We could not find any results for:

Make sure your spelling is correct or try broadening your search.

| Name | Symbol | Market | Type |

|---|---|---|---|

| Alpha Healthcare Acquisition Corporation III | NASDAQ:ALPAU | NASDAQ | Trust |

| Price Change | % Change | Price | Bid Price | Offer Price | High Price | Low Price | Open Price | Traded | Last Trade | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0.00 | 0.00% | 9.75 | 8.51 | 11.17 | 0 | 00:00:00 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR Section 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): July 6, 2023

ALPHA HEALTHCARE ACQUISITION CORP. III

(Exact name of registrant as specified in its charter)

| Delaware | 001-40228 | 86-1645738 | ||

| (State or other jurisdiction of incorporation or organization) |

(Commission File Number) |

(I.R.S. Employer Identification Number) |

| 1177 Avenue of the Americas, 5th Floor New York, New York |

10036 | |

| (Address of principal executive offices) | (Zip Code) |

(646) 494-3296

Registrant’s telephone number, including area code

N/A

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

| ☒ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading |

Name of each exchange on which registered | ||

| Units, each consisting of one share of Class A Common Stock, $0.0001 par value, and one-fourth of a redeemable Warrant to acquire one share of Class A Common Stock | ALPAU | The NASDAQ Stock Market LLC | ||

| Class A Common Stock, par value $0.0001 per share | ALPA | The NASDAQ Stock Market LLC | ||

| Redeemable Warrants, each whole warrant exercisable for one share of Class A Common Stock at an exercise price of $11.50 | ALPAW | The NASDAQ Stock Market LLC |

☒ Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

☐ If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Item 8.01. Other Items.

On July 6, 2023, Alpha Healthcare Acquisition Corp. III (the “Company”) published a Corporate Presentation Deck (the “Corporate Presentation Deck”) discussing its acquisition of Carmell Therapeutics Corporation (“Carmell”) pursuant to a Business Combination Agreement, dated as of January 4, 2023, by and among the Company, Candy Merger Sub, Inc. and Carmell.

On July 6, 2023, the Company released a video of a Nasdaq interview with Chairman & Chief Executive Officer, Rajiv Shukla, filmed on June 27, 2023 (the “Nasdaq Interview”), discussing its acquisition of Carmell.

The foregoing description of the Corporate Presentation Deck and the Nasdaq Interview does not purport to be complete and is qualified in its entirety by reference to the full text of the presentation, which is filed as Exhibit 99.1, and a transcript of the Nasdaq Interview, which is filed as Exhibit 99.2, in each case, to this current report on Form 8-K and incorporated herein by reference.

The information contained in this Item 8.01 and in the accompanying Exhibit 99.1 shall not be deemed filed for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or incorporated by reference in any filing under the Exchange Act or the Securities Act of 1933, as amended (the “Securities Act”), except as shall be expressly set forth by specific reference in such filing.

Item 9.01. Financial Statements and Exhibits.

The information contained in this Item 9.01 and in the accompanying Exhibit 99.1 shall not be deemed filed for purposes of Section 18 of the Exchange Act or incorporated by reference in any filing under the Exchange Act or the Securities Act, except as shall be expressly set forth by specific reference in such filing.

(d) Exhibits.

| Exhibit Number |

Description | |

| 99.1 | Corporate Presentation Deck (July 6, 2023). | |

| 99.2 | Transcript of Nasdaq Interview with Chairman & Chief Executive Officer Rajiv Shukla (filmed on June 27, 2023 and released on July 6, 2023) | |

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document). | |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

Dated: July 6, 2023

| ALPHA HEALTHCARE ACQUISITION CORP. III | ||

| By: | /s/ Rajiv Shukla | |

| Name: Rajiv Shukla | ||

| Title: Chairman & Chief Executive Officer | ||

Exhibit 99.1

Carmell Therapeutics Merger With Alpha Healthcare Acquisition Corp III (Nasdaq: ALPA) July 6, 2023

PRESENTERS

Rajiv Shukla

Chairman & CEO, Alpha Healthcare Acquisition Corp. III

Executive Chairman of

“New Carmell”

• 4-time public company CEO, since 2013

• Served as Director on the Boards of 14 companies

• Raised $500+ million via

IPO+PIPE as CEO since 2017

• Closed ~$65 billion in healthcare acquisitions at Pfizer and investment career at Morgan Stanley Investment

Management & Citi Venture Capital International

• Conducted 45+ healthcare equity investments including multiple

roll-ups/control investments

• Began career at the Boston Consulting Group

• Bachelors in Pharmaceutics, Indian Institute of Technology

• Masters in Healthcare

Management, Harvard University

Randy Hubbell

President & CEO,

Carmell Therapeutics

Chief Executive Officer of “New Carmell”

• Former Chief Commercial Officer at Cardiva Medical

• Worldwide

Vice President, Strategic Marketing, J&J Biosurgery. Expanded sales footprint from 10 to 30 countries resulting in 60% sales growth over 2008-13

• Worldwide Vice President, Global Strategic Marketing, Pain Therapeutics and Cardiology, J&J

• Launch leader at Cordis, J&J, for the first drug-eluting stent, CYPHER, that achieved $1 billion in US sales within 8 months of launch

• Previously at Boston Scientific and IBM

• Bachelors in Engineering from Tulane

University

• Masters in Business Administration from Loyola University

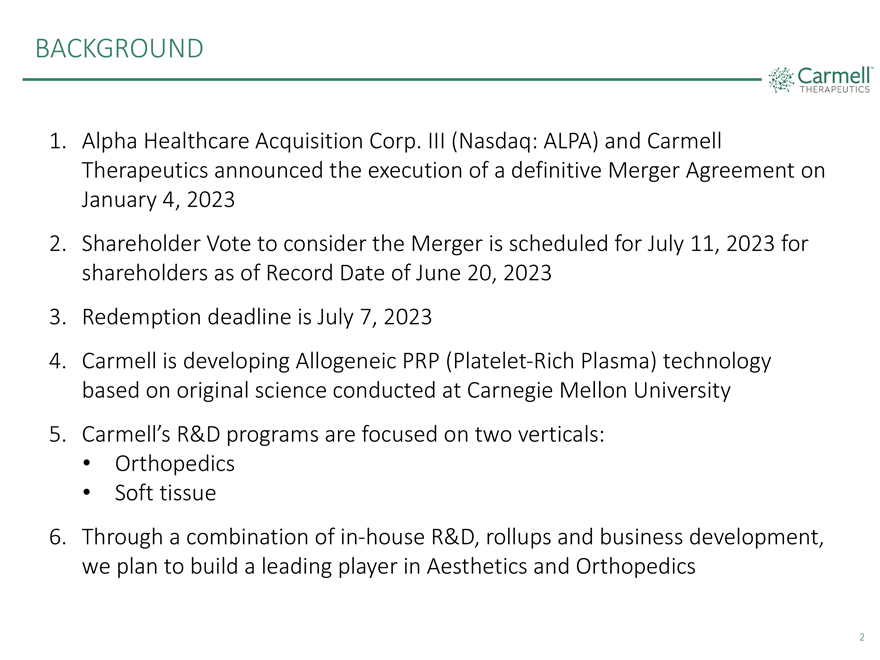

BACKGROUND 1. Alpha Healthcare Acquisition Corp. III (Nasdaq: ALPA) and Carmell Therapeutics announced the execution of a definitive Merger Agreement on January 4, 2023 2. Shareholder Vote to consider the Merger is scheduled for July 11, 2023 for shareholders as of Record Date of June 20, 2023 3. Redemption deadline is July 7, 2023 4. Carmell is developing Allogeneic PRP (Platelet-Rich Plasma) technology based on original science conducted at Carnegie Mellon University 5. Carmell’s R&D programs are focused on two verticals: • Orthopedics • Soft tissue 6. Through a combination of in-house R&D, rollups and business development, we plan to build a leading player in Aesthetics and Orthopedics 2

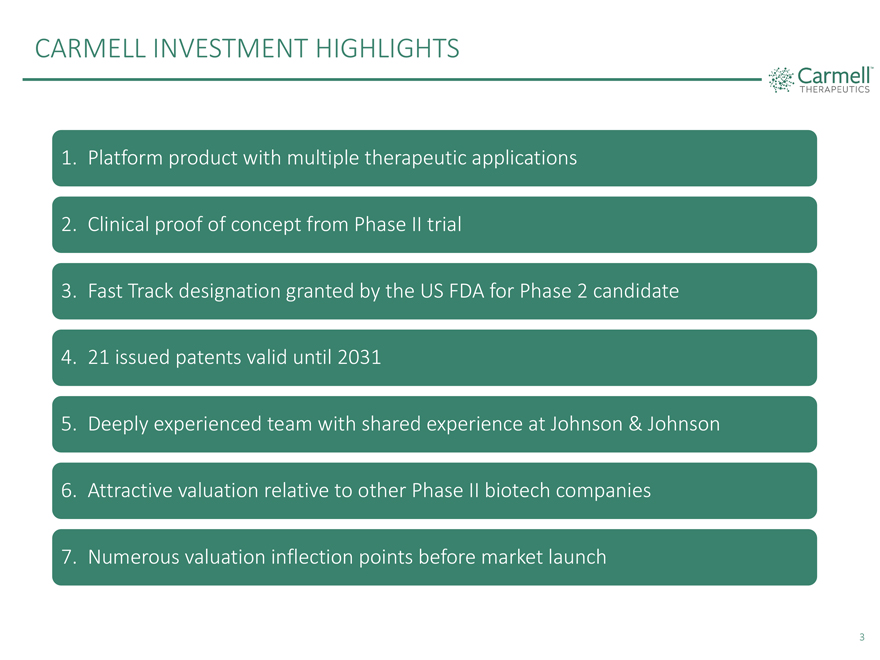

CARMELL INVESTMENT HIGHLIGHTS 1. Platform product with multiple therapeutic applications 2. Clinical proof of concept from Phase II trial 3. Fast Track designation granted by the US FDA for Phase 2 candidate 4. 21 issued patents valid until 2031 5. Deeply experienced team with shared experience at Johnson & Johnson 6. Attractive valuation relative to other Phase II biotech companies 7. Numerous valuation inflection points before market launch 3

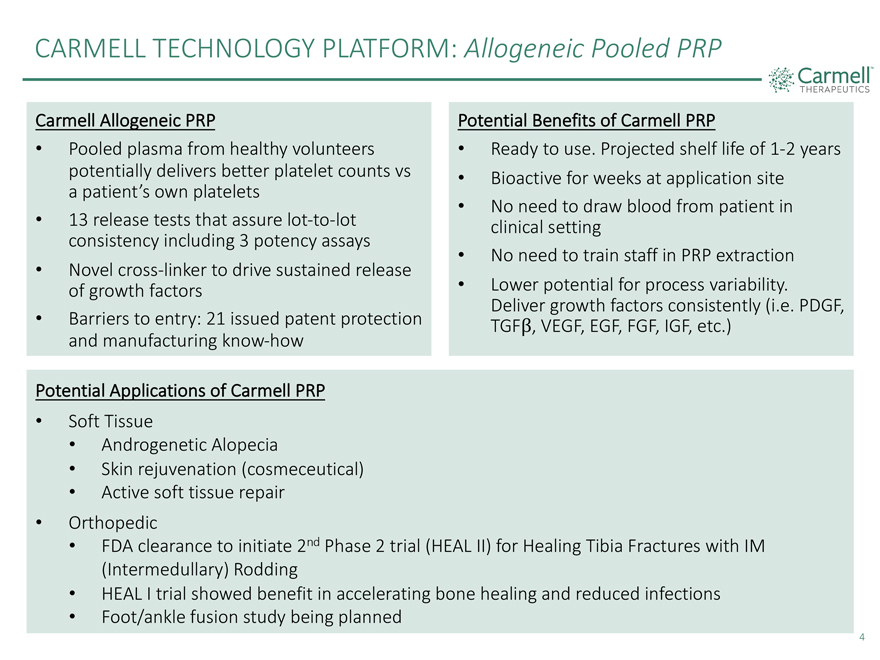

CARMELL TECHNOLOGY PLATFORM: Allogeneic Pooled PRP Carmell Allogeneic PRP Potential Benefits of Carmell PRP • Pooled plasma from healthy volunteers • Ready to use. Projected shelf life of 1-2 years potentially delivers better platelet counts vs • Bioactive for weeks at application site a patient’s own platelets • No need to draw blood from patient in • 13 release tests that assure lot-to-lot clinical setting consistency including 3 potency assays • No need to train staff in PRP extraction • Novel cross-linker to drive sustained release of growth factors • Lower potential for process variability. Deliver growth factors consistently (i.e. PDGF, • Barriers to entry: 21 issued patent protection VEGF, EGF, FGF, IGF, etc.) and manufacturing know-how Potential Applications of Carmell PRP • Soft Tissue • Androgenetic Alopecia • Skin rejuvenation (cosmeceutical) • Active soft tissue repair • Orthopedic • FDA clearance to initiate 2nd Phase 2 trial (HEAL II) for Healing Tibia Fractures with IM (Intermedullary) Rodding 4

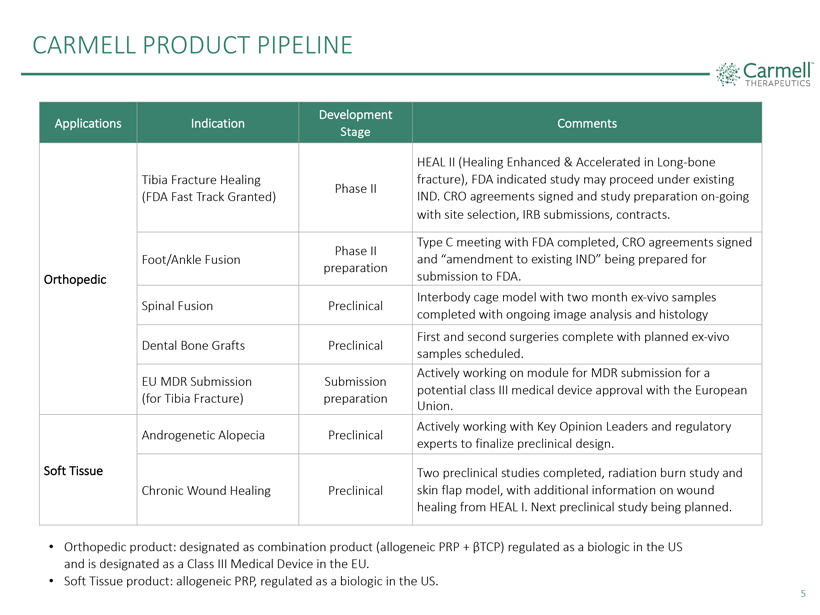

CARMELL PRODUCT PIPELINE

Development

Applications Indication Comments

Stage

HEAL II (Healing Enhanced & Accelerated in Long-bone Tibia Fracture Healing fracture), FDA indicated study may proceed under existing Phase II

(FDA Fast Track Granted) IND. CRO agreements signed and study preparation on-going with site selection, IRB submissions, contracts.

Type C meeting with FDA completed, CRO agreements signed Phase II

Foot/Ankle

Fusion and “amendment to existing IND” being prepared for preparation Orthopedic submission to FDA.

Interbody cage model with two month ex-vivo samples Spinal Fusion Preclinical completed with ongoing image analysis and histology First and second surgeries complete with planned ex-vivo Dental Bone Grafts

Preclinical samples scheduled.

Actively working on module for MDR submission for a EU MDR Submission Submission potential class III medical device approval with

the European (for Tibia Fracture) preparation Union.

Actively working with Key

Opinion Leaders and regulatory Androgenetic Alopecia Preclinical experts to finalize preclinical design.

Soft Tissue Two preclinical studies completed, radiation burn study and Chronic Wound Healing Preclinical skin flap model, with additional information on wound healing from HEAL I.

Next preclinical study being planned.

• Orthopedic product: designated as combination product (allogeneic PRP + βTCP) regulated as a biologic in

the US and is designated as a Class III Medical Device in the EU.

• Soft Tissue product: allogeneic PRP, regulated as a biologic in the US.

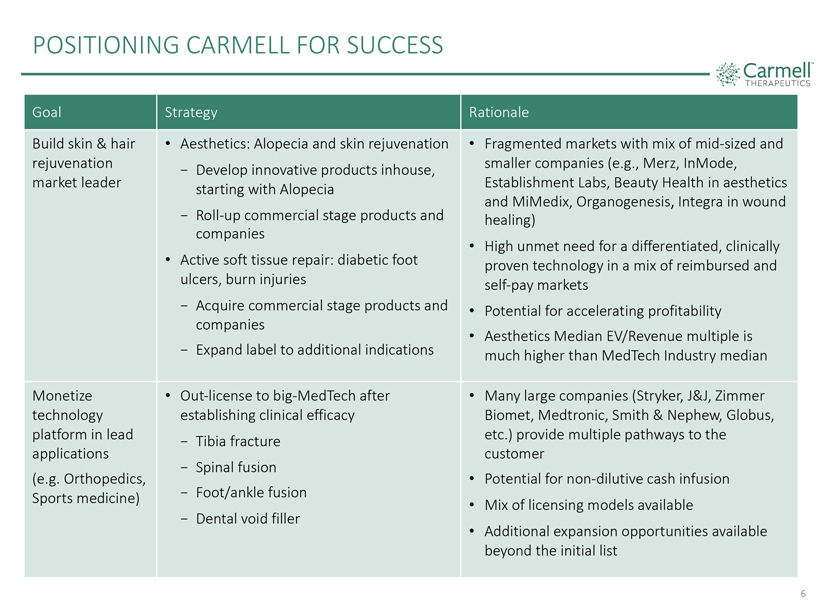

POSITIONING CARMELL FOR SUCCESS

Goal Strategy

Rationale

Build skin & hair • Aesthetics: Alopecia and skin rejuvenation • Fragmented markets with mix of

mid-sized and rejuvenation—Develop innovative products inhouse, smaller companies (e.g., Merz, InMode, market leader starting with Alopecia Establishment Labs, Beauty Health in aesthetics and MiMedix,

Organogenesis, Integra in wound

- Roll-up commercial stage products and healing) companies

• • High unmet need for a differentiated, clinically Active soft tissue repair: diabetic foot proven technology in a mix of reimbursed and ulcers, burn injuries self-pay markets

- Acquire commercial stage products and • Potential for accelerating profitability companies

• Aesthetics Median EV/Revenue multiple is

- Expand label to additional indications much

higher than MedTech Industry median Monetize • Out-license to big-MedTech after • Many large companies (Stryker, J&J, Zimmer technology establishing

clinical efficacy Biomet, Medtronic, Smith & Nephew, Globus, platform in lead—Tibia fracture etc.) provide multiple pathways to the applications customer

- Spinal fusion

(e.g. Orthopedics, • Potential for

non-dilutive cash infusion Sports medicine)—Foot/ankle fusion

• Mix of licensing models available

- Dental void filler

• Additional expansion opportunities available beyond the initial

list

6

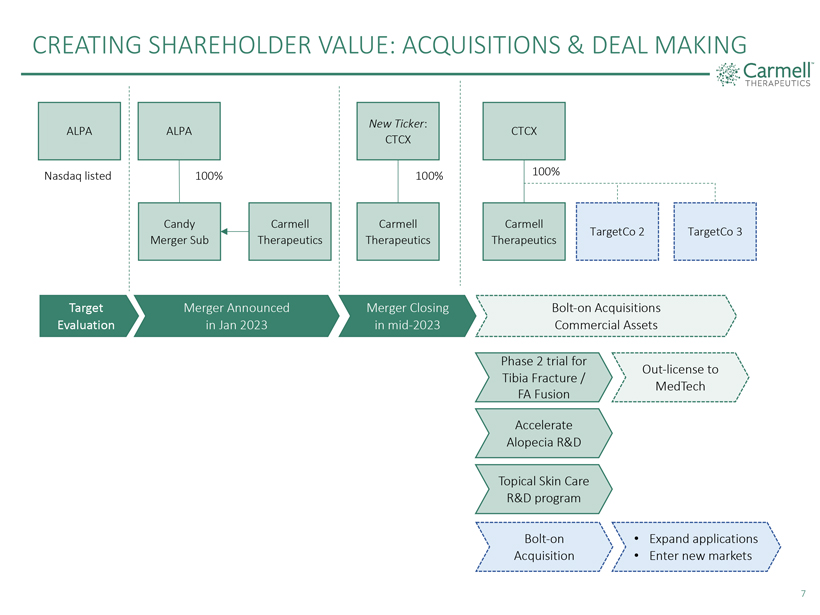

CREATING SHAREHOLDER VALUE: ACQUISITIONS & DEAL MAKING

Carmell THERAPEUTICS

ALPA Nasdaq listed

ALPA 100% Candy Merger Sub Carmell Therapeutics

New Ticker: CTCX 100% Carmell Therapeutics

CTCX 100% Carmell Therapeutics TargetCo 2 TargetCo 3

Target Evaluation

Merger Announced in Jan 2023

Merger Closing in mid-2023

Bolt-on Acquisitions Commercial Assets

Phase 2 trial for Tibia Fracture / FA Fusion

Out-license to MedTech

Accelerate Alopecia R&D

Topical Skin Care R&D

program

Bolt-on Acquisition

· Expand applications

· Enter new markets

7

NON-BINDING LOI TO ACQUIRE COMMERCIAL STAGE COMPANY

• Target manufactures and develops human allograft products for active soft tissue repair, aesthetics and orthopedic indications.

• Target’s marketed products meet all criteria for regulation under section 361 of the PHS Act and 21 CFR part 1271 as affirmed by the FDA Tissue Reference Group (TRG).

• As of March 31, 2023, the Target had achieved ~$50 million in unaudited trailing 12-month

(“TTM”) net revenue and ~$5 million in unaudited TTM EBITDA from the sales of its products.

• During Q2, 2023:

• Two of the Target’s products were added to CMS Part B Drug and Biological Average Sales Price pricing files

• Target became a preferred vendor via a national pricing contract with one of the top 3 largest group purchasing organizations serving over 1,500 hospitals in the United

States.

• Per the terms of the LOI, the Target’s shareholders will receive $65 million in Initial Equity Valuation at Closing (structured as

$8 million in cash and $57 million in CTCX stock) plus up to $75 million in Milestone Equity Payments (structured as 12% cash and 88% in CTCX stock) linked with the achievement of revenue and business milestones.

• The Target’s shareholders will be locked up for 12 months following closing.

8

SOFT TISSUE APPLICATIONS

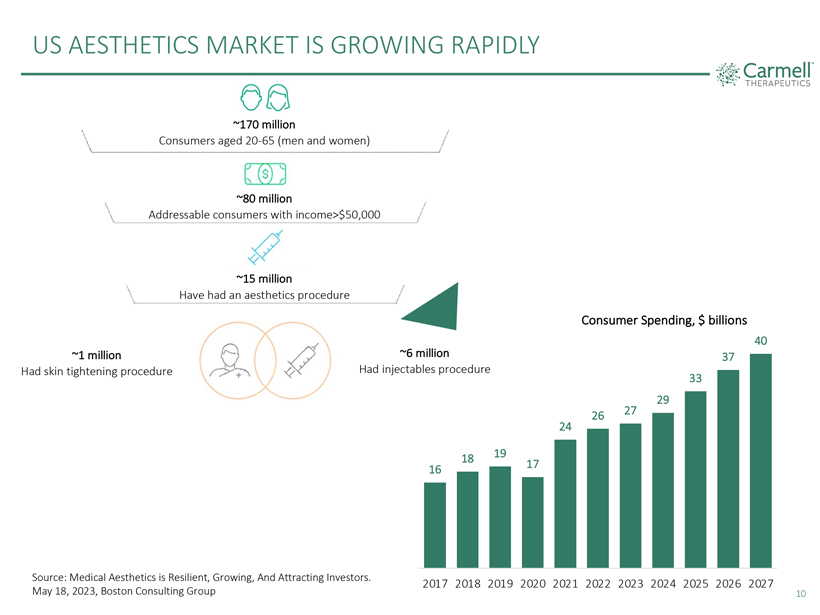

US AESTHETICS MARKET IS GROWING RAPIDLY

~170 million

Consumers aged

20-65 (men and women)

~80 million

Addressable consumers with income>$50,000

~15 million

Have had an aesthetics procedure

Consumer Spending, $ billions

40 ~1 million ~6 million 37

Had skin tightening procedure Had injectables procedure

33

4 37

33 29

26 27 24

18 19 40

16 17

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Source: Medical Aesthetics is

Resilient, Growing, And Attracting Investors. May 18, 2023, Boston Consulting Group

10

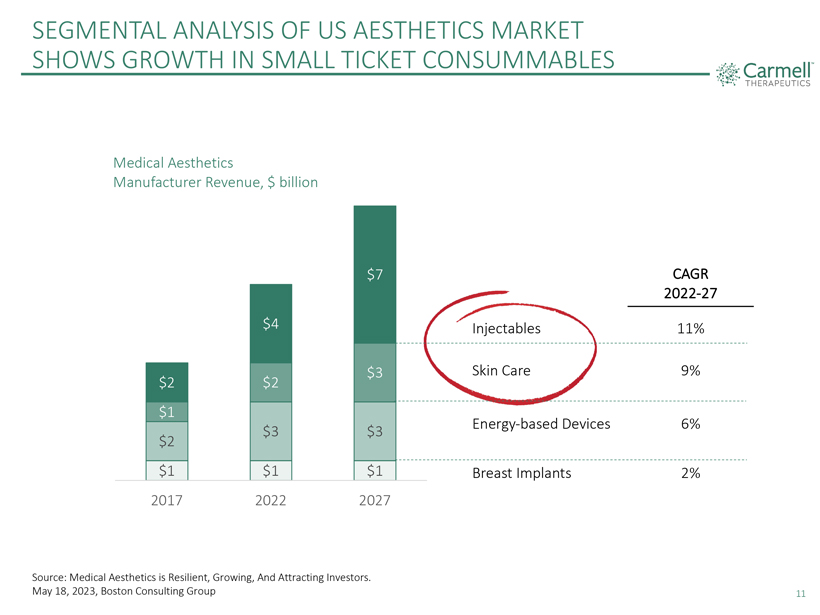

SEGMENTAL ANALYSIS OF US AESTHETICS MARKET SHOWS GROWTH IN SMALL TICKET CONSUMMABLES Carmell TM THERAPEUTICS Medical Aesthetics Manufacturer Revenue, $ billion $2 $1 $2 $1 2017 $4 $2 $3 $1 2022 $7 $3 $3 $1 2027 Injectables Skin Care Energy-based Devices Breast Implants CAGR 2022-27 11% 9% 6% 2% Source: Medical Aesthetics is Resilient, Growing, And Attracting Investors. May 18, 2023, Boston Consulting Group 11

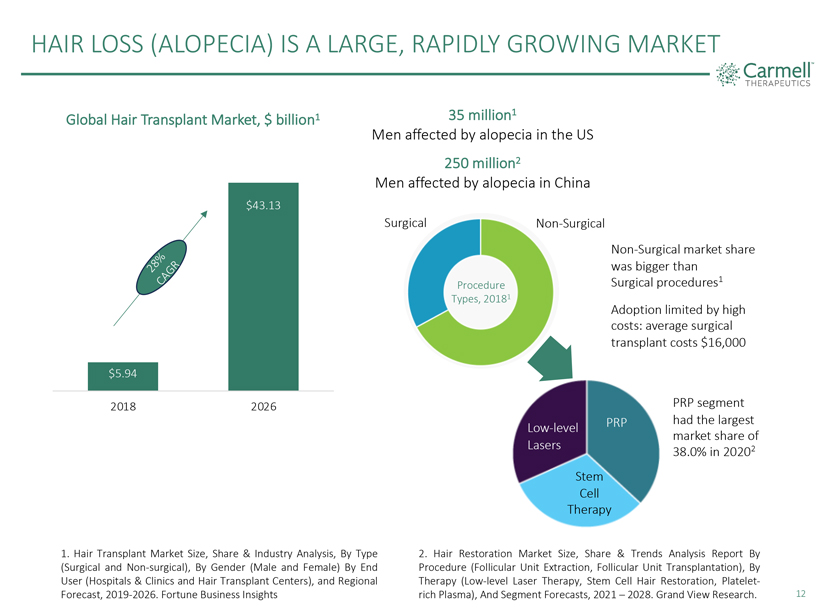

HAIR LOSS (ALOPECIA) IS A LARGE, RAPIDLY GROWING MARKET Carmell TM THERAPEUTICS Global Hair Transplant Market, $ billion1 28% CAGR $5.94 2018 $43.13 2026 35 million1 Men affected by alopecia in the US 250 million2 Men affected by alopecia in China Surgical Non-Surgical Procedure Types, 20181 Non-Surgical market share was bigger than Surgical procedures1 Adoption limited by high costs: average surgical transplant costs $16,000 Low- level Lasers PRP Stem Cell Therapy PRP segment had the largest market share of 38.0% in 20202 1. Hair Transplant Market Size, Share & Industry Analysis, By Type (Surgical and Non-surgical), By Gender (Male and Female) By End User (Hospitals & Clinics and Hair Transplant Centers), and Regional Forecast, 2019-2026. Fortune Business Insights 2. Hair Restoration Market Size, Share & Trends Analysis Report By Procedure (Follicular Unit Extraction, Follicular Unit Transplantation), By Therapy (Low-level Laser Therapy, Stem Cell Hair Restoration, Platelet-rich Plasma), And Segment Forecasts, 2021 – 2028. Grand View Research. 12

ALOPECIA IS ONE OF THE TOP UNMET NEEDS IN AESTHETICS Carmell TM THERAPEUTICS APRIL 2022 DERMATOLOGY TIMES Linda Scotum, Associate Editor Patients with androgenetic alopecia (AGA) want better treatment options, according to survey results presented at both the 2022 Winter Clinical Dermatology Conference and 2022 Maui Derm Meeting* Some highlights of the poster* were: 64% of respondents indicated their hair loss had a negative impact on their lives. This negative impact was greatest for those with AGA onset within the past 3 years but was still prominent even for those living with the condition for more than 10 years. 56% of respondents stated they had never sought treatment for their hair loss while 19% of all subjects tried but did not continue. Reasons cited by both cohorts included poor efficacy or cost; uncertainty on how to seek treatment; or lack of concern with their condition. 74% of all respondents indicated they were either likely (44%) or extremely likely (31%) to request a new therapeutic approach to AGA described as an investigational in-office treatment. * Poster presentation demonstrating unmet treatment needs in androgenetic alopecia at 2022 Winter Clinical Dermatology Conference and 2022 Maui Derm Meeting. Follica, Inc. January 19, 2022. 13

WHAT IS ANDROGENETIC ALOPECIA (AGA) • Androgenetic alopecia (AGA), or hair loss mediated by the presence of the androgen dihydrotestosterone, is the most common form of alopecia in men and women1 • Almost all persons have some degree of AGA2. The hair loss usually begins between the ages of 12 and 40 years and is frequently insufficient to be noticed. • Visible hair loss occurs in ~50% of all persons by the age of 50 years3 • Prevalence and severity increases with age although those with early onset typically have more rapid balding progression • Differences in common pattern and incidence of balding exist, but we see this condition across most racial/ethnic groups as demonstrated by studies from the United States, Norway, Australia, Nigeria and China • Other disorders include alopecia areata, telogen effluvium, cicatricial alopecia, and traumatic alopecia 1. Alopecia in Women. C. CAROLYN THIEDKE, M.D., Medical University of South Carolina, Charleston, South Carolina 2. Dawber RP, Van Neste D. Alopecia areata. In: Dawber PRP. Hair and scalp disorders: common presenting signs, differential diagnosis, and treatment. Philadelphia: Lippincott, 1995:41-138. 3. Price VH. Treatment of hair loss. N Engl J Med 1999;341:964-73 14

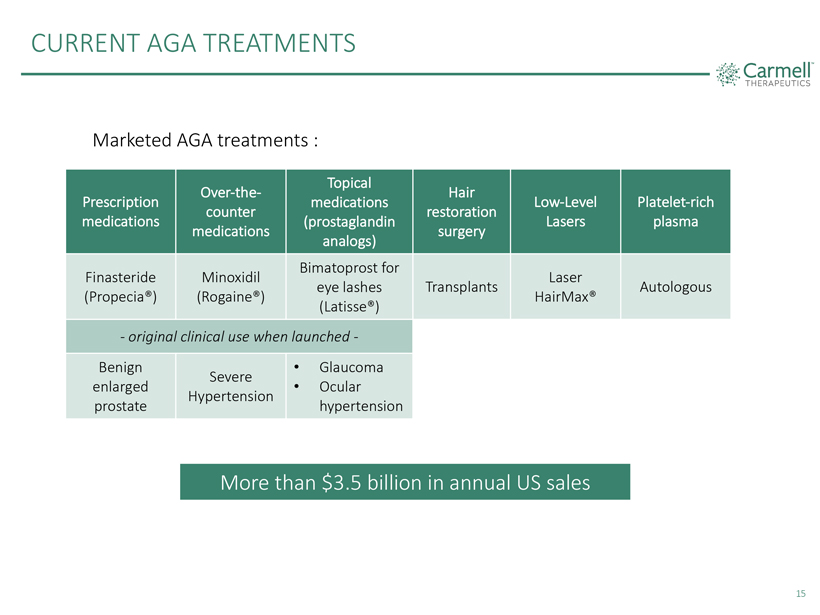

CURRENT AGA TREATMENTS Carmell THERAPEUTICS Marketed AGA treatments : Prescription medications Over-the-counter medications Topical medications (prostaglandin analogs) Hair restoration surgery Low-Level Lasers Platelet-rich plasma Finasteride (Propecia®) Minoxidil (Rogaine®) Bimatoprost for eye lashes (Latisse®) Transplants Laser HairMax® Autologous - original clinical use when launched - Benign enlarged prostate Severe Hypertension • Glaucoma • Ocular hypertension More than $3.5 billion in annual US sales 15

MINOXIDIL IS THE GOLD STANDARD FOR TREATING AGA Minoxidil and its use in hair disorders: a review Drug Design, Development and Therapy 2019, Poonkiat Suchonwanit, Sasima Thammarucha, Kanchana Leerunyakul First introduced in the 1970’s as an oral medicine for severe hypertension Meta-analysis of multiple human studies showed that 2% or 5% topical minoxidil resulted in an increase in hair density versus placebo. Robust results demonstrated in FDA approved indications of Androgenetic Alopecia and Female-pattern hair loss (not in Alopecia Areata or in Chemotherapy-induced alopecia) Finasteride (Propecia) is FDA approved for AGA but frequent side effects* related to male sexual dysfunction and gynecomastia/feminization were observed * Finasteride drug profile on MayoClinic.org CarmellTM THERAPEUTICS 16

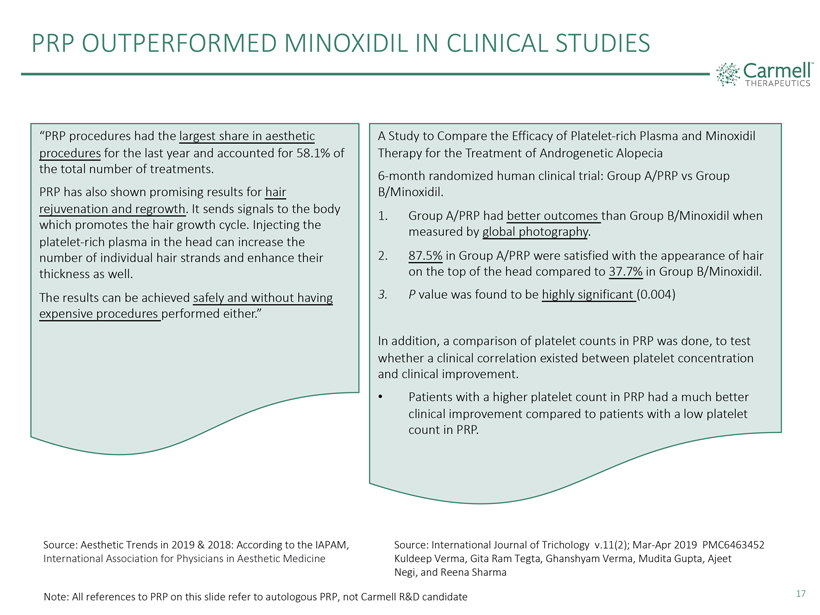

PRP OUTPERFORMED MINOXIDIL IN CLINICAL STUDIES “PRP procedures had the largest share in aesthetic procedures for the last year and accounted for 58.1% of the total number of treatments. PRP has also shown promising results for hair rejuvenation and regrowth. It sends signals to the body which promotes the hair growth cycle. Injecting the platelet-rich plasma in the head can increase the number of individual hair strands and enhance their thickness as well. The results can be achieved safely and without having expensive procedures performed either.” A Study to Compare the Efficacy of Platelet-rich Plasma and Minoxidil Therapy for the Treatment of Androgenetic Alopecia 6-month randomized human clinical trial: Group A/PRP vs Group B/Minoxidil. 1. Group A/PRP had better outcomes than Group B/Minoxidil when measured by global photography. 2. 87.5% in Group A/PRP were satisfied with the appearance of hair on the top of the head compared to 37.7% in Group B/Minoxidil. 3. P value was found to be highly significant (0.004) In addition, a comparison of platelet counts in PRP was done, to test whether a clinical correlation existed between platelet concentration and clinical improvement. Patients with a higher platelet count in PRP had a much better clinical improvement compared to patients with a low platelet count in PRP. Source: Aesthetic Trends in 2019 & 2018: According to the IAPAM, International Association for Physicians in Aesthetic Medicine Source: International Journal of Trichology v.11(2); Mar-Apr 2019 PMC6463452 Kuldeep Verma, Gita Ram Tegta, Ghanshyam Verma, Mudita Gupta, Ajeet Negi, and Reena Sharma Note: All references to PRP on this slide refer to autologous PRP, not Carmell R&D candidate 17

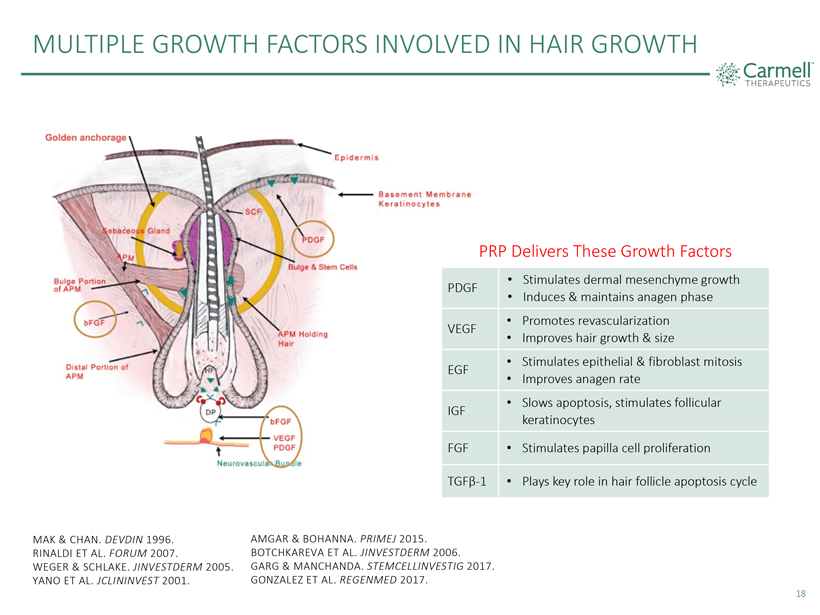

MULTIPLE GROWTH FACTORS INVOLVED IN HAIR GROWTH PRP Delivers These Growth Factors Stimulates dermal mesenchyme growth Induces & maintains anagen phase Promotes revascularization Improves hair growth & size Stimulates epithelial & fibroblast mitosis Improves anagen rate Slows apoptosis, stimulates follicular keratinocytes Stimulates papilla cell proliferation Plays key role in hair follicle apoptosis cycle PDGF VEGF EGF IGF FGF TGFß-1 MAK & CHAN. DEVDIN 1996. RINALDI ET AL. FORUM 2007. WEGER & SCHLAKE. JINVESTDERM 2005. YANO ET AL. JCLININVEST 2001. AMGAR & BOHANNA. PRIMEJ 2015. BOTCHKAREVA ET AL. JINVESTDERM 2006. GARG & MANCHANDA. STEMCELLINVESTIG 2017. GONZALEZ ET AL. REGENMED 2017. 18

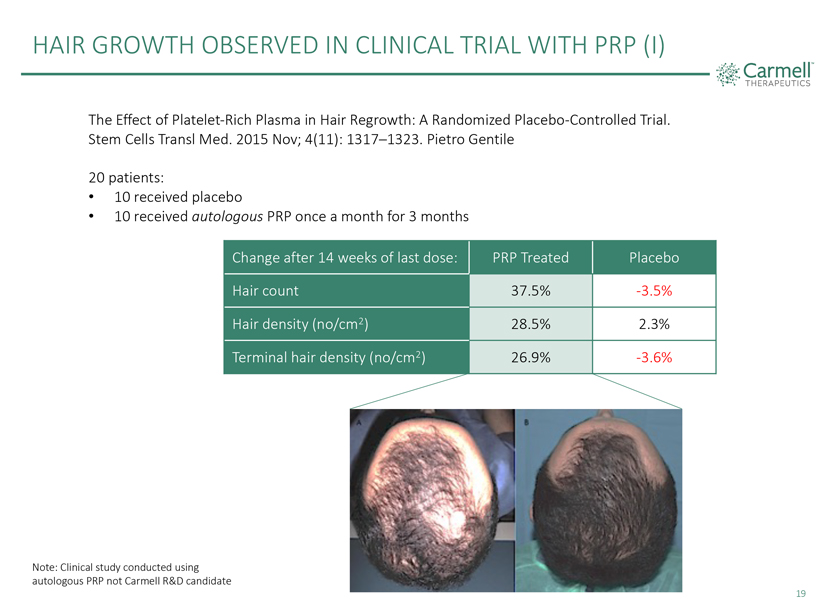

HAIR GROWTH OBSERVED IN CLINICAL TRIAL WITH PRP (I) Carmell TM THERAPEUTICS The Effect of Platelet-Rich Plasma in Hair Regrowth: A Randomized Placebo-Controlled Trial. Stem Cells Transl Med. 2015 Nov; 4(11): 1317–1323. Pietro Gentile 20 patients: 10 received placebo 10 received autologous PRP once a month for 3 months Change after 14 weeks of last dose: PRP Treated Placebo Hair count 37.5% -3.5% Hair density (no/cm2) 28.5% 2.3% Terminal hair density (no/cm2) 26.9% -3.6% Note: Clinical study conducted using autologous PRP not Carmell R&D candidate 19

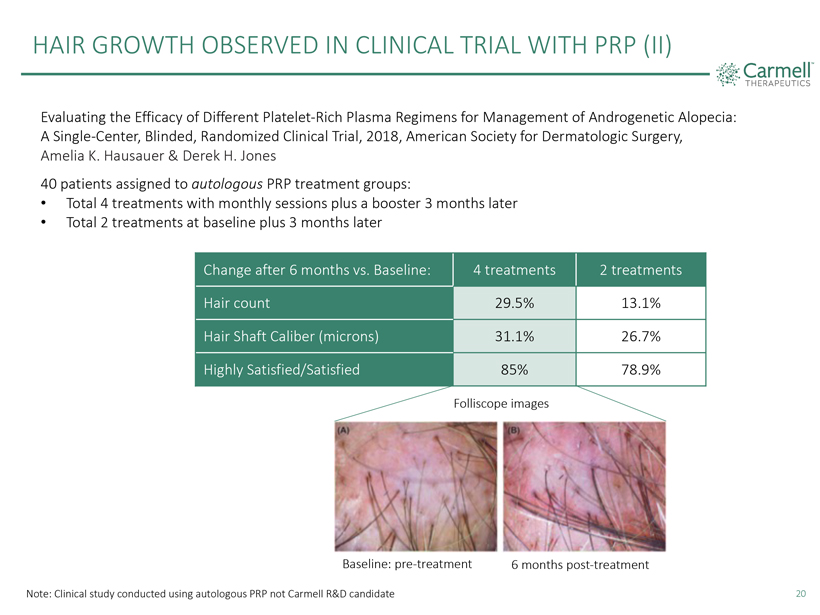

HAIR GROWTH OBSERVED IN CLINICAL TRIAL WITH PRP (II) Carmell TM THERAPEUTICS Evaluating the Efficacy of Different Platelet-Rich Plasma Regimens for Management of Androgenetic Alopecia: A Single-Center, Blinded, Randomized Clinical Trial, 2018, American Society for Dermatologic Surgery, Amelia K. Hausauer & Derek H. Jones 40 patients assigned to autologous PRP treatment groups: Total 4 treatments with monthly sessions plus a booster 3 months later Total 2 treatments at baseline plus 3 months later Change after 6 months vs. Baseline: 4 treatments 2 treatments Hair count 29.5% 13.1% Hair Shaft Caliber (microns) 31.1% 26.7% Highly Satisfied/Satisfied 85% 78.9% Folliscope images (A) Baseline: pre-treatment (B) 6 months post-treatment Note: Clinical study conducted using autologous PRP not Carmell R&D candidate 20

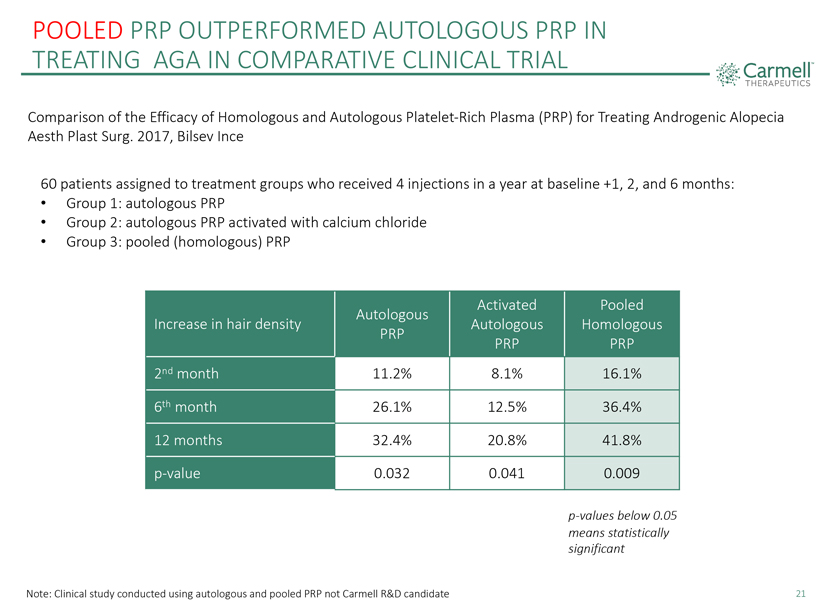

POOLED PRP OUTPERFORMED AUTOLOGOUS PRP IN TREATING AGA IN COMPARATIVE CLINICAL TRIAL Carmell ™THERAPEUTICS Comparison of the Efficacy of Homologous and Autologous Platelet-Rich Plasma (PRP) for Treating Androgenic Alopecia Aesth Plast Surg. 2017, Bilsev Ince 60 patients assigned to treatment groups who received 4 injections in a year at baseline +1, 2, and 6 months: • Group 1: autologous PRP • Group 2: autologous PRP activated with calcium chloride • Group 3: pooled (homologous) PRP Increase in hair density Autologous PRP Activated Autologous PRP Pooled Homologous PRP 2nd month 11.2% 8.1% 16.1% 6th month 26.1% 12.5% 36.4% 12 months 32.4% 20.8% 41.8% p-value 0.032 0.041 0.009 p-values below 0.05 means statistically significant Note: Clinical study conducted using autologous and pooled PRP not Carmell R&D candidate

orthopedic applications

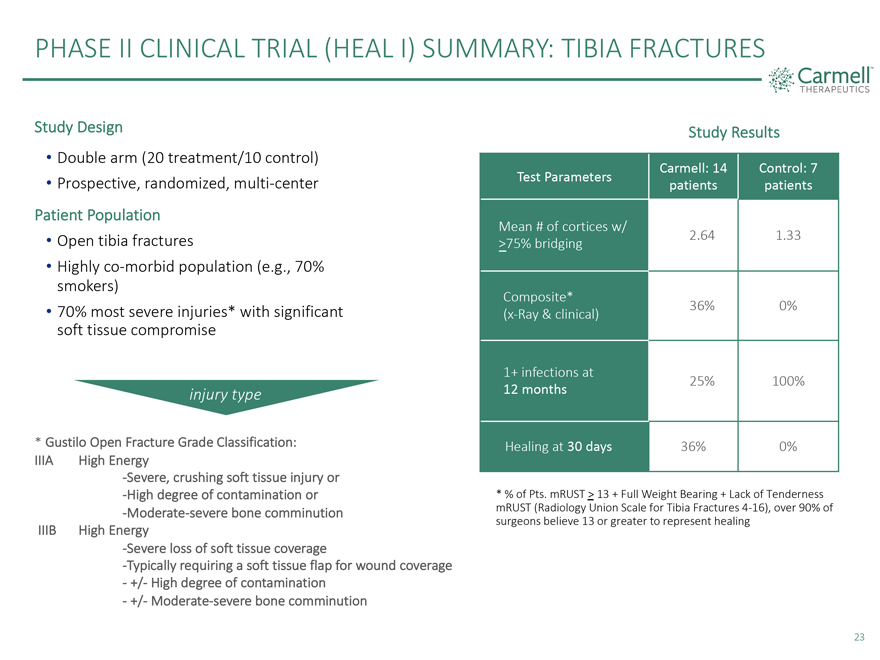

PHASE II CLINICAL TRIAL (HEAL I) SUMMARY: TIBIA FRACTURES Study Design Study Results • Double arm (20 treatment/10 control) Carmell: 14 Control: 7 • Prospective, randomized, multi-center Test Parameters patients patients Patient Population Mean # of cortices w/ • Open tibia fractures 2.64 1.33 >75% bridging • Highly co-morbid population (e.g., 70% smokers) Composite* • 70% most severe injuries* with significant 36% 0% soft tissue compromise (x-Ray & clinical) 1+ infections at 25% 100% injury type 12 months * Gustilo Open Fracture Grade Classification: Healing at 30 days 36% 0% IIIA High Energy -Severe, crushing soft tissue injury or -High degree of contamination or * % of Pts. mRUST > 13 + Full Weight Bearing + Lack of Tenderness -Moderate-severe bone comminution mRUST (Radiology Union Scale for Tibia Fractures 4-16), over 90% of surgeons believe 13 or greater to represent healing IIIB High Energy -Severe loss of soft tissue coverage -Typically requiring a soft tissue flap for wound coverage—+/- High degree of contamination—+/- Moderate-severe bone comminution 23

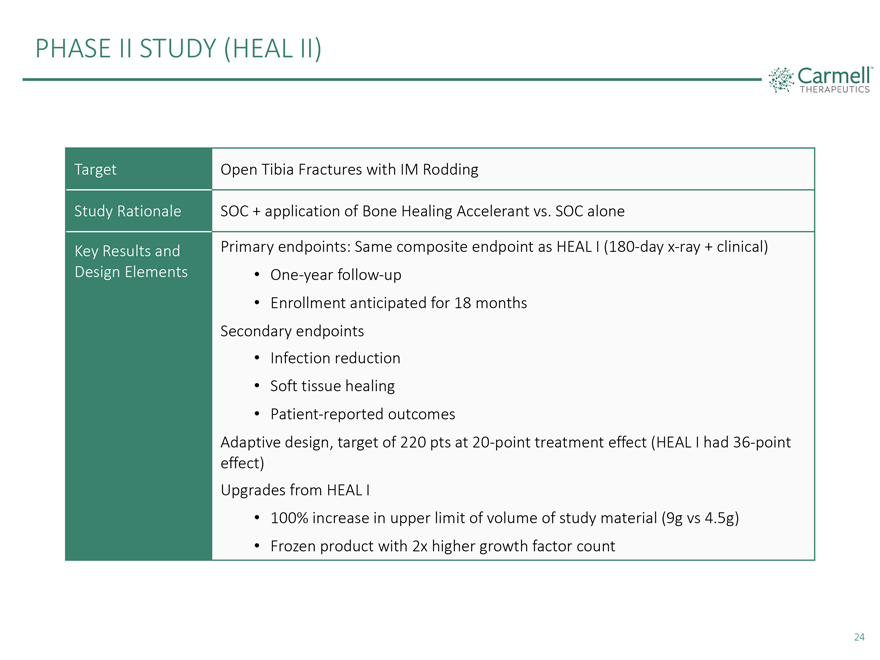

PHASE II STUDY (HEAL II) Target Open Tibia Fractures with IM Rodding Study Rationale SOC + application of Bone Healing Accelerant vs. SOC alone Key Results and Primary endpoints: Same composite endpoint as HEAL I (180-day x-ray + clinical) Design Elements • One-year follow-up • Enrollment anticipated for 18 months Secondary endpoints • Infection reduction • Soft tissue healing • Patient-reported outcomes Adaptive design, target of 220 pts at 20-point treatment effect (HEAL I had 36-point effect) Upgrades from HEAL I • 100% increase in upper limit of volume of study material (9g vs 4.5g) • Frozen product with 2x higher growth factor count 24

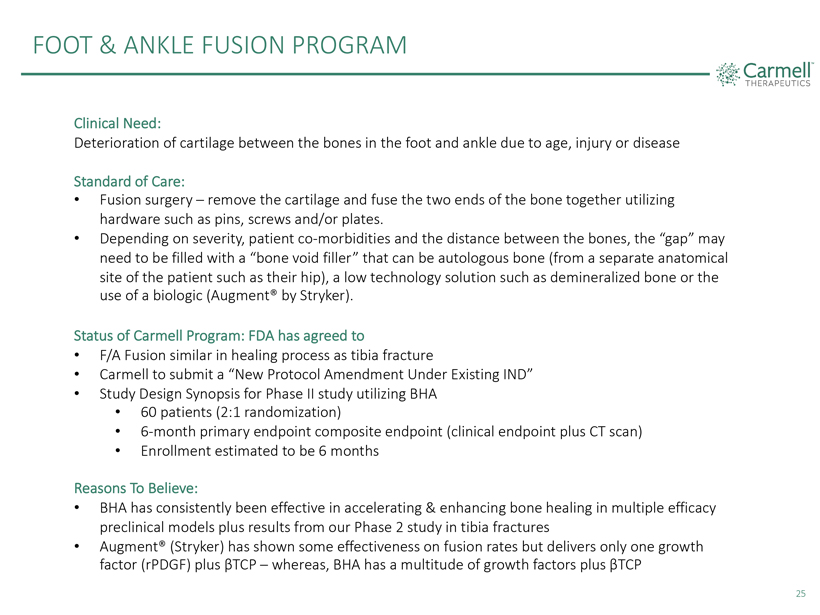

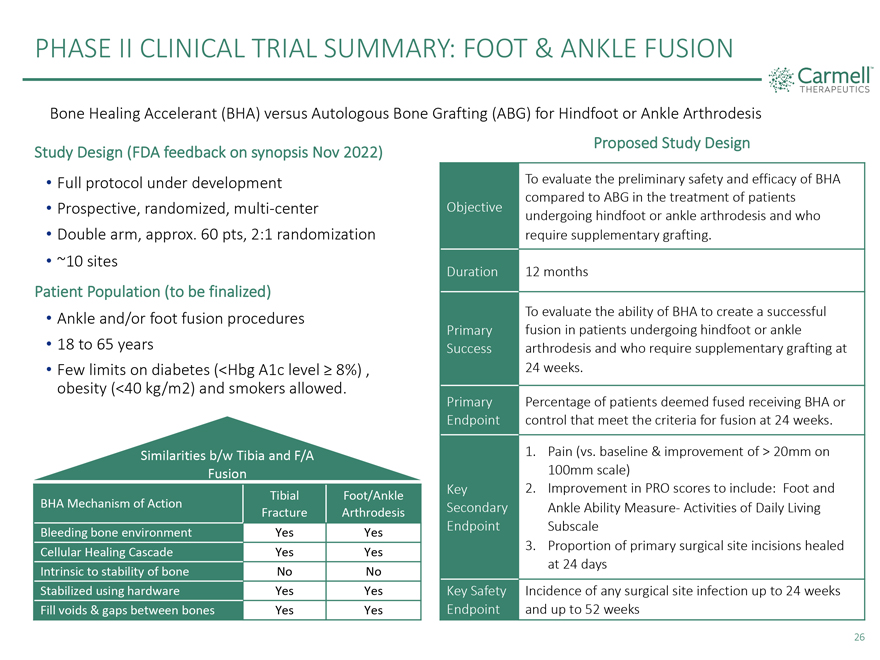

FOOT & ANKLE FUSION PROGRAM Clinical Need: Carmell ™THERAPEUTICS Deterioration of cartilage between the bones in the foot and ankle due to age, injury or disease Standard of Care: • Fusion surgery - remove the cartilage and fuse the two ends of the bone together utilizing hardware such as pins, screws and/or plates. • Depending on severity, patient co-morbidities and the distance between the bones, the “gap” may need to be filled with a “bone void filler” that can be autologous bone (from a separate anatomical site of the patient such as their hip), a low technology solution such as demineralized bone or the use of a biologic (Augment® by Stryker). Status of Carmell Program: FDA has agreed to • F/A Fusion similar in healing process as tibia fracture • Carmell to submit a “New Protocol Amendment Under Existing IND” • Study Design Synopsis for Phase II study utilizing BHA • 60 patients (2:1 randomization) • 6-month primary endpoint composite endpoint (clinical endpoint plus CT scan) • Enrollment estimated to be 6 months Reasons To Believe: • BHA has consistently been effective in accelerating & enhancing bone healing in multiple efficacy preclinical models plus results from our Phase 2 study in tibia fractures • Augment® (Stryker) has shown some effectiveness on fusion rates but delivers only one growth factor (rPDGF) plus ßTCP - whereas, BHA has a multitude of growth factors plus ßTCP

PHASE II CLINICAL TRIAL SUMMARY: FOOT & ANKLE FUSION Bone Healing Accelerant (BHA) versus Autologous Bone Grafting (ABG) for Hindfoot or Ankle Arthrodesis Proposed Study Design Study Design (FDA feedback on synopsis Nov 2022) • Full protocol under development To evaluate the preliminary safety and efficacy of BHA compared to ABG in the treatment of patients • Prospective, randomized, multi-center Objective undergoing hindfoot or ankle arthrodesis and who • Double arm, approx. 60 pts, 2:1 randomization require supplementary grafting. • ~10 sites Duration 12 months Patient Population (to be finalized) • Ankle and/or foot fusion procedures To evaluate the ability of BHA to create a successful Primary fusion in patients undergoing hindfoot or ankle • 18 to 65 years Success arthrodesis and who require supplementary grafting at • Few limits on diabetes (<Hbg A1c level ≥ 8%) , 24 weeks. obesity (<40 kg/m2) and smokers allowed. Primary Percentage of patients deemed fused receiving BHA or Endpoint control that meet the criteria for fusion at 24 weeks. Similarities b/w Tibia and F/A 1. Pain (vs. baseline & improvement of > 20mm on Fusion 100mm scale) Key 2. Improvement in PRO scores to include: Foot and Tibial Foot/Ankle BHA Mechanism of Action Secondary Ankle Ability Measure- Activities of Daily Living Fracture Arthrodesis Endpoint Subscale Bleeding bone environment Yes Yes 3. Proportion of primary surgical site incisions healed Cellular Healing Cascade Yes Yes at 24 days Intrinsic to stability of bone No No Stabilized using hardware Yes Yes Key Safety Incidence of any surgical site infection up to 24 weeks Fill voids & gaps between bones Yes Yes Endpoint and up to 52 weeks 26

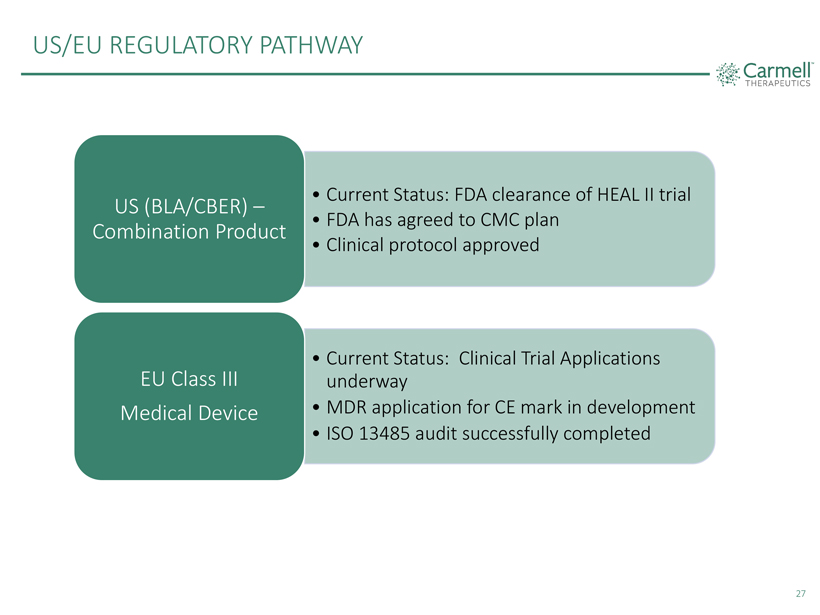

US/EU REGULATORY PATHWAY

• Current Status:

FDA clearance of HEAL II trial

US (BLA/CBER) –

• FDA has agreed to

CMC plan

Combination Product

• Clinical protocol approved

EU Class III • Current Status: Clinical Trial Applications underway Medical Device • MDR application for CE mark in development

• ISO 13485 audit successfully completed

27

TRANSACTION OVERVIEW 28

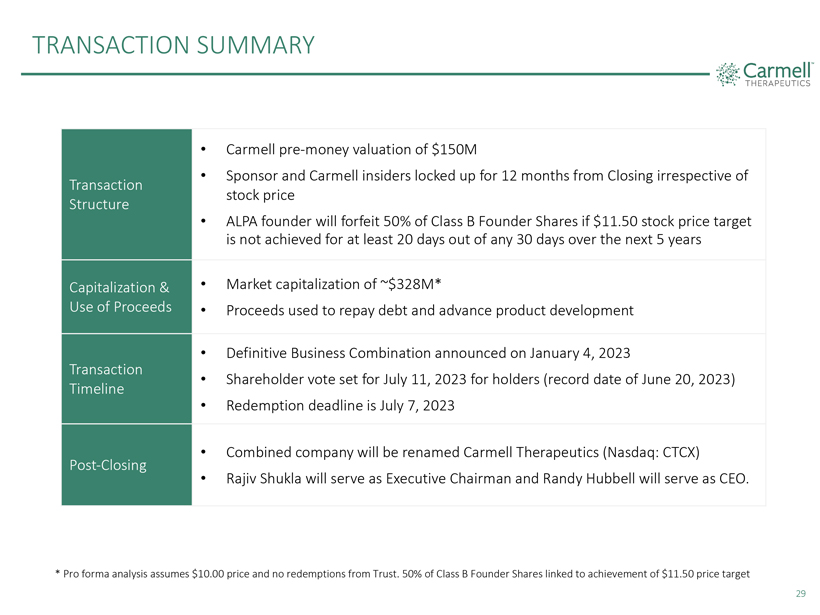

TRANSACTION SUMMARY

Transaction Structure

Capitalization & Use of Proceeds

Transaction Timeline

Post-Closing

Carmell pre-money valuation of $150M

Sponsor and Carmell insiders locked up for 12 months from Closing irrespective of stock price

ALPA founder will forfeit 50% of Class B Founder Shares if $11.50 stock price target is not achieved for at least 20 days out of any 30 days over the next 5 years

Market capitalization of ~$328M*

Proceeds used to repay debt and advance product development

Definitive Business Combination announced on January 4, 2023

Shareholder

vote set for July 11, 2023 for holders (record date of June 20, 2023)

Redemption deadline is July 7, 2023

Combined company will be renamed Carmell Therapeutics (Nasdaq: CTCX)

Rajiv Shukla will serve

as Executive Chairman and Randy Hubbell will serve as CEO.

* Pro forma analysis assumes $10.00 price and no redemptions from Trust. 50% of Class B Founder

Shares linked to achievement of $11.50 price target

29

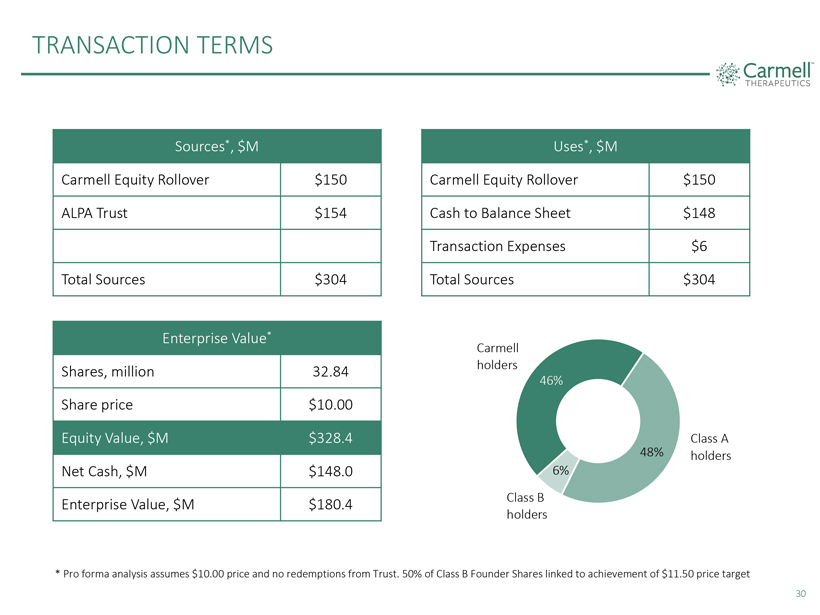

TRANSACTION TERMS

Sources*, $M

Carmell Equity Rollover $150 ALPA Trust $154

Total Sources $304

Uses*, $M

Carmell Equity Rollover $150 Cash to Balance Sheet $148 Transaction Expenses $6

Total Sources $304

Enterprise Value*

Shares, million 32.84 Share price $10.00

Equity Value, $M $328.4 Net Cash, $M $148.0 Enterprise Value, $M $180.4

Carmell holders 46%

Class A 48% holders 6% Class B holders

* Pro forma analysis assumes $10.00 price and

no redemptions from Trust. 50% of Class B Founder Shares linked to achievement of $11.50 price target

30

DISCLAIMER

This presentation

(“Presentation”) is for informational purposes only to assist interested parties in making their own evaluation with respect to the proposed business combination (the “Business Combination”) between Alpha Healthcare Acquisition

Corp. III (“ALPA”) and Carmell Therapeutics (the “Company”). The information contained herein does not purport to be all-inclusive and none of ALPA and the Company nor any of their

respective affiliates nor any of its or their control persons, officers, directors, employees or representatives makes any representation or warranty, express or implied, as to the accuracy, completeness or reliability of the information contained

in this Presentation. You should consult your own counsel and tax and financial advisors as to legal and related matters concerning the matters described herein, and, by accepting this Presentation, you confirm that you are not relying upon the

information contained herein to make any decision. The reader shall not rely upon any statement, representation or warranty made by any other person, firm or corporation in making its investment or decision to invest in the Company. None of ALPA or

the Company nor any of their respective affiliates nor any of its or their control persons, officers, directors, employees or representatives, shall be liable to the reader for any information set forth herein or any action taken or not taken by any

reader, including any investment in shares of ALPA or the Company. Certain information contained in this Presentation relates to or is based on studies, publications, surveys and the Company’s own internal estimates and research. In addition,

all of the market data included in this Presentation involves a number of assumptions and limitations, and there can be no guarantee as to the accuracy or reliability of such assumptions. Finally, while the Company believes its internal research is

reliable, such research has not been verified by any independent source. This meeting and any information communicated at this meeting (including this Presentation) are strictly confidential and should not be discussed outside your organization.

Forward-Looking Statements. Certain statements in this Presentation may be considered forward-looking statements. Forward-looking statements generally relate to

future events or ALPA’s or the Company’s future financial or operating performance. For example, statements concerning the following include forward-looking statements: the success, cost and timing of product development activities,

including timing of initiation, completion and data readouts for clinical trials; the potential attributes and benefits of product candidates, including in comparison to other products on the market for the same or similar indications; ability to

compete with other companies currently marketing or engaged in the development of treatments for relevant indications; the size and growth potential of the markets for product candidates and ability to serve those markets; the rate and degree of

market acceptance of product candidates, if approved; the potential pricing of product candidates, if approved; the proceeds of the Business Combination and the Company’s expected cash runway; and the potential effects of the Business

Combination on the Company. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expect”, “intend”, “will”, “estimate”,

“anticipate”, “believe”, “predict”, “potential” or “continue”, or the negatives of these terms or variations of them or similar terminology. Such forward-looking statements are subject to risks,

uncertainties, and other factors which could cause actual results to differ materially from those expressed or implied by such forward looking statements. These forward-looking statements are based upon estimates and assumptions that, while

considered reasonable by ALPA and its management, and the Company and its management, as the case may be, are inherently uncertain. New risks and uncertainties may emerge from time to time, and it is not possible to predict all risks and

uncertainties. Factors that may cause actual results to differ materially from current expectations include, but are not limited to, various factors beyond management’s control including general economic conditions and other risks,

uncertainties and factors set forth in the section entitled “Risk Factors” and “Cautionary Note Regarding Forward- Looking Statements” in ALPA’s final prospectus relating to its initial public offering, dated July 27,

2021, and other filings with the Securities and Exchange Commission (SEC), as well as factors associated with companies, such as the Company, that are engaged in clinical trials in the biopharma industry, including uncertainty in the timing or

results of clinical trials and receipt of regulatory approvals for product candidates, and in the healthcare industry, including the impact of the COVID-19 pandemic; competition in the healthcare industry;

inability to recruit or retain a sufficient number of patients or physicians and other employees; changes to federal and state healthcare laws and regulations; changes to reimbursement rates; overall business and economic conditions affecting the

healthcare industry, including conditions pertaining to health plans and payors; failure to develop new technology and products, if approved; and security breaches, loss of data or other disruptions. Nothing in this Presentation should be regarded

as a representation by any person that the forward-looking statements set forth herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved. You should not place undue reliance on forward-

looking statements in this Presentation, which speak only as of the date they are made and are qualified in their entirety by reference to the cautionary statements herein. Except as required by law, neither ALPA nor the Company undertakes any duty

to update these forward-looking statements. This Presentation contains certain financial forecast information of the Company. Such financial forecast information constitutes forward-looking information and is for illustrative purposes only and

should not be relied upon as necessarily being indicative of future results. The assumptions and estimates underlying such financial forecast information are inherently uncertain and are subject to a wide variety of significant business, economic,

competitive and other risks and uncertainties. See “Forward-Looking Statements” above. Actual results may differ materially from the results contemplated by the financial forecast information contained in this Presentation, and the

inclusion of such information in this Presentation should not be regarded as a representation by any person that the results reflected in such forecasts will be achieved.

Additional Information. This Presentation does not contain all the information that should be considered concerning the proposed Business Combination and is not intended to form

the basis of any investment decision or any other decision in respect of the Business Combination. ALPA’s shareholders and other interested persons are advised to read the definitive proxy statement/prospectus and other documents filed in

connection with the proposed Business Combination, as these materials contain important information about the Company, ALPA and the Business Combination. The definitive proxy statement/prospectus and other relevant materials for the proposed

Business Combination were mailed to shareholders of ALPA on June 27, 2023. Shareholders can obtain copies of the definitive proxy statement/prospectus and other documents filed with the SEC, without charge, at the SEC’s website at

www.sec.gov, or by directing a request to: ALPA Healthcare Acquisition Corp. III, 1177 Avenue of the Americas, 5th Floor New York, New York 10036.

Participants in

the Solicitation. ALPA, the Company and their respective directors and executive officers may be deemed participants in the solicitation of proxies from ALPA’s shareholders with respect to the proposed Business Combination. A list of the names

of ALPA’s directors and executive officers and a description of their interests in ALPA is contained in ALPA’s final prospectus relating to its initial public offering, dated July 27, 2021, which was filed with the SEC and is

available free of charge at the SEC’s web site at www.sec.gov, or by directing a request to ALPA Healthcare Acquisition Corp, 1177 Avenue of the Americas, 5th Floor New York, New York 10036. Additional information regarding the interests of the

participants in the solicitation of proxies from ALPA’s shareholders with respect to the proposed Business Combination is contained in the proxy statement/prospectus for the proposed Business Combination.

No Offer or Solicitation. This communication is for informational purposes only and does not constitute, or form a part of, an offer to sell or the solicitation of an offer to sell

or an offer to buy or the solicitation of an offer to buy any securities, and there shall be no sale of securities, in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the

securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended, and otherwise in accordance with applicable law.

31

Exhibit 99.2

Kristina: Live from NASDAQ’s MarketSite. I’m your host, Kristina Ayanian, and joining me today is Chairman and CEO of the Alpha Healthcare SPACs, Rajiv Shukla. Rajiv, thank you so much for joining us.

Rajiv: Thanks for having me. Kristina.

Kristina: Let’s talk about your background. You have over 25 years, an extensive period of time in M&A. Talk a little about your investment strategy and how you got started in this space.

Rajiv: Well, I got my start at Pfizer, the mothership of Pharma. At the time of my leaving, I was running global M&A for their R&D division. So, I really cut my teeth on acquisitions there. And then, further learned the trade at Morgan Stanley and Citibank where I did hedge fund and private equity investing. There’s really no one investment style. You have to tailor your approach to the market. So, for instance, in the current market environment, investors are not very keen on companies that don’t have profitability or at least a near term path to profitability. And the reason for that is simple—equity capital is scarce, debt is expensive. So, companies that don’t need either debt or equity are better placed. However, before this, when market conditions were much more healthy, investors would favor companies that are potentially very high risk, high reward kind of plays. But I’d say the current market environment favors companies that have a near term path to profitability.

Kristina: Have you always focused on healthcare?

Rajiv: I’ve always been a healthcare man. I had a brief stint outside of healthcare running a defense company but that was really a chance for me to test my corporate finance skills, uh, and restructuring skills. But healthcare through and through.

Kristina: Talk to me about your pending acquisition. How does that fit in and align with your overall strategy and mission?

Rajiv: So, one of the most exciting things in medicine is regenerative medicine. And the theme of regeneration is being applied across all aspects of medicine. Even cancer medicine, for example, has gone from chemotherapy, which is using extremely toxic chemicals to using immunotherapy, which is using your own body’s immune system to help you. The same thing is now happening in other sectors, which are much more complex sectors like orthopedics, bone healing, or soft tissue healing, the skin and, and other soft organs. And that’s the space that the company we are acquiring is in. It’s called Carmell Therapeutics. Carmell is a name derived from Carnegie Mellon; that’s where the technology comes from. And what Carmell can do is it can create an allogeneic version of platelet rich plasma. PRP has been around for a long time. It’s something that has a lot of clinical data. It’s been shown to work very successfully in all kinds of healing. The problem is all PRP currently in the market is autologous. Autologous, meaning the blood is drawn from the patient and then the platelets are put back into the same patient. What we are able to do is we are able to make a universal allogeneic version of PRP - the product is still in clinical trials, so it still remains to be seen whether it will make it to market…we believe it will, based on the phase two data we’ve seen, but just to caution viewers that it is still very much in clinical trials. Now, what does allogeneic PRP do versus autologous PRP? It’s like handwriting the Bible versus printing it on the Gutenberg press. So, the, the possibility of doing something at mass scale versus handmade is enormous, and that’s what Carmelll has.

Kristina: At the same time, are you offering personalized solutions at the mass scale?

Rajiv: Actually, that’s a very good question. We are personalizing the formulation design. So, we can make PRP in the form of sheets which can be applied as a protective barrier on the skin if one has burns, for example. It can be applied as a screw. We can formulate the PRP as a screw that goes into your bone (because as you know, sometimes you have these terrible fractures and you need to put in steel screws)…you can put in one of our screws instead, which will heal the bone and then dissolve instead of leaving a steel implant there.

Kristina: That’s incredible. So, your solutions, your universal and personalized solutions are offering permanent solutions for your patients?

Rajiv: The idea behind regenerative medicine is that the body takes over and that you do not need to use a crutch forever. So that’s the idea behind it.

Kristina: That’s incredible. What are you most excited for with this acquisition?

Rajiv: You always back the jockeys in every investment opportunity. This is no exception. This is a great Company. It’s run by an exceptional team of former J&J leaders. The J&J team is excellent. They’ve got tremendous backgrounds. The team is run by Randy Hubbell, who is a very experienced commercial leader in the MedTech space. So, I’m most excited about the team and the therapeutic indications that this Company is going after. We have phase two data, meaning we’ve tested this in humans and found efficacy. What we’ve seen is that in the case of tibia fracture (tibia is the bone between your knee and the ankle)…if one breaks that bone, that’s a load bearing bone that you put all your weight on. We’ve seen that by using our product, we saw faster healing of the bone and much lower infections because these are terrible fractures. You get awful infections along with the break. So, we’ve seen that. So that’s a very exciting product, but there’s another product that we’re going after. You know, there is an investment theme to bet on – “Vice and Vanity”. We are going to be betting on vanity with this Company—where we are looking to cure or treat, at least. alopecia (baldness). You’ve just seen this recent announcement by Pfizer for alopecia areata, which is an autoimmune disorder impacting very young people. But for male pattern baldness (folks who get baldness at an older age), or even women who get it because of hormonal changes, there really is not a whole lot one can do besides minoxidil. We’ve done clinical work in humans. These are not with our product, but with PRP - where we’ve seen tremendous results up to 40% increase in hair follicles and an increase in the thickness of the hair as well. So, we are very excited about the idea of bringing hair back.

Kristina: That would be great.

Rajiv: Broadly we will focus this Company on orthopedics (where our strategy will be to develop products and then out license them or partner them with large MedTech companies) and in the aesthetics space, we will build ourselves into a leader. In fact, we’ve announced a non-binding LOI this morning with another company, which will help us extend into the aesthetic space much more quickly and effectively.

Kristina: talk to us about that acquisition. What is that second company and how is that going to help the business?

Rajiv: Before I talk about the second company, I want to be very clear that the deal is at a LOI stage. And as with all deals, unless the deal is signed, sealed and delivered, one should never bet on them. The reason we announced that transaction is because we believe we have tremendous alignment with the owners of the company. They want what we want. The first thing that’s interesting about this company is that it’s in the same space that Carmell is in. It’s a regen medicine company. And, it has very effective products. This company is a commercial stage company. In the last 12 months, they’ve done $50 million plus of revenue and $5 million or so of EBITDA. They should do a lot better than that this year in both revenue and EBITDA based on how they’re doing thus far. So, it’s a high growth company. It’s in a synergistic space as Carmell, and it has certain products that they have also tested in alopecia and in aesthetics. We are very excited about that. Our strategy will be (it depends on finding the right deals and the right market conditions) to go out and acquire commercial stage businesses in aesthetics and rapidly build up a company in that space. There isn’t a whole lot of competition in this space, unlike Pharma or MedTech where you have very large established players. In aesthetics, maybe you have 3-4 companies at best and a lot of those companies have now been acquired by conglomerates, where the conglomerate is much more focused on pharma than aesthetics. So, we feel that there’s an opportunity here, if you favor chess parlance, to attack the undefended square. So, going after therapeutics is of course a very high risk, high reward play so we’ll just use a business development strategy on that front.

Kristina: You are definitely transforming lives in that sense. And it’s a new space, so it’s exciting to see everything that you’re developing and will continue to develop as well. You’re staying on as Chairman of the new entity? Is this strategic?

Rajiv: Yes. Usually SPAC sponsors are deal makers. My background is in private equity…I’ve been, on 14 boards, I’ve done 45 investments…I don’t tend to stay on with all of these assets. You tend to stay on the Board. But in this Company given the chemistry with the Team and the opportunity set, I’m staying on as Executive Chairman. I’m going to drive a very heavy business development and M&A agenda. I’m going to try and use my investor relationships to help the Company grow. Our goal goals are quite ambitious. We don’t want to guide the Street, but we have very ambitious goals set for ourselves. All of us, myself included, are locked up for 12 months after the deal is closed - the Carmell Insiders and us. So, no matter what the stock price is, we will not be able to sell, nor do we want to sell. In fact, I haven’t sold a single share of my previous transaction which was done over two years ago, given how bullish I am on the Company. So yeah, I intend to stay on and back this Company.

Kristina: You’re definitely unlocking new possibilities in healthcare, that’s for sure. Well, what’s next?

Rajiv: I think for now, I intend to focus on building Carmell into an aesthetics leader worldwide. I might do some transactions outside of Carmell. But, really my goal is to focus on building Carmell into something spectacular.

Kristina: Thank you so much for sharing your story and joining us.We look forward to welcoming you back to celebrate.

Rajiv: I’ll be back.

1 Year Alpha Healthcare Acquisi... Chart |

1 Month Alpha Healthcare Acquisi... Chart |

It looks like you are not logged in. Click the button below to log in and keep track of your recent history.

Support: +44 (0) 203 8794 460 | support@advfn.com

By accessing the services available at ADVFN you are agreeing to be bound by ADVFN's Terms & Conditions

Hot Features

Hot Features