % | 1,791,740 | (166,496 | ) | -9 | % | |||||||||||||||||||||

| Tangible equity |

189,029 | 182,673 | 6,356 | 3 | % | 164,782 | 24,247 | 15 | % | |||||||||||||||||||||||

| Tangible book value per share |

$ | 22.50 | $ | 21.76 | $ | 0.74 | 3 | % | $ | 19.78 | $ | 2.72 | 14 | % | ||||||||||||||||||

| Tangible equity / tangible assets |

9.55 | % | 9.24 | % | +31 Basis Points | 8.10 | % | +145 Basis Points | ||||||||||||||||||||||||

| Gross loans / total deposits |

95.96 | % | 92.15 | % | +381 Basis Points | 88.93 | % | +703 Basis Points | ||||||||||||||||||||||||

| Noninterest-bearing deposits / total deposits |

40.44 | % | 40.23 | % | +21 Basis Points | 45.30 | % | -486 Basis Points | ||||||||||||||||||||||||

| QUARTERLY AVERAGE | Change | Change | ||||||||||||||||||||||||||||||

| HIGHLIGHTS: | Q4 2023 | Q3 2023 | $ | % | Q4 2022 | $ | % | |||||||||||||||||||||||||

| Total assets |

$ | 1,984,337 | $ | 1,993,147 | $ | (8,810 | ) | 0 | % | $ | 2,088,206 | $ | (103,869 | ) | -5 | % | ||||||||||||||||

| Total earning assets |

1,896,954 | 1,910,755 | (13,801 | ) | -1 | % | 2,007,243 | (110,289 | ) | -5 | % | |||||||||||||||||||||

| Gross loans |

1,571,994 | 1,551,708 | 20,286 | 1 | % | 1,621,322 | (49,328 | ) | -3 | % | ||||||||||||||||||||||

| Deposits |

1,700,625 | 1,719,416 | (18,791 | ) | -1 | % | 1,785,693 | (85,068 | ) | -5 | % | |||||||||||||||||||||

| Tangible equity |

187,399 | 181,384 | 6,015 | 3 | % | 161,919 | 25,480 | 16 | % | |||||||||||||||||||||||

| Tangible equity / tangible assets |

9.48 | % | 9.13 | % | +35 Basis Points | 7.78 | % | +170 Basis Points | ||||||||||||||||||||||||

| Gross loans / total deposits |

92.44 | % | 90.25 | % | +219 Basis Points | 90.80 | % | +164 Basis Points | ||||||||||||||||||||||||

| Noninterest-bearing deposits / total deposits |

41.46 | % | 41.59 | % | -13 Basis Points | 44.47 | % | -301 Basis Points | ||||||||||||||||||||||||

| YEAR-TO-DATE AVERAGE | Change | |||||||||||||||

| HIGHLIGHTS: | Q4 2023 | Q4 2022 | $ | % | ||||||||||||

| Total assets |

$ | 1,983,964 | $ | 1,953,168 | $ | 30,796 | 2 | % | ||||||||

| Total earning assets |

1,900,678 | 1,871,813 | 28,865 | 2 | % | |||||||||||

| Gross loans |

1,570,810 | 1,495,981 | 74,829 | 5 | % | |||||||||||

| Deposits |

1,701,046 | 1,649,512 | 51,534 | 3 | % | |||||||||||

| Tangible equity |

178,562 | 153,443 | 25,119 | 16 | % | |||||||||||

| Tangible equity / tangible assets |

9.03 | % | 7.89 | % | +114 Basis Points | |||||||||||

| Gross loans / total deposits |

92.34 | % | 90.69 | % | +165 Basis Points | |||||||||||

| Noninterest-bearing deposits / total deposits |

42.14 | % | 45.61 | % | -347 Basis Points | |||||||||||

-9-

CALIFORNIA BANCORP AND SUBSIDIARY

SELECTED INTERIM FINANCIAL INFORMATION (UNAUDITED) - ASSET QUALITY

(Dollars in Thousands)

| ALLOWANCE FOR CREDIT LOSSES (LOANS): | 12/31/23 | 09/30/23 | 06/30/23 | 03/31/23 | 12/31/22 | |||||||||||||||

| Balance, beginning of period |

$ | 15,921 | $ | 15,722 | $ | 15,382 | $ | 17,005 | $ | 16,555 | ||||||||||

| CECL adjustment |

— | — | — | (1,840 | ) | — | ||||||||||||||

| Provision for credit losses, quarterly |

87 | 121 | 340 | 464 | 1,100 | |||||||||||||||

| Charge-offs, quarterly |

— | (156 | ) | — | (247 | ) | (650 | ) | ||||||||||||

| Recoveries, quarterly |

20 | 234 | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Balance, end of period |

$ | 16,028 | $ | 15,921 | $ | 15,722 | $ | 15,382 | $ | 17,005 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| NONPERFORMING ASSETS: | 12/31/23 | 09/30/23 | 06/30/23 | 03/31/23 | 12/31/22 | |||||||||||||||

| Loans accounted for on a non-accrual basis |

$ | 3,781 | $ | 1,236 | $ | 181 | $ | 222 | $ | 1,250 | ||||||||||

| Loans with principal or interest contractually past due 90 days or more and still accruing interest |

— | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Nonperforming loans |

$ | 3,781 | $ | 1,236 | $ | 181 | $ | 222 | $ | 1,250 | ||||||||||

| Other real estate owned |

— | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Nonperforming assets |

$ | 3,781 | $ | 1,236 | $ | 181 | $ | 222 | $ | 1,250 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Nonperforming loans by asset type: |

||||||||||||||||||||

| Commercial |

$ | 3,728 | $ | 1,183 | $ | — | $ | — | $ | 1,028 | ||||||||||

| Real estate other |

— | — | — | — | — | |||||||||||||||

| Real estate construction and land |

— | — | — | — | — | |||||||||||||||

| SBA |

53 | 53 | 181 | 222 | 222 | |||||||||||||||

| Other |

— | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Nonperforming loans |

$ | 3,781 | $ | 1,236 | $ | 181 | $ | 222 | $ | 1,250 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| ASSET QUALITY: | 12/31/23 | 09/30/23 | 06/30/23 | 03/31/23 | 12/31/22 | |||||||||||||||

| Allowance for credit losses (loans) / gross loans |

1.03 | % | 1.01 | % | 0.99 | % | 0.95 | % | 1.07 | % | ||||||||||

| Allowance for credit losses (loans) / nonperforming loans |

423.91 | % | 1288.11 | % | 8686.19 | % | 6928.83 | % | 1360.40 | % | ||||||||||

| Nonperforming assets / total assets |

0.19 | % | 0.06 | % | 0.01 | % | 0.01 | % | 0.06 | % | ||||||||||

| Nonperforming loans / gross loans |

0.24 | % | 0.08 | % | 0.01 | % | 0.01 | % | 0.08 | % | ||||||||||

| Net quarterly charge-offs / gross loans |

0.00 | % | 0.00 | % | 0.00 | % | 0.02 | % | 0.04 | % | ||||||||||

-10-

CALIFORNIA BANCORP AND SUBSIDIARY

INTERIM CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

(Dollars in Thousands, Except Per Share Data)

| Three months ended | Twelve months ended | |||||||||||||||||||

| 12/31/23 | 09/30/23 | 12/31/22 | 12/31/23 | 12/31/22 | ||||||||||||||||

| INTEREST INCOME |

||||||||||||||||||||

| Loans |

$ | 24,523 | $ | 23,804 | $ | 23,972 | $ | 94,275 | $ | 74,240 | ||||||||||

| Federal funds sold |

2,386 | 2,814 | 2,236 | 9,198 | 3,519 | |||||||||||||||

| Investment securities |

1,496 | 1,476 | 1,272 | 5,737 | 4,519 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total interest income |

28,405 | 28,094 | 27,480 | 109,210 | 82,278 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| INTEREST EXPENSE |

||||||||||||||||||||

| Deposits |

9,234 | 8,961 | 4,536 | 31,710 | 7,810 | |||||||||||||||

| Other |

597 | 555 | 1,084 | 2,945 | 3,496 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total interest expense |

9,831 | 9,516 | 5,620 | 34,655 | 11,306 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income |

18,574 | 18,578 | 21,860 | 74,555 | 70,972 | |||||||||||||||

| Provision for credit losses |

181 | 314 | 1,100 | 1,297 | 3,775 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income after provision for credit losses |

18,393 | 18,264 | 20,760 | 73,258 | 67,197 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| NON-INTEREST INCOME |

||||||||||||||||||||

| Service charges and other fees |

1,055 | 1,003 | 1,653 | 3,788 | 4,913 | |||||||||||||||

| Gain on sale of loans |

— | — | — | — | 1,393 | |||||||||||||||

| Other non-interest income |

284 | 291 | 309 | 1,087 | 1,068 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non-interest income |

1,339 | 1,294 | 1,962 | 4,875 | 7,374 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| NON-INTEREST EXPENSE |

||||||||||||||||||||

| Salaries and benefits |

8,449 | 8,238 | 7,443 | 32,394 | 29,097 | |||||||||||||||

| Premises and equipment |

1,554 | 1,155 | 1,249 | 5,057 | 5,093 | |||||||||||||||

| Other |

2,215 | 2,458 | 3,021 | 10,064 | 10,475 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non-interest expense |

12,218 | 11,851 | 11,713 | 47,515 | 44,665 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income taxes |

7,514 | 7,707 | 11,009 | 30,618 | 29,906 | |||||||||||||||

| Income taxes |

2,173 | 2,306 | 3,340 | 8,985 | 8,798 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| NET INCOME |

$ | 5,341 | $ | 5,401 | $ | 7,669 | $ | 21,633 | $ | 21,108 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| EARNINGS PER SHARE |

||||||||||||||||||||

| Basic earnings per share |

$ | 0.64 | $ | 0.64 | $ | 0.92 | $ | 2.58 | $ | 2.54 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted earnings per share |

$ | 0.63 | $ | 0.64 | $ | 0.91 | $ | 2.56 | $ | 2.51 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average common shares outstanding |

8,398,497 | 8,390,138 | 8,330,145 | 8,374,614 | 8,306,282 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average common and equivalent shares outstanding |

8,525,420 | 8,455,917 | 8,463,738 | 8,453,423 | 8,404,317 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| PERFORMANCE MEASURES |

||||||||||||||||||||

| Return on average assets |

1.07 | % | 1.08 | % | 1.46 | % | 1.09 | % | 1.08 | % | ||||||||||

| Return on average equity |

10.88 | % | 11.35 | % | 17.96 | % | 11.63 | % | 13.12 | % | ||||||||||

| Return on average tangible equity |

11.31 | % | 11.81 | % | 18.79 | % | 12.12 | % | 13.76 | % | ||||||||||

| Efficiency ratio |

61.36 | % | 59.64 | % | 49.17 | % | 59.82 | % | 57.01 | % | ||||||||||

-11-

CALIFORNIA BANCORP AND SUBSIDIARY

INTERIM CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(Dollars in Thousands)

| 12/31/23 | 09/30/23 | 06/30/23 | 03/31/23 | 12/31/22 | ||||||||||||||||

| ASSETS |

||||||||||||||||||||

| Cash and due from banks |

$ | 27,520 | $ | 17,128 | $ | 19,763 | $ | 15,121 | $ | 16,686 | ||||||||||

| Federal funds sold |

184,834 | 181,854 | 187,904 | 198,804 | 215,696 | |||||||||||||||

| Investment securities |

145,401 | 149,244 | 151,129 | 153,769 | 155,878 | |||||||||||||||

| Loans: |

||||||||||||||||||||

| Commercial |

626,615 | 633,902 | 622,270 | 656,519 | 634,535 | |||||||||||||||

| Real estate other |

849,306 | 858,611 | 856,344 | 853,431 | 848,241 | |||||||||||||||

| Real estate construction and land |

44,186 | 40,003 | 60,595 | 63,928 | 63,730 | |||||||||||||||

| SBA |

4,032 | 4,415 | 4,936 | 5,610 | 7,220 | |||||||||||||||

| Other |

35,394 | 36,184 | 39,486 | 37,775 | 39,695 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loans, gross |

1,559,533 | 1,573,115 | 1,583,631 | 1,617,263 | 1,593,421 | |||||||||||||||

| Unamortized net deferred loan costs (fees) |

1,107 | 1,312 | 1,637 | 1,765 | 2,040 | |||||||||||||||

| Allowance for credit losses |

(16,028 | ) | (15,921 | ) | (15,722 | ) | (15,382 | ) | (17,005 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loans, net |

1,544,612 | 1,558,506 | 1,569,546 | 1,603,646 | 1,578,456 | |||||||||||||||

| Premises and equipment, net |

2,207 | 2,432 | 2,625 | 2,848 | 3,072 | |||||||||||||||

| Bank owned life insurance |

25,878 | 25,697 | 25,519 | 25,334 | 25,127 | |||||||||||||||

| Goodwill and core deposit intangible |

7,432 | 7,442 | 7,452 | 7,462 | 7,472 | |||||||||||||||

| Accrued interest receivable and other assets |

48,021 | 41,614 | 41,708 | 43,790 | 39,828 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total assets |

$ | 1,985,905 | $ | 1,983,917 | $ | 2,005,646 | $ | 2,050,774 | $ | 2,042,215 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| LIABILITIES |

||||||||||||||||||||

| Deposits: |

||||||||||||||||||||

| Demand noninterest-bearing |

$ | 657,302 | $ | 686,723 | $ | 742,160 | $ | 740,650 | $ | 811,671 | ||||||||||

| Demand interest-bearing |

26,715 | 28,533 | 29,324 | 30,798 | 37,815 | |||||||||||||||

| Money market and savings |

631,015 | 672,119 | 633,620 | 616,864 | 671,016 | |||||||||||||||

| Time |

310,212 | 319,706 | 333,192 | 329,298 | 271,238 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total deposits |

1,625,244 | 1,707,081 | 1,738,296 | 1,717,610 | 1,791,740 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Junior subordinated debt securities |

54,291 | 54,256 | 54,221 | 54,186 | 54,152 | |||||||||||||||

| Other borrowings |

75,000 | — | — | 75,000 | — | |||||||||||||||

| Accrued interest payable and other liabilities |

34,909 | 32,465 | 28,894 | 25,417 | 24,069 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total liabilities |

1,789,444 | 1,793,802 | 1,821,411 | 1,872,213 | 1,869,961 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| SHAREHOLDERS’ EQUITY |

||||||||||||||||||||

| Common stock |

113,227 | 112,656 | 112,167 | 111,609 | 111,257 | |||||||||||||||

| Retained earnings |

84,165 | 78,824 | 73,423 | 68,082 | 62,297 | |||||||||||||||

| Accumulated other comprehensive loss |

(931 | ) | (1,365 | ) | (1,355 | ) | (1,130 | ) | (1,300 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total shareholders’ equity |

196,461 | 190,115 | 184,235 | 178,561 | 172,254 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total liabilities and shareholders’ equity |

$ | 1,985,905 | $ | 1,983,917 | $ | 2,005,646 | $ | 2,050,774 | $ | 2,042,215 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| CAPITAL ADEQUACY |

||||||||||||||||||||

| Tier I leverage ratio |

9.61 | % | 9.27 | % | 9.01 | % | 8.76 | % | 7.98 | % | ||||||||||

| Tier I risk-based capital ratio |

9.53 | % | 9.34 | % | 9.07 | % | 8.54 | % | 8.23 | % | ||||||||||

| Total risk-based capital ratio |

13.16 | % | 13.00 | % | 12.73 | % | 12.08 | % | 11.77 | % | ||||||||||

| Total equity/ total assets |

9.89 | % | 9.58 | % | 9.19 | % | 8.71 | % | 8.43 | % | ||||||||||

| Book value per share |

$ | 23.38 | $ | 22.64 | $ | 21.98 | $ | 21.37 | $ | 20.67 | ||||||||||

| Common shares outstanding |

8,402,482 | 8,395,483 | 8,383,772 | 8,355,378 | 8,332,479 | |||||||||||||||

-12-

CALIFORNIA BANCORP AND SUBSIDIARY

INTERIM CONSOLIDATED AVERAGE BALANCE SHEET AND YIELD DATA (UNAUDITED)

(Dollars in Thousands)

| Three months ended December 31, | Three months ended September 30, | |||||||||||||||||||||||

| 2023 | 2023 | |||||||||||||||||||||||

| Yields | Interest | Yields | Interest | |||||||||||||||||||||

| Average | or | Income/ | Average | or | Income/ | |||||||||||||||||||

| Balance | Rates | Expense | Balance | Rates | Expense | |||||||||||||||||||

| ASSETS |

||||||||||||||||||||||||

| Interest earning assets: |

||||||||||||||||||||||||

| Loans (1) |

$ | 1,571,994 | 6.19 | % | $ | 24,523 | $ | 1,551,708 | 6.09 | % | $ | 23,804 | ||||||||||||

| Federal funds sold |

177,331 | 5.34 | % | 2,386 | 208,725 | 5.35 | % | 2,814 | ||||||||||||||||

| Investment securities |

147,629 | 4.02 | % | 1,496 | 150,322 | 3.90 | % | 1,476 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total interest earning assets |

1,896,954 | 5.94 | % | 28,405 | 1,910,755 | 5.83 | % | 28,094 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Noninterest-earning assets: |

||||||||||||||||||||||||

| Cash and due from banks |

20,310 | 20,351 | ||||||||||||||||||||||

| All other assets (2) |

67,073 | 62,041 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| TOTAL |

$ | 1,984,337 | $ | 1,993,147 | ||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY |

||||||||||||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||||||

| Deposits: |

||||||||||||||||||||||||

| Demand |

$ | 28,678 | 0.29 | % | 21 | $ | 28,766 | 0.33 | % | 24 | ||||||||||||||

| Money market and savings |

638,623 | 3.02 | % | 4,857 | 642,909 | 2.95 | % | 4,775 | ||||||||||||||||

| Time |

328,270 | 5.26 | % | 4,356 | 332,662 | 4.96 | % | 4,162 | ||||||||||||||||

| Other |

56,715 | 4.18 | % | 597 | 54,235 | 4.06 | % | 555 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total interest-bearing liabilities |

1,052,286 | 3.71 | % | 9,831 | 1,058,572 | 3.57 | % | 9,516 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Noninterest-bearing liabilities: |

||||||||||||||||||||||||

| Demand deposits |

705,054 | 715,079 | ||||||||||||||||||||||

| Accrued expenses and other liabilities |

32,161 | 30,665 | ||||||||||||||||||||||

| Shareholders’ equity |

194,836 | 188,831 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| TOTAL |

$ | 1,984,337 | $ | 1,993,147 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net interest income and margin (3) |

3.88 | % | $ | 18,574 | 3.86 | % | $ | 18,578 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| (1) | Nonperforming loans are included in average loan balances. No adjustment has been made for these loans in the calculation of yields. Interest income on loans includes amortization of net deferred loan costs of $53,000 and $82,000, respectively. |

| (2) | Other noninterest-earning assets includes the allowance for credit losses of $15.9 million and $15.8 million, respectively. |

| (3) | Net interest margin is net interest income divided by total interest-earning assets. |

-13-

CALIFORNIA BANCORP AND SUBSIDIARY

INTERIM CONSOLIDATED AVERAGE BALANCE SHEET AND YIELD DATA (UNAUDITED)

(Dollars in Thousands)

| Three months ended December 31, | ||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||

| Yields | Interest | Yields | Interest | |||||||||||||||||||||

| Average | or | Income/ | Average | or | Income/ | |||||||||||||||||||

| Balance | Rates | Expense | Balance | Rates | Expense | |||||||||||||||||||

| ASSETS |

||||||||||||||||||||||||

| Interest earning assets: |

||||||||||||||||||||||||

| Loans (1) |

$ | 1,571,994 | 6.19 | % | $ | 24,523 | $ | 1,621,322 | 5.87 | % | $ | 23,972 | ||||||||||||

| Federal funds sold |

177,331 | 5.34 | % | 2,386 | 229,209 | 3.87 | % | 2,236 | ||||||||||||||||

| Investment securities |

147,629 | 4.02 | % | 1,496 | 156,712 | 3.22 | % | 1,272 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total interest earning assets |

1,896,954 | 5.94 | % | 28,405 | 2,007,243 | 5.43 | % | 27,480 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Noninterest-earning assets: |

||||||||||||||||||||||||

| Cash and due from banks |

20,310 | 20,692 | ||||||||||||||||||||||

| All other assets (2) |

67,073 | 60,271 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| TOTAL |

$ | 1,984,337 | $ | 2,088,206 | ||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY |

||||||||||||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||||||

| Deposits: |

||||||||||||||||||||||||

| Demand |

$ | 28,678 | 0.29 | % | 21 | $ | 39,582 | 0.06 | % | $ | 6 | |||||||||||||

| Money market and savings |

638,623 | 3.02 | % | 4,857 | 647,213 | 1.45 | % | 2,359 | ||||||||||||||||

| Time |

328,270 | 5.26 | % | 4,356 | 304,784 | 2.83 | % | 2,171 | ||||||||||||||||

| Other |

56,715 | 4.18 | % | 597 | 110,650 | 3.89 | % | 1,084 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total interest-bearing liabilities |

1,052,286 | 3.71 | % | 9,831 | 1,102,229 | 2.02 | % | 5,620 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Noninterest-bearing liabilities: |

||||||||||||||||||||||||

| Demand deposits |

705,054 | 794,114 | ||||||||||||||||||||||

| Accrued expenses and other liabilities |

32,161 | 22,467 | ||||||||||||||||||||||

| Shareholders’ equity |

194,836 | 169,396 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| TOTAL |

$ | 1,984,337 | $ | 2,088,206 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net interest income and margin (3) |

3.88 | % | $ | 18,574 | 4.32 | % | $ | 21,860 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| (1) | Nonperforming loans are included in average loan balances. No adjustment has been made for these loans in the calculation of yields. Interest income on loans includes amortization of net deferred loan (costs) fees of $(53,000) and $1.0 million, respectively. |

| (2) | Other noninterest-earning assets includes the allowance for credit losses of $15.9 million and $16.5 million, respectively. |

| (3) | Net interest margin is net interest income divided by total interest-earning assets. |

-14-

CALIFORNIA BANCORP AND SUBSIDIARY

INTERIM CONSOLIDATED AVERAGE BALANCE SHEET AND YIELD DATA (UNAUDITED)

(Dollars in Thousands)

| Twelve months ended December 31, | ||||||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||||||

| Yields | Interest | Yields | Interest | |||||||||||||||||||||

| Average | or | Income/ | Average | or | Income/ | |||||||||||||||||||

| Balance | Rates | Expense | Balance | Rates | Expense | |||||||||||||||||||

| ASSETS |

||||||||||||||||||||||||

| Interest earning assets: |

||||||||||||||||||||||||

| Loans (1) |

$ | 1,570,810 | 6.00 | % | $ | 94,275 | $ | 1,495,981 | 4.96 | % | $ | 74,240 | ||||||||||||

| Federal funds sold |

178,540 | 5.15 | % | 9,198 | 220,084 | 1.60 | % | 3,519 | ||||||||||||||||

| Investment securities |

151,328 | 3.79 | % | 5,737 | 155,748 | 2.90 | % | 4,519 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total interest earning assets |

1,900,678 | 5.75 | % | 109,210 | 1,871,813 | 4.40 | % | 82,278 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Noninterest-earning assets: |

||||||||||||||||||||||||

| Cash and due from banks |

19,500 | 19,838 | ||||||||||||||||||||||

| All other assets (2) |

63,786 | 61,517 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| TOTAL |

$ | 1,983,964 | $ | 1,953,168 | ||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY |

||||||||||||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||||||

| Deposits: |

||||||||||||||||||||||||

| Demand |

$ | 30,436 | 0.21 | % | 64 | $ | 40,054 | 0.08 | % | 31 | ||||||||||||||

| Money market and savings |

629,419 | 2.63 | % | 16,529 | 651,429 | 0.70 | % | 4,544 | ||||||||||||||||

| Time |

324,439 | 4.66 | % | 15,117 | 205,681 | 1.57 | % | 3,235 | ||||||||||||||||

| Other |

67,984 | 4.33 | % | 2,945 | 121,464 | 2.88 | % | 3,496 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total interest-bearing liabilities |

1,052,278 | 3.29 | % | 34,655 | 1,018,628 | 1.11 | % | 11,306 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Noninterest-bearing liabilities: |

||||||||||||||||||||||||

| Demand deposits |

716,752 | 752,348 | ||||||||||||||||||||||

| Accrued expenses and other liabilities |

28,920 | 21,256 | ||||||||||||||||||||||

| Shareholders’ equity |

186,014 | 160,936 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| TOTAL |

$ | 1,983,964 | $ | 1,953,168 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net interest income and margin (3) |

3.92 | % | $ | 74,555 | 3.79 | % | $ | 70,972 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| (1) | Nonperforming loans are included in average loan balances. No adjustment has been made for these loans in the calculation of yields. Interest income on loans includes amortization of net deferred loan (costs) fees of $(535,000) and $1.5 million, respectively. |

| (2) | Other noninterest-earning assets includes the allowance for loan losses of $16.0 million and $15.4 million, respectively. |

| (3) | Net interest margin is net interest income divided by total interest-earning assets. |

-15-

CALIFORNIA BANCORP AND SUBSIDIARY

INTERIM CONSOLIDATED NON GAAP DATA (UNAUDITED)

(Dollars in Thousands, Except Per Share Data)

| REVENUE: | Three months ended | Twelve months ended | ||||||||||||||||||

| 12/31/23 | 09/30/23 | 12/31/22 | 12/31/23 | 12/31/22 | ||||||||||||||||

| Net interest income |

$ | 18,574 | $ | 18,578 | $ | 21,860 | $ | 74,555 | $ | 70,972 | ||||||||||

| Non-interest income |

1,339 | 1,294 | 1,962 | 4,875 | 7,374 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total revenue |

$ | 19,913 | $ | 19,872 | $ | 23,822 | $ | 79,430 | $ | 78,346 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| NON-INTEREST EXPENSE: | Three months ended | Twelve months ended | ||||||||||||||||||

| 12/31/23 | 09/30/23 | 12/31/22 | 12/31/23 | 12/31/22 | ||||||||||||||||

| Total non-interest expense |

$ | 12,218 | $ | 11,851 | $ | 11,713 | $ | 47,515 | $ | 44,665 | ||||||||||

| Total capitalized loan origination costs |

824 | 668 | 960 | 2,837 | 4,119 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating expenses, before capitalization of loan origination costs |

$ | 13,042 | $ | 12,519 | $ | 12,673 | $ | 50,352 | $ | 48,784 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| TANGIBLE ASSETS: | 12/31/23 | 09/30/23 | 06/30/23 | 03/31/23 | 12/31/22 | |||||||||||||||

| Total assets |

$ | 1,985,905 | $ | 1,983,917 | $ | 2,005,646 | $ | 2,050,774 | $ | 2,042,215 | ||||||||||

| Goodwill and core deposit intangibles |

7,432 | 7,442 | 7,452 | 7,462 | 7,472 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Tangible assets |

$ | 1,978,473 | $ | 1,976,475 | $ | 1,998,194 | $ | 2,043,312 | $ | 2,034,743 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| TANGIBLE EQUITY: | 12/31/23 | 09/30/23 | 06/30/23 | 03/31/23 | 12/31/22 | |||||||||||||||

| Total shareholders’ equity |

$ | 196,461 | $ | 190,115 | $ | 184,235 | $ | 178,561 | $ | 172,254 | ||||||||||

| Goodwill and core deposit intangibles |

7,432 | 7,442 | 7,452 | 7,462 | 7,472 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Tangible equity |

$ | 189,029 | $ | 182,673 | $ | 176,783 | $ | 171,099 | $ | 164,782 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| BOOK VALUE PER SHARE: | ||||||||||||||||||||

| Total shareholders’ equity |

$ | 196,461 | $ | 190,115 | $ | 184,235 | $ | 178,561 | $ | 172,254 | ||||||||||

| Common shares outstanding |

8,402,482 | 8,395,483 | 8,383,772 | 8,355,378 | 8,332,479 | |||||||||||||||

| Total shareholders’ equity / common shares outstanding |

$ | 23.38 | $ | 22.64 | $ | 21.98 | $ | 21.37 | $ | 20.67 | ||||||||||

| TANGIBLE BOOK VALUE PER SHARE: | ||||||||||||||||||||

| Tangible equity |

$ | 189,029 | $ | 182,673 | $ | 176,783 | $ | 171,099 | $ | 164,782 | ||||||||||

| Common shares outstanding |

8,402,482 | 8,395,483 | 8,383,772 | 8,355,378 | 8,332,479 | |||||||||||||||

| Tangible equity / common shares outstanding |

$ | 22.50 | $ | 21.76 | $ | 21.09 | $ | 20.48 | $ | 19.78 | ||||||||||

-16-

Exhibit 99.2 INVESTOR PRESENTATION Q4 2023 Steven E. Shelton Thomas A. Sa CEO President, CFO & COO

FORWARD-LOOKING STATEMENTS During the course of the presentation and any transcript that may result, written or otherwise, California BanCorp (the “Company”) may make projections or other forward-looking statements regarding a variety of items. Such forward-looking statements are based upon current expectations and involve risks and uncertainties. Actual results may differ materially from those stated in any forward-looking statement based on a number of important factors and risks. Although the Company may indicate and believe that the assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove inaccurate or incorrect and therefore, there can be no assurance that the results contemplated in the forward-looking statements will be realized. The Company undertakes no obligation to release publicly the results of any revisions to the forward-looking statements included herein to reflect events or circumstances after today, or to reflect the occurrence of unanticipated events. The Company claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. 2

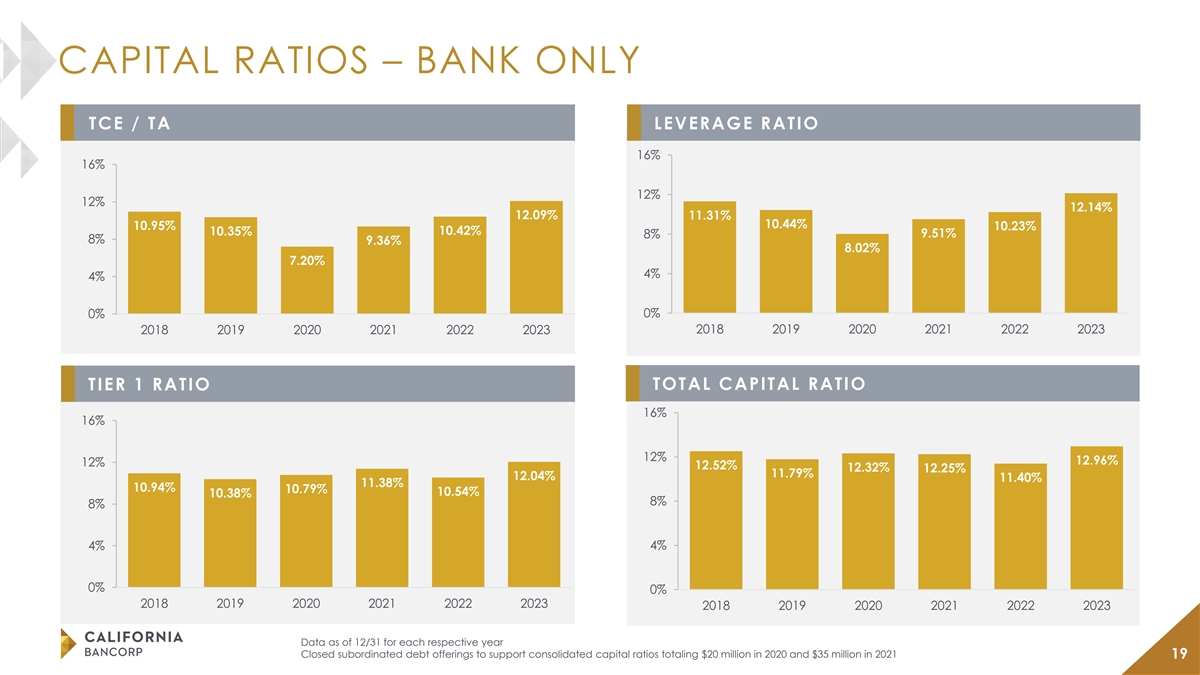

OVERVIEW OF CALIFORNIA BANCORP FOCUSED REGIONAL OFFICE FOOTPRINT COMPANY OVERVIEW ► Established in 2007 as a relationship focused commercial business bank serving Northern California with $1.99 billion in assets and a (1) market capitalization of ~$208 million ► Majority of executive management joined the bank at inception ► Significant commercial core deposit base ► Primary relationship managers with average banking experience of over 25 years and average loan books of $45 million ► Positioned to leverage recent investments to enhance our platform and extend our markets Walnut Creek FINANCIAL SNAPSHOT – 12/31/23 Balance Sheet ($mm) Q4 2023 Profitability (%) Assets 1,986 ROAA 1.07 Loans 1,560 ROATCE 11.31 Deposits 1,625 Net Interest Margin 3.88 Tangible Equity 189 Efficiency Ratio 61.36 Loans/ Deposits (%) 96% Cost of Deposits 2.15 Loan Composition (%) Deposit Composition (%) C&I Loans / Gross Loans 40.2 DDA/ Total Deposits 40.4 CRE Loans / Gross Loans 54.5 Core Deposits/ Total Deposits 80.9 ► Headquarters/Regional Office in Oakland Capital Ratios ► Regional Offices in San Jose, Walnut Creek and Sacramento (Consolidated) (%) Credit Metrics (%) ► Branch services in Walnut Creek TCE / TA 9.55 NPAs / Loans & OREO 0.24 Leverage Ratio 9.61 NPAs / Assets 0.19 Tier 1 Ratio 9.53 Reserves / Gross Loans 1.03 (1) Based on CALB’s stock price of $24.76 as of 12/29/2023 TRBC Ratio 13.16 NCOs / Avg. Loans 0.00 3

INVESTMENT HIGHLIGHTS Branch light, commercial Experienced management focused business bank with team and seasoned C&I Proven organic and strong middle market relationship teams with strong acquisitive growth story relationships throughout ties to the local markets Northern California Strong earnings outlook as Quality core deposit Disciplined underwriting franchise and commercial standards with best-in-class efficiencies from investments are realized relationship strategy asset quality metrics 4 3

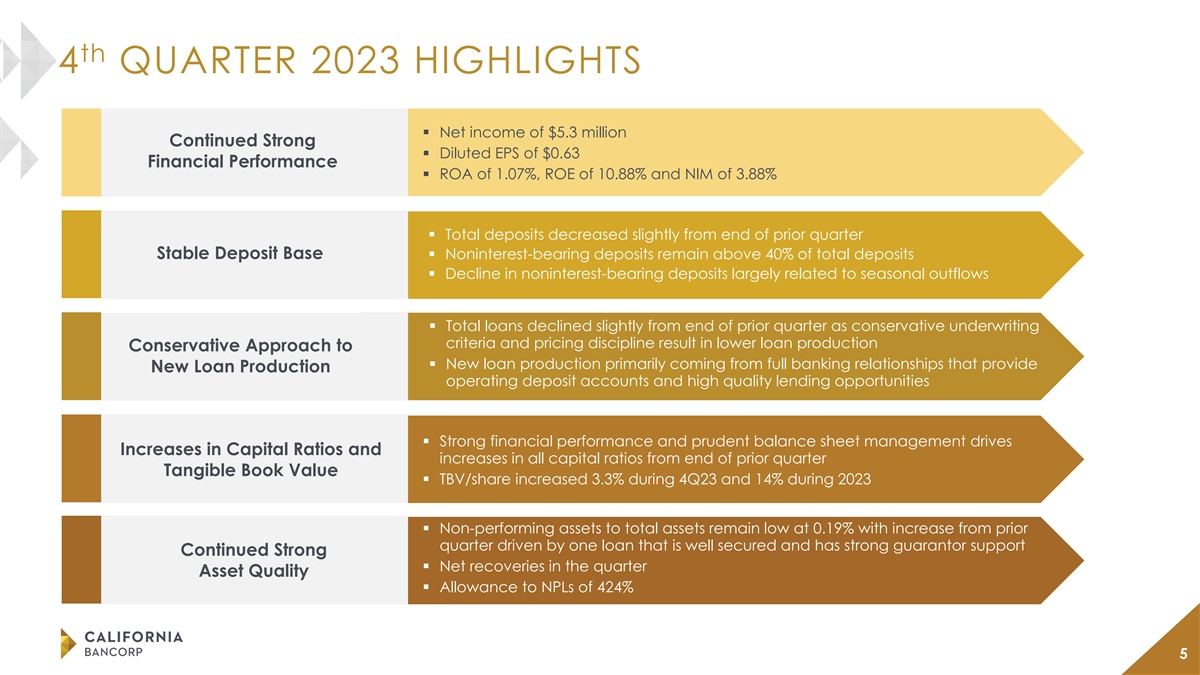

th 4 QUARTER 2023 HIGHLIGHTS § Net income of $5.3 million Continued Strong § Diluted EPS of $0.63 Financial Performance § ROA of 1.07%, ROE of 10.88% and NIM of 3.88% § Total deposits decreased slightly from end of prior quarter Stable Deposit Base § Noninterest-bearing deposits remain above 40% of total deposits § Decline in noninterest-bearing deposits largely related to seasonal outflows § Total loans declined slightly from end of prior quarter as conservative underwriting criteria and pricing discipline result in lower loan production Conservative Approach to § New loan production primarily coming from full banking relationships that provide New Loan Production operating deposit accounts and high quality lending opportunities § Strong financial performance and prudent balance sheet management drives Increases in Capital Ratios and increases in all capital ratios from end of prior quarter Tangible Book Value § TBV/share increased 3.3% during 4Q23 and 14% during 2023 § Non-performing assets to total assets remain low at 0.19% with increase from prior quarter driven by one loan that is well secured and has strong guarantor support Continued Strong § Net recoveries in the quarter Asset Quality § Allowance to NPLs of 424% 5

BRANCH LIGHT, COMMERCIAL FOCUSED BUSINESS BANK LOAN GROWTH BUSINESS MODEL OVERVIEW $2,000 2015 – 2023 CAGR ► Middle market commercial banking focus Total gross loans = 14.8% $1,500 $2 • Privately owned companies with $30 million - $300 million in Gross loans (ex. PPP) = 14.8% $73 annual revenue $306 $1,000 • Clients with minimum lending relationships of $2 million or $1 $1,591 $1,560 $1,304 million in deposits $1,063 $500 $950 $847 $733 $628 $518 $0 ► Portfolio managed over the long term to ~40% C&I loans 2015 2016 2017 2018 2019 2020 2021 2022 2023 and ~40% noninterest-bearing deposits Gross Loans (ex. PPP) PPP Loans ► Investing in other asset generating business lines • Asset-Based Lending division established in July 2011 • Practice Acquisition division established in March 2011 DEPOSIT GROWTH • Construction division established December 2015 • Sponsor Finance division established in February 2020 $2,000 2015 – 2023 $1,800 CAGR = 14.7% $1,792 $1,600 ► Strong core commercial deposit generation strategy $1,680 $1,625 $1,400 $1,532 • Utilize technology with minimal branches $1,200 • Provide commercial cash management services to middle $1,000 market clients $988 $800 $874 • Dedicated treasury management sales team and platform $600 $760 $650 $400 $542 $200 $0 2015 2016 2017 2018 2019 2020 2021 2022 2023 Dollars in millions Data as of 12/31 for each respective year 6

TAKING SHARE FROM NATIONAL/REGIONAL BANKS PRODUCT AND SERVICE DIFFERENTIATION OUR “TYPICAL CLIENT” Combine Capabilities of a Big Bank with the $8 M ~$75 M $3 M High Service Levels of a Community Bank revolving line in annual equipment with $3 M average ► Attract top talent with deep market experience to compete revenue term loan outstanding against and win business from large banks ► Professional team with a consultative delivery process $5 M $5 M $3 M ► Invest in systems, tools, and technology for success in niche markets money market commercial real demand deposit accounts to hold ► Offer clients access to key decision makers estate loan operating account surplus deposits ► Ability to execute quickly, with market leading responsiveness Fee income driven by commercial portfolio account analysis and treasury management services INDUSTRY & SPECIALTY LENDING FOCUS Commercial Banking Focused on Four Core Industries Manufacturing and Professional Contractor Investor CRE Distribution Specialty Lending Groups Practice Asset Based Sponsor Construction Acquisition Lending Finance 7

EXPERIENCED MANAGEMENT TEAM ► Previously served as an Executive Vice President of the Bank primarily responsible for managing production since the Bank’s founding in 2007 Years at CALB: 16 Steven E. Shelton, Age : 58 ► Served for thirteen years in various executive management positions including President of Years in Industry: 37 CEO CivicBank of Commerce ► More than 30 years’ experience in executive finance and risk management roles, most recently Joined 2019 serving as Chief Risk Officer for Western Alliance Bank. Thomas A. Sa, Age: ► Previously served in various executive and director roles at Bridge Bank and its holding company 57 President, CFO & COO Years in Industry: 33 Bridge Capital Holdings (BBNK), including Chief Financial Officer and Chief Strategy Officer. ► Previously served as Deputy Chief Credit Officer and part of senior management from 2007 to 2018 Vivian Mui, Years at CALB: 16 Age Age : 84 : 40► 17 years of experience in various positions including lending and credit administration at SEVP & CCO Years in Industry: 20 Mechanics Bank Scott Myers Joined 2019 ► Veteran banker with more than 15 years banking experience in the Sacramento area Age : 49 SEVP & CLO ► Previously served as Wells Fargo Senior Vice President and Sacramento Region Manager Years in Industry: 25 ► Previously served as the Bank’s Executive Vice President & East Bay Market President Years at CALB: 16 Michele Wirfel, Age ► Has worked in financial management and commercial banking since 1991 in various executive : 51 SEVP & CBO Years in Industry: 30 management positions including regional manager for CivicBank of Commerce ► Previously served as a Senior Vice President and Chief Information Officer for North Bay Bancorp Tom M. Dorrance, Years at CALB: 16 Age ► Has worked in financial management and commercial banking since 1992 including I.T. : 57 SEVP Technology & Operations Years in Industry: 29 Manager at CivicBank of Commerce ► Served as Executive Vice President and CCO from 2007 through 2017 Years at CALB: 16 John Lindstedt, ► Previously served in various executive management positions including Executive Vice President Years in Industry: 53 SEVP & CCO Emeritus and Senior Lending Officer for Wells Fargo’s corporate bank and President & CCO of CivicBank of Commerce 8

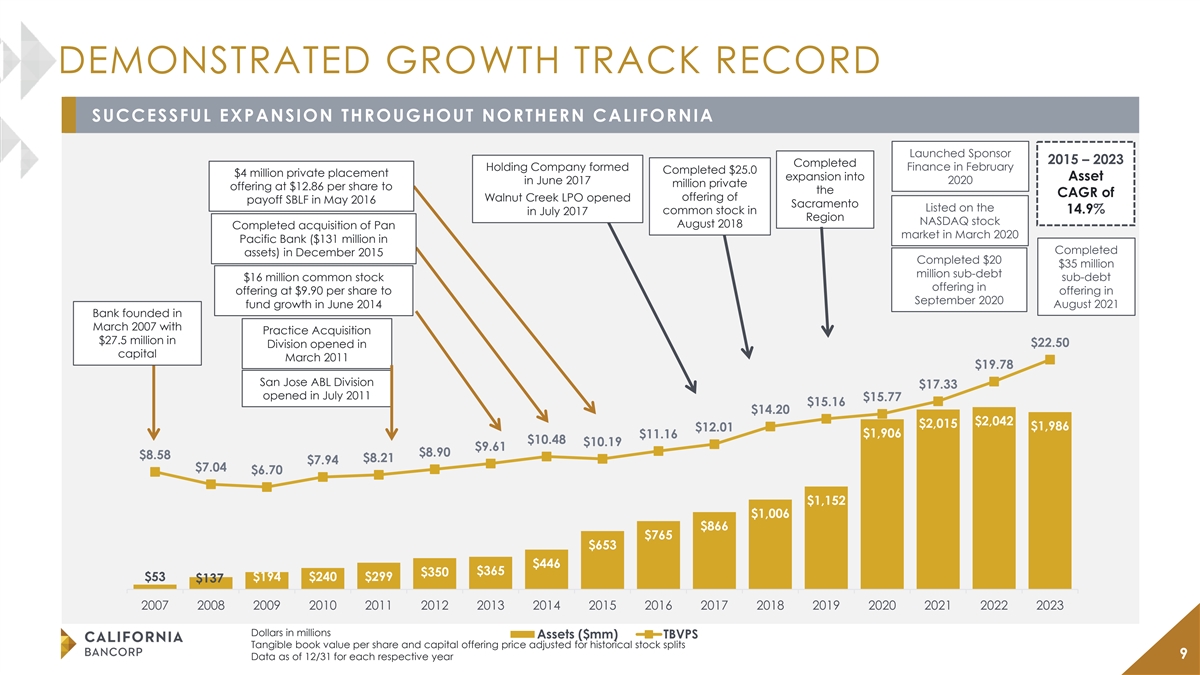

DEMONSTRATED GROWTH TRACK RECORD SUCCESSFUL EXPANSION THROUGHOUT NORTHERN CALIFORNIA Launched Sponsor 2015 – 2023 Completed Holding Company formed Finance in February Completed $25.0 $4 million private placement expansion into Asset 2020 in June 2017 million private offering at $12.86 per share to the CAGR of Walnut Creek LPO opened offering of payoff SBLF in May 2016 Sacramento Listed on the common stock in 14.9% in July 2017 Region NASDAQ stock August 2018 Completed acquisition of Pan market in March 2020 Pacific Bank ($131 million in Completed assets) in December 2015 Completed $20 $35 million million sub-debt $16 million common stock sub-debt offering in offering at $9.90 per share to offering in September 2020 fund growth in June 2014 August 2021 Bank founded in March 2007 with Practice Acquisition $27.5 million in Division opened in $22.50 capital March 2011 $19.78 San Jose ABL Division $17.33 opened in July 2011 $15.77 $15.16 $14.20 $2,042 $2,015 $1,986 $12.01 $1,906 $11.16 $10.48 $10.19 $9.61 $8.90 $8.58 $8.21 $7.94 $7.04 $6.70 $1,152 $1,006 $866 $765 $653 $446 $365 $350 $53 $194 $240 $299 $137 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 Dollars in millions Assets ($mm) TBVPS Tangible book value per share and capital offering price adjusted for historical stock splits 9 Data as of 12/31 for each respective year

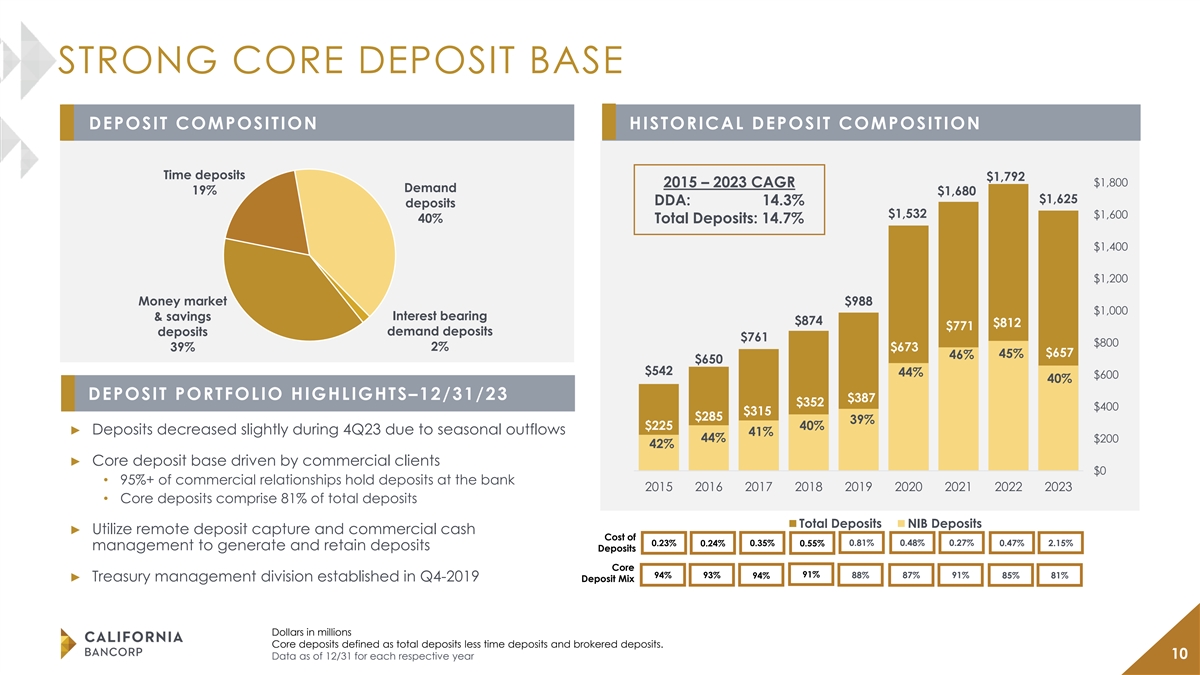

STRONG CORE DEPOSIT BASE DEPOSIT COMPOSITION HISTORICAL DEPOSIT COMPOSITION Time deposits $1,792 $1,800 2015 – 2023 CAGR Demand 19% $1,680 $1,625 DDA: 14.3% deposits $1,532 $1,600 40% Total Deposits: 14.7% $1,400 $1,200 Money market $988 $1,000 Interest bearing & savings $874 $812 $771 deposits demand deposits $761 $800 39% 2% $673 45% $657 46% $650 $542 44% $600 40% DEPOSIT PORTFOLIO HIGHLIGHTS–12/31/23 $387 $352 $400 $315 $285 39% $225 40% ► Deposits decreased slightly during 4Q23 due to seasonal outflows 41% 44% $200 42% ► Core deposit base driven by commercial clients $0 • 95%+ of commercial relationships hold deposits at the bank 2015 2016 2017 2018 2019 2020 2021 2022 2023 • Core deposits comprise 81% of total deposits Total Deposits NIB Deposits ► Utilize remote deposit capture and commercial cash Cost of 0.23% 0.24% 0.35% 0.55% 0.81% 0.48% 0.27% 0.47% 2.15% management to generate and retain deposits Deposits Core 91% 94% 93% 94% 88% 87% 91% 85% 81% ► Treasury management division established in Q4-2019 Deposit Mix Dollars in millions Core deposits defined as total deposits less time deposits and brokered deposits. 10 Data as of 12/31 for each respective year

DIVERSIFIED COMMERCIAL LOAN PORTFOLIO (1) LOAN PORTFOLIO COMPOSITION HISTORICAL LOAN COMPOSITION 2017 – 2023 CAGR Other 3% $1,560 $1,593 $1,600 C&I: 11.2% $1,377 Construction 2% $1,369 Total Loans: 13.4% $950 $1,100 $847 $733 $635 $627 $474 $415 $600 $390 $341 Commercial 40% $329 CRE - Non-Owner 40% 40% 45% 41% Occupied 37% 30% 40% 34% $100 (41% (39% (36% ex.PPP) ex.PPP) ex.PPP) -$400 2017 2018 2019 2020 2021 2022 2023 Total Loans C&I Loans Yield on CRE - Owner 4.88% 5.09% 5.19% 4.22% 4.29% 4.96% 6.19% Loans Occupied 17% Loans / 96% 96% 89% 82% 89% 96% 97% Deposits (2) OPERATING LOC USAGE GROSS LOAN FUNDING VS. NET LOAN GROWTH $131 43% $150 $1,000 44% $800 42% $100 40% 40% $64 39% $43 $46 $600 40% $42 $24 $50 $889 $920 $884 37% $862 $400 38% $6 $380 $0 $366 $347 $333 $200 $327 36% -$11 -$14 $911 $0 34% -$50 -$34 4Q22 1Q23 2Q23 3Q23 4Q23 4Q22 1Q23 2Q23 3Q23 4Q23 Commitment Amount Gross Balance Usage Gross Loan Funding Net Loan Growth Dollars in millions (1) Data as of 12/31 for each respective year 11 (2) Excludes PPP loans

NEW LOAN PRODUCTION IN 4Q23 (1) BOOKING NEW LOANS AT ATTRACTIVE RATES ► Funded new loans with balances of $64 million in 4Q23 compared to $46 million in 3Q23 and $131 million in 4Q22 ► Weighted average rate on newly funded loans was 8.86% in 4Q23 compared to 8.34% in 3Q23 and 6.72% in 4Q22 ► 4Q23 new loan dollar mix was 73% commercial, 22% CRE and 5% other (1) (1) NEW LOAN FUNDINGS WTD. AVG. RATE ON NEW LOANS $140 $1 8.86% $120 8.34% $45 8.41% $100 7.72% $80 6.72% $3 $60 $14 $0 $0 $0 $85 $40 $8 $7 $17 $47 $20 $38 $36 $25 $0 4Q22 1Q23 2Q23 3Q23 4Q23 Commercial CRE Other 4Q22 1Q23 2Q23 3Q23 4Q23 Dollars in millions (1) Excludes PPP loans 12

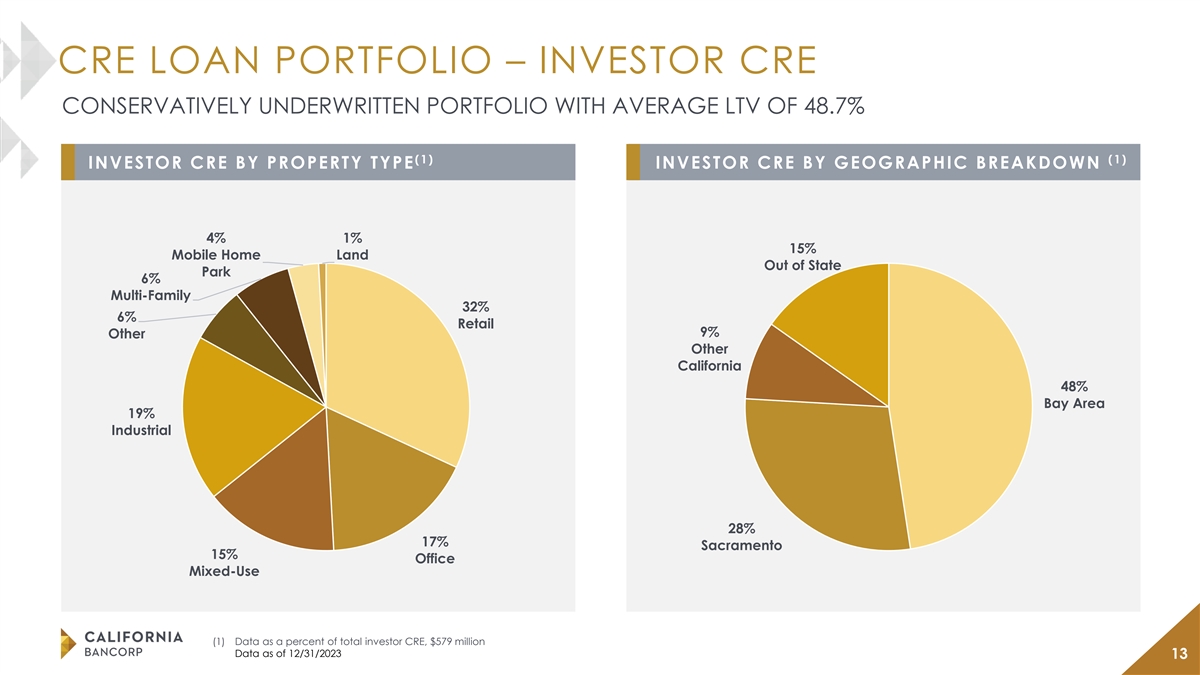

CRE LOAN PORTFOLIO – INVESTOR CRE CONSERVATIVELY UNDERWRITTEN PORTFOLIO WITH AVERAGE LTV OF 48.7% (1) (1) INVESTOR CRE BY PROPERTY TYPE INVESTOR CRE BY GEOGRAPHIC BREAKDOWN 4% 1% 15% Mobile Home Land Out of State Park 6% Multi-Family 32% 6% Retail 9% Other Other California 48% Bay Area 19% Industrial 28% 17% Sacramento 15% Office Mixed-Use (1) Data as a percent of total investor CRE, $579 million Data as of 12/31/2023 13

CRE LOAN PORTFOLIO – INVESTOR CRE: OFFICE (1) CRE PORTFOLIO COMPOSITION INVESTOR CRE OFFICE COMPOSITION CRE Office Investor - $100 million (6% of Total Loans) Medical/Dental - $40 million (2% of Total Loans) CRE Office OO - $75 million (5% of Total Loans) Office - $60 million (4% of Total Loans) CRE Other $674 million (43% of Total Loans) INVESTOR CRE NON-MEDICAL OFFICE PORTFOLIO HIGHLIGHTS (2) GEOGRAPHY ► Office CRE represents 11.2% of total loan portfolio with more Out of State - $1 million than 80% of credits being recourse loans (<1% of Total Loans) • Investor Office Non-Medical/Dental portfolio represents 4% of total portfolio Sacramento - $27 million ► No exposure to downtown San Francisco market (2% of Total Loans) Bay Area -$33 million ► Majority of credits are located in suburban markets with stable (2% of Total Loans) tenants like medical and dental practices ► Conservative underwriting criteria with low LTVs and high DCRs 14

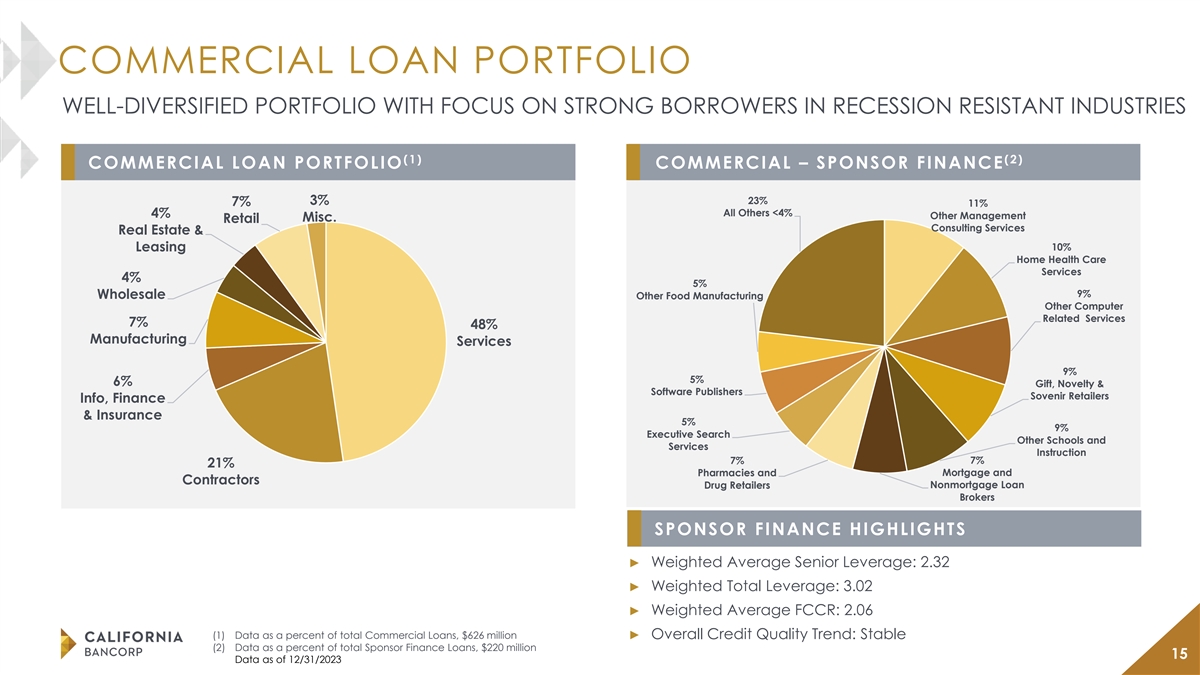

COMMERCIAL LOAN PORTFOLIO WELL-DIVERSIFIED PORTFOLIO WITH FOCUS ON STRONG BORROWERS IN RECESSION RESISTANT INDUSTRIES (1) (2) COMMERCIAL LOAN PORTFOLIO COMMERCIAL – SPONSOR FINANCE 23% 3% 7% 11% All Others <4% 4% Other Management Misc. Retail Consulting Services Real Estate & Leasing 10% Home Health Care Services 4% 5% 9% Wholesale Other Food Manufacturing Other Computer Related Services 7% 48% Manufacturing Services 9% 5% 6% Gift, Novelty & Software Publishers Sovenir Retailers Info, Finance & Insurance 5% 9% Executive Search Other Schools and Services Instruction 7% 7% 21% Pharmacies and Mortgage and Contractors Drug Retailers Nonmortgage Loan Brokers SPONSOR FINANCE HIGHLIGHTS ► Weighted Average Senior Leverage: 2.32 ► Weighted Total Leverage: 3.02 ► Weighted Average FCCR: 2.06 (1) Data as a percent of total Commercial Loans, $626 million► Overall Credit Quality Trend: Stable (2) Data as a percent of total Sponsor Finance Loans, $220 million 15 Data as of 12/31/2023